There are tentative signs that the usual spring lift in property sales is underway, with a rise in new listings on property website Realestate.co.nz.

August usually marks the seasonal turning point for the real estate market as more people start to list their properties for sale over spring and this year was no different.

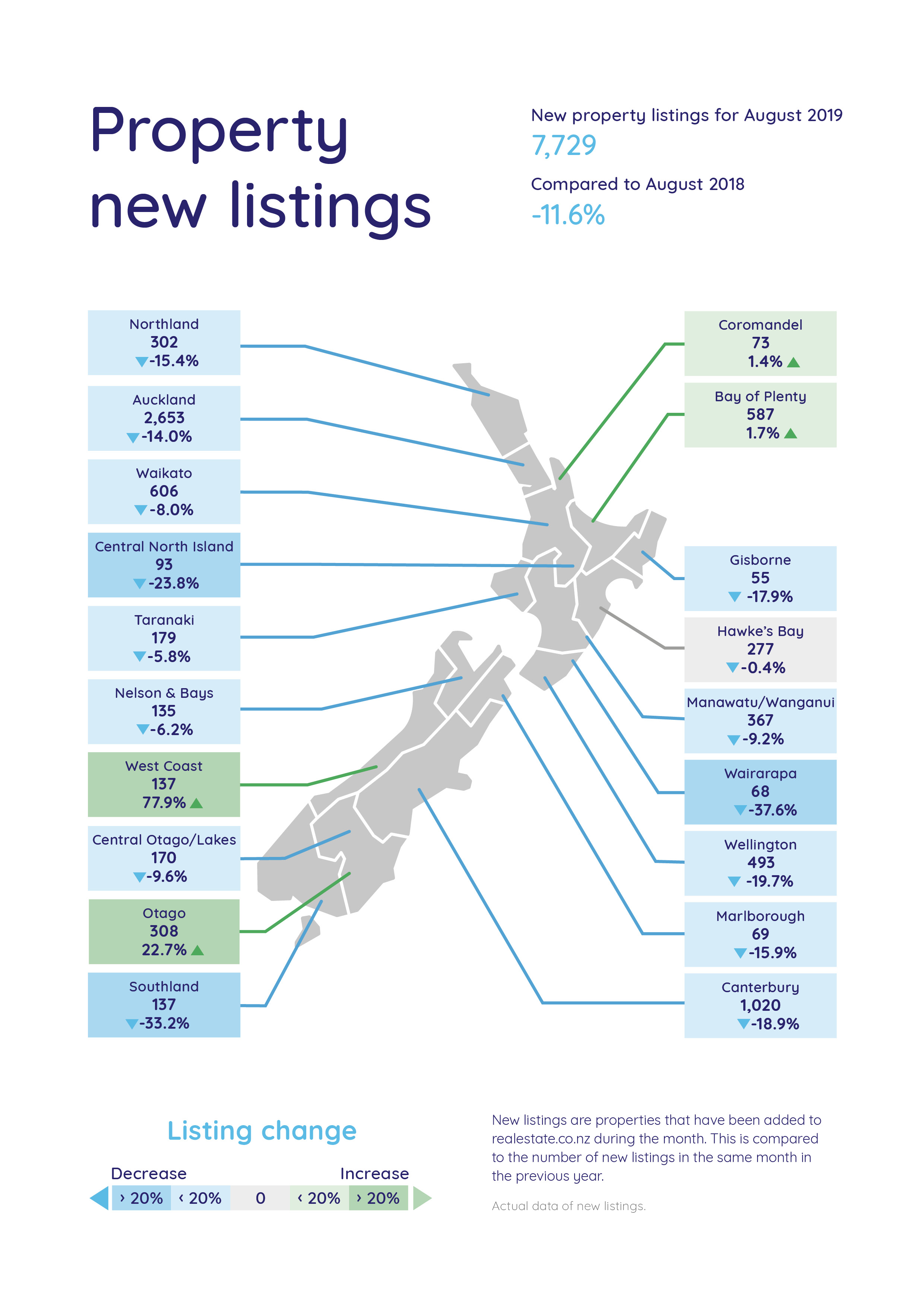

Realestate.co.nz received 7729 new listings in August, up 5.9% compared to July, possibly aided by the Reserve Bank's decision to slash interest rates at the beginning of the month.

The upturn in new listings usually continues through until October but it is still too early to say how strong the spring upturn will be this year. That's because although there was lift in new listings in August, they were still down 11.6% compared to August last year (see chart below for the regional breakdown).

However falling mortgage rates may be having a bigger impact on potential buyers, with Realestate.co.nz reporting 24% growth in new visitors to the website in August compared to August last year, although ironically they would have had less to choose from than they did a year ago.

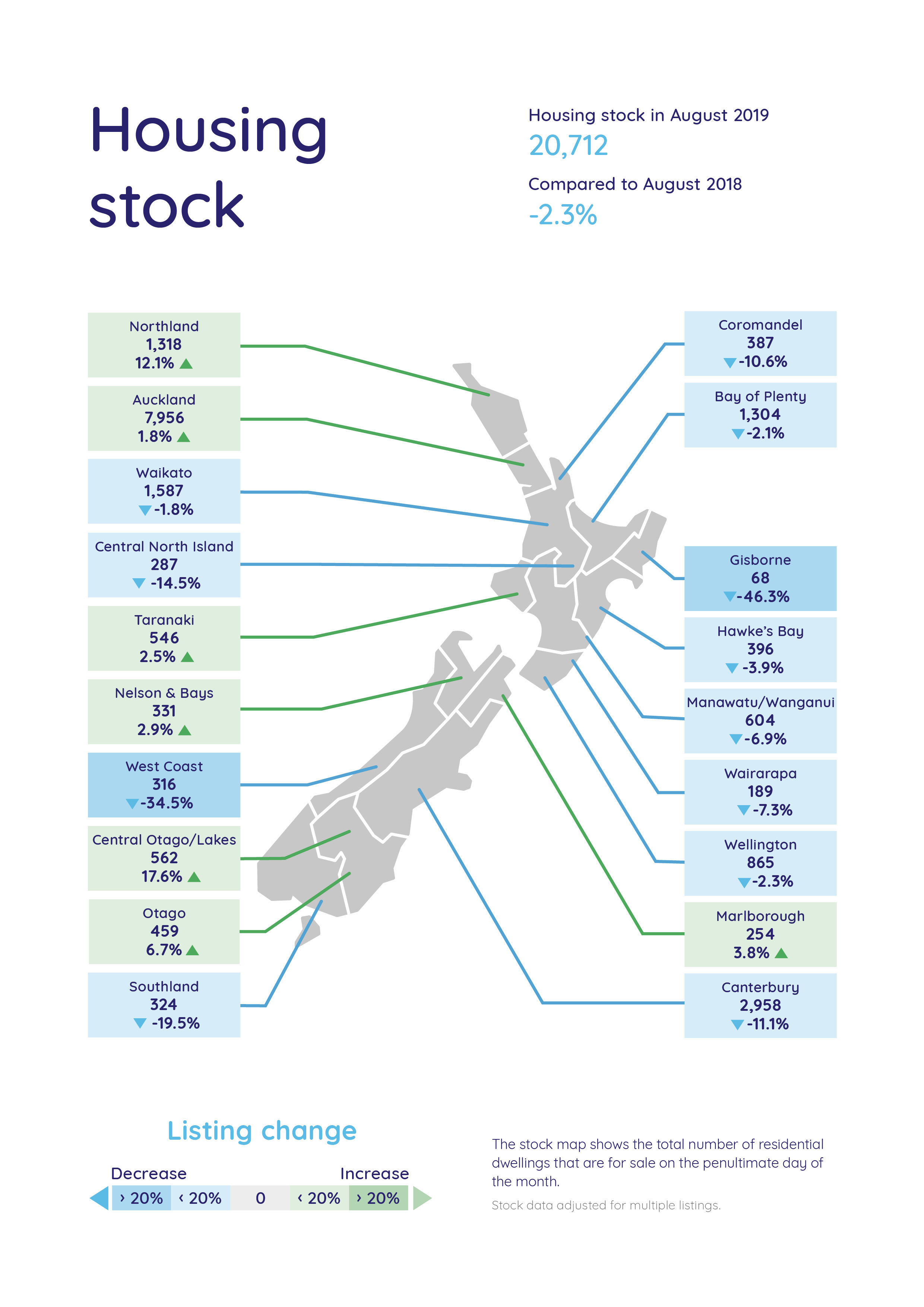

Realestate.co.nz's stock levels, the total number of homes available for sale on the website, fell for the fourth consecutive month in August to 20,712 at the end of the month, down 2.3% compared to the same period last year (see chart below for the regional breakdown).

That is the lowest number of properties the website has had available for sale in any month of the year since July 2016, and suggests although the market has been quiet over winter, there has not been a glut of unsold properties building up in the market.

"The rates cut took the country by surprise," Realestate.co.nz spokesperson Vanessa Taylor said.

"Prospective home buyers can look at the property market with fresh eyes in terms of affordability, either for a first home, or for those looking to move up the property ladder with a higher level of equity.

"August is typically one of the quietest months for the property market, but reports are coming in from real estate agents that it's like an early spring in terms of buyer interest, despite the cold weather," she said.

The comment stream on thsi story is now closed.

45 Comments

There are tentative signs that the usual spring lift in property sales is underway, with a rise in new listings on property website Realestate.co.nz

One of these things is not like the other. Might need to wait till some of those listings have the word 'sold' beside them before declaring the market is taking off.

Greg is to property what Roger is to the $NZD.

There's nothing wrong with Greg's sentence, he does say "there are tentative signs" which is absolutely correct

No, listings are not sales.. they might become sales, or they might not. If there are some signs of increases in sales, perhaps you could point them out.

B&T's sales for august were miserable..

so Listings <> Sales, but spruikers will do anything to boost their chances of creating a false image of the situation

One of the signs of a full blown crash would be a lot of places on the market at one time with very few buyers, so this news means nothing yet.

"B&T's sales for august were miserable.."

And getting worse by the moment.. when i first saw the banner it was "lowest August in 8 years", and now its 9 years..

do you see the pattern???

its the stairways to hell!!!!

I have noticed the open homes have been reasonably busy around my area and good houses have been selling without difficulty. There is also quite a lot of renovating and developing going on. I'd say the low interest rates and uptick in activity across the Tasman portend a renewed, probably less intense, property boom. For FHBs now may be the time to buy rather than holding on any longer. You can't sit around forever waiting for doomsday.

"...uptick in activity across the Tasman ..." ? Maybe...but probably not.

"..Australia is in recession. Can an economy grow by house prices alone? We’re about to find out because everything else is headed south fast."

The answer to that question is No, but the remainder of the sentence looks about right.

https://www.macrobusiness.com.au/2019/09/australia-is-on-the-verge-of-r…

Used car imports have fallen drastically in NZ while new car sales have slumped as well. The average household is holding back on replacing their car with a flash, pre-owned Nissan Tiida

Given all this, why wouldn't economists believe that FHB's will leverage the next 20 years of their meagrely-growing income to buy an overpriced house.

Timing the market is hard, and has to ultimately be based on individual circumstances cost of rent and savings income v's actual cost of home ownership vs the psychological benefits of homeownership vs the pain of your home potentially losing value. Market timing is not entirely subjective though, there are measures to lend some objectivity. You can't know the absolute bottom, but you can make a fairly educated stab at the moment the market is just about to start improving again, which is near as dammit to the bottom as you can probably get. Over the years, I have gleaned the following from various comments on interest.co.nz

If the market is about to warm up again (ie nearest you can get to the bottom of the market cycle);

3 months of declining inventory YoY

3 months of declining mortgage defaults

3 months of rising auction clearance rates YoY

3 months of increasing sale volumes YoY

3 months Days on Market decreasing Yoy

3 months of asking prices increasing YoY

In addition where is the 6 months supply (ie= total number of homes sold per month divided by the total number of homes on the market)

Above 6 months supply = Buyers market

Below 6 months supply = Sellers market

One of these measures is not enough, you need to see most of them move.

Human behaviour is highly predictable. Fear and greed are deeply rooted evolutionary motivators deep in the Amygdala. If you can battle with FOMO you are bucking the trend. Try to use whatever objective measures you can. 3 months YoY data is indicative of a trend. If you want to be very conservative, maybe 4-6 months, but know that you won't get the absolute cheapest but perhaps saved yourself from a dead cat bounce or double dip so look to global head winds and the economic news for signs of a false spring!

Great post Ginja!

Good houses are never difficult to sell. The stagnate or declining prices for some are just the market paying up the debt for years of bad design and construction.

Increases in listings does not necessarily equate to increases in sales. Unless there is the same (or even similar) increase in sales, this is a useless metric.

And listings always lift a lot in spring

Easier to sell a damp house when it's warmer.

My prediction- FHB price range till about 750k will be steady as she goes with the potential to go gangbusters. Price range above that will require some level of vendors meeting the market. Another interesting point, we tend to follow the Australian market, and things are picking up there too driven by low interest rate. About to list our home so will be the heat of things!

RE NZ listings 2 years ago for Auckland were 20% lower. This extra is inventory they cannot sell. What you need is stats on listings 3,4,6 months old. Looking and listing does not equate to sales. Last 3 months Auckland residential sales are 12% lower than in 2018 and exactly flat cf 2017. I watch re nz like a hawk and it’s total listings is still falling. Disappointed in lack of detail in this article therefore or rather selectivity

Regards to Auckland, listings DOWN, Stock UP, asking prices DOWN, which equates to AUCKLAND being DOWN DOWN DOWN

Following Aus so soon? It's not that simple.

Their housing supply boom kicked in 2-3 years ago and was a factor in their price slump.

Ours has only kicked in in the last 12 months.

The low OCR will provide some market support, but I suspect it will be short lived

Yea I reckon the OCR cut will have a minimal effect as many FHB can't even afford a deposit, never mind worrying about the debt servicing costs.

Agree. But see below.

A 10% deposit on a 800k home becomes a lot more doable than a 20%.

Decision on LVRs is critical.

Very good point indeed, all eyes on the LVR decision at next RBNZ MPS

Yes it will the 20% deposit is a major hurdle. However, do you think the banks will allow 10% deposits in the current economic climate?

I wouldn't be surprised. Responsible banking seems to be a thing of the past.

I wouldn't be surprised either. In fact I expect it. Profit comes way above everything else

Was chatting to a broker online, apparently yes, 10% deposits are still okay (with adequate income and credit record), and even 5% deposits are possible, but you pay for it in higher interest rates, no cash payment etc.

Useful Intel. How commonly are they allowing 10% deposits for FHBs? If fairly commonly then potentially lvr changes in November wouldn't have a big impact.

I didn't ask, but nothing in the exchange made me think it was too much of a challenge with a decent income behind you.

November decision on LVRs will be critical for the housing market through 2020.

I think they will loosen the shackles a lot because they know that our urban economy is a one trick money.

Will it matter? Are the banks actually bouncing off the limits as it is, or are their own limits/ the CAR the real limiting thing?

People need spending money for Christmas, right ? Property is the ATM they go to, sellers, real estate agents, et al.

With new listings up 78 percent it could be a tough time on the West Coast property market .Although I feel a Bindi of Gisborne fame moment is close at hand.

Kudos Greg for writing the article at 5am !!!

Listings 11.6% down and site visits from potential buyers up 24% (both on August 2018)… will make for an interesting spring indeed!

This is only part if the story. The real question is how much stock is being held back by developers for fear of flooding the market.

Perhaps a three way comparison of total sales, listings of existing homes and the number of completion certs issued might give some answers.

Hard to say for sure what the market is doing right now. My sense is that there is a fair amount of stock out there where the vendors are still looking for unrealistically high prices. At the very least I expect the screws to be turned on some of these, as buyers realize they are in the driving seat. Even 6 months ago I saw instances of buyers being happy to throw in an extra $100K or more to secure a purchase on high end properties. Perhaps things will be different this spring - time will tell.

Here are a couple of potentially interesting comparisons if/when they sell:

Sold for 2.88m one year ago: https://www.realestate.co.nz/3587467

Sold for 4m just over 4 years ago: https://www.realestate.co.nz/3615407

Is going to be a very interesting Spring, thats for sure.

I have certainly noticed that the certainty of predictive commentary on this site has dropped dramatically, from both sides, in the past few months. It really does feel like the whole thing could go either way, and most commentators are holding their breath waiting to see.

As a cashed-up FHB'er, it is certaintly a nerve-wracking time!

Agree, I feel far less certain in my views.

In particular, I think a minor lift-off in the market is possible now, especially if the LVRs are relaxed.

Not a good outcome, in my view, but here is the reality of our property-reliant urban economy.

But there are some headwinds that may limit the lift-off:

- How much new housing is actually coming on line in Auckland, and how might that affect the market?

- How much will the economy drop and how much will unemployment rise?

The RBNZ seems intent on doing whatever necessary to keep the market pumped and the mortgage debt flowing.

Yes. And the willpower amongst policy makers to keep the market afloat is always a strong barrier to letting the crash that needs to happen, happen.

But the day of reckoning will come, it might just be a few years later rather than in the coming year.

I don't understand why policy makers continue to try and avoid market correction - the longer the market is artificially propped up, the worse off everyone will be. They should have kept it under control in the first instance

Michael Crichton. "I am certain there is too much certainty in the world"

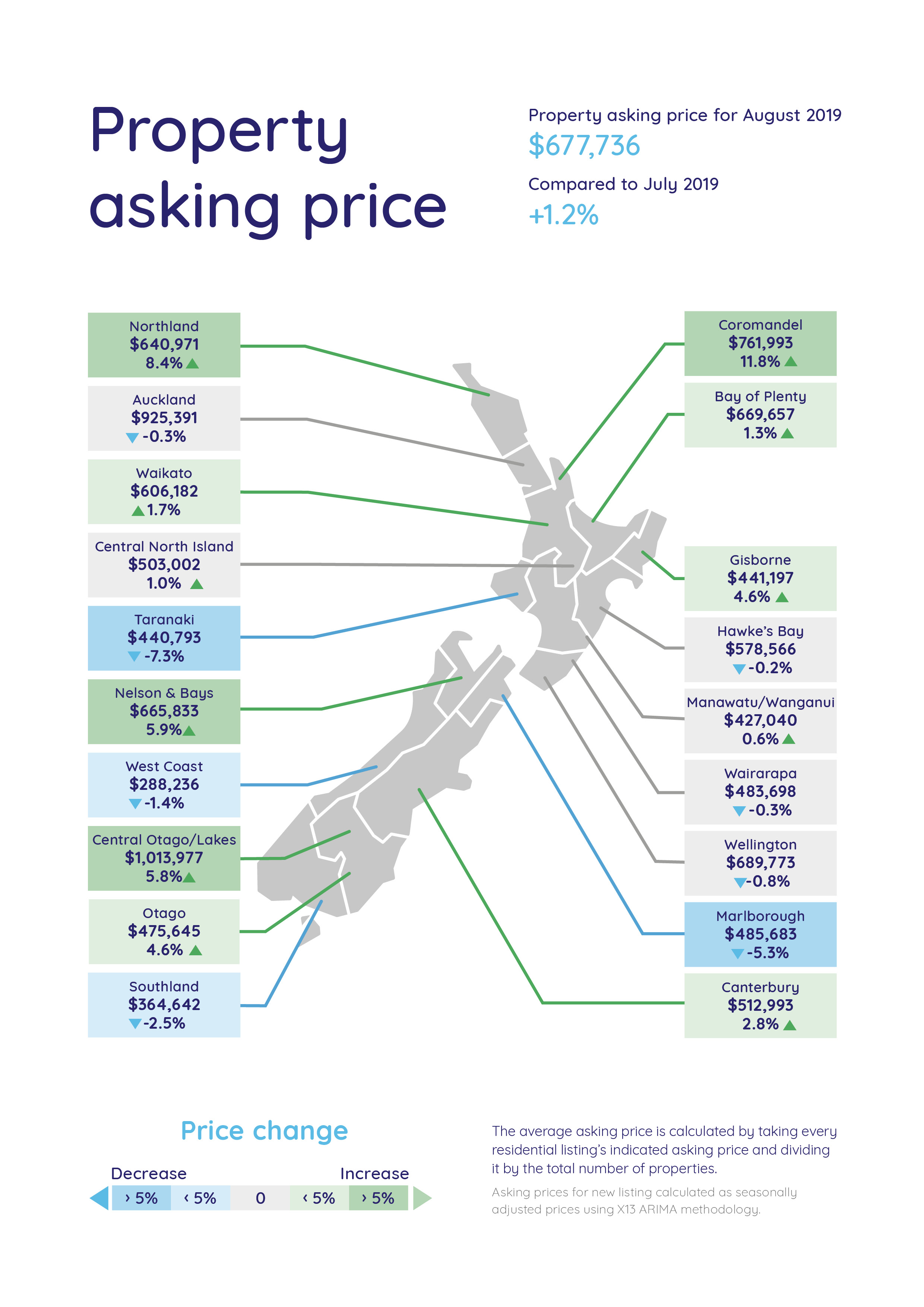

Anyone notice the -0.3 asking price drop for Auckland, down again. If this carries on for a year, we're looking at a continued downward slide. We'll have to see. If there's a pick up, it'll certainly be due RBNZ's aggressive rates drops.

Akld still in the Doldrums

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.