The latest figures from property website Realestate.co.nz paint a very subdued picture of the market, with new listings and total inventory well down and prices mostly easing.

The website received 7295 new residential listings in July, which was the lowest number of new listings it has received in the month of July since it began recording the data in 2007.

Inventory, which is the total number of properties available for sale on the website, was also down, with 21,843 residential properties available for sale on Realestate.co.nz at the end of July, down 3.4% compared to July last year.

Average asking prices have also been trending down, falling from $702,090 in February to $646,842 in July.

The average asking price in Auckland was $890,603 in July.

In May, average asking prices in Auckland dropped below $900,000 for the first time since August 2016, and they have stayed there ever since.

Other regions showing a falling trend in average asking prices were Coromandel, Waikato, Bay of Plenty, Wairarapa, Wellington, Nelson Bays and Canterbury.

The decline in prices would probably have been greater if new listings hadn't trailed off, preventing a glut of unsold properties building up.

However, record high average asking prices were achieved in Hawkes Bay $579,647, Taranaki $475,424, Otago $454,727 and Southland $373,897.

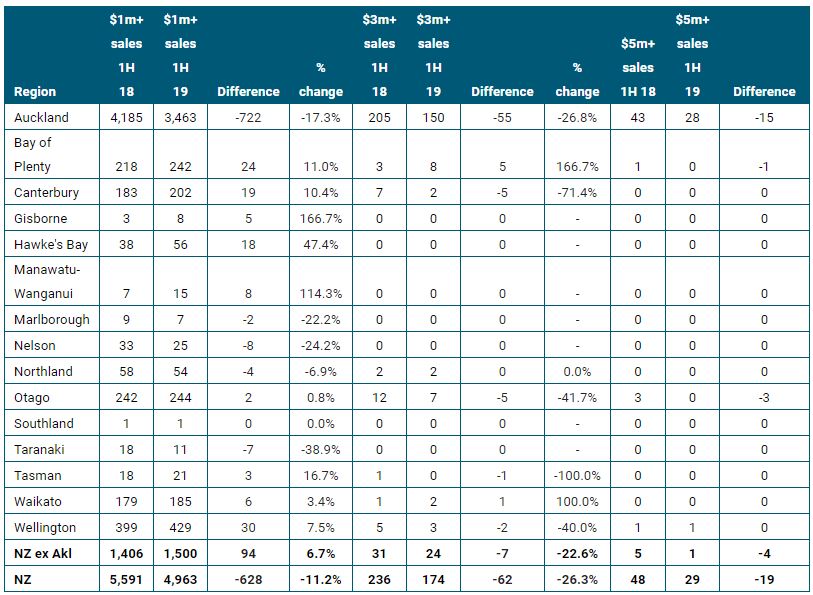

Hard on the heels of Realestate.co.nz's latest figures was a report from the the Real Estate Institute of NZ which showed a big fall in the number of homes selling for more than $1 million.

The REINZ said 4963 homes sold for more than $1 million in the first half of this year, down 11.2% compared to the first half of last year.

The fall was particularly pronounced in the Auckland market, where million dollar-plus sales were down 17.3% in the first half of this year compared to the first half of last year.

The decline was even greater for $3 million-plus homes in Auckland, which were down 26.8% compared to the first half of last year.

The table below shows the trend for million dollar-plus sales throughout the country.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

159 Comments

Auckland is bombing!

Spruik that!

I think these figures have already been spruiked.

The falls in volumes are actually much higher in the traditional money areas. Which makes me think that this blended table is hiding a story.

I'm guessing (and it is a guess) that a bunch of completion sales went through on CBD apartments and that has lifted the total transactions in a number of buckets.

One thing is for sure. Volumes in Remuera, Herne Bay etc are down a lot more than 17% & 27%. It's closer to 50% and sales are continuing to weaken.

Scroll down Glitzy, for undistorted figs.

Saying over 1m is a good way (as usual with averages) of hiding things

No As per Newshub - Auckland in Booming!

https://www.newshub.co.nz/home/money/2019/07/property-prices-regions-hi…

However hard one may try to influence with vested news - Fall is imminent. Like it or not.

Trend is your friend, until the end!

This must be some sort of hoax

Oscillations.

No wait, it’s “Taxcinda’s” fault.

Ha-ha-ha:) yes true. If National were still in power the entire world would still be prospering (^_-)

The Sir JK devotees should've taking a lead from him in selling up (his place in Parnell), taking profit, and downsizing, at the top of the market as it's turning out.

Some did! Mr Hoskins for example.

Not a JK devotee by any means but so did I. Saw the writing on the wall, and nothing to do with the change in govt. it’s a bubble.

Yes after allowing open immigration higher per capita of population than even in the United Kingdom

No wonder property went up

Price will double in 7-10 years.

I mean, it's not impossible. Only takes a 7% annual inflation rate over 10 years.

By 2026 apparently.

LOL

Auckland affordability gradually improving for young Kiwis. That seems positive news.

Unfortunately the lower end is still holding. Hopefully not for long.

As a FHB I really hope they don't cut the OCR next week because if they don't I think there will be a bit of panic.

Not in Chch. Up until this winter they had been, but prices seem to be collapsing in the $300k range now. I suspect its due to the old rentals being put on the market, and the absence of investors wanting to buy them.

Since last month or two even lower end has started to move downwards. Domino effect. Earlier when was going up. it was faster as was supported/highlighted by RE Agents, vested news and ow when it is the other way down all effort is made by the same people to down play it if cannot hide it but for how long as now the process has started and even FHB who were earlier rushing are showing constrain and waiting for the right price to get maximum for their $$ deposit.

but that will never be highlighted by the media.. they will portray that its all bad and gloomy..

That's why it's called the Granny Herald.

Pardon? That would be why sales are down in last 6m in their price bracket of $600 - 750k, by 7% and apartment sales in that bracket are down 33% then.

Spruik this spruikers

- Just a blip!

- Low interest rates will stimulate the market!

- High immigration will stimulate the market!

- Housing shortage will stimulate the market!

- Increasing rental yields will stimulate the market!

- CGT ban will stimulate the market!

- FBB was a fizzle

- Low unemployment rates will stimulate the market!

- Westpac chief says it will be 7% up, and he's an EXPERT!

- Our housing market is armour plated

- Tony Alexander says Australia built more houses so we're diffrunt

Am I doing it right?

Oh, and some more:

- I don't know ANYONE who bought a house and regrets it!

- CHCH is where it's at, BUY NOW, buy in Christchurch! Buy! In Christchurch, it's amazing! Please

Dude you forgot Palmy North..

Damn, you're right... how could ANYONE forget about Palmy North?

It can't be done.... many good whiskeys later and I still can't forget...

Court Jester, you need some facts before this outburst.. Speak to Sharon the hairdresser , down the long road, next to the alley, she has 45 properties , and buying more .

Nah, I just went to a National fundraiser and talked to a LOT of hard working YOUNG KIWIS who make $400k a year. There are a lot of young kiwi couples who can easily afford to buy now (and they should!).

And not to forget that NZ is immune to what happens in rest of the world and house price never goes down.

snap...…... funny post. Well done

Things will never change for NZ

1. NZ's future depends on more migrants

2. Land availability is fixed

3. Politicians are incompetent

4. Climate in NZ improves

All these factors will contribute an ever increasing house price in NZ.

Climate in NZ improves?

getting warmer..

So's the Antarctic. It doesn't make it an improvement. It makes it a likely global disaster.

The weather is also predicted to get more volatile and wilder....

Which might be a concern if ANY of the predictions had actually come to bear. Which they haven't. And not only haven't they, but they've been so wildly off that there is simply zero credibility.

What are you on about?

Melting is proceeding much faster than predicted only a few years ago.

What was supposed to not happen pre 2080 is already happening.

Do you occupy a river in Egypt?

Every report I've seen asserting something like that has been debunked within a few weeks. As with the markets...one has to consider the sources and look at the figures oneself.

how are you qualified to comment, and to dispute the opinion of the VAST MAJORITY of the scientific community

Those factors also apply to the capital cities in Australia but that didn't stop their house values to nosedive over the last few months.

They may have somehow extended their pre-doomsday grace period somehow but for how much longer?

1. In what way? What happens to NZ's future if immigration is cut back by, say, 50% next year?

2. Land availability is fixed by the law. The law can be changed. If you mean the actual land area of the whole country, then yes, it's fixed, and it can support about 60 million people or even more.

3. Show me a country where politicians aren't incompetent in some way.

4. God... I won't even comment on this. If climate change is your argument for increasing house prices, you are desperate.

1. you would not get your superannuation, school and hospital would close, beneficiaries would loot on street

2. which party in NZ has the wisdom or the ball to change it?

3. Singapore and China. I know I always get tomato threw at me whenever I say anything positive about China. (I wondered why)

4. Heat waves in AUS, EU, USA, China. Do you watch news?

Aint no one denying climate change. They're denying it somehow helps increases NZ house prices because it's a bit warmer here.

1. And the rivers will turn into blood, the sky will fall, plague breaks out and all the volcanoes in NZ will erupt simultaneously.

2. Does it need to be changed right now?

3. If your idea of a competent political system is China's, then... I guess we have very different definitions of what 'competent' means.

4. I'm convinced there is a climate change. But how is this relevant to house prices in NZ? Do you think everyone will suddenly flee to NZ? There are no other places on Earth where the climate will become 'better'? Also, a lot of people live in Norway, Sweden, Finland, Canada, Iceland, Moscow etc. where the climate is not very pleasant.

Meanwhile China is sitting on the world's biggest demographic timebomb because of the poor leadership's one-child policy. How will the pensions for that bubble be paid?

1. Yes and no.

2. Land availability is fixed everywhere, in case you haven't noticed. That hasn't stopped house price busts.

3. The competence of politicians is mixed everywhere.

4. Relevance? You think it will be warmer so more people will be attracted here? It will also be wetter and windier. Even if its 1-2 degrees warmer, that doesn't turn NZ into Florida,,,,

And all of this is occurring in an environment where:

- Interest rates are already low and have recently been cut

- LVR's were relaxed earlier in the year

- Employment remains high

- Migration is still at elevated levels

- CGT changes being taken off the table

Normally these should all be putting upwards pressure on prices. The really interesting part will be if some of the above factors shift from supporting prices to putting downwards pressure on them.

You get a rates cut! You get a rates cut! EVERYONE GETS A RATES CUT!

Throw the pensioners under the bus! Gotta protect the speculators!

Pensioners have their universal benefit. Hard to feel sorry for them when their snouts are deep in the trough.

A tiny fall for Auckland (barely registering on the scale) compared with the magnitude of the last upswing.......

And for many landlords it will have been cancelled out by rental yield.

Wellington and Auckland remain two of the best cities in NZ for residential property investment.

But, notably, “forgotten” cities such as Palmerston North have been faring remarkably well.

NZ has vast potential for real estate investment, as its international profile expands.

Wait and see what the future brings......

TTP (-:

We can always count on you TTP, blinkers on...

Regardless, no rush for the FHBs. The FOMO has long gone.

Wellington and Auckland remain two of the best cities in NZ for residential property investment

Best cities in NZ? Depends who you talk to. Some might say in the world. In the case of Auckland, perhaps that's why the cost of parking in the CBD is on par with central Tokyo.

TTP. The trouble with real estate is that it's a long term investment, the negative nancies cant get their heads around that. Over time the little improvements, the small rent increases and even the good deals here and there that add up. Its then that people wake up and say that property is too expensive for the average Joe and Josephine.

Holy s*** it isn't that complicated; no one fails to understand that housing is a long term investment. However you would have to be a complete financially illiterate moron to buy something for today for $100, which you could get for $80 tommorow.

No one doubts that one day NZ house prices will be much higher than they are now. No one. But that doesn't mean the trajectory is unfalteringly upwards, and that savings cannot be made by buying in the dips.

And while I get the arguments previously saying that now isn't that time, and we were not actually heading for a dip... Well just read this article for gods sake; its falling. Anyone who bought a first home 2 years ago, will be kicking themselves they didn't wait, save more, and get a better house for less later.

No Milkyone, don't you get it? Only they alone understand those houses will be worth more in 50 years! We must ignore that they'll all be cheaper next year than now... We must ignore all reports and keep the party going.

This comment is PRECISCELY what I'm saying " However you would have to be a complete financially illiterate moron to buy something for today for $100,..."

You just dont get it Milkyone .... the property market is not Homogenous .... and neither is the milk market there is not one price even for the same thing. Funny that! But at least a buyer can negotiate with property vendors you cant do that buying two litres of milk. Learn how to negotiate and dont be a moron

Even though the underlying asset is the same (residential real estate), the financial economics and motivations for those getting into the residential real estate leasing business are very different to the economics and motivations for owner occupiers of residential real estate.

That is the essential difference between Houseworks (residential real estate lessor) and Milkyone (potential owner occupier)

In the case of Milkyone, the debt service payments is coming out of his own pocket.

In the case of Houseworks, assuming a positively geared real estate leasing business, the debt service payments are being paid by their Housework's customer (i.e the tenant)

This is very true. Which makes it very frustrating when the property investors give financial advice which applies to their situation, but not FHBers, and seemingly willfully cannot get their heads around the difference.

I've heard that argument before, the classic "despite the position of the market, if you are smart you can get a good deal". And its completely correct.

BUT

The same logic applies in a lower market. So if the average/media/HPI is at $100 today, and $80 tommorow, if I am smart and 'learn how to negotiate', you would assume I can get a better deal in the $80 market than the $100 market.

I mean for f***s sake; no matter how smart you think you are, do you think you can negotiate for a property in Auckland for the price it sold for 10 years ago? Of course not. The market matters.

But how about this; answer me this hypothetical; the market proceeds to fall (by whatever measure) in Auckland by 15% over the next year. Do you think a 'smart negotiator' is going to be able to buy a reasonable property for less now, or in a years time?

"Do you think a 'smart negotiator' is going to be able to buy a reasonable property for less now" than "in a years time?"

Yes. After years and decades of experience in the property market I can say that confidently. We've also bought several properties in the last few years, investment and personal, I dont regret any one of them. Being hands on property is excellent. The other thing I know is that when the market tightens up, it will happen faster than you can move, all of a sudden vendors refuse to negotiate.

Lets say you are Rockefeller incarnate, and you can negotiate to buy a property 20% less than the market average.

Market average is $100. So you get a place for $80. Well done.

Market average is $80. So you get a place for $64. Even better.

Unless your magic powers of negotiation increase in a more expensive market, I find your claim slightly implausable.

And a simple glance at historical prices will tell you that the property market obviously doesn't move faster than a person. I mean, houses sold for less in 2014 than in 2016 didnt they?

Edit: To be honest it's up to you whether you believe me or not, you're a smart guy. No one can guarantee you what the market will be. But after a long downturn oneday there will probably be a cusp and change in the wind and in the market. Given that the market usually moves in a ripple effect you can probably jump into the next hot area before anyone else. Quote, find out where people are going to and buy a property before they get there.

Houseworks, you're the modern day version of a "two-bit snake oil salesman" that's for sure. You say "The trouble with real estate is that it's a long term investment" Well said although, it does sound like you've conveniently branded it as a "long term" investment and that its telling it will land you in even deeper trouble the longer the slump lasts.

I have one question for you. If real estate has always been a "long term" investment, why do we have the Brightline test? Do you have that sinking feeling that you've purchased the wrong property?

The brightline test (BLT) was put in place by National for spruikers of residential property. I think it's best you put your question to a spruiker. Note that the BLT does not apply to all types of commercial property and farms, thank you Sir John. Why would I ever think I had purchased the wrong property? I dont get buyers remorse.

I can agree with all of that.

Hi Milkyone,

You make good points and I don't want to argue with you. But fundamentally Houseworks makes a point I very much agree with (although he could put it across in a nicer way).

Too many FHB worry too much about where the market is going to be in 1 year, and we can argue as much as we want , nobody knows 100%

Rather than spending so much time analysing/guesstimating the market, you would be far better off spending that time getting to know the area you want to buy in really, really well, go to as many open homes as you can and you will soon get a good feeling for which house represents good value and which doesn't. This way you WILL be able to buy below market for sure rather than hoping that the market goes down for you to buy

I'll say it again, buying a house and hoping for the market to go up is not investing, it's speculating. A true investor creates value in Real Estate to make money. I would be perfectly happy to keep investing if the market stays flat forever

Yvil, I agree wholeheartedly with the investment philosophy in your comment. Although, I do suspect you're now morphing your comments to fit the new in vogue narrative of "housing is a loooooooong term investment". Where I come from is that because in recent times we've seen too much speculation in NZ housing, it's best FHB's wait until market forces shake out those speculators who are in it to win it quick. When, on sounder fundamentals, the market is "flat" less volatile, it is then safe for those who have only just scraped together their deposits, to proceed making what is most likely the biggest purchase of their entire lives. It's not fair that it should wind up being their worst.

Getting to know a local market, months or even years before you are going to buy is excellent advice.

But being aware of downside risks in the short term is absolutely critical for FHB unless they have a decent equity buffer (most don’t) and have high degree of stability (most don’t).

FHB right now dominated by people buying with <20% deposits or using equity from family. This is a recipe for financial disaster if prices fall in the short term

Oh absolutely, market/area research is vital. Me and my partner have identified a few areas of Auckland we would like to live in, and have been going to a 6-12 open homes maybe every second weekend for the past 18 months. (though less in winter, as the number of new listings are so low). And we track all the info on every place we visit in a 35 point spreadsheet. So be assured, we are doing our research!

However at this stage, we are waiting to achieve two things (assuming I am right and market will drop furthur in the short term);

-Lower the future debt we take on

-Get a better property for the budget we have

I remember doing the legwork etc like that when we bought our first home. When you do buy a property I am sure you will be very happy. A friend of mine said after you get married close your eyes and beforehand have them wide open. This quote seems appropriate for house buying too, make a good choice and then be satisfied :)

Very good advice! The day I vanish from this site will be the day I buy.

No chance I will be paying any attention to anything to do with the property market (for a few years at least) once I buy!

"However you would have to be a complete financially illiterate moron to buy something for today for $100, which you could get for $80 tommorow."

And if that owner occupier had an LVR of 80% ($800,000) and paid $1,000,000 for a house, and the price went to $800,000, then their equity of $200,000 went down by 100% to zero. How long did it take that owner occupier to save the $200,000 deposit? Only to see it evaporate.

Meanwhile they could have waited for a lower purchase price of $800,000, used that original $200,000 to take on a smaller mortgage of $600,000 (an LVR of 75%).

The annual interest reduction on the two amounts of debt:

1) 4% mortgage rate on $800,000 = $32,000

2) 4% mortgage on $600,000= $24,000

That is an interest reduction of $8,000 per year for 30 years (totalling $240,000).

Also there would be lower annual P&I payments:

1) $800,000 mortgage at 4% over 30 years = $46,264

2) $600,000 mortgage at 4% over 30 years = $34,698

That is a reduction in payments of $11,556 per annum for 30 years. (equivalent to $346,981)

Same or similar asset, yet different price paid, different amount of debt taken on, different annual cashflow payments over 30 years.

That is the potential financial impact of that single decision of an owner occupier to buy a house at today's price levels in Auckland.

So potential first home buyers & other potential owner occupier buyers in Auckland should assess the house price risk accordingly to avoid being potential collateral damage.

"However you would have to be a complete financially illiterate moron to buy something for today for $100, which you could get for $80 tommorow."

So you'll buy tomorrow right? But what if the day after it's $60… you'd be a moron as well, so you'll wait a bit longer, except the the day after it may not by $60 but $85… hmmm what to do? It may just be an odd day in a declining market… better wait till the next day, Yeehaa you were right the next day It's $75 it's going down indeed so wait some more… day after it's back at $80, "normal oscillation it'll go down again" oops the day after it's $95 what should you do now ???

I still say if you want to buy a home for yourself, buy today, because you really don't know when the lowest price will be and it's a very dangerous game trying to time the market, you might end up still timing the market in 10 years while your mate, who did not buy at the lowest price, has repaid 1/3 of his mortgage by then and had the benefit of living in his own home for 10 more years

Yvil,

Not sure what area of NZ you are invested in, but it may be in the South Island where valuations are lower, and you may be speaking from experience regarding the area you are invested in.

1) for an owner-occupier, the debt service to income ratio should be acceptable. In Auckland, at current price levels, some households are taking on a debt service to gross income ratio of above 45% which does not allow for sufficient financial flexibility for unexpected changes in circumstances. Owner-occupiers should be able to hold on throughout all economic environments including a recession, and a debt service to gross income ratio of 45% would not only be high risk in itself but be potentially even higher risk for someone employed in a cyclical industry (for example construction).

2) buying regardless of consideration to valuation is potentially risky. Valuation is an essential consideration in buying. Property is commonly valued on a most recent comparable transaction basis. This is acceptable in most circumstances except extreme conditions - as a rising tide lifts all boats as the investment adage goes. Alternative valuation metrics are required.

A alternative valuation comparison of residential property located in Auckland and Christchurch:

1) Auckland - house price to income ratio range is 8.2 - 9.9x, gross rental yield ranges from 2.1% - 4.5%.

2) Christchurch - house price to income ratio is 4.94x, gross rental yield ranges from 5.8 - 6.4%

Refer:

1) https://www.interest.co.nz/pro…/house-price-income-multiples

2) https://www.qv.co.nz/property-trends/rental-analysis

Hi CN, you do make very valid points above, just to clarify I was talking about buying a home to live in, not an investment. They are obviously very different but yes point taken about servicing loans in Auckland

You're right, it is a dangerous game trying to predict markets. However just because its a risk, doesn't mean its not a risk worth taking.

And sure, if the thing worth $100 today, which I buy for $90 tommorow, ends up being worth $60 in a weeks time, I have missed out on $30 of potential savings. But equally I did save $10 by not buying immediately.

Also unlike the sharemarket, the property market does move quite slowly. Its not like I'm sitting here getting all my property info from delayed data published by Interest.co.nz et al. I'm going to open homes every few weekends, keeping in touch with REAs, and genuinely feeling out the market. If it starts to pick up again, then sure, I will bite the bullet and buy. But I'm happy to wait for now.

And on the topic of waiting; yes my mate will have paid off some of his mortgage, but he had to pay interets on that mortgage. Meanwhile I am building a much larger deposit, which I obviously don't pay interest on, but will also reduce my future mortgage, and therfore future interest payments.

So what it comes down to is 'the benefit of living in your own home'. Which is a sacrifice sure, but isn't that what FHBers keep gettign told? Make sacrifices now for the future? I gave up avocado toast and SKY, I can probably manage to give up the warm fuzzies of living in my own home for another year or so if it saves me hundereds of thousands of dollars down the track...

From a previous post it looks like you are saving some very serious money, very well done to you Milkyone, that's awesome!

Careful CN, that looks too much like math. I have noticed that the usual suspects never respond to comments with math. Or at least if they do, they ignore it entirely in their response.

Interestingly I have another firend who bought an aprtment off the plans 18 months ago in Auckland. Still under construction after delays. He is painfully aware that he subsequently could have bought better apartments elsewhere for the same amount, and that his small deposit has basically vanished in terms of equity reduction. He is essentially stuck in this property until

A - he raises another deposit

B - the rising market brings his apartment value back up to where he bought it

Oh well you might say, he can just wait. Sure, but what if his circumstances change? Yikes.

And of course that leaves aside the fact that if he had just waitied, he would have got a much nicer apartment for the same amount.

I wouldn't buy an apartment if I were you.

Absolutely not.

And here's hoping they don't start falling apart like their Sydney counterparts. And that the developer can remain solvent to complete the building and remediate any defects.

Crikey, I'd be crapping bricks right now if I were signed up to a current development.

Oh Milkyone, please don't buy an apartment off the plans, actually all FHB, don't buy any house or apartment that is not built and that you cannot walk into and settle on right away. That's not the stuff for FHBs it just adds large amounts of risk.

(probably someone is going to reply that they have done really well by buying of the plan, good on you, but for a FHB it's not worth the risk)

Not in a million years :)

There were similar stories in Sydney by buyers off the plan.

Here is a potential risk that your friend faces at settlement that you might want to warn them about and prepare for.

https://www.smh.com.au/money/investing/off-the-plan-units-warning-as-mo…

https://www.abc.net.au/news/2018-10-04/off-the-plan-apartment-pain-grow…

Also there were stories of buyers off the plan facing price increases being passed on by developers:

"But one buyer said he faced a 12.5 per cent increase. Instead of $465,000, he would was being asked for $535,000 and he was unhappy about that." https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

Of course the other one is credit risk of the developer and the developer is unable to complete the project.

The guys a property lawyer, which is good as he will avoid any of those pitfalls, but does beg the question of how he got himself in such a situation to start with...

At one point they hit some issue with the bedrock they hadn't anticipated. He was desperately hoping they were going to pull the plug entirely, as his deposit was protected. No such luck.

Just another victim of the FOMO mentality.

"The guys a property lawyer, which is good as he will avoid any of those pitfalls, but does beg the question of how he got himself in such a situation to start with"

He is an expert in property law. To avoid being a victim of FOMO and buying at high prices, one needs to be aware and experienced in property valuations and property price bubbles - that is an entirely different skill set.

Same underlying asset, different areas of expertise.

Similar with some property developers and how they get caught out at the top of a property price cycle - https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

The banks will only lend on the newer valuation, not the agreed OTP purchase price. So he may have to find the money to fund the difference. So not only has his deposit gone, he will have to put even more cash into it.

The trouble with real estate is that if you need to sell in a bear market it’s not the most liquid of assets.

Try buying in a bear market then. It is possible to buy low and sell high perhaps even buy high and sell higher

Last I heard, the vast bulk of investment properties were held by baby boomers. They don't have 20 years to "recover" their investment. In fact, they are all likely to be selling up soon to fund their retirements. And if younger buyers cant afford to buy them, then prices are only going one way.

Many boomers are in their 50s (born before 1965) and probably do have 20 years to recover. I think 75 is not too old, I know of 80 year old investors

At 80 they won't be investors.. they'll be holding on to their existing investments.. ie. holders, not investors.

Ttp, Are you John key?

"Wellington and Auckland remain two of the best cities in NZ for residential property investment.

But, notably, “forgotten” cities such as Palmerston North have been faring remarkably well."

Tothepoint,

In which locations in NZ do residential real estate prices double every 8-10 years?

ChCh is a far better place to invest with positive returns and guaranteed capital gains in the future as it gets rebuilt.

You can all laugh at “The Man” don’t care, but at the end of the day, he will be correct.

The Man. I have seen an as is commercial property in Christchurch for sale. Needs strengthening, what do you think. I dont think it can be bowled, uneconomical maybe

I used to own an "as is" EQ damaged house in Chch. It was a very good investment because the vendor got paid out for the building and only wanted land value which I paid.

There are a couple of issues to consider though.

1) Since the house has been written off and settled by the previous insurer, you cannot get new insurance on it which also means you cannot get a mortgage on it, you need to have the cash in full.

2) Being a commercial building, are you legally allowed to lease it? what about building WOF? If you cannot lease it, it's worthless

Good points cheers. Due to the scale probably helps if based nearby which I'm not.

Yvil, You can get insurance for “as is where is” property in ChCh.

We have done that as often there are reasons that the house is “as is where is” and not much wrong with the house and can be easily repaired and insurance obtained.

Would be wary of an “as is where is” commercial property, it depends on many things whether you would buy it.

It depends on the damage, land classification, price etc.

Only if you are a pale variety.. anyone else in darker shade, it's shxt place to live and invest! By the way buttercup, not laughing at "The Man" !

ChCh is a far better place to invest with positive returns and guaranteed capital gains in the future as it gets rebuilt.

You can all laugh at “The Man” don’t care, but at the end of the day, he will be correct.

Your robot seems to have a glitch and is repeating itself.

Give it a bit of a shake..!

'dont Tase me bro'

An alternative valuation comparison of residential property located in Auckland and Christchurch:

1) Auckland - house price to income ratio range is 8.2 - 9.9x, gross rental yield ranges from 2.1% - 4.5%.

2) Wellington - house price to income ratio range is 5.23 - 7.1x, gross rental yield ranges from 3.3% - 4.9%.

3) Christchurch - house price to income ratio is 4.94x, gross rental yield ranges from 5.8 - 6.4%

CN, and the fact is that most investors have bought many of their investment properties many years ago and returns are much higher than you have quoted!

Personally, our returns are from over 6% up to 15%, So returns are extremely good and safe in ChCh.

You have built up a profitable residential real estate leasing business in Christchurch, by buying below true market value in a more reasonably priced location in NZ. Congratulations to you.

Contrast that to those that are building a residential real estate leasing business in Auckland, by buying at or above true market value. Some of these people who have bought in the last few years in Auckland have leveraged themselves to maximum allowable levels, and their residential real estate leasing operations are loss making, and require funding from the owner. That is the polar opposite from the financial economics of your business in Christchurch.

You are correct CN, that is my point, that it is possible to be investing profitably other than in Auckland.

It is also possible to start from a very low point if you are prepared to look outside of Auckland, as that is not the only property market in NZ!

A trend is not a fixed point from which you are observing. This is why if you want to hit a moving target you aim in front of it.

Things are continuing to decline, as credit impulse declines.

House price gains are supported primarily by increase in rate of increase in credit or mortgage debt. This has been slowing since last 2016 and all efforts to revive it by cutting interest rates are running out of impact.

... Auckland remain two of the best cities in NZ for residential property investment.

So net yields in the 2-3% range, while your property is falling in value by around 3-4% yoy is a good property investment? Jesus, you can't make this shit up.

Let not forget that those increases in rent are now down to around 2.5% per year, so the only way yields improve in a realistic time frame will be via further price falls.

"Jesus, you can't make this shit up."

There are many people who honestly believe and place a higher importance of the following narratives (kindly provided earlier by CourtJester above and repeated here) over the quantitative analysis you and many others here have provided on the Auckland residential real estate market.

- Just a blip!

- Low interest rates will stimulate the market!

- High immigration will stimulate the market!

- Housing shortage will stimulate the market!

- Increasing rental yields will stimulate the market!

- CGT ban will stimulate the market!

- FBB was a fizzle

- Low unemployment rates will stimulate the market!

- Westpac chief says it will be 7% up, and he's an EXPERT!

- Our housing market is armour plated

- Tony Alexander says Australia built more houses so we're diffrunt

- I don't know ANYONE who bought a house and regrets it!

- there is an underlying shortage of housing

- there is fixed amount of land for residential dwellings

- there is strong economic growth in NZ

- property prices double every 8-10 years

This is how property prices can get to extreme levels.

And in Auckland

1) there is an underlying shortage of housing

2) there is fixed amount of land for residential dwellings

3) there is strong economic growth in NZ

"there is strong economic growth in NZ" Rock star economy!

Sorry CN, cannot agree. There is a shortage of good quality reasonably priced rental property.

There is a shortage of 3 bed houses being built

There is a surplus of 4 beds for sale.

There is a surplus of apartments (sales of which are imploding in last 6m - down 39% on 2018)

Just reiterated further reasons that are frequently repeated by property price bulls as to why property prices in Auckland will continue to increase in addition to those posted by Miguel.

I agree with you that there is a shortage of AFFORDABLE residential property in Auckland.

Thank you for your data and analysis on the various price segments of Auckland market.

Understood thanks CN

Anyone know if the report is available? Don't see it on the website...

Oh look, developer Ralan Group in Australia has collapsed, owing about $500m, and a cement manufacturer has issued a severe profit downgrade. We'll be right on this side of the Tasman though. Different...

https://www.abc.net.au/news/2019-07-31/construction-slump-hits-profits-…

If only they had the armour plating we do!

lol

We're diffrunt!

Isn't property king, why are developers collapsing???

Oh wait.. it's been a speculative BUBBLE and the chickens are coming home to roost...

Interesting stats for Auckland's top end. I've noticed perhaps a further weakening there recently. For example, this very high quality property didn't sell at auction or in the following few weeks: https://www.realestate.co.nz/3574156 (Maybe the location isn't quite ideal for the top spenders).

Also, this excellent property isn't even going to auction. Pretty sure it would have gone to auction previously. https://www.realestate.co.nz/3600249

Is $2m the new $3m...and similar decline in lower brackets? Is anyone surprised?

Talk to any agent at the coal face off the record, its the same story. The market has lost its rocket boosters, especially in a certain school zone. Private school roles doing well, showing that the difference between fees and DGZ house debt payment must revert back to being much much closer than it has been in the last 5 years.

Hoorah. FINALLY, they are admitting what I noticed months ago and documented!!

Market sales collapsing from top down.

All we need now is price brackets, with sales in each, from 600k to 2.5m, for last 6m.

Just to save you waiting......40% drop in sales above $3m, last 6m, compared to 2018

between 2-3m, sales drop is 38%

1.4 - 2m it s 23%

1 - 1.2m it is 14%

800 - 1m it is 8%

600-800k it is 7%

Are we approaching some transparency!

Nice work Mike.

Mike, why does your $3m+ figure differ from that shown in the article?

I believe their figure is 55% above $3m, from memory. I don't know. I based mine on their website data.

Also, mine refers to total sales, not just residential sales (ie houses)

Trouble is that when writing or speaking about sales, REINZ only references decline or increase I residential only. SO, when land sales and apartment sales were going gang-busters, this is not shown in their statements and when that type of sale goes down the toilet (as it has in dramatic fashion in last 9 months in particular) they do not reference it again.

Yes, your observations have been incredibly accurate. In addition, the trends we have seen in Auckland now appear to be spreading to other cities.

And all of this prior to the RBNZ capital requirement changes coming into affect, which I think will have a significant impact over the next few years.

Mikekirk, the number of sales has been down for 2 years now, that's not new.

It's understandable that number of sales is most important for you as a RE agent because it means less commission, less income for you.

But for most people buying or selling a house, what matters is the price

Latest headline in Newshub : Property prices: Regions hit record highs, Auckland lifts again | Newshub

Latest Headline in Interest.co.nz : Real estate activity slumps to new low in July, top end property sales well down in Auckland

What a contrast : Both are referring to the same market / same time and may be same data BUT :)

FHB should learn to identify Paid/Fae/VESTED News / Article to avoid rushing a buying in a falling market. Patience is a virtue in this market.

Who owns Newshub? Yes, it is American.

Interest is for not your average reader. And it has to be READ, not watched.

Selling advertising and covering it with popcorn is what TV is for.

Note Channel One news "all you need to know" - what about that for condescension?? And "we" know what that is don't we.

Note please that RE NZ is stating what people are pricing their property as: this is the market price. Or really, what it sells for subsequently. And it's falling. So, yes, that's right folks: prices do go down and it is not over by a long chalk yet. Trouble in asset markets is that due to all 'confidence ' memes, no one (apart from rich who sell up and wait) sees it coming until it hits them in the face. Well, here it comes.

I prefer to rely on sale price as a more concrete measure, but as you say, this is more indicative of seller sentiment. Sales volumes, asking prices are all pointing towards downwards pressure in the big cities.

Anecdotally I have certain noticed a big shift in asking prices in Wellington with the majority now asking for less than RV.

Remember that time foreign money laundering in the NZ property market produced all time high valuations and the bank economists said it was a housing shortage and half a million relatively skilled migrants and students? Yea... those were heady days maaaan. I was around to see it. People were talking sh**. But now my children. Here in Venezuela, we can start a new life.

Are you kidding about Venezuela?

If not, would be fascinating to hear about your on the ground experiences living in Venezuela, with respect to prices in an environment of hyperinflation, and the availability of products for daily living.

No man I'm not in Venezuela.

Investors responses are certainly understandable. It's been a pretty golden run over the last 30 years, which is probably the living investment memory of many.

It'll just be interesting to see whether the same ability to extrapolate from the past applies here, or whether NZ's market has seen some unique differences that mean a rare event will occur or future gains can't be assumed from the last 30 years.

Certainly seems like the period 2012-2016 was pretty remarkable and had unusual factors involved. Very hard to tell what's going to happen next, though.

I don't think it's hard to pick what happens next. From mid-late 2018 I was picking at least 3 OCR cuts in 2019 and also for Auckland prices to drop 5-10% from peak. They are down 4%, and it's very likely they will fall from peak by more than 5%.

And I still don't think they will fall more than 10%, mainly because the market will only just be held together by repeated ocr cuts, and by the avoidance of major increases in unemployment.

I’d agree if current macro economic conditions remain stable.

But given the global outlook is worsening and RBNZ capital requirements look likely to go through I see high downside risks in the medium term.

If prices are slowing/falling despite strong tailwinds it won’t take a massive event to exasperate those falls.

Will be interesting to watch Aussie over the next few months. Everyone is calling this the bottom, but I believe there are still a lot of downside risks

25-30% from peak. Median at 670k by end 2021

Things are improving across the ditch:

https://www.abc.net.au/news/2019-08-01/house-prices-continue-stabilisat…

ZS, don't get too excited. It's more than likely a dead cat bounce. As you know, markets don't always fall in a straight line. Australia has a steadily declining Chinese economy to deal with yet. NZ is at the bottom of this entire food chain.

Housing market is on decline..like it or not.....

Retired Poppy. Would you have called 2010 a dead cat bounce too?

Houseworks, in hindsight of course not. More to the point, (sigh) when are you going to demonstrate some foresight ?

How about yourself, in our case the last ten years have been the best.

Because of 1) cheap credit and 2) China's capital outflows.

What's the next booster, you reckon?

The next booster is real cost of living inflation, wage scale compression from the bottom up, and the realization by those late boomers,(still in their last ten years of useful earnings), that without some rental income in their retirement portfolio, that its rice gruel for tea in a small town location.i.e. shyte ur pants soon ahout your real retirement prospects, rather than in your senior nappies later, when you can not fix it because time ran out on you, . I do agree we have not seen the Bottom..of this dip. One last upswing to catch after a prolonged slump.Complacency patterns would suggest that most in need of catching it, will miss it.Again.

Relevant and accurate JimmyH. Real cost of living inflation will be offset by more cheap imports where consumers can do that. Cheap imports since the 1980s have been partly responsible for increased housing costs as it left more discretionary spend in consumers pockets to use bidding up property

Surely that doesn't make Auckland look a very good investment for them? Would they not need to invest a fair chunk as deposit for returns that don't exceed ownership costs by much? Perhaps better buying in Dunners or the mystical Eldorado that is Palmerston North?

Following the Australian market perfectly.

Wait till the RBNZ brings in Debt to income rules that they want. Debt speculators are exposed. Rents would have to increase by a factor of 50 to make the maths work.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.