The Auckland housing market remains extremely subdued with the region's largest real estate agency reporting the lowest sales volume for the month of June since 2010.

Barfoot & Thompson sold 786 residential properties in June, down 13% on June last year and the lowest number for the month of June since 2010.

The real estate agency's sales have been at nine year lows in three of the last four months.

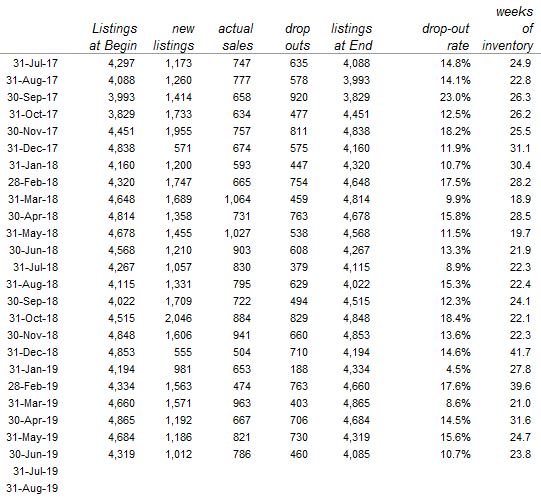

The decline in listings was even steeper, with the agency receiving 1012 new listings in June, down 16.4% compared to June last year and the lowest number of new listings in the month of June in at least 11 years.

The lower number of new listings helped to keep total inventory levels at a manageable volume, with the agency having 4085 residential properties available for sale at the end of June, the lowest number since August last year and down 4.3% compared to June last year.

While sales volumes were down, prices remained relatively stable. Barfoot's average selling price was $939,945 in June, up $10,953 from $928,992 in May. That's the highest it has been since December last year, but is still down from the record high of $968,570 set in March 2017.

The median selling price was $845,000 in June, down $5,000 from $850,000 in May, and well below the record of $900,000 set in March 2017. The latest figures suggest prices are continuing to fluctuate within a fairly narrow pricing band.

Barfoot & Thompson Managing Director Peter Thompson said properties priced between $1 million and $2 million sold well in June and accounted for 34.6% of total sales, while just 6.4% of sales were for less than $500,000.

"While prices in June remained solid and sales numbers were modest, there were a number of underlying trends that suggest greater activity was building than has been present over the last few months," he said.

"There are more first time buyers looking, there is a shortage of properties in the $800,000 to $1 million price segment resulting in competition for properties, vendors are more inclined to meet the market and banks are showing more interest in lending.

"All are positive signs for vendors who are prepared to price their properties at market," he said.

The comment stream on this story is now closed.

Barfoot Auckland

Select chart tabs

107 Comments

Where have all the houses gone.

“At month end we had 4,085 properties on our books, the lowest number for 10 months."

Last seen floating down a river in Egypt.

“.......... but prices steady.”

I seem to recall having read that before..... (-;

TTP

But drop-outs not exeptional at all

https://www.interest.co.nz/images/barfoot-reconciliation.jpg

{kind=link}

David, your basing your percentage dropouts against stock , not flow. Given the low level of sales, drop outs on a flow basis are significant , and when compared with last years same six month period have increased in percentage terms.

That "drop out" rate should be calculated based on the last 12 months ("LTM") and yes, on "flow" (i.e. listings) not stock.

You're not going to have the same property listed and dropping out in the same month so it's a bit meaningless to look at individual months.

LTM also normalises for seasonality.

I've been tracking that statistic on an LTM basis since January 2016.

The LTM drop out stat for June 2019 is 44.0% (15,809 B&T listings and 6,951 'drop-outs' in the 12 months to June).

That is high within the range I have.

The time series I have started at 32.8% in January 2016;

Hit a low of 31.5% in December 2016;

Climbed steeply to a high of 48.3% in February 2018; and

Has stayed around / just below that level since - now at 44.0% per above.

I'd love to have a longer time series to know what a 'normal' level is for this stat, I think it could be a real indicator.

My interpretation is that the higher the "drop out" rate the greater the expectation gap is between vendors and the market.

The market will only return to equilibrium when that rate settles closer to longer term "norms" - but I'm not sure what that "norm" is.

Edit: Checked all my data against David's and noticed I had incorrect listing figure for September 2018 (very minor - 7 listings)

Dear cmat

excellent contribution and thanks for keeping records as alternative to what conventional outlets give us.

Its nice we still have people making useful insightful comments, based on actual data/evidence. Keep it up.

Another way of looking at the withdrawal rate. The figures used are the same.

Listings start of January 4194 end of June 4085 difference 109.

New listings Jan 1st to June 30th - 6319

Sales Jan 1st to June 30th - 4361

Total New Listings 6319 + 109 (difference between starting and finish stock) = 6428

Sales / Total Listings over period. = 4361/6428 = 67.8% success rate so far in 2019.

So 32.2% of Barfoots Listings have been withdrawn. This is how any manager in RE industry should be calculating the Instructions to Sales Ratio.

Don't worry, there will be a lot more coming online soon. Stats just reported the greatest number of home consents in 45 years:

https://www.stats.govt.nz/news/townhouses-boost-monthly-consents-to-45-…

June volumes are 1/3 down on where they were at the peak of the frenzy.

786 sales in June 2019, compared to

903 in June 2018

855 in June 2017

1168 in June 2016

1167 in June 2015

1037 in June 2014

And Low New Listings are a classic symptom of where people can't afford to sell or don't want to sell for less than they paid. To give you an example consider Auckland.

Approximately 500,000 rooftops,

2015 - 30,883 sales

2016 - 25,987 sales

2017 - 20,172 sales

2018 - 21,447 sales

That’s 98,489 sales over a 4 year period. Or nearly 20% of the total stock where owners, if they wanted to sell would be selling for less than (2016,2017,2018 purchases) or equal to (2015 purchases). Either way the likelihood is that after transaction costs to sell most won’t have enough equity to trade. Unless circumstances force a sale, these people are stuck, either through not wanting to sell at a loss, or just being stuck by their equity position. Generally very little is paid off the capital in the first 5-10 years so reality is that volumes of sales are going to be low for a very long time ahead and this is going to have an effect on credit growth at some point in the near future.

I'm missing something here. Do we know when these sellers purchased, their equity position and thus ability to trade up? Perhaps you explained elsewhere?

Hi Rastus

Probably best to review yesterday's stream

https://www.interest.co.nz/property/100473/new-listings-realestateconz-…

Let me all save you a lot of time:

Reality is that the housing market is stuffed, everyone knows it's going to go down by 200%

Just look at what happened on Mars 3 centuries ago, we're not duffrent

Houses are crashing because people can't afford them, baby boomers are retiring and my hair dresser told me so.

The parabolic tangent demonstrates the symmetrical anti thesis

You humor me, you're irked, hahaha

Also we live on a finite planet, therefore we're all stuffed anyway.

Shhh, please let the grown ups talk.

Haha

I’m sure your investment properties make you happier than the upvotes that these “adults” like to give each other

Are you having a stroke?

Spruiker-DGZ started making similar irrational posts. Shortly afterwards he disappeared. The evidence is stacking, Yvil has become overwhelmed.

You humor me, are you irked? LOL

...nah. Seems as though you're irked though ;-) To many red flags got you so fired up today. So many useless posts in such a short time frame, business must be quiet. I suggest you try some volunteer work. Give something of use back to the community. It's highly fulfilling.

Those poor souls at the hospice you're at, they are probably so sick of listening to your spout they are hoping for the quick exit.

Houseworks, OMG, whatever next? Your disrespectful comment speaks volumes about the state of your inner soul. My role is to help fundraise to provide better end of life care, not provide financial advice. Since you present yourself as a rudderless individual constantly arguing against sound financial advice, it's also foolish to argue the possibility you'll one day need Hospice care too.

Assume everything and you'll come away knowing little of value.

Ha did I say anything about financial advice, of course not. Look who is making assumptions rhetoric poppy. You are so egocentric you ASSUME others do not volunteer or do stuff to help others. They just dont go boasting about it in the way you do.

Whatatool....

Intelligent comment not

Houseworks, consider yourself self outed by your own pricked conscience. Maybe there's some good in there after all.

You competently discredit yourself. For example, you have a "diversified invesment portfolio"

(sigh) - I'll now leave you and your conscience to wrestle it out ;-)

I doubt you know what a conscience is. Anyone who goes about boasting about volunteering and trying to belittle others are total losers.

I've volunteered for a year longer than I've been a member here on interest.co. (since I retired in fact) I've only just very recently thought it appropriate to make mention of it. If you've really got a problem with those who utilize their spare time to support others, get out yourself and donate something other than worthless criticism.

It will help settle your conscience.

You say "donate something other than worthless criticism." If the cap fits wear it retired poppy

Cognitive dissonance, when firmly held beliefs are confronted by irrefutable evidence that contradicts them.. does strange things to the brain.

Might want to look up "sarcasm" instead. ;)

Oh, we got what you were trying to do.. it just flopped harder than the Auckland real estate market has.

Sarcasm is a western thing, and Yvil has only just discovered it.

Yeah, D- more effort required.

Don't get so hung up on the property market. It's the financial system that is the real concern.

Spot on. And of course the leveraged property sector and sub-prime is what made finance system world wide crash last time

You do seem a bit rattled by the situation. Not to worry though, hold tight and go ahead and buy a few of those mediocre central Auckland apartments for $10,000+ per sq metre. Great time to buy, can't lose...

Not interested in an apartment, the whole building maybe, it's slowly getting easier getting value (still very hard in Auckland) when the market is less hot

Yes - stay away from Auckland’s inner-city apartments.

They’re a blight on the landscape.

TTP

Buying a whole apartment building!!! That DOES NOT make sound financial sense!!! Just ask retried poppy, he knows that stuff.

It doesn’t in NZ at the moment I don’t think. The Sydney situation is getting interesting though. There’s a glut, developers are getting desperate, the market has declined -15% average, and poor quality building is being revealed (see Opal and Mascot Towers etc). Buyers are becoming wary and prices are dropping. Now is not a great time, but when things bottom out there’ll no doubt be some real bargains for good quality long term, and immigration is solid there. Odds are Auckland will go through similar.

Just as I said, not good financial sense! Like 2009 and 2010 in the aftermath of the financial crisis must have been a bad time to buy a house because virtually no-one was buying property.

"Barfoot & Thompson Managing Director Peter Thompson said properties priced between $1 million and $2 million sold well in June and accounted for 34.6% of total sales"

This is wrong, several commenters here, who of course know better, posted that the top end is definitely tanking, so it must be. Mikekirk's hairdresser told him so

"Selling well" is not the same as "selling at a high price". You could say that my ex-landlords house was "selling well" because they managed to sell it. Mind you, they sold it for $1.19 million. RV $1.7 million.

What % of AKL properties have CVs above $2 million? Is 1-2m really the top end?

You are quite right, it is not. In the first 5m of 2019 sales above $2m were 5.3% of sales of residential property in Auckland.

In 2017, same period it was 10%.

Sales above $2m in 5m of 2017 were 615.

In 5m of 2019 it was 398.

So, 40% drop.

between 1.5m and 2m the drop in the 2 years concerned, is 25%

between 800-1m only 1.2% drop.

No point in comparing to 2018 only, because 2018 were front-running cadges in shape of OBB and AML

2017 was a bad year so if 2019 is worse, you know it is bad and worse.

Hi Yvil,

what I in fact said was that she reported to me what had happened at an Orewa auction house 3 weeks ago, when there were no bids for a house with a reserve in region of $1.2m. Sales of Orewa houses and townhouses (fact, from REINZ figures) in May were 69% lower than in 2018. Sales of property in Auckland, in the $2m plus bracket, are down 42% on first 5m of this year, compared to 2018. This is not opinion It is fact. Above $2m is not cited by Barfoots note. When looking at media outlets with vested interest in "confidence " it is as well to look at what is NOT said, or cited, and then ask oneself why that is. it is called selective editing. The bracket which is dropping least is that between $600-800k (about 7% in same 5m period) The higher the price bracket, the greater the % fall in sales. Nice to get a citation form you. Shame about the accuracy

Sorry can't be bothered reading such a long post.

You keep getting RE advice from your hairdresser, just be careful when you get your hair cut by your RE agent, I hear some are not that good

Oddly enough - I had heard that a lot or real estate agents where currently taking a 'hair-cut'

LOL, smart

I AM A REAL ESTATE AGENT mate

You're brave saying that in this part of town.

Yes Mike Kirk is a real estate agent. Heads up Mike there is an error on your listings web page, it shows no properties for sale.

Thanks mate!

Thanks for admitting that mikekirk29, Good to see an REA who's willing to discuss what's actually happening with the market.

Thanks for admitting that MikeKirk, unlike most on this site (especially Retired Poppy) I don't mind RE agents at all. I'll give you a bit of slack and I hope sales improve for you, sincerely.

Yvil translated "I'm now highly embarrassed and feel foolish"

mikekirk29, you come across as open and honest. You tell it as it is. You're an asset to a profession that's struggling with its reputation. The more of (you) the better.

RP, you repeatedly call TTP, "REA TTP" in an attempt to discredit him... you're full if it

Yvil, neither you nor REA-TTP need any assistance from others in the discrediting department - lol!

"Star performers"

Your incessant bickering like two old ladies is tiresome. Please stop baiting each other and grow up. Sick of having to sift through your immature posts to find some insightful information. You are providing a massive amount of pointless noise with your school yard insults.

Yes it's very refreshing to come across a RE agent who is honest and not full of BS. Could be a niche market there....

"Barfoot & Thompson Managing Director Peter Thompson said properties priced between $1 million and $2 million sold well in June and accounted for 34.6% of total sales"

This is wrong, several commenters here, who of course know better, posted that the top end is definitely tanking, so it must be. Mikekirk's hairdresser told him so

36.4% of the number of houses sold? or 36.4% of total $ of sales? Quite different answers those two. And then we get back to seeing if that number is actually strong or weak historically.. without context its hard to say what it actually means.

From Feb 2017, the price graph bounced 8 times.. be patient just a few more and it will roll off into GFC cliff!

Median selling Price is not actually a true indicator as now many who were early trying to buy for $700000 are streching to high 700s and so on as are getting much more value for their $$$$$$$ - Also supported by low interst rate.

Best time to buy is in high 800s to 900s as are getting houses that would have earlier sold for million plus. Also many who bought from 2016 onwards are unable to sell without a lose (mostly) so all those who have holding capicity will hold for few years and if have no deep pockets are and should be ready to book a lose (minimize the lose) as in future may bleed, if are unable to hold for few years.

Read the market as now no amount of manipulation will help and anyone who thinks that the market is not bad or is going to go up is fooling oneselves.

"Best time to buy is in high 800s to 900s "

I've looked for 800s & 900s on my watch, couldn't find it, what time is 800s to 900s please?

Yes HPI is the measure

Shortage? Between $800-1m? Precisely what Rodney builders have been churning out for last 6 years running.

He is right that this is category performing least badly in sales terms, along with 3 beds between $600-800k.

But, sorry, sales over $2m (not referred to by Mr Thompson) in Auckland are down over 45% in last 5m, compared to 2018. Listings are also misleading because they include A LOT of duplicate listings. In Hibiscus Coast for example, duplication is 80 out of 525 houses and townhouses, with a further 25% of these listings under that category in FACT being house and land packages - ie no house on it for sale yet at all. That is, 25% are awaiting development into a usable house. So, available for living in is a totally different and much lower figure. Sections and apartment sales are over 25% down in Auckland year on year, despite the fact that they are building loads of apartments. Why? Price , yes, but mostly because who likes apartments? Foreign buyers and they cannot buy now. Auckland is returning to the norm (reverting) which is approximately the level of 2012.

I'd say price is the biggest issue with apartments. It's just completely insane that a 2 bedroom apartment costs $700-800k, and you can't get a decent 3 bedroom apartment under $800k. People in Europe buy apartments because they are much more affordable than houses. In New Zealand, they cost pretty much the same.

Spot on mikekirk29. "Foreign buyers and they cannot buy now. Auckland is returning to the norm (reverting) which is approximately the level of 2012".

It will be interesting to watch what happens to the regions that were popular with local Investors when they were pushed out of Auckland by high LVR rates. I wonder how quickly Hamilton, Tauranga and Queenstown will return to normal price value levels, at least they seem to have come off the boil.

CJ

You say "Hamilton ... seem to have come off the boil."

Wrong. Check the facts. Am very keen to debate this with you CJ

While sales volumes were down, prices remained relatively stable. Barfoot's average selling price was $939,945 in June, up $10,953 from $928,992 in May. That's the highest it has been since December last year, but is still down from the record high of $968,570 set in March 2017.

Yeah, that isn't prices remaining stable, that is the amount spent staying stable. Price is determined by what you got for your spending. And HPI is the best measure of that.

Since the peak in late 2016/early 2017 the Auckland HPI looks quite stable to me, relatively speaking. Just looking at the graph it seems to have hung within a band of about 200 points.

It was for a while, but recently started to drop was -4.4%Yoy, then recovered slight to -3.3%Yoy. We'll find out where it went this month in a couple of weeks. My prediction is it'll be back to about -4.5% again.

Just out of interest - is the HPI inflation adjusted or not?

I don't think that it is.

For example, CPI (inflation) for the last year has been 1.9% yoy. If the HPI is not adjusted for inflation, then if the HPI is -4.4% yoy, then on an inflation adjusted basis, that would mean HPI is -6.3% yoy - so in inflation adjusted terms (i.e in economist's jargon "real returns") are -6.3% yoy.

Recall in the mid to late 1970's, nominal house prices (i.e unadjusted for inflation) were still rising, whilst the reason that "real returns" were negative was due to the high inflation rate which more than offset the nominal house price rise.

Then you add the impact of leverage used to finance house purchases, and the inflation adjusted returns on the equity value is even more negative.

it's a good question. a quick bit of googling suggests "no", but i suspect someone here knows more about the methodology.

"Just out of interest - is the HPI inflation adjusted or not?"

Yes it is not inflation adjusted. I am just wondering is the NZX50 gross index inflation adjusted? Also does it count dividends twice, when they are paid out and when they are grossed back in the index? If it does, would that show a higher share market value than normal which could potentially mislead novice investors and Kiwisavers??

The NZX50 is a simple cap weighted index, no adj for inflation. It's a rough measure as this type of index is also changed when the constituent stocks are rejigged.

HPIs aren't usually inflation adjusted either ~ as far as I am aware. Happy to be corrected on this though.

To take the example further for a leveraged house owner using a LVR of 80%, where the HPI has fallen 4.4% yoy:

1) in nominal price terms - the value of their equity has fall 23.0%

2) in inflation adjusted price terms, the value of their equity has fallen 24.4%

So in the span of 12 months, that equity value now has purchasing power of 75.6% of the amount it could purchase a year ago.

Compare that to the situation that if instead, the house purchaser had waited for a lower house purchase price, and put the equity deposit into the bank for the time being, the purchasing power would be about 100% of that of a year ago (as the interest from the bank offsets the increase in prices due to inflation)

Great comment

From Barfoots website:

June 19 v June 18

Central Auckland: 13 v 46 (-72%)

Central suburbs: 110 v 135 (-18.5%)

Eastern suburbs: 44 v 66 (- 33%)

Franklin/Maukau: 67 v 108 (- 38%)

North Shore: 124 v 134 (-7.4%)

Rodney: 73 v 68 (+7.3%) - notice the average price for these sales was $65k lower than in June 18

S Auckland: 125 v 94 (+33%)

West Auckland: 128 v 139 (-8%)

Watch the rate of lowered listings on RE NZ on first 4 days of calendar month, when listings are not renewed.

On a slightly different note, I see that Shayne Elliott is threatening to downsize ANZ New Zealand if the RBNZ don't backdown !https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12….

Stand firm Adrian Orr - You are doing the right thing for the people of New Zealand!

Yep, I noticed this too. Its an unusual strategy for a bank to publicly comment with such a brash narrative.

If ANZ were to pull back I'm pretty sure competitors would look to fill the void.

Is that a threat or a kindhearted offer, you wonder?

It’s funny, they say there is a shortage of capital at the reduced rate of return but I see the OCR might go to 1%. If there was a surplus of better investment options I’m thinking the OCR would not be going down. So I’m picking their investors won’t have any better options for their equity.

Property investment is still by far the safest and best returning investment available!

With interest rates so low and will remain low, there are plenty of opportunities to invest with positive returns and capital gains assured in many parts of NZ, Christchurch being my choice due to many reasons!

If you are currently renting and can afford to buy a property, I would be encouraging it!

Reality is that if the Reserve Bank demands that Banks hold more cash then if you are a marginal borrower, in the future you may not be approved for finance!

Seasoned investors will have good equity and will be taking advantage of the negativity that many talk too often!

If people took advice from the property bears on this site, they would be financially disadvantaged by hundreds of thousand and even millions!

The tide is turning, RBA just cut official rate to 1%.. RBNZ is next on the line!

This low volume of sales despite the major players (ANZ,BNZ,Westpac, ASB) negotiating cheap mortgage rates in the 3.5% to 3.79% range fixed for 1 or 2 years - well below carded rates! It is no surprise that people are withdrawing homes off the market and refinancing at such low rates.

Any areas that previously had rampant offshore buyer activity and strong migrant flows like Albany and other areas of the North Shore are suffering as are the investor districts like Massey, Mangere, Manukau etc.

Change of tack gents: If you had $1m to $1.2m to purchase a house (4 bed) where would you buy in Auckland suitable for a family with plenty of amenities?

I'd split it and buy two 4 bed homes on the West Coast of Auckland where foreign Investors hadn't price distorted that market as much, so therefore less likely to experience big price corrections in the next few years.

Where are you talking? Piha? Pretty pricey there now. Also a pretty long way to City.

1 Mil range I’d buy a 1000sqm do up in Beach Haven mixed housing urban easy consent to build more on it and good transport links bus and ferry which are only going to get better and better very nice area New Lynn prices but far more attractive. Titirangi is beautiful but expensive and has bad transport links

Titirangi, Kaurilands, Laingholm, Parau, Cornwallis; all commutable with close train connections at Glen Eden, good primary schools. Popular with those use to commuting for 40 mins such as Europeans, very low crime rate. Prices are balancing out.

Oritia, Glen Eden bit more suburban. Piha, Waitakere, Waiatarua is a bit far for a commute, though friends of mine who are in to surfing say it worth it for that better quality of life.

Also younger Kiwis are starting to realize that they need to commute if they want a nice home with a garden.

titirangi? tor bay?

Which area do you work ? Or do you work from home ? I ask as the first thing I'd consider is the traffic issues and how long you want to spend in the car each day.

Surrey1, good on you for actually using this forum to good use. You will get plenty of opinions (they're like… everyone has one), make sure you take advice from people who have actually achieved what you're looking to do.

Yvil version of. Look at me, look at me!

not many people know about Oranga..... until now...

https://en.wikipedia.org/wiki/Oranga

President of Property

These are all good suggestions and have looked at Titirangi, Torbay, Beachhaven etc as well as all the predictable locations somewhere beachy sounds appealing . Im ok with a commute of less than an hour into the city Im in corporate banking so realistically the city is the only option but over here I can essentially work from home 2 days per week if I like would be good if I can replicate this in NZ. Im in a fortunate situation as I would need a small mortgage or maybe not one at all but while in my view a falling market presents a great opportunity to buy its been so long since I lived there Ive forgotten what its like best to rent for a while and get a better feel.

Another loophole for property speculation is closed. Government has ended negative gearing. The law was passed last week. Now, speculators can not offset their property losses from income elsewhere.

https://www.parliament.nz/en/pb/bills-and-laws/bills-proposed-laws/docu…

Cheers.

Why is everyone getting so stressed about the devaluation of residential property market? There are other property markets besides housing. The commercial market is booming with net yields ranging from 4-8% after all expenses are paid. For the same money as a house or apartment you can buy a shop, office or factory. No bright line test, no foreign buyer ban, no tenancy tribunal, no warm and dry bleeding heart stuff, no bond limitations, no political interference, and tenants pay all outgoings. How much better can it get than that? There is a huge demand for commercial space in all the main centres, so vacancies are rare.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.