By Gareth Vaughan

Australian Treasurer Josh Frydenberg last week rubber-stamped an Australian Competition and Consumer Commission (ACCC) inquiry into foreign currency conversion fees, citing evidence these fees are higher in Australia than other countries.

Frydenberg says Australians are charged A$2 billion of foreign transaction fees every year for converting money into a foreign currency, transferring money overseas, the use of debit and credit cards overseas, using debit or credit cards online to make purchases in a foreign currency, and transferring money to a foreign currency on a prepaid travel card.

"Evidence from the Productivity Commission suggests these fees are higher than other countries, costing Australians hundreds of dollars more than in other countries per year. As a result, the 10.5 million Australians who travel abroad every year and the individuals and businesses who send money internationally every day deserve a better deal. At the request of the Coalition Government, the Australian Competition and Consumer Commission will put these excessive fees under the microscope," Frydenberg says.

How do Kiwi consumers fare? We know that the cost of currency conversion services varies significantly between different providers. So what are the prospects of us getting an inquiry into foreign currency conversion fees on this side of the Tasman?

Interest.co.nz put questions to the Commerce Commission, Financial Markets Authority (FMA) and Reserve Bank. And much as it was in 2015 when Australian authorities were probing high credit card interest rates and NZ authorities couldn't and wouldn't do the same, so it appears with foreign currency conversion fees in 2018.

"The Commerce Commission does not have the same market studies powers that the Australian Competition and Consumer Commission is using to look into foreign currency fees," a spokeswoman for the consumer watchdog told interest.co.nz

"Whether or not a fee is reasonable would only come under our remit if it was a credit fee, that is a fee payable under a credit contract. This could include fees charged under credit card contracts. Credit fees can only recover the creditor’s costs in association with providing the service. We are not currently investigating this issue but we did look at overseas transaction fees charged by banks on credit cards in 2011 and issued banks with compliance advice."

"The issue you raised is about the fee being too high but if there were any disclosure issues then that is covered by the Fair Trading Act (FTA). The FMA [Financial Markets Authority] has primary jurisdiction for misleading and deceptive behaviour under the FTA for financial products that aren’t consumer credit products," the Commerce Commission spokeswoman added.

So over to the FMA.

“The FMA licenses large financial institutions for financial advice, as a QFE [Qualified Financial Entity], not for foreign exchange. Companies providing foreign exchange services are not licensed by the FMA, but must be registered on the Financial Service Providers Register. Where foreign currency exchange fits into our remit is through our fair dealing powers, which are broad. These powers essentially cover deceptive or misleading conduct," an FMA spokesman said.

So what about the Reserve Bank, which since Adrian Orr took over as Governor in late March has started taking an interest in consumer issues, even though these are technically outside its remit.

"As you know, the Reserve Bank’s prudential objectives concern a sound and efficient financial system. Matters relating to product pricing and fees charged by individual firms is not an area that we focus on. Other government agencies may be better placed to comment," a Reserve Bank spokesman said.

'Fees should be fairly shared between NZ business and consumers'

So what about Commerce and Consumer Affairs Minister Kris Faafoi, what does he think? Faafoi was overseas, thus interest.co.nz received a response to its questions from a spokeswoman for Finance Minister Grant Robertson. She said the Government's expectation is any fees should be fairly shared between NZ business and consumers, with the Government keen to see that consumers are getting a fair deal.

"It is also worth noting that these currency conversion services are subject to New Zealand’s fair trading and competition laws. This means that currency conversion services should be provided on a competitive basis and the fees must not be misleading. In 2007, the Commerce Commission reached settlement with a number of banks and credit card companies for inadequate disclosure of currency conversion fees," she said.

"There are some fintech providers other than banks emerging in this market and offering innovative new products."

"Some credit card fees are subject to controls under the Credit Contracts and Consumer Finance Act 2003. For instance credit fees cannot be unreasonable, i.e. the fee must be connected to the creditor’s reasonable costs. However, this would not apply to charges for an optional service. The Minister [Faafoi] has signalled previously that he does not want to see further increases in interchange fees or merchant service fees for credit cards and debit cards in general," the spokeswoman added.

In 2007 Commerce Commission prosecutions of ANZ National Bank, BNZ, Westpac, Kiwibank, ASB, Diners Club, TSB, The Warehouse Financial Services and American Express International resulted in them paying more than $29,214,305 in compensation to customers, fines and costs. The total compensation for customers, after the companies pleaded guilty to breaching the Fair Trading Act, was $24 million, with the prosecutions due to inadequate disclosure of currency conversion fees.

ACCC inquiry follows Budget funding boost

The ACCC inquiry is into the supply of foreign currency conversion services to consumers and small businesses in Australia by authorised deposit-taking institutions and remittance service providers. It's under subsection 95H(2) of the Competition and Consumer Act 2010. The inquiry comes after the Australian Government announced A$13.2 million of funding in its 2017-18 Budget over four years for a Financial Services Unit to facilitate greater and more consistent scrutiny of competition. An additional A$1.2 million funding was provided for the Unit's first inquiry, which is into residential mortgage pricing and is due for completion next month.

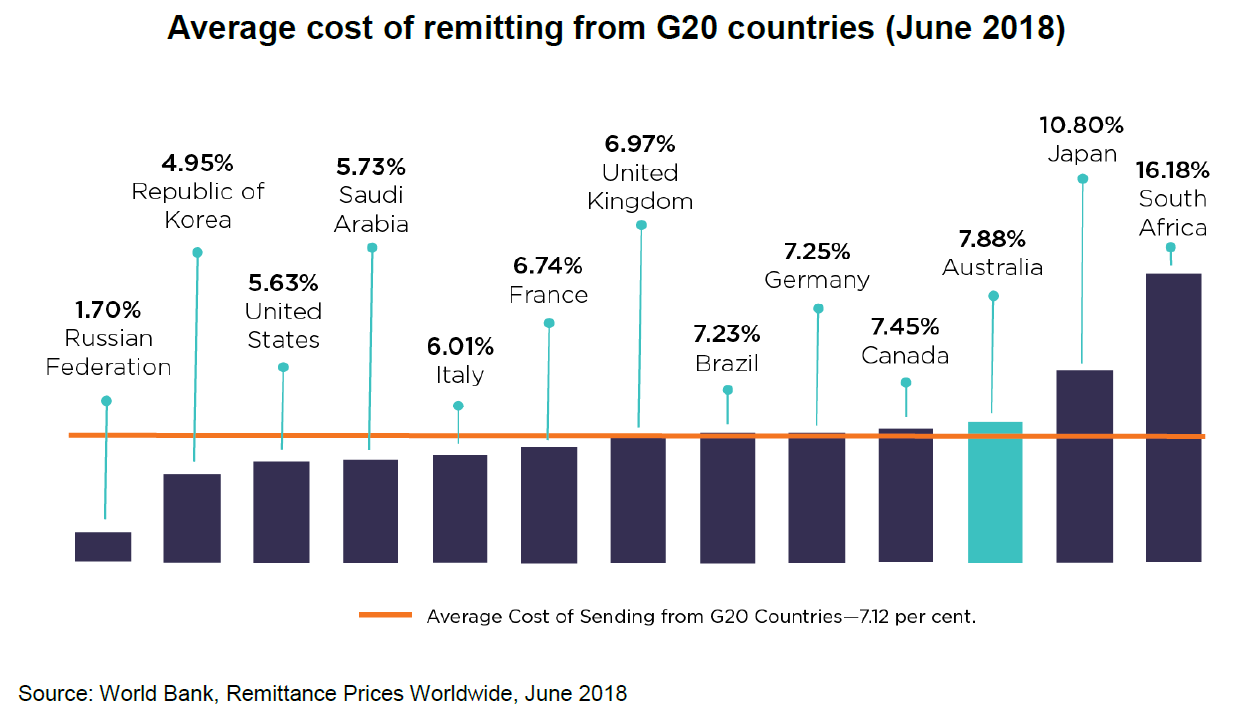

The ACCC's FX Inquiry Issues Paper notes Australian sent about A$8.8 billion overseas in 2016, and that prices for foreign currency conversion services are consistently high by international standards, as the chart below demonstrates.

The ACCC also says the inquiry comes after it has received consumer complaints over the past few years. Matters to be taken into consideration by the inquiry include;

- The pricing of and costs associated with supplying foreign currency conversion services;

- The nature and extent of competition between existing suppliers of the services;

- The existence and extent of any barriers to entry and/or expansion, and;

- Whether there are factors limiting the ability of consumers to effectively compare services and prices.

The ACCC's final report is due with Frydenberg by May 31 next year.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

21 Comments

why is it that New Zealand doesn't take the initiative on things like this and we only consider when Australia has had it brought up?

Commission for brokering or clipping every transaction (hi Visa) is far too high in NZ and we just continue to accept it as a part of life because there's rarely another alternative. EFTPOS has not caught up to the ease of payment that is contactless and we don't really have a choice in foreign currency :(

Lets hope the enquiry requires them to trim the margins.

That question is easy - the powered elite looking after the moneyed elite. Us little folk should just learn to do as we're told!

Because it's easier to move to another country than fight an uphill battle in NZ trying to effect change. My fellow Kiwis are petty minded and mostly brainwashed so decent people don't bother trying to get involved in politics.

Most of the talented people here have their potential wasted due to poverty or imprisonment. Those who are able flee overseas to escape our increasingly feudal society do so.

Who knows why things don't change, but at the end of the day; every one dollar you can get out of NZ is two dollars saved! Pay the exchange rates and count yourself lucky.

OrbitRemit is good.

Bank foreign exchanges are a rip off. Use Transferwise.

I recently travelled an per experience monitored exchange rates leading to the travel and purchased foreign funds using one of the Fx dealers identified through this site. They gave me a much better deal than the bank. I then noted the MasterCard Passport debit card and asked the bank if I could load my foreign exchange on to it. No can't happen. The fees put me off considering they took a cut on all conversions. Customer service seems to be a fairly low priority these days. Customer fleecing however is still top of the list.

The cash passports and travel cards are a rort. You load up with inferior-to-bank rates and then pay $ to withdraw from ATMs overseas despite it being in local currency. Surely mastercard/visa have the buying power not to pay bank fees for ATM use - well of course they do, but that's irrelevant when you can charge a poor sucker around $5 every time. Oh, and if your travel card runs out of the currency you load and you use NZD, there's up to 5.95% margin on that, plus any withdraw fee at an ATM. Nuts.

Travelling is a minefield when it comes to currency. I travel overseas on holiday for up to three months a year and do try to get the best deal. The fluctuating exchange rates is only the start and it means monitoring it and keeping abreast with international events (many thanks interest.co especially for including foreign exchange charts in your morning briefing).

The following is my experience and I am very keen to hear of others views.

I tend to use a combination of credit card (mainly for use with larger purchases and in larger establishments and I generally find BNZ Visa not too bad) but also take a fair amount of cash (e.g. surprisingly in Germany, restaurants do not take credit cards at all).

If travelling in Asia, cash is king and the only way to bargain - emphasis of cash comes later in the piece when trying to get the best price.

Credit card seems the lesser of the evil compared to Cash Passport. I see the current Euro Cash Passport rate to buy is about .53 compared to cash at .55 (about 3.5% more) and then the overseas bank gets in as there is invariably a $7+ transaction fee using a foreign ATM. Take out equivalent of $500 so well over 5% more than cash.

I am off to Vanuatu at the end of the week and I got cash a few weeks back - not only with the likelihood of a declining $NZ - but in Vanuatu even if a credit card is accepted by the retailer / restaurant (not always) there is a surcharge of 5% even before the banks start to apply their less than favourable exchange rate.

Last place to buy foreign cash seems to be at the airport - their rates and commissions invariably seem horrific. I tend to use TSB who have good rates and a wide range of currencies on hand (the only local HB bank to carry the Vanuatu Vatu, and always have the Vietnam Dong on hand).

If travelling in Asia, cash is king and the only way to bargain - emphasis of cash comes later in the piece when trying to get the best price.

This right here.

Bring a wad of NZ cash with you to Asia and you can often get really good rates, right at the airport.

Agreed somewhat, but little old NZ's $NZ not always in demand.

One of the best currency conversion rates I got was from a group of camel drivers in Rajasthan who often took out tourists who would tip them in $US (mainly $1 to $20 notes) for which there was no bank where to exchange into rupees and the local mafia types black market rates were extortion.

(A combination of rupees and $US is best in India; also in Laos and Vietnam where $US are well sort after).

Bring a wad of NZ cash with you to Asia and you can often get really good rates, right at the airport.

I disagree. The exchange rates on cash for NZD and AUD are relatively poor compared to USD or JPY.

The best exchange rate I ever got for NZ$ cash was a currency exchange in Hong Kong (after reading online reviews to find the best one). I was stopping over in Hong Kong on my way back from Europe in 2015 and got a much better rate converting my euros into NZ$ than I would have if I'd brought the euros back home and converted here.

It is probably justifiable to slag off banks who make considerable profits.

However, a couple of bouquets.

When buying glasses in Bangkok a few years back, my wife and I paid two lots of deposits and then two lots of final payments; the bank was doing a great job of monitoring my transactions and contacted me to confirm the payments. I also understand that they have reimbursed fraudulent activity on cc.

Having carefully read my banks automatic free travel insurance and comparing it to commercially available ones (quoted over $700 for 90 days to Europe) I am grateful - and with the credit card I that have, there is no requirement to pay any of the travel by means of credit card. (I did contact the insurers who said that it was best to put cc in ATM for a balance inquiry at airport as proof of my presence in NZ as my 90 day trip was the time limit for coverage.)

Probably. This was holiday money, so I was just thrilled it was getting like 1/5th the fee I would walking into any of our banks.

For serious amounts you probably want to do more research

The best currency exchange at an airport is usually an ATM. Every one of the money changers at any airport use usurious fees and rates. I hope that you are a bit more astute about finance when you buy a house. In short, the transaction fee is just one part of the rort, the exchange rate is the other aspect.

I've significant experience in currency exchange (coincidentally, I am currently writing this while in Greece). I get very grumpy if my small exchange amount fees and currency exchange rate slippage exceeds 1.5% in total cost. For large amounts, it should be under 1% in total compared to mid-market exchange rates. The 6% value shown in the article is evidence of a tax on the less than astute... Paypal was started by someone that wanted to reduce exchange fees, but then the concept got monetized, and now PayPal has very high fees. Many banks have usurious fees and poor exchange rates. There are some fx companies that have quite competitive rates, although I strongly recommend shopping around. The advertised rates sometimes do not align well with the spot rate. Similarly, there are sometimes significant variations in bank card transaction fees. For almost a decade I used an ATM card that used a conversion rate averaging 0.55% from the spot mid-market rate, and would refund the foreign ATM charge fee. I suspect that I contributed in a very large way to this bank changing their fee policy in that for a bit over a year, I was using the ATM daily to withdraw ~$500 USD value in NZD in late 2008 and early 2009. The net rate I was getting after fees and exchange slippage was better than the best discount fx transfer services...

The interesting part is that the credit union that I have the ATM card from, now charges a 0.9% exchange fee for an ATM withdrawal, but has removed the fees for using a credit card. When I want to buy a big ticket item, I now use my foreign credit card as it results in a transaction cost that is around 0.55% in total.

Looking forward to ripple solving this probelem

If the government can get enough "inquiries" going at once all our unemployment worries will be over.

The banks in NZ shut down a number of 3rd party foreign currency transfer businesses using the new money laundering law requirements for disclosure.

Keep an eye out for Revolut - they provide a fantastic retail and corporate FX service and are meant to be starting in NZ/Aus soon - banks are soon going to be forced to get more competitive, even if not by the regulators

We do get screwed overall. In the UK, some banks offer fee-free overseas cards, so you just translate at the Visa or Mastercard rate. In New Zealand...it's up to 2.50% commission with ANZ, TSB, Westpac

Credit & Debit Cards. Kiwibank does, however, lead with 1.85%. What interests me is that the fee is broken into a bank fee and a Mastercard or Visa fee, despite the credit card payment processor already taking a margin and giving a less-than-interbank FX rate. So basically if I spend US$100 overseas I pay the banks up to US$2.50 for doing so (source: https://www.moneyhub.co.nz/best-credit-card-overseas-fees.html)

We receive foreign funds regularly - more and more individuals are using Transferwise. Has worked for us now for some months - very straight forward. Good documentation.

Check it out - an interesting competitor that has recently emerged. Very easy to use.

Certainly much better rates / charges than the banks. https://transferwise.com/nz/

I agree, forget having a government investigation. the banks will be forced to respond to TransferWise taking their market share. I also got a TrasferWise debit card which is now loaded with euros and NZD. Now whenever I buy arduinos or whatever online I don't pay extortionate paypal conversion fees.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.