People who have invested in the share market are more confident in New Zealand’s financial markets than those who have invested in the residential property market, according to a Financial Markets Authority (FMA) survey.

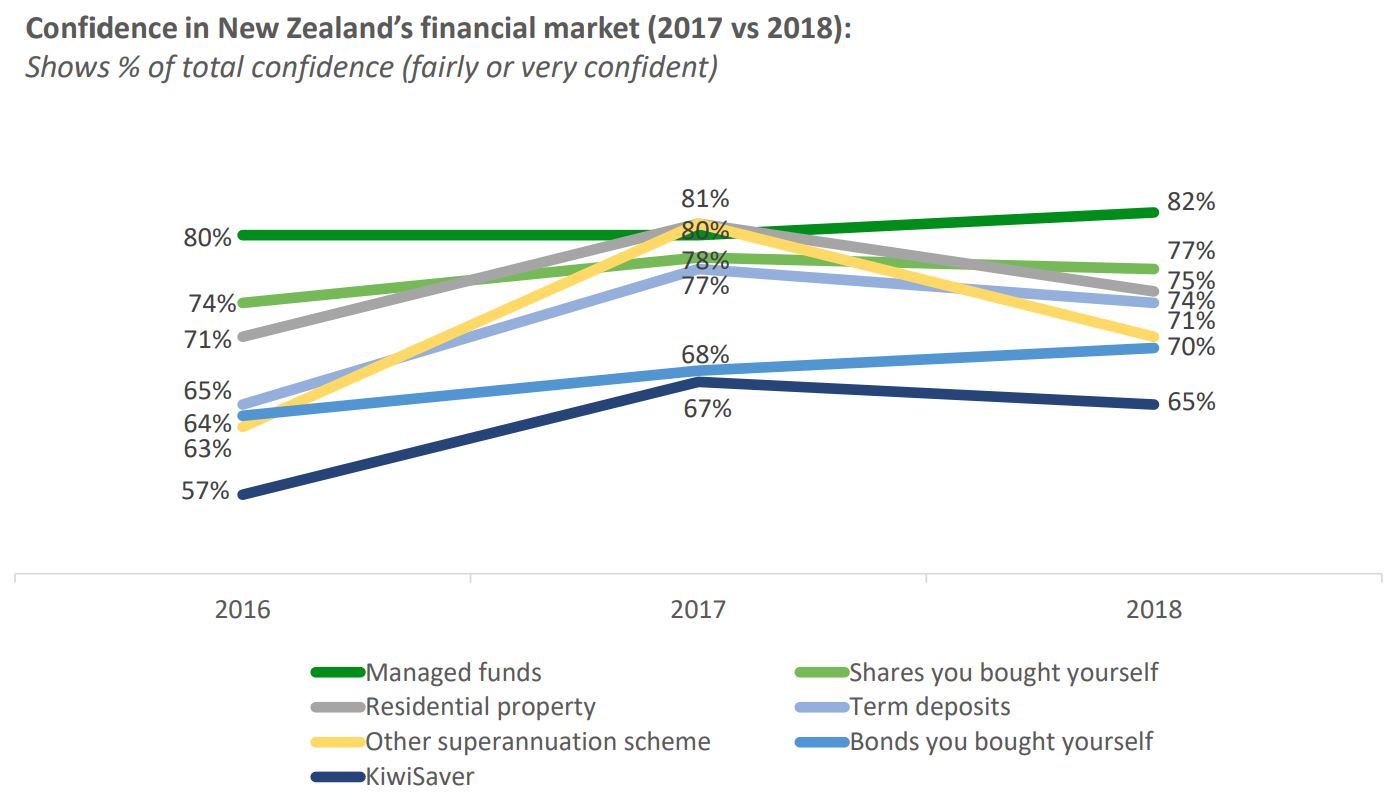

While 75% of property investors surveyed in May were confident in the market, 82% of people who had invested in managed funds and 77% of those who had invested in shares themselves were confident.

A year ago, property investors were as confident as those who had invested in managed funds, and even more confident than those who had invested in shares.

Confidence among property investors took a notable dip year-on-year, while confidence among equity market investors remained stable.

This is despite there being jitters in both the property and equity markets.

Market dynamics

The new Coalition Government is introducing a raft of new measures to cool the housing market. It’s upping supply through KiwiBuild, banning foreign buyers, extending the bright line test from two to five years, preventing investors from using rental property losses to get tax breaks and considering introducing other taxes like a capital gains tax.

The median Auckland house price has fallen off its peak reached in March 2017, according to Real Estate Institute of New Zealand figures.

Meanwhile, house prices across the country have been on the up, with the latest figures showing the median house price hitting a new high in May.

Sales volumes across the board are down.

Meanwhile global equity markets are volatile. Fears around the US/China trade war and the Federal Reserve raising interest rates faster than expected have largely contributed towards the VIX index spiking to its highest level since 2011.

While the Shanghai Composite has plummeted, the likes of the NZX 50 and S&P 500 have continued to perform well.

Asked whether the survey results show that New Zealanders are more sensitive to events that affect the property market than those that affect equity markets, FMA CEO Rob Everett pointed to the different philosophies different types of investors use.

“The [global market] backdrop looks dark, but actually on the ground here, it doesn’t feel like that’s manifested itself. I suspect that’s kept confidence levels in markets a little higher…

“Property’s difficult right. It’s quite a different investment approach. It’s much more physical, it’s much more tangible, it feels more real to people, which is I think part of the reason people like to put their money into something they can look at.

“The problem with property is that it’s not diversified. It’s very concentrated. It’s actually far more difficult to get some of your money out than it is in other types of investments.

“It’s actually a very different investment philosophy.

“There are still a lot of people in New Zealand putting money into term deposits and residential property, who probably just haven’t actively considered putting it into a market investment.”

KiwiSaver

Adding KiwiSaver investors to the mix, the FMA’s survey shows KiwiSaver investors are much less confident in New Zealand financial markets than any other type of investor.

For example, while 82% of managed fund investors have confidence in the market, only 65% of KiwiSaver investors have confidence.

Everett put this divide down to people investing in managed funds and shares being more involved in the investment decision than those who invest in KiwiSaver. Actively deciding to invest, rather than becoming an investor by default, they are likely to be more confident.

In fact, across the board, the FMA said: “Confidence is considerably higher among those who are more knowledgeable about investments and the risk associated with them...

“The more experienced investors who do not only have a KiwiSaver scheme are the most confident about New Zealand’s financial markets and its regulation.

“These investors are more likely to be male, aged 40 years and over, and earning higher personal and household income.

“On the other hand females and the younger age groups under 30 years are the least likely to have an investment and significantly less likely to follow the financial markets, and are therefore the least knowledgeable and confident.

“They are more likely to be noninvestors, or have only a KiwiSaver investment, and are more likely to say they don’t know enough to have an opinion on some of the topics asked.”

54 Comments

No surprises there.....

I do hope those invested in this boom sharemarket realize there will be a correction

It’s laughable the local Kiwi investment firms holding much more in cash for a reason

I feel sad for anyone late to the market sucked in by the current market heights and the claims it’s only going to

go higher and higher.

Didn’t Aucklands property market actually perform better than many others around the world during the GFC ?

No I don’t think property owners need to panic but sharemarket investors may wish to sell some stocks

I certainly wouldn't say a share market crash is impossible, but one advantage it has over the housing market is the Government is not actively taking steps to bring it under control and limit capital gains, or introducing new tax measures on shares. Nothing is risk free.

The S&P 500 and it's predecessors has averaged around 10% pa for the last 90+ years. That includes the great depression, WWII, and the 1970's malaise. Not too bad.

That is fine if an investor is willing to wait 90+ years before they need the funds - (typically inheritances, charities, institutional pension funds etc) If you're requiring the funds before then (such as for deposit to buy a house in a few years, potential retirees who may need funds to retire on, etc), then you need to consider market prices before you need the funds. If they're at risk of a large price fall and there is insufficient time for the value to recover to its current value, then it might be worthwhile reducing market risk exposures.

Think about employees who were about to retire in 2009 - 2011. Many portfolios with large equity market exposures would have fallen in value, and retirees would have needed to raise cash for retirement and been forced to sell at low market price levels. Some retirees discovered that they needed to keep working longer than planned. Retirees or near retirement employees with 5 years or less to retirement should assess market risk exposures if they have large equity market risk allocations.

.

CN - What would be your advice for the over 55's carrying mortgages on the family home that are in excess of $300,000?? Given that costs of funding in Australia are rising and that their banks are our banks...???

If you have a mortgage on your own house, no matter your age, pay it off as soon as you can

Nic Johnson,

Some things for you to consider.

Everyone has a unique set of circumstances surrounding :

1) financial position

2) liquidity needs,

3) investment objectives

4) time horizon,

5) tax considerations,

6) risk tolerance,

7) expected returns for different asset classes

One suggestion would be to determine estimated liquidity needs over the next 5 years - my personal preference is that this cash should be in capital protected investments so that you know the capital value is there when you need to liquidate them. Personally, I would not have this cash in equity investments (i.e company shares). This was really the key message to the point raised above.

From a purely financial perspective, another suggestion would be to stress test your own balance sheet to determine the impact on your net worth to see what you are willing to tolerate on the market risk exposure side based on your future expectation of returns for different asset classes that you own. Any leverage would magnify the impact of asset price falls on net worth, whilst any asset price gains would magnify the impact on net worth.

Personally, I would not want any market exposure to banks in Australia - if you're concerned about residential property prices, then look at what happened to the prices of banking stocks in Ireland in 2008/2009, or financial stocks in the US in 2008/2009. Given your UK experience, you might recall what happened to the price of UK bank stocks in 2008 / 2009.

So you're making the argument that shares are WORSE than property because of liquidity concerns?

Wow.

There is strange logic, and then there is this.

The point being made is more about value concerns for those needing near term liquidity who have that future liquidity currently invested in stock markets.

1) for those who think that there is going to be a significant property price fall in NZ in the next few years

2) and have a very large proportion of your assets (and percentage of net worth) in NZ shares

3) and believe that the NZ share market will take at least 5 years before recovering to current price levels

3) and if there are circumstances that require a need to sell these shares to raise cash within the next 5 years,

then one might want to reconsider the re-allocating that proportion invested in shares that one could expect to sell within the next 5 years for cash needs. If the property prices fall, then the NZ stock market may also fall, thereby depressing the value of the equity portfolio and one may be required raise cash and sell shares at lower price levels.

Let me illustrate with an example. Let's say a person needs 20,000 per year to use for living costs in retirement. This would mean total cash in the next 5 years to use to retire on would be 100,000 (5x 20,000 per year). And that this person has a current share portfolio with a total value of 300,000 (all in no or very low dividend yielding stocks). The 100,000 cash need would represent 33% of the portfolio if sold at current price levels. If the share market fell 20% (this would mean the share portfolio falls from 300,000 to 240,000 in market value), and did not fully recover until at least 5 years, then the person raising 100,000 in cash would then need to sell a larger proportion of their share portfolio (in this case 42% - 100,000 / 240,000). If the person is invested in higher dividend yielding shares, then this may offset the amount of the share portfolio that they might need to sell for cash needs. In fact, one of the possible equity reallocations could be to change the share mix from low dividend yielding shares to higher dividend yielding shares.

Any funds that are required after 10 years (i.e. a 10 year investment horizon) could remain invested in shares ...

I do hope those invested in this boom sharemarket realize there will be a correction

Of course. I'm in it for decades, not months. It's volatile, and I'm fully prepared to weather a hell of a financial storm without putting my livelihood in jeopardy.

How many property investors could weather an Irish style housing crash, I wonder?

.

Wait longer and buy the dip?

.

Pragmatist, glad you know what you are talking about, no wonder most people stay the hell out of the share market.

You don't need to know what he's talking about to do well in the share market, if you have plenty of time before you need the cash (>10 years or longer?) then buying an index and ignoring it until you need it is pretty hard to beat.

.

Pragmatist,

Just out of curiosity,

1) on which exchange are you buying put options?

2) and for what duration?

Most listed put options are with short maturities. The only listed long term put options that I'm aware of are LEAPS listed in the US.

The only other way to get long term maturity put options are in the OTC market, however that is only open to institutional investors due to premium sizes, and subject to counterparty credit risk.

.

How exactly do you hedge against a 20% drop in the housing market?

Difficult, given the lack of direct hedging securities available, and it can be expensive. The easiest and most cost effective solution is to reduce your gross portfolio exposure to real estate - i.e. sell.

If it is an investment property, then you could sell assuming you only had financial considerations.

That may be difficult if it is your home when non financial considerations come into play, such as financial peace of mind, school zoning, emotional attachment, wanting to pass on as an inheritance to children, not wanting to deal with landlords when renting, pets not allowed when renting, etc. In this instance, looking purely at financial considerations, one way to reduce gross exposure to real estate property prices may be to downsize and buy an owner occupier residence in the same area (that way reducing the gross portfolio exposure to a market price decline) - that is how John Key reduced his real estate exposure. This method allows you some real estate market exposure should property prices not fall, and if property prices rise, you get some upside - it reduces your cost of being wrong should property prices rise.

For owner occupiers, the other option is sell and to rent in the same area and deploy the sales proceeds elsewhere, or to hold onto the cash until opportunities arise.

.

Yes, markets go both up and down. If you believe in a company, buy their stock I guess.

this data set is skewed..

they forgot to survey the likes of BLSH, eco bird, TM2, dgz, chessmaster................

I was in Ireland in 2007/2008. I didn't see any share holders gleefully mocking housing fanatics.

When a major economic correction comes then everything is stuffed.

It just shows you how resilient property investors really are!

They know that they are sitting on an asset that is safe in the medium term despite this government trying to shaft the property investors big time.

The funny thing is that this government will be voted out at the next election due to them not have any ability whatsoever of being able to run a country.

Totally out of their depth in everything they do.

Grant Robertson and Winnie are sweating big time and have no answer to all the strikes that are coming.

TM2, "the funny thing is that this government will be voted out at the next election due to them not have any ability whatsoever of being able to run a country"

Is this your seriously uneducated opinion or a pining wish in order to protect your interests? Pick one

Gosh you are a crack up - "shaft the property investors big time" yes the Government is intent on doing this especially in CHCH were you guys are making too much dough and not paying your fair share of tax..be warned they are coming!!

here is some bedtime reading for you ...

https://www.landlords.co.nz/article/6504/tax-working-group-agrees-prope…

Ha ha, gosh that is hard headed and independent analysis, you are such a sweet naive old man, I do worry about you being left alone on these kinds of websites and swallowing this stuff hook line and sinker......so worried

opinion piece from a vested group arguing they still need to be favored in the current climate.

you have to take with a grain of salt,

good for a laugh thought that people still trot out the same proven untruths and believe them.

the tax laws were changed in during rogernomics to advantage house investors over OO so this is just plain wrong, i could sit her and try to example using figures why but that is a huge waste of time to one eyed vested groups that gain the advantage

"Just because a rental provider can claim expenses from their rental income does not make buying a property easier for them compared to a home buyer.

These tax laws have always been in place and therefore had nothing to do with home ownership rates falling since the 1990's. What did change in the early 1990's is that Government assistance for first home buyers was removed, a far more likely reason for a reduction in new home buyers"

lol, worry about yourself .. I am very safe and secure.

These websites provide info which your likes do not want to know about ... not to disturb your sweat naive dreams...

conclusion - Westpac are 'rubber ducked'

.

Don't forget the DTI to add to your woes, that's in the RBNZ armory as well, no more gorging on debt for you TM2.

Once the Government debt bond bubble pops capital will flee into stock markets..only a matter of time. Current data exposes the flow (or should that be flight) of capital from ailing Europe and emerging markets into the US $ and US equities for safety. The US has its own debt but compared to the rest of the world it is the best dirty shirt and will be the last to fall over.

https://www.armstrongeconomics.com/world-news/sovereign-debt-crisis/why…

"..The crisis we face globally is that as interest rates rise, the servicing of the debt will rise exponentially. This will impact everyone around the world. Now, if the US dollar rallies sharply because of the structural crisis in Europe and the turning down of the economies elsewhere, then the past debt of the USA will rise in real terms as was the case with Greece. Then add to this Cauldron and stir gently rising interest rates.

Shabam! You reach the threshold of a debt crisis!.."

https://www.armstrongeconomics.com/armstrongeconomics101/economics/the-…

When Equities typically decline, people run to the government bonds, and this we call the Flight to Quality...What nobody seems to be talking about is what happens when the crisis is confined to government? Is that when gold rises? But then what about stocks? When CONFIDENCE collapses in government, the Flight to Quality becomes the opposite of tradition sell equities and buy bonds."

Much higher interest rates coming soon - what will that do to NZ houses?

.

What happens when equities are the government" ie: the BoJ. You have to see this for what it is, a credit fueled asset bubble. when the bubble blows it will affect all assets that were artificially inflated by it.

Summertime,

I assume do know that the global bond market is much greater than the global equity market? Do you really believe that if there is a major bond sell-off,then much of that will go into equities? If so,I think you are delusional.

can you tell me when such an event has happened previously? I read the articles and they are,in my view useless-and badly written.

I read around this topic six months or so ago when Trump was rattling his sabres at Nth K and getting his tradewar wagon rolling, the flight to stockmarkets appears to be well underway in NZX at least, my holdings didn't even blink when the went ex div at y/e and have put on some serious weight since then.

To say that realestate is a better investment then shares or shares a better investment then bonds is a futile discussion. We / no one has a crystal ball to predict the outcome. A proper diversified portfolio with a mixture of different asset classes by far has proven to be the best strategy with an emphasis on yield /dividends/cash flow. The problem of course is many cannot afford to diversify with wealth tied up into 1 asset class and in this case realestate. Making bad decisions is part of life....blaming others for wrong decisions when they happen is just immature.

One wonders if the debt leverage team had been restrained with dti ten years ago would the nurses need such a catchup?

Wish we could just get on with the reset and get on with being able to survive in our own country and not be screwed over by international printed leverage. The big winner has been the banks shareholders.

Averageman. Not to detract from your well made point but investment in bank equity has not exactly been the 'big winner' you assert. I'm a well diversified share investor but my big Aussie bank shares have on a gross basis performed only modestly in the post GFC period, relative to many other holdings. Given the way the banks have recently attracted so much political interest I've seriously considered ditching them a number of times and may yet do so. I definitely would if calls from people like the erudite Mr Chaston for bank shareholders to stump up capital to fortify bank solvency ratios, looked like becoming a reality.

Solidname, yes you are correct, if they bring in DTI’s for us then we won’t be able to borrow anymore.

Not really a problem for us at all though, as we have more than enough property and sometimes I think it would be easier having our money on Term Deposits!

The thing is though that we prefer returns of 9% plus capital gains on paper to 3% on TD.

TM2, in such ripe times, this flawed strategy is the one to first bite you then haunt you for many years. I guess some people prefer the role of rotating goldfish. "houses always go up, wait, houses always go up, wait, houses always go up.....

I legit hope he gets himself out of this situation. As much as I argue with him, I'm not so mean spirited to want someones grandpa to go bankrupt because he placed a bet that the property market will never turn bad.

He'll be fine, he can follow the advice that generation rent have been given - stopping paying for sky, stop those fancy holidays, no smashed Avos and drinking coffee, stop buying the latest phones, stop buying cars. Move to a cheaper area, it was just as hard in my day to buy a house etc etc...

Did you just admit to us all that you are horribly in debt due to property speculation?

Someone your age - who can't even figure out how to reply to people on a message board - should really not be in this situation. You need to get debt free ASAP.

Of course we have debt, it is the only way to go.

Leverage leverage leverage.

Thing is that we own a lot more that what our Banks do and in fact have been told by our Business Bank manager that we are his safest client, so that tells you something.

The thing is with DTI’s I’d that they should be far higher for investors as each property doesn’t have the living costs compared to owner occupied.

Property investment the way of the future for investment

.

It is this way of thinking that limits people’s ability to get ahead in life.

I think you will find that all people who have been financially successful will do something to improve their worth whereas the ones who analyse too much will never get ahead.

Yes we do have mortgages on properties but in the context of things it is the only way to be and our returns on both return from rents and capital gain on purchase price for what we actually put in is very attractive.

You can knock me as much as you like, but it will take a lot more than what is given to me on here to upset The Man,

Life’s good in Landlord land!

.

He sounds like a coke dealer who’s been sampling way too much of his own product

Who here has the charts for Fund performance over the last 2 decades incl GFC.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.