Prime Minister Christopher Luxon says, if re-elected next year, the National Party will increase KiwiSaver default contribution rates to 12% by 2032, matching Australia.

Here's National's announcement.

National to lift KiwiSaver contributions

A National Government elected next year will ensure Kiwis are more financially secure in retirement by gradually increasing KiwiSaver contributions to match Australia’s 12 per cent rate, National Leader Christopher Luxon says.

“Financial security for retired people comes through home ownership and supplementing New Zealand Superannuation with long-term savings. KiwiSaver supports both of those, so National will strengthen it further,” Mr Luxon says.

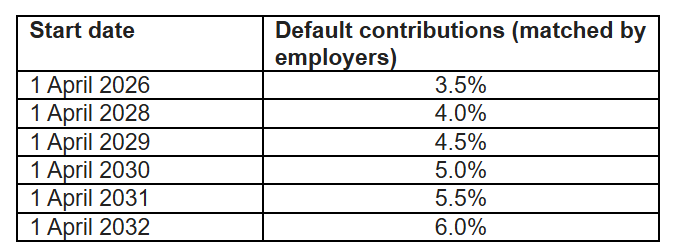

“In Government, we are already lifting the default rate of KiwiSaver contributions for employers and employees from 3 per cent to 4 per cent by 1 April 2028.

“But even after those changes, KiwiSaver contributions would be much lower than the equivalent scheme in Australia. For Kiwis working in New Zealand, that means smaller KiwiSaver balances and less financial security than friends or family working and saving in Brisbane, Sydney or Melbourne.

“Smaller retirement balances present a challenge for New Zealand as a whole, too, as we rely more on investment from offshore to fund the infrastructure, start-ups, and housing we need to grow our economy, create jobs and lift incomes.

“If we’re serious about building the future, and I am, it’s time to aim higher.”

If elected next year, National will continue to increase default contribution rates by 0.5 per cent from 1 April 2029, rising by 0.5 per cent a year until 1 April 2032, to achieve a 6 per cent contribution each from employers and employees.

That will mean a combined rate of 12 per cent by 2032, matching Australia.

“For a 21-year-old earning $65,000 a year today, these changes would mean they retire with a KiwiSaver balance of around $1.4 million, around $400,000 more than they would have with the Budget 2025 contribution settings,” Mr Luxon says.

“If you’re a New Zealander who does the right thing by working hard and saving for the future, you deserve to get ahead. National backs you every step of the way.”

And here's a KiwiSaver fact sheet released by National.

12 Comments

Feels a bit misleading being that they've combined employer and employer contribution and comparing it to the Australian minimum employer contribution number, and that they're campaigning for something that isn't even in the next term

They do make increases next term. No government will change super in one term, for example if they change the retirement age they need to do it slowly or give plenty of notice. Same with making employers pay 6%, can’t force it on them overnight.

So, while a necessary, obvious & long overdue change, employees & employers will ultimately result in an additional 6% wage/salary cost...sounds a bit inflationary?

Deferred consumption via investment in a portfolio of shares and equity is not the answer to our challenges. What a weird world.

Exactly. In times of financial struggle, most voters will see it as another reduction in weekly income. They're looking for more money in their pockets over the short term, not less.

I strongly support the urgent need to move to a robust and sustainable superannuation saving scheme, and yes, the Australian scheme seems to provide a good model.

However, I strongly oppose National’s policy announcement, even if the policy survives collation agreements, its longevity is only while National remains the government. We have a history of previous schemes - such as KiwiSaver and Superannuation funds - being severely eroded with change of government.

The Retirement Commission has called to ‘Stop piecemeal policy change’ such as this proposal. The Commission calls for a 10-year roadmap and long-term political accord with all major parties following the release of its review of retirement income policies. This was reported by Interest.co on 14th November.

While each party continues to campaign on its own superannuation proposal we will not have a robust and sustainable scheme nor confidence in saving for retirement.

What’s the long term goal? Does someone who contributes 12% all their life still get NZ super too? If so that seems like quite a high compulsory savings rate when NZ super already takes care of your basic costs. If they want to get rid of NZ super, then please tell us in advance! What is the friggen plan?

In Aussie super is means tested, so I suspect in NZ in time it will be as well. After all it's a gold standard system in aussie.

When will they tell us this news? Hey remember how you opted into KiwiSaver and saved your own money, well now we aren’t giving you NZ super, we’re only giving it to the people who didn’t save.

People saving for retirement need to know what the deal is now. Which generation is the last to get NZ super? Is the means testing on assets or income? Etc.

Let’s say you save 12% all your life, you would retire with a pretty decent sum. Even someone on min wage is probably going to be a millionaire.

Are the working population at that time going to be happy to also pay you NZ super? Basically this policy would be the end of NZ super, National also need to decide when that will occur and how so we all know.

Something more meaningful might be to stop taxing contributions on the way in, but tax them when they are used - the way the sensible countries do it - as it allows balances to grow faster.

But that would require deferred returns for government, which is exactly what they are asking for from the public.

It's also going to mean top ups for low wage earners to stand some chance of being equitable and to save enough for a dignified retirement. I don't have a problem with that, but it's not being talked about.

Stop using it to fuel the housing ponzi.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.