By Gareth Vaughan

When a member of the Reserve Bank's senior management team describes a new proposal as "a holy grail we've been searching for" it's definitely something worth taking a look at.

This is how Toby Fiennes, the Reserve Bank's head of prudential supervision, described a proposed new ‘dashboard’ approach to disclosure for New Zealand incorporated banks at a recent briefing with journalists.

"What we're trying to do is design something that's far simpler and more accessible that people can get their heads around. It's a holy grail that we've been searching for for a while and it's difficult. And it does depend upon people actually wanting to look at the information. But I think it's very important that the public are fully informed about the relative risk of the banks, the banking sector," Fiennes said.

Asked why the Reserve Bank is doing this, Fiennes said the proposal is primarily aimed at boosting market discipline, and thus financial stability.

"To stimulate more interest from depositors or their advisers in the banks, and the relative safety of the different banks in New Zealand. If banks know they're more under scrutiny from the market, they're going to be keener to be safe and show that they're safe," Fiennes said.

As at the end of October, NZ dollar household deposits stood at $156.2 billion.

Household deposits

Select chart tabs

Innovative

As Victoria University's Martien Lubberink noted in this interest.co.nz article the dashboard proposal is an innovative one. And disclosure information on banks made available to the public, especially those who deposit money with the banks, should be easily accessible and simple to understand.

The dashboard plan stems from a broad review the Reserve Bank has done of its regulatory regime for banks. This included looking at the disclosure regime, which is topped currently by the requirement for banks to issue quarterly general disclosure statements. Whilst full of crunchy detail, these complex and dense disclosure statements are about as accessible to the average depositor as the planet Mars.

As University of Auckland professor of banking and finance and former Reserve Bank chief economist David Mayes said: "I was in the Reserve Bank when we set up the current scheme and we thought that disclosure documents would actually be read by somebody. This was a dream. I don't know why we thought it."

Although the average depositor, often focused on little more than the interest rate they're being offered, may not read disclosure statements, the statements do, however, present a rich vein of information for the likes of us at interest.co.nz, academics, sophisticated depositors and banks' rivals. Thus the Reserve Bank's proposal, which will see the quarterly disclosure statement requirement cut to twice a year, is not insignificant. Banks will be required to supply the Reserve Bank with the dashboard information quarterly, with the regulator ultimately wanting it up within a month of a bank's reporting date.

Incidentally, the Reserve Bank estimates halving banks' annual requirement to publish disclosure statements from four to two will save big banks about $200,000 a year each.

So what is it?

Just what is this so-called dashboard approach to bank disclosure? Below is an explanation from the Reserve Bank's consultation paper. (Consultation is open until December 15, with the Reserve Bank aiming to reveal final decisions in the first quarter of 2017).

The Dashboard would provide a side-by-side comparison of individual locally incorporated banks, according to key metrics, hosted on the Reserve Bank’s website and updated quarterly. We believe that the Dashboard approach would enhance market discipline by presenting individual bank data in a more accessible and comparable way. This data would be largely drawn from information locally incorporated banks will report to us privately and therefore achieve efficiencies for these banks by allowing their public disclosures to leverage off data they already privately report.

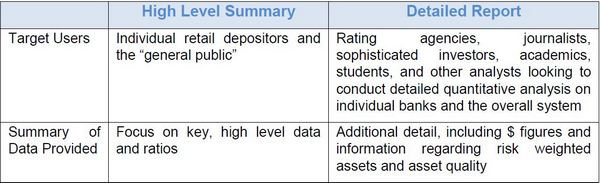

The consultation paper proposes to include in the Dashboard credit ratings, key financial performance and position information, capital, asset quality and liquidity information, and potentially a metric comparing information on large credit exposures. We are currently proposing to present the data on the Dashboard in two formats: a “High Level Summary” and a “Detailed Report.” We are also proposing to provide enhanced explanatory material on some of the matters being disclosed on the Dashboard. (This would just aim to explain certain core concepts like capital ratios, rather than provide commentary on data relating to specific banks).

We believe the Dashboard will broadly meet and, in many respects exceed, international standards for quarterly capital and asset quality disclosure by banks. We also consider that the Dashboard will be an innovative way of enhancing disclosure and market discipline. Because of the relatively small number of locally incorporated banks in the New Zealand system, it is possible to see all banks side by side, either all together or in peer groups. We believe this offers a greater opportunity to compare institutions and to bolster market discipline, one that would be more difficult in a market with a much larger number of participants.

The Dashboard also has the potential to result in material efficiency gains for locally incorporated banks by allowing them to use material prepared for private reporting to the Bank as the basis of the information that they publicly disclose. We recognise that the extent of these efficiency gains is substantially influenced by the nature of the sign-off or assurance process that this information is subject to once it is publicly disclosed.

In terms of the two levels of dashboard information, as noted above, one features "high level information" aimed at a general audience, and the second features "detailed information" for those wanting more. The two levels of information are demonstrated in the table from the Reserve Bank's consultation paper below.

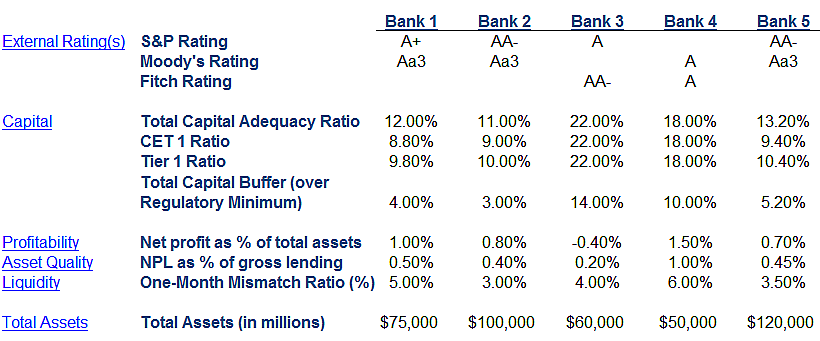

And below is an example of a proposed high level dashboard table.

No deposit insurance in NZ

A crucial point to remember in terms of why bank disclosure is especially important in New Zealand is because this country is an outlier among Organisation for Economic Co-operation and Development (OECD) members in that we don't have deposit insurance or a deposit guarantee scheme. Frighteningly, the fact that NZ bank deposits are not guaranteed by either the Government or the banks is news to many people, as this 2014 Financial Markets Authority survey demonstrated.

Here's Auckland University's Mayes making the case for deposit insurance in a video interview, and here's me doing the same in an opinion article here. Others to raise concerns are credit rating agencies S&P Global Ratings and Fitch Ratings.

S&P has said the lack of a deposit insurance scheme puts NZ in a relative weaker position compared to other OECD countries, such as Australia, that have deposit insurance schemes in place.

"In our view, the absence of a deposit insurance scheme heightens the risk of a run on the banking system," S&P has said.

Fitch has suggested the lack of deposit insurance would likely see the big four banks - ANZ, ASB, BNZ and Westpac - benefit from a flight to quality in a time of market stress.

"...In supporting market discipline, we do not guarantee that no financial institution will fail, and we do not have explicit customer protection. While the New Zealand financial system is sound, history tells us that banks, NBDTs [non-bank deposit takers] and insurers can, and do, fail. Consequently, depositors and policyholders - both wholesale and retail - may suffer losses. Our mandate is soundness and efficiency of the financial system as a whole. The growth and demise of individual institutions in accordance with the competence of their management and demand for their services are a natural part of a competitive and efficient economy," Fiennes has said.

"Since no financial institution is guaranteed by the government, there is more market pressure on institutions to compete on safety than there would be in a system with guarantees," said Fiennes.

We do have the OBR...

NZ does, of course have the Reserve Bank's Open Bank Resolution (OBR) Policy, a potential tool the Government could use - if a bank failed - as an alternative to a liquidation or taxpayer funded bailout that would keep a bank open for business. See how it would work, if used, here in: If a bank failed and the Open Bank Resolution Policy was implemented, how would it affect bank depositors, bondholders and shareholders?

Below is what the Reserve Bank says about its OBR policy in its dashboard consultation paper.

The regulatory framework in New Zealand stresses market discipline and is not a “zero-failure” model. Disclosure is a key element that supports this framework, and significantly scaling it back would be inconsistent with this approach. In this context we note that depositors in New Zealand are not covered by a deposit insurance scheme, and if their bank becomes insolvent and is subject to Open Bank Resolution (OBR) they may lose part of their deposits. A key benefit of OBR is that it provides authorities with the ability to impose losses on creditors without closing the bank. We believe this supports market discipline and improves incentives for investors and larger depositors to monitor banks. However, for this monitoring to be effective it is essential that relevant information is disclosed to the market on a frequent basis.

If and when the OBR would actually be used on a flailing or failing bank is a good question. If one or more of the big four Australian owned banks was in trouble it's easy to imagine the phone calls from Canberra, Melbourne and Sydney to Wellington demanding NZ government action. And it's easy to imagine a government worried about retaining the support of thousands of bank depositors and other customers who are also voters, and wanting to shore up the broader economy, throwing taxpayers' money at a troubled bank. The words 'too big to fail' come to mind.

In my view OBR would most likely actually be put into action if one of the country's smaller banks struck serious troubles, that were isolated to just that bank. But even then a taxpayer funded bailout cannot be ruled out.

How do you know when a bank's in trouble?

At the media briefing Fiennes and his colleagues were asked whether the Reserve Bank has modelled the information planned to be included in its dashboard against real bank failures to see whether this information would have raised the alarm that a certain bank was about to fall over. The answer was no.

"Bank failures are correlated with capital in the sense that the more capital there is the less likely there is going to be a bank failure. But it isn't a perfect match because there could be all sorts of things that are hidden. And bank failures can happen very quickly," said Fiennes.

"It [the dashboard information] does show the relative resilience of the banks. So a bank with more capital and more liquidity is, other things being equal, going to be more resilient and therefore safer than one with lower levels."

The consultation paper notes the Reserve Bank views capital as "the single most critical piece of information in assessing financial stability," with a bank’s capital ratio indicating its ability to "withstand a range of risks, including credit risk, liquidity risk and operational risk."

(Here's a useful Reserve Bank article on banking crises from NZ's past, and here's a Treasury working paper on putting a price on the risk of bank failure).

A key point with the data banks will be required to provide for the dashboard is that the Reserve Bank is proposing that there'll be no specific liability regime for false or misleading disclosures on the dashboard itself. Asked about this Fiennes said the Reserve Bank expects to see a "good and robust" process for verifying the information internally at the banks. And within one month of the dashboard coming out in two of the four quarters there will be a full disclosure statement from the banks, which will be audited.

The Reserve Bank is also proposing to keep a log of breaches by banks of their conditions of bank registration on its website. Currently these are disclosed in the general disclosure statements.

Publicity campaign possible

Given the importance, albeit un-sexy nature, of the Reserve Bank's planned changes to bank disclosure rules, Fiennes said there is some discussion of running some sort of public education campaign.

"We've talked about that. Formally we haven't decided where we're going to land on it yet. There's obviously a range of things we could do. it's a bit of chicken and egg, we need to get it out and show them [the public] what it looks like," Fiennes said.

Option B

Given that, at this stage, the dashboard proposal is merely a proposal albeit the regulator's strongly preferred option, the Reserve Bank has a back up plan. The consultation paper also features "Option B," or "a Pillar 3 approach." This option would "provide essential information on capital and asset quality, plus liquidity, and would help to still meet international standards on disclosure. "Option B is our 'fall-back' option, should the Dashboard not prove feasible," the Reserve Bank says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

19 Comments

So, RBNZ are out to increase the reporting bank's profits by $200K.

And they want the public to be "fully informed" so that when a bank fails they can say to the public "we told you so".

How will I know what the dashboard of a bank in distress looks like?

Will this dashboard become my home page?

I think I will borrow money and invest in property - at least I can have some control over that!

A depositors exposure to a bank depends more on how they lend than what their capital is.

The effects of easy lending are for all to see in the state of the real estate market and credit growth.

However the Dashboard will not tell you which bank has been the most reckless in its lending until the downturn comes.

It seems to me that the magical 'dashboard' is a tremendous cop out by the RBNZ, If there are some key indicators to differentiate stability and safety of specific banks then the RBNZ should be regulating to insure financial stability as a prime aspect of their duty of care for NZ depositors.

To leave it up to depositors to do this for them is ludicrous in my opinion.

As Fiennes himself says: "Bank failures are correlated with capital in the sense that the more capital there is the less likely there is going to be a bank failure. But it isn't a perfect match because there could be all sorts of things that are hidden. And bank failures can happen very quickly,"

Dear RBNZ,

Wake up. The dashboard is a joke.

Joe Average will not be able to fully understand this or reduce it down to a risk level for themselves.

It is also insane that the near safest form of investment carries such high risk levels.

Deposit insurance should be implemented like almost all other OECD countries and Government bonds should be available to Joe Average through the banks in small trances with the banks taking a tiny % of the bond coupon rate as admin fee.

I disagree. I think the dashboard idea will be of real value to many, many more people than the old general disclosure statements. Plus they will enable many more people to compare institutions and the risks they face in a meaningful way.

And I suspect it is an idea that will be picked up by other banking regulators around the world. Maybe not the exact Kiwi version, but in principle at least.

I also disagree about your deposit insurance idea. The only deposit insurance anywhere in the world is provided by the taxpayer. It is not real insurance. No real insurance company ever gets into this business, mainly because it is a terrible concept. It is only wanted by people who seek a free lunch on risk. That equates to a moral hazard, and the taxpayer backing up a moral hazard is a very bad idea.

The existance if moral hazards in other countries in not a good reason why we should make the same mistake here.

I agree - a dashboard, provided it has all the right info (not just that which the banks themselves are happy to disclose/report) would be a real advantage to both borrowers and savers. The higher risk taker banks are after all going to be the ones who lean harder and more ruthlessly on their debtors as well. So, both borrowers and depositors would find the info beneficial.

The risk of any lending institution failing I would say wouldn't even cross the mind of the average borrower.

Not their problem.

Most of NZ doesn't even know what the RBNZ does.

Sorry,

1) The dashboard will never tell Joe Average enough to make an informed decision. I dont disagree that the dashboard should exist, I disagree it will be meaningful for Joe Average.

2) Deposit insurance is generally limited to a maximum amount & does not give financial institutions unfetted rights to gamble, such as would be the case where the total deposit was covered.

3) It is totally absurd that someone can insure a house and car but cannot insure a bank deposit.

Mortgage backed Securitization is that not a form of Insurance.

David,

I have made a submission to the Bank on the Dashboard proposal. One of the points I made was that without a sustained public awareness and education campaign,it will fail. My own research,admittedly somewhat unscientific,strongly suggests that the level of knowledge on the current system-OBR- is woefully low,so just implementing a dashboard would by itself,achieve nothing.

The key metrics to be included will have to be understood by ordinary depositors for this to work and that will not be a simple task. Then,the information will have to be made easily available.I am far from convinced that this will achieve what it ostensibly sets out to do,but will allow the Bank/government to claim that they have done everything they reasonably could,should the proverbial ever hit the fan.

This risks backfiring,as there would be immense pressure(SCF?)for the government to intervene,in the event of a bank collapse.

Personally,I would like to see a deposit scheme implemented with say,a limit of $75,000 per person and I would be prepared to see a small reduction in my TD rates to help pay for it. I am not convinced that the moral hazard argument trumps the peace of mind that this would give to many ordinary depositors.

Although this dashboard may work for 5% of the population, I can't see it work for 95% of the population. Nobody has heard of credit rating agencies.

"many, many more people"

How many average Joes/Janes out there read the General Disclosure statements?

Now how many read it, and use it as a means of analysing whether or not they puts their cash in said bank?

Time and time again it has been shown that the average Kiwi does not actively change banks. Most people are still signed up to the original bank they joined as a Child.

Thinking a dashboard report will change the entrenched culture/habits of millions of Kiwis is just a daydream.

As for deposit insurance being a moral Hazard. A moral hazard is a "lack of incentive to guard against risk where one is protected from its consequences,"

A bank account, for all intensive purposes is compulsory. With out a bank account

- I cannot receive any form of Government assistance.

- I cannot pay or receive tax.

- I cannot be paid by the overwhelming majority of employers.

So in effect almost all funds entering my account do so whether I want them to or not.

Now, do I have an incentive to guard against risk? Yes, of course - I do not want my hard earned money dissapearing. So what can I do to mitigate the risk?

Answer: Nothing, legally once the funds are deposited they are not mine. It is completely impossible for me to control the bank in any way shape or form, short of being the majority shareholder.

I have no control at all over how the bank is funded, operated, or its exposure to risk

The only way to mitigate risk is to withdraw funds from the bank. Which depending on the bank, account type, or the amount. I may not be able to do without advanced notice.

"The existance if moral hazards in other countries in not a good reason why we should make the same mistake here."

Mistake? Good one, can you even imagine the catastrophe if you let the banks go under and watched every single Kiwi lose their cash. I know I would not want to be a Politician or banker when that happens.

Deposit insurance.

Leds do it like mortage insurance. But reverse the flows.

Eg. When a bank takes a deposit, it must offer deposit insurance, premium paid by said bank, in favour of the retail depositor.

Would this make the finance johnnies run?

Or give them.

Gareth: Frighteningly, the fact that NZ bank deposits are not guaranteed by either the Government or the banks is news to many people

I think that's a feature! Clearly it needs to be advertised more, but having the taxpayer on the hook for failed banks leads to bad incentives, both for banks and for account holders.

Just replying to myself: what about, every time you open a new account, you have to tick: I understand the taxpayer does not guarantee my deposits?

Not a bad idea, given neither the RBNZ nor the current government has shown any interest in introducing a deposit guarantee/insurance scheme.

dashboards are an admission that they allow risky or dodgy operators to flourish and plunder the unwary,that offer lifetime annuities and have a B rating,possibly for those with short life expectancies?goldbuyers,send your gold in an envelope and we will give you a quote!just be careful out there.

This, throwing more light on how brutal an OBR event could be., how's this for a de minimus.

Grant Spencer, deputy governor and head of financial stability, said there was scope for the minister to determine a minimum guaranteed repayment amount to protect small depositors, and the bank was having some discussion as to whether to fix that number more specifically, at around $5000.

What about if you happen to have a mortgage and also some deposits, apparently set off does not exist, your savings disappear but the loan remains.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.