The Reserve Bank says a publicity campaign promoting its Dashboard initiative will focus on ordinary depositors as it strives to encourage them to exert more influence over banks' behaviour.

The Reserve Bank outlines this in its Regulatory Impact Statement for the dashboard approach to quarterly bank disclosure. This was posted on the central bank's website on Friday afternoon along with other information on the Dashboard.

By increasing accessibility of banks' disclosure information for users, the Reserve Bank says the Dashboard will potentially broaden the range of market participants who exert 'market discipline.'

"A communications strategy that will accompany the Dashboard's introduction will help in this regard, with a focus on ordinary depositors who are currently only weakly exerting such influence over banks' behaviour. It is hoped that this set of stakeholders will better understand the financial position of their bank and make more informed financial decisions," the Reserve Bank says.

"This is particularly important since the Reserve Bank operates a non-zero failure regime, and where a proportion of depositor funds are potentially subject to loss in the event that their bank fails and is liquidated or resolved using the Open Bank Resolution (OBR) policy."

'The Dashboard may contribute to an improvement in financial literacy'

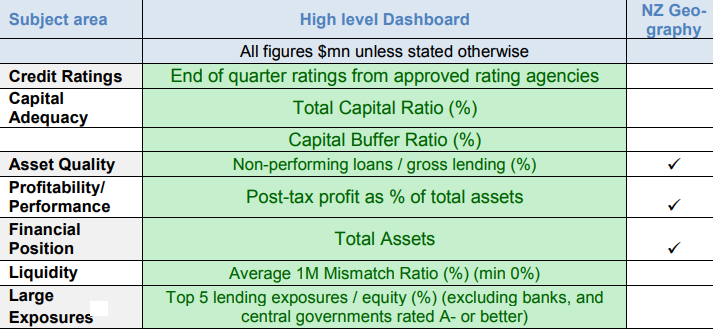

The Reserve Bank wants the Dashboard to make it easier for people, including bank depositors, to assess the financial stability of banks by improving the disclosure and accessibility of key financial information. The Reserve Bank says the Dashboard should provide greater transparency about banks' financial health and performance, making for better informed investors who will help promote a sound and efficient financial system. (See more on background to the Dashboard here).

The Dashboard will allow users to make "side-by-side comparisons of banks in an apples-with-apples scenario" on seven key subject areas. The seven are credit ratings, capital adequacy, asset quality, profitability, the balance sheet, liquidity, and credit concentrations. The introduction of the Dashboard from late May on the Reserve Bank's website means banks will only have to publish disclosure statements twice yearly instead of quarterly. Dashboard content will come from banks' private reporting to the Reserve Bank.

"The Dashboard may contribute to an improvement in financial literacy, particularly for those groups of stakeholders who currently only exert a low level of market discipline on registered banks, such as ordinary depositors. The effect of this is uncertain and will depend on the outcomes and success of the communications strategy the Reserve Bank will develop to accompany the launch of the Dashboard," the Reserve Bank says.

"The focus initially will be on raising awareness among the media and general public prior to introduction, followed by engagement with other key stakeholders and broader education efforts post-implementation."

As the Reserve Bank puts it, information contained in banks' general disclosure statements is to some degree not standardised in either content or layout. This in part is due to flexibility allowed by accounting standards, and also by banks having different reporting dates.

'This was a dream, I don't know why we thought it'

The Reserve Bank's efforts to get more "ma and pa" retail investors, many of whom have a reputation for not looking beyond the interest rate they'll be paid, to dig into bank disclosure detail will be interesting to observe. David Mayes, University of Auckland professor of banking and financial institutions and a former chief manager and chief economist at the Reserve Bank, has an interesting perspective on the introduction of the current disclosure statement regime in 1996.

"I was in the Reserve Bank when we set up the current scheme and we thought that disclosure documents would actually be read by somebody. This was a dream. I don't know why we thought it," Mayes has said.

Today's Reserve Bank staff will be hoping things turn out differently this time around.

Meanwhile, the Reserve Bank is pushing ahead with plans for banks to publish liquidity ratios on the Dashboard despite opposition from the banks themselves to this concept. However, it has made a concession by agreeing the liquidity ratios will be included within the scope of banks' existing auditor review of their capital adequacy information rather than being subject to a "positive assurance" form of audit opinion. The existing auditor review of capital adequacy information is covered by a "negative" assurance option.

Note, the Dashboard will only apply to locally-incorporated banks. These include key retail banks such as ANZ, ASB, BNZ, Kiwibank and Westpac.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

33 Comments

in short NO, joe public has the perception that a BANK is the safest place to put your money and you are not "investing " your deposit when you put it in the bank

Apparently Kiwis want term deposits in their Kiwisaver. The perception of what an investment is in NZ is broken.

Banks aren;t safe.HOUSING is.

Clearly not someone who's experienced living in an earthquake or leaky building zone. Houses are only as financially secure as the relevant insurance company.

Totally correct. The average Joe cabbage has swallowed the propaganda of the last 100 years or so that the banks were the only place where your money would be safe. What they didn't wake up to, was that at the same time the banks were lobbying governments to quietly change the rules which meant that depositing YOUR hard earned money in a bank was actually GIVING it to them with no guarantee of it being returned.

This, IMO is a fundamental betrayal of the people by their governments. The huge profits that banks report are not earned, but money stolen from ordinary working stiffs. If a situation arises that means an OBR will be acted upon and the people realised just how badly they have been manipulated and lied to, it will be politicians as well as bankers who will be burned at the stake.

Sorry, but that is an inaccurate, uninformed rant. Yes, banking can be criticised. Myself, I see excessive leverage as a real problem. But decsending into conspriacy and drawing untrue and silly conclusions is just not reasoned comment. Please base critiques on something more than bile.

Really David? Through my schooling it was exactly what i was taught. I was shocked to learn only relatively recently that the money i had put in the bank was not actually mine, and that i effectively had no security in it as legally i was an unsecured creditor. And worse i have little come back on the bank if through their practices my money is lost. That the banks under stress can legally take part (possibly to all) of my money under the OBR 'Haircut' provisions to cover their loses, rather than being liable for the quality of their practices, and have to take active measures to protect my money that they want from me to put to work.

More to the point if i asked the bank to agree to terms and conditions for the use of my money, that i would have to agree to if i borrowed from them I would be politely and brusquely shown the door! This relationship is completely one sided for the ordinary man on the street as from that perspective every bank is the same. We do not have a great deal of spare money by the bank's standard, but what little we do have is exceedingly important to us because it represents far too much sweat.

When you say that my comment is inaccurate are you saying the reported profits do not include the deposits in their accounts (I do understand that there will be a balancing liability on the ledger)?

More to the point today there is the common perception that we expect the government to protect protect us by providing a taxpayer funded guarantee. i would much prefer to see legislation put in place that make my money mine, not the bank's when i deposit it, and that the banks are liable to safeguard it, which is the exact purpose of it. Other wise what is the alternative - the mattress?

Your comment is far from an uninformed rant. It is why wealthy German families like to keep some gold in a vault in Switzerland. Why Indian dowries are in gold and silver.

The only comment I would make is that the current system is a result of collusion between banks and governments, as the special interests of banks, government employees and politicians seem to align. It doesn't need a conspiracy, so its not a conspiracy theory.

Paper money systems are not very durable. There have been at least 50 instances of severe inflationary episodes in the last 100 years in different countries where the value of the currency was destroyed.

Sir Isaac Newton actually designed the most recent successful monetary system, the one that led to the Industrial Revolution in Britain and gave birth to the modern world. It lasted from 1700 to 1931.

For a more in depth study, this chap seems to know more than most:

http://www.24hgold.com/english/news-gold-silver-detractors-of-adam-smit…

https://en.wikipedia.org/wiki/List_of_countries_by_inflation_rate

The IPTF's notes from the 16 May 2017 meeting are now available and state the following view of the Task Force:

Countries with three-year cumulative inflation rates exceeding 100%:

South Sudan Ukraine Venezuela

Countries where the three-year cumulative inflation rates had exceeded 100% in recent years:

Malawi Sudan

Countries (a) with projected three-year cumulative inflation rates greater than 100%; (b) with projected three-year cumulative inflation rates between 70% and 100%; (c) where the last known three-year cumulative inflation rates previously exceeded 100% and current actual inflation data has not been obtained; or (d) with a significant increase in inflation during the current period

Argentina Libya Suriname Angola Yemen Egypt Mozambique

The report also notes that there may be additional countries with three-year cumulative inflation rates exceeding 100% or that should be monitored which are not included in the above analysis because the sources used to compile the list do not include inflation data for all countries or current inflation data. An example cited is Syria.

https://www.iasplus.com/en/news/2017/08/hyperinflationary-economies-upd…

Several of these currently hyperinflationary countries have larger economies than New Zealand.

Your comment is far from an uninformed rant. It is why wealthy German families like to keep some gold in a vault in Switzerland. Why Indian dowries are in gold and silver.

And Japanese in post office savings and Vietnamese also in gold.

Sorry, but that is an inaccurate, uninformed rant. Yes, banking can be criticised. Myself, I see excessive leverage as a real problem.

Inaccurate and uninformed? Perhaps, but he's no more uninformed that elected politicians who have no understanding how money is lent into existence. You then proceed to allude to the consequences (excessive leverage) of the retail banks' monopolistic power and privilege.

Then take your money out, you are free to do so.

Then take your money out, you are free to do so.

Yes and no. You're free to take your money out of a bank, but the banks have the monopoly. If the serfs don't play the game, then you're not going to get any favors from them. I say that as I have no debts with any NZ banks, yet in terms of cash and term deposits, I would be in the top quintile in terms of cash savings. The reality is that a punter who lives paycheck to paycheck with a cool million in loans is of of far more value to them.

easy to say hard to do, not many companies will pay you in cash now let alone government departments, without a bank history you wont have a credit history or very limited one making finance very hard to obtain.

unless you run a cash only enterprise you are pretty much forced to funnel your funds through a bank

You're right murray86.

When you "deposit" money in a bank, you give it to them, it's no longer yours, you become an insecured creditor.

Same with a bank loan, the bank does not lend out money from other deposits, it creates this money out of nothing and charges you interest for it.

Read this powerpoint by Prof. Werner

http://www.actuaries.org/LIBRARY/Presentations/2014/WERNER_Intl_Actuari…

and do watch this video:

https://www.youtube.com/watch?v=EC0G7pY4wRE

a) If you dont like the profits being earned and teh risks move your money elsewhere.

b) Then people are blind to history at the very least if not stupid. There is no and never was any guarantee in any investment I am aware of that money will be returned. On the plus side an OBR event is not likely to be without any warning. It would I expect come after a severe collapsing economy and house prices losses made banks in-solvent. The Q then is not to worry about an OBR but to worry where you can put your $s to avoid the OBR "costs"

c) "it will be politicians as well as bankers who will be burned at the stake." indeed possible but not for the OBR event but the major causes of it.

There is no and never was any guarantee in any investment I am aware of that money will be returned.

There are implicit guarantees, but nothing like in Australia where deposits are guaranteed up to AUD250K.

Oh how i long for those two magic words''''secured debenture'''.

Without accurate reliable information on Banks Capital Ratio and the value of assets not already pledged elsewhere (Covered Bonds etc) providing the value of free assets actually available to depositors the dashboard is little more than a partial view of a Banks soundness. Changing behaviour is more problematic as suggestions etc are easily disregarded especially as such suggestions will not be visible to the public and removing deposits whilst effective if done by enough but may well precipitate the very thing the RBNZ is trying to avoid.

Are you one of the people who actually read the General Disclosure Statements? (ANZ's Sep-17 one ran to 86 pages.) They are very detailed. You can find a lot of valuable information in them.

If you are, you are a very rare bank depositor (disclosure: I am one of them).

But most people don't, even those that know how to read such documents. The Dashboard will surprise you. It is a much better way to explore the data in those GDS's and I hope many more people will do that.

But the GDS's aren't disappearing. They will only not be required for off-quarter statements. It's the best of both world's. This is no conspiracy - it is the RBNZ doing its job to get more people looking at vital transparency.

But the GDS's aren't disappearing. They will only not be required for off-quarter statements. It's the best of both world's. This is no conspiracy - it is the RBNZ doing its job to get more people looking at vital transparency.

As long as it doesn't spook the populace. That is part of the RNNZ's (and the retail banks) role. To allay any fears

I have to admit trying to describe pertinent points from a GDS to others flies right over their heads and many do not make past the first page rather they rely on stereotypical information & what their family tells them. I had a few legal friends in contract specialisations who admitted they often don't even look. But then you might be interested to know that it is more related to a known neurological feature where the human brain will skip over information to proceed, much like terms of use, disclosures, security information, even resorting to simplified pattern matching in day to day tasks so unexpected things get missed. The research is backed up by a few studies and is accepted scientifically (in tech industries has been a cause for many jokes for a while, in legal industries it has been used for customer detriment, often it is a known issue but many cannot act against it).

I agree having the RBNZ work on better ways to convey more information to consumers who might not find it easy to digest, (or have the time), to begin with is good. However like scientific communication issues it may need to have a lot more pomp and ceremony to even come into the sphere of public perception and education. Other sources of information and myths are far easier to come across and far more exciting in presentation. The RBNZ is in competition with social media, blogs, news, youtube, reddit, apps, tv shows & movies, ads... I really wish them the best because this is important information to know and parse. It being difficult to parse has been an issue for a long time. Working to fix the issue it better for the NZ public financial health overall and we certainly have the technology to do so. Perhaps we are not at Chin family level yet but it is a start https://www.thechinfamily.hk/web/en/

(I have to admit I love the cat used in the videos, icons and graphics... but that is because I am a geek and the internet runs on cats https://www.thechinfamily.hk/web/en/about-the-chin-family/characters/in…).

David Chaston,

"I hope many more people will do that". I think you are dreaming,to paraphrase a previous statement. Given the woeful state of financial literacy,just how many depositors will look at the Dashboard and of those who do,how many will be able to make sense of say,the credit ratings from the 3 agencies?

How will they differentiate between a Moodys rating from a Fitch rating? Just how well will they be able to 'read' the capital adequacy ratios?

In my brief submission on the proposed dashboard,I said that without a sustained and well publicised information campaign,this will be useless.

I challenge you to do a survey in say a local pub. Explain that the Australian banks have deposit insurance of $250,000 per individual in Australia,while the same banks here would be subject to OBR and see what the reaction is. I suggest that virtually none will know what OBR is and will be unimpressed when you tell them.

Thank you David for telling me about the GDS I didn't even know existed, I have Googled this and read the BNZ 2002 & 2006 GDS which do contain a lot of information but doesn't inform me of the level of risk if any BNZ takes in its business that would adversely my deposit with them. If the dashboard is as good as you reckon and does improve my understanding of Banks actual risk exposure then the dashboard will be a welcome addition especially if its existence becomes well know - perhaps a link on deposit statement as GDS/Dashboard updates are published will help. I appreciate you are knowledgeable in this area whilst most depositers are not so cut us a little slack and help us understand what the information means.

Thanks for publicising this information David. I'm a bank depositor and guilty of not reading the GDS's. As nervous as I am about the security of my bank deposits, I suspect that I'm like a lot of other people and only look at the banks credit rating, which is once over lightly to say the least. Hopefully the dashboard will help me become somewhat better informed.

I am not sure it matters. The problem is the monolithic nature of the banks business/lending models, ie they are all broadly in the same game with similar %s in the various sectors the only difference is the name out front Then consider that the entire economy is highly interlocked. Can any sector collapse and not take others with it? I dont think so myself.

So which bank do you put your money with? well since they are all pretty similar and you would get warnings I think it doesnt matter that much.

PS you are right to be worried, long term this game of grow for ever in a finite planet isnt sustainable.

It's what banks don't disclose thats the problem

http://www.newser.com/story/127362/bank-of-america-didnt-disclose-aig-l…

What the Dashboard will not tell you:

- extent of reckless lending at high DTI, interest only loans, etc.

- the woeful inadequacy of capital requirements regulation

- internal incentives for loan growth that leads to accounting control fraud by internal managers

This all shows up as loan growth that exceeds growth in incomes that has been apparent for some time, leading ultimately to a crisis and bailouts by either taxpayers or depositors (via OBR)

Yes, and more importantly, it will not educate NZers on the basic premise that loans are not back by deposits.

Is there anyone naive enough to believe that?

Yes, and according to Mervyn King, the majority of politicians in the UK govt didn't know this fact. Therefore, would you expect NZ MPs and the Waynes and Bettys to be any better informed?

Agree wont cover everything but its a good start into the murky world of record profits. Once its up and running then banks can be compelled to add additional measurements. I wonder if there will be a penalty for lying on your disclosure....?

Average man - record profits ? - do you mean higher than in the past - name me good businesses that don’t plan that, and name me shareholders who don’t expect their dividends to rise to new levels - name me good businesses that over time don’t grow their profits to new levels - name me a bank you’d want to put your money into that is making falling profit (other than Kiwibank)......

Will the dashboard make a difference? No!

Why?

1. No one knows about it. So Interest are running stories on it (as are some other financial websites). Is it leading news on any of the mass market media?

2. No one can do anything about it. All the banks are functionally the same (to the point some would say colluding)

3. Education. Although you disagree even though you are "Technically" Correct. The public have no idea how a bank works. No one outside of the industry would ever say they are "investing" in a bank. They are simply a function of society. Try get paid? Trade? Pay tax? etc... without one.

If an OBR were to ever happen, it would be the end of all banks. Joe Public loses his money in Bank A, you can bet your bottom dollar, every one of his friends and family will pull the cash from their own banks just in case.

But this isn't really a problem is it, after all they are just an "investment" not the backbone of the modern financial system.

Noncents,

I agree. This is just a fig leaf,so that if the worst happens,they can say,but look at all the information on our Dashboard-it's not our fault. Yea right.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.