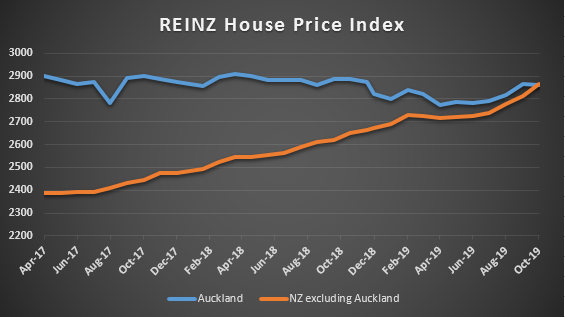

Residential property prices remained weak in Auckland in October after showing some slight improvement over the previous couple of months, according to the Real Estate Institute of New Zealand's House Price Index (HPI).

The REINZ produces two measures of market price activity every month- the median price and HPI.

Both are useful and the median is the better known of the two because it gives a dollar value, which makes it easier for people to understand.

However the median can also be affected by changes in the mix of properties sold in a particular month. For example, if more smaller and cheaper properties were sold and less in more upmarket suburbs, the median might decline even though the prices of individual properties may not have moved.

The HPI takes the mix of properties sold into account and is more likely to reflect overall price movements each month. And it clearly shows differences in price movements in Auckland compared to the rest of the country, as illustrated in the graph below.

Although there have been monthly movements in Auckland prices, overall they have been largely flat, generally staying within a fairly narrow price range. And although there was a slight rise in prices from June to August, they flattened out again in September and October.

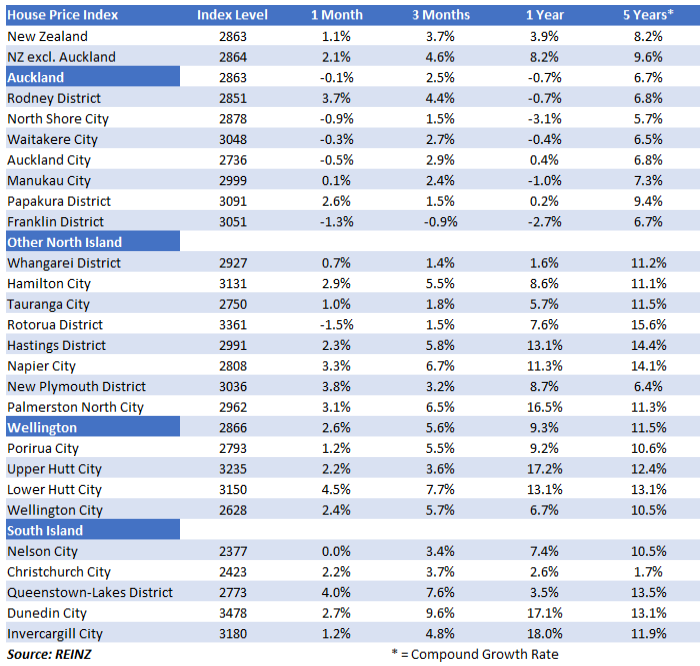

As the table below shows, prices in Auckland have risen by just 6.7% over the last five years, with growth ranging from 5.7% on the North Shore over that period to 9.4% in Papakura. Therefore any capital gains are likely to have been modest at best.

But around the rest of the country, price growth has been much more robust and is still rising. The graph shows steady upward price growth for the rest of the country excluding Auckland, and that growth has accelerated since the middle of this year.

Several centres have posted double digit price gains over the last year with the biggest gains occurring in centres where property prices are still relatively affordable, such as Invercargill +18.0%, Upper Hutt +17.2%, Dunedin +17.1%, and Palmerston North +16.5%.

Of the main centres, Wellington posted the strongest price growth with the HPI rising 9.3% in the last 12 months with the biggest gains occurring in the Hutt Valley. Annual price growth was modest in Christchurch at 2.6%.

The comment stream on this story is now closed.

REINZ House Price Index October 2019

142 Comments

Housing investment in this country is going to become such a terrible investment that even Ashley Church will become bearish! I think we're in for a slow painful fall in house prices the next 10 years....NZ the new Perth?

Possibly. Church's claims (prices doubling every 7-10 years) are biblical in their majesty. Mind you, these are crazy times and what Church says seems to be broadly accepted by the mainstream and would not sound unusual at a neighborhood BBQ or at the local bowls club. It does raise some interesting questions though. Let's assume that we are reaching a peak in this whole 'bubble economics' experiment. What the heck is on the other side? Incomes to start exploding by 7-10% a year in a frantic rebalancing? Armageddon?

My only suggestion is google Ray Dalio and follow his news pieces that come out regularly. He thinks we are repeating the 1930's....hopefully the imbalances created to benefit some don't cause society to break down completely like they did towards the end of the 1930's in parts of the world. But if one part of society continues to kick/exploit another part of society, then human nature will say they will be tolerant until they are no longer willing to be tolerant.

OK. By the way, that's a mammoth shift moving from the world of thoughts of Ashley Church to those of Ray Dalio.

Issue is that Ashly Church has far more influence in NZ investment decision making by a typical kiwi than Ray Dalio does - and there we idenfity the problem.

If Ray is correct, it dosent matter how much influence Church has in the NZ housing or any other market, there will be very few dollars in the system to buy houses.... Supply / Demand... down we go...

You guys are incredible, you can look at a table with 29 regions where ALL of them had gains over the last 5 years, (28 of them large gains), the average gain being 8.2% pa = 48% over the 5 years and conclude "house prices are going down in NZ". How can you be so completely, totally disconnected from reality? Are you really that arrogant to think your own opinion is more correct than data of all houses sold in NZ over the last 5 years?

So the past predicts the future? If you have no awareness of a confirmation bias then yes houses will continue to grow at the current rate forever until the end of time.

The data is 100% positive on ALL areas surveyed and you guys conclude: "it's going to go down" it's just a completely ridiculous conclusion.

It's a bit like having an All Backs coach that wins 100% of his games, you guys would sack him because… you'd say "we can't be guaranteed he'll win in the future"

How good was Steve Hansen....up to the point that we lost the world cup semi! Who would have seen that coming....pretty much won every game up to that point....what a disaster.

Black Swan or Fooled By Randomness (Taleb) might be good reads for you Yvil.

... yes .. investors seem to have forgotten " reversion to mean " ... when an obviously overpriced asset class sinks back to its long term trend line ... then sinks another 10 or 25 % below that ...

Markets typically over or under shoot ... they seldom sit upon the trend line .... houses in NZ are way above that line ... way way above the long term average ...

In fairness, people discussing Auckland's recent direction are more discussing the last one or two years, rather than the 5 year figure. In the October of 2019 and 2018 we've seen Auckland's HPI declining from the years before.

I make no claims to know where the market is going, but merely find Auckland rather an interesting market at the moment. Certainly not a market in which one could say that all the indicators look fantastically positive.

You will also notice that if you study other markets that prices have gone up in all markets before they have gone down! Its amazing! But just becuase they've gone up, doesn't mean they will continue to go up!

You do the studying, I'll keep making money

Do you admist there is a chance that housing prices could fall significantly in NZ? This is purely out of interest...even just a chance. Or do you 100% think house prices will continue to rise no matter the economic conditions/business/debt cycles.

In my opinion, there is a larger than 50% chance of house prices increasing, a small chance of them reducing by a small margin a still smaller chance of house prices increasing significantly and a minute chance of them falling significantly. There is also a very small chance that I could die in the next 5 years and a more than 50% chance that one of the commenters will have passed on in 5 years time. (I hope yo get my point)

Ok thats good to see you're open to all possibilities. If you weren't open to all possibilities then there would be no point in having any discussion or debate on the topic. I agree prices could go either way. They could continue to rise, but equally they could fall. But my personal opinion is that they're likely to fall at some point and the fall could be gradual (like Perth) or could be dramatic (like Dublin). These are all possibilities - I'm not saying they are going to happen.

The issue is that people have assigned different probabilities to possible outcomes.

For example, on a 10 year investment horizon, what is the probability that each person assigns to each possible return scenario of median house prices in Auckland?

-6% p.a.

-5% p.a.

-4% p.a.

-3% p.a.

-2% p.a

-1% p.a

0% p.a

+1% p.a

+2% p.a

+3% p.a

+4% p.a

+5% p.a

+6% p.a

+7% p.a

+8% p.a

etc

Those who expect property prices to double every 10 years have assigned a higher probability of +7% p.a (say a 80-100% chance of occurring)

Those who expect property prices to crash have assigned a higher probability to negative returns.

In reality there is a range of possible outcomes each with different chances of occurring.

These probabilities change according to changes in the underlying variables (such as the current house price, implementation of foreign ownership ban, etc)

Just because there is a 90% chance of something occurring, it doesn't mean it will occur.

Conversely, just because there is a 10% chance of something occurring, it doesn't mean it will not occur.

Take the example of the All Blacks in the recent Rugby World Cup:

1) there was a high chance (say 85%) of winning the Rugby World Cup

2) there was a low chance (say 15%) of not winning the Rugby World Cup

Just because there was a low chance of the All Black's not winning the RWC, it doesn't mean it can't happen.

Many property investors ignore and discredit Bernard Hickey now due to his viewpoint in 2009 / 2010 about property prices falling being incorrect subsequently. He was expressing his high probability outcome. The fact that he was subsequently incorrect misses the point of the counterfactual that could easily have occurred and Bernard Hickey would have been right. Imagine if the government had chosen not to guarantee bank bonds and bank deposits in 2009 - banks would have had their funding cut off and be forced to deleverage, depositors may have moved their funds out of banks, banks would reduce credit lines and contract credit to the economy. In that environment, unemployment would have risen significantly, and property prices would have fallen significantly, and the economy would not have recovered as quickly as it did. Also in that scenario, the likes of Ashley Church, Tony Alexander would have been wrong and they may have lost their credibility.

I’ll take Ray Dalio over Ashley Church anyday!

Yep.

Ashley Church would know who Ray Dalio is, dose Ray know who Church is?

Can anyone enlighten me as to how Church commands any authority on economic or housing matters?

He seems to have been a professional chameleon, having been a councillor and CEO of a few organisations - yes property related, but a CEO is a management role not a role of professional expertise. As is a councillor, for that matter.

He might well have an extensive property portfolio.

Bit like Mike Hosking - he some how has listeners but you don't really know how or why....bit like how did the Kardashians become famous? If aliens ever came to earth, they would look at the sitatuion and think WTF happened here. Instagramers following Kim Kardashian, investors following Hosking/Church but nobody knows why.

"investors following Hosking/Church but nobody knows why"

They have been given access to mainstream media platforms which reach a broad audience to disseminate their opinion.

If they were nobody's, and nobody had ever seen them on mainstream media, then they could try to start a following on social media from scratch. Not sure how likely they would reach a broad audience, or achieve a large following.

Ashley Church does make presentations at property investor conferences. Similar to Tony Alexander ...

At least Tony is an economist...

Independant O.

With Ray being a major voice / player in the market you also need to see and grasp where he is coming from.

My guess is that Ray is ready for a crash and wants it to crash to make a tone of $'s. He'll be sitting back in cask like Buffet and like Buffet they are managing other people's funds who are starting to say 'get the hell back in there, I'm missing out on the fun times'.... For now both of them are resisting but for how much longer can they maintain order in the ranks???

Buffet and Dalio are getting their view that it is going to blow because they want it to blow.

As per usual, a grain of salt needs to be added.

I'm not quite sure what your point is - people invest with Berkshire and Bridgewater because they want to. Anyone could sell their holdings at any given point in time if they didn't like their investment approach - but would you have the arrogance to think that you're a better investor than Buffet/Dalio? And if you pull your money from them - where do you put it?

Dalio thinks we're at the end of this cycle or pretty close to it and it positioned as such - being well diversified vs highly leveraged in one asset class (like the majority of kiwis)....I know where I'd put my money...

"Incomes to start exploding by 7-10% a year in a frantic rebalancing?"

1) Would that result in higher inflation?

2) Would the RBNZ act to maintain their inflation target of 0-2%?

Good, that way speculators could either take their money out of the residential property market and leave or invest in something productive.

Unlike Perth where the economy ends at property and mining, NZ has multiple new-age sectors with the potential to deliver long-term gains but are short on growth capital.

Yeah but it is still a while and when the bubble actually bust will be painfull and may take a decade to come out of it, whenever it happens.

auckland housing is similar to iron ore... what used to be worth is weight in gold, is not desirable anymore..

Christchurch stands out as the anomaly, 1.7% annualised growth is nothing, especially over the last 5 years. Auckland yes, we all get that, a market which overshot fair value. Napier vs New Plymouth, might be the weather, more likely to be jobs.

Christchurch sounds more terrible than it is, why? My theory is all the as is where is properties, selling well under the RV. Take a look right now 55 properties on Trademe "as is where is" in Christchurch, and all will sell for about 60% of their RVs, not only that, they will sell, because the owners will sell at almost any price. Go to any auction, it's the "as is" properties which sell, and the others get passed in. It doesn't take many selling at 40% under RV, to skew the numbers for those selling 10% above RV, which is closer to the mark for a house in good condition.

You are correct DIYman, I have been saying this for a long time, that the figures are massively skewed by the “A’s is where is” sales.

However, many people have made a lot of money out of them.

I don’t agree that sellers will sell at any price, as I believe that so many vendors want too much for them and quite often get it!

Some of the biggest winners have been the people who have had insurance payouts far in excess of what their home was previously worth and then they get to keep their damaged house, which they then get an inflated amount for.

Personally we have only bought 2 “as is” properties and yes there is good profit in them if we ever sell, however we are getting an excellent yield on them being rented out.

If investors can not see that Christchurch is the place to invest then there is something wrong.

It is going to be the city of choice In The years to come from both young and old as it continues to get rebuilt.

Yes there have been too much land opened up which has kept prices down but DIYman is correct!

THE MAN is 100% correct, some of the as is properties do sell for a lot more than they theoretically should.

For example. I know of one, worth 650K before the EQ, then owner receives a 900K payout, and sells the as is property for 375K, that's a winner if ever there was one. Plus, the new owner is very happy with the house, it has a stunning view over the estuary to the mountains, was completely renovated just before the EQ, and has a small crack in the floor, keeping it "just for entertaining" .

We picked up a very nice, completely level, well insulated sunny home, with a council park in front, double garage, in St Martins, needs a new driveway , but that probably wasn't because of the EQ for 182K, been renting it for 350 a week for the last 5 years. No problem getting quality tenants for a quality house either.

If you want a new house, then think about this one, a lovely old house on the hill above St Martins, was worth about 600k, part of an estate and was rented before the EQ. Insurance company demos the old girl, spends a packet on retaining walls and a modern new house, we were told 1.5M. Executors of the estate decides to sell on completion, sells for 1.05M.

When you add the value of the land, its pretty much a half price house, and brand new, beat that anywhere in NZ, buy it lock the door, and wait ten years and more than double your money

But, no one wants to live in Christchurch.

About 400'000 people do. It may not be your choice but accept other people's choices

Nelson and Hastings might have an edge, can't think of any other places in NZ ahead of Christchurch, with a great climate, every outdoor activity under the sun at our doorstep, good public transport, no commute issues, and affordable housing, correct me if I'm wrong but probably half of Christchurch doesn't have a mortgage.

Sums you up in a sentence Man..."Yes there have been too much land opened up which has kept prices down"Boo hoo some FHB now have a new home and a manageable MTG while you yearn for only capital gains.

Your argument might make sense if it was still 2014. But its 2019. There were far more "as is where is" properties selling from 2011-2015 than from 2015 to 2019. So if anything, prices should have fallen from 2011 after the earthquake as people sold up but they didnt - prices went up. Then prices hit the peak around 2015 as new supply started coming on. Far more brand new houses, selling for much more than the old houses they replaced, or new builds in the multitude of new subdivisions, should also have pushed up median prices - but they didnt. The simple fact of the matter is that prices are stagnant because supply matches demand. Jacinda couldnt even sell a Kiwibuild in Christchurch.

I started following this site 3 years ago, even then contributors were overwhelmingly house price negative. Auckland aside, what an absolute travesty if any first-time buyer was dissuaded from buying due to the bitter amateurs here. When do you put your hand up and admit you got it wrong?

Given that the price negative discussion was generally about Auckland (from what I have seen on here), they don't seem to have had it wrong so far.

Plenty of bitter amateurs to go around on both sides.

However, your point does highlight that we need to be doing more as a country to make home ownership more affordable for more people, as we did in the past. It's a travesty to make it an investment vehicle above all and push home ownership out of the reach of young Kiwis.

Yes, some comments are Auckland specific but on balance most general in nature, and where are the bitter owners? The reason prices have risen so is varied - from favourable local tax treatment through to global ZIRP. I'm not defending it, just that it shouldn't be a surprise.

If you're looking at this over a three year time frame, your thinking is probably a bit short sighted. Perhaps ask this question again in 10/15/20 years time and decide then whether now or the recent past was a good time for FHB to enter the NZ housing market.

Remember most of the boomers are going to be dead in 15 years time and they own a lot of property.

Very well said Te Kooti, they will never admit to being wrong and of course they will keep being wrong. Their only hope is to forever push out the date of "the big crash is coming" mantra, until they die

Bit like the everyone should buy shares in 1929 and 1987 and 2000 and 2007 mantras? But if you took the counter to that argument during those times you were a fool?

Who do you think has made more mistakes in their life, a successful and wealthy person or someone who never took a risk?

How do you define successful and wealthy? I know quite a few people who would be considered to be successful and wealthy but their wives have left them and their children dislike them. They could have made many mistakes along the way of creating their success and wealth - but life is complex with many twists and turns right?

I also know of people who wouldn't be considered by western society to be successful nor wealthy, but they have great family lives. One risked everything for career/financial wealth, the other for their family. Who made more mistakess? I'm not sure. I guess the one who has less regrets when it comes time to pass.

Is risk meant to be linked to success and wealth?

If your family leaves you you're definitely NOT successful

where are the bitter owners?

In the new thread on the government's rental regulations to bring NZ in line with more mature rental markets.

Exactly, much of the 'price-negative' commentary has focussed on Auckland.

And not all of us, including myself, have been predicting a crash.

Although I do predict a crash the next time a recession hits (I'm predicting 2021/2022)

I don't recall many if any posters simultaneously talking the regions up and Auckland down.

I recall some talking about regions following Auckland, with a lag.

The DGM problem on this site started over a decade ago. Below is a random example from back in 2011 before prices took off. Naive prospective first home buyers may have listened to that joker. Imagine the regret. Sadly, there will be prospective first home buyers listening to the rubbish advice of the DGMs on the site today. The cycle continues.

by Realistic view | 11th Nov 11, 10:37am

“...We have a house price bubble and it is slowly deflating. Imagine a balloon being constantly pricked with a pin and these holes being patched with a band aid, eventually it deflates. That’s your famous housing market.”

https://www.interest.co.nz/property/56675/opinion-olly-newland-says-now…

Here's another beauty from 2011 -

by Houses Overpriced | 13th Jun 11, 6:11pm

"Prices will keep falling"

https://www.interest.co.nz/property/53858/volume-house-sales-rises-may-…

They both got stopped out.

The DGM problem on this site started over a decade ago

There's plenty of DGM right now if you look in the right places. That doesn't mean the future direction of house prices is all about having a sunny disposition in suburban NZ.

I started following this site 3 years ago, even then contributors were overwhelmingly house price negative. Auckland aside, what an absolute travesty if any first-time buyer was dissuaded from buying due to the bitter amateurs here. When do you put your hand up and admit you got it wrong?

I would think being "negative on house prices" is not necessarily a bad thing. Let's assume house prices had gone backwards in P3Y. You're likely to be singing from a different choir if that were the case. All you're really exhibting is that house prices have been financialized to such an extent that it's necessary "not to lose" without negatively impacting lives. That to me is not a healthly economic life.

My point is if you were an ex-Auckland FHB 3 years ago with a deposit and you held back, that was undisputedly a very poor financial decision. There is never any acknowledgment of that.

I stay away from the house price threads, they are an echo chamber of resentment. Everyone should do what's in their best interest.

That isn't true Te Kooti - house prices in NZ could yet fall, and fall quite a long way. Even if you purchased 3 years ago and had a gain now - who is to say that housing across NZ doesn't fall soon by 50% and stay that way for a significant period of time? Then who is the fool? The person who purchased at the top of the market, or the person who purchased with a 50% discount?

If prices fell 50% then I would be looking to buy that many it wouldn’t be funny.

The yields would be phenomenal

So the bank would lend to you if property prices fall by 50% - and yields...that would assume income is being earned by tenants to pay current levels of rent? Are you sure that would be the case?

Yep.. and who is going to lead the bank the $'a to the bank at 1%.???

Any loans that will be approved will have a 50% LVR and you would need to show a level of saving above your out going expences.

KR,. It's almost certain the RBA will introduce QE in the coming months. That QE isn't going to be sovereign bonds (there aren't enough), it's going to be RMBS. Banks will write $250m clips of mortgages, securitise them and sell the AA and AAA to the RBA. Or, they can repo them. Funding sorted, it will not be an issue.

They will do whatever it takes to keep the housing market functioning.

.

"Banks will write $250m clips of mortgages, securitise them and sell the AA and AAA to the RBA. Or, they can repo them. Funding sorted, it will not be an issue.

They will do whatever it takes to keep the housing market functioning."

1) Would Central Banks in free markets be able to provide limitless emergency liquidity support for banks? What interest rate would the Central Bank charge for emergency liquidity support funding?

2) Would this would create a potential moral hazard by the banks in the local economy collectively?

3) if bank trading counterparties know that the Central Bank is providing liquidity support for a bank, trading counterparties may pull bank from doing business with the bank for fear of non payment (I.e increased credit risk)

4) if wholesale funding for banks realise that the Central Bank has given a bank liquidity support, then wholesale funders may choose not to provide financing to the bank due to fear of non payment (I.e credit risk increased)

5) the actions of 3) and 4) may cause loss of confidence by retail depositors leading to a potential deposit run on the bank. Imagine if you had all your savings deposited at a bank and your friends told you that they were pulling their savings out and you saw lines at bank branches/ATM's of people taking their savings out, would you feel compelled to take your money out also? Most of the general public who have savings at that bank would. Then it might cause a run on other banks ... Australia has a deposit insurance limit of A$250,000, so that may provide confidence to small depositors, but big depositors may choose to reduce their balances to below the limit.

From the Bank of England on Northern Rock:

"The larger deposit-taking institutions, such as banks and building societies, are ‘special’ organisations in modern life, similar in some ways to utility providers. Banks should be allowed to ‘fail’ so as to preserve market discipline on financial institutions.

However, it is important that such ‘failure’ should be handled in an ordered manner, managed in such a way as to prevent further damage to the economy, the financial system and the interests of small depositors."

Out of the ECB on lender of last resort - https://www.ecb.europa.eu/explainers/tell-me-more/html/what-is-a-lender…

If prices fell 50% yes Banks would lend to us without doubt.

Yes our existing property would fall in value as well however equity and servicing would not be a problem.

However there is no way that prices would ever drop by that much as people would be buying as it would be so much cheaper than renting.

If people couldn’t afford to rent or buy, then the country would not be worth to live in.

People that make predictions about prices dropping are just people that are hoping to buy because they currently can’t afford to buy!

In this situation some of your tenants would stop paying rent, putting you under pressure to service your mortgages. The bank would not lend to you as you start defaulting on your payments.

You conveniently miss the point that if prices fell 50%, the whole economy would be under massive stress. Nothing else will be the same, people might not have job to go to and in turn pay your rent. You can't exactly kick them out and good luck for recovering for the lost rent! The whole is like a balloon, squeeze one area and it will be stretched somewhere else..

Basic Econ101!

Did you go to school?

^^What he said.

And banks will experience losses on their loan portfolios. If banks are making large losses, then banks may have capital adequacy issues. Most people in NZ under the age of 50 may not know about the fallout of the 1987 stock market crash, impact on bank loans and bank capital which resulted in the subsequent recapitalisation of the BNZ by the government.

Ask BigDaddy about his experience with the banks during the late 1980's and early 1990's ...

CM you are not allowing for the government reaction. Remember U.S. and Australian governments pumped that balloon 2008 to 2016 and beyond.

It wasn't as simple as squeezing a balloon.I dont think pumping trillions of dollars into the system is covered in 101.

Sorry IO, that's flawed logic. Like I bought Apple shares at a 30% discount to market and telling me they can still crash 50%. I can take profit on both the shares and house today if I choose. Yes, of course house prices will fall again at some point. However they could go up another 15% first.

See Te Kooti, IO is the perfect example of the person never ever admitting to be wrong. What he believes is much more important in his mind than reality

Ouch good dig - thanks Yvil!

I've been wrong in the past and I'll be wrong in the future (not sure why you think I'd never admit to being wrong - do you take my posts personally?).....I just won't be highly leveraged on the bets that I'm doubful about - will you?

Te Kooti said: if you were an ex-Auckland FHB 3 years ago with a deposit and you held back, that was undisputedly a very poor financial decision"

You replied "that isn't true"

Well it may not be! Give it 10-15 years and we'll find out! Or do you need to know who is right and who is wrong at this very minute then change you're opinion of who is right and wrong based upon the irrationality of markets and human psychology?

Speaking of Apple - have you seen how much cash they are holding at present?

Are you telling me houses are just as liquid as shares?

Are shares purchased with leverage by most people - magnifying gains/losses?

Yes, amazing. You are correct on the liquidity, Apple is liquid and houses are not and that is a risk. Shares can be purchased with leverage, with physical and ETF's/CFD's. It's no secret that banks willingness to lend against property is where the returns and risk comes from. Basel risk weightings are skewed this way and so is government policy. Just more reasons not to fight the system.

JC, to be fair though, 8 years later than what you have stated is not that accurate!

JC, to be fair though, 8 years later than what you have stated is not that accurate!

Not talking about 8 years ago. I'm not really big on this kind of childplay where people say "you should have bought Xero shares at a few cents." Kind of misses the point and doesn't indicate whether buying Xero at $77 is a prudent decision.

The DGM comments of 8 years ago were based on a combination of bitterness and conspiratorial/half-baked ideas about how the NZ/international economy works. The DGM comments of today are no better.

Typically go something along the lines of -

Because China!

Because Sydney!

Because NZ is 2007 Ireland!

Because prices are too high to be sustainable based on what I personally feel is a fair price!

Because money laundering!

Because [insert random city] has a lower price to income ratio than Auckland!

Because houses are for living in, not investments!

Because we will have no tools left when RBNZ runs out of interest rate cuts!

Because some people have high indebtedness!

Because ma feelings!

The DGM comments of 8 years ago were based on a combination of bitterness and conspiratorial/half-baked ideas about how the NZ/international economy works. The DGM comments of today are no better.

Sounds like you've picked up on the Hosking 'common sense' approach to economics. And what does that actually mean? That anyone who talks about inherent risk in the economy is bitter and a conspiracy theorist?

Hi J.C. & I.O.

I say the following in a nice and honest way. You remind me a lot of my dad, he was a great dad and I miss him a lot since he's gone. There's much more to life that money but this is a business website and the article is about house values, hence money, so I'd like to focus on this. My dad would analyse everything, forever and he would always find risk somewhere and as a result, he never took a chance. We all find what we look for and you will always find a reason not to do something J.C. I.O., not buy a house, not approach that girl, not travel, not start a business, not have kids etc… I was lucky that my wife came form a risk taking family and open minded enough (just) to listen to her and give it a go. When we take a risk, it's is hugely rewarding, we also generally make it work. I hope you will find the strength in you to look for positive outcomes at least as much as you currently look for the bad outcomes, you have only one life to live, go for it, trust yourself, you'll be fine.

Yvil

Most of the financial world focuses on risk analysis. Without any understanding of it, you would never really become part of it or get through their doors (unless you were delivering coffee).

It's very unfortunate you did not really get my post, I shall stop wasting my time. I hope you can at least sometimes, see the bright side of life

Your post had little relevance to risk analysis. And yes, if it has no interest to you, don't waste your time discussing it.

It is just his normal completely patronising drivel.

J.C. sounds like he has had experience in financial markets or investment banking.

Interested to know how many on here have had experience in financial markets, and investment banking.

Click thumbs up on this comment, if you've had experience in financial markets or investment banking.

My sense is that there are a few.

cmat previously was involved in investment banking

Wilkes was previously involved in banking in the UK.

Others that I can think might also have been involved are: bw, & Tainuibabe.

I'm so, so happy I'm not part of that group. I have studied Architecture for 5 years in one of the best schools in Europe and came out having no idea about the real world. Being a young 50 yo (lol) I value "been there done that" infinitely more than the theoretical BS we learn at school which really only prepares us to be a good employee.

The point is, that group of people have had training and experiences which shape their viewpoint. They can see dots that others don't see and make connections between those dots, especially in financial markets, free markets, and potentially credit bubbles and market vulnerabilities. Given the international nature of financial markets and their influence on economies, they can see important dots overseas and make connections, and the potential impact on the NZ economy. Imagine the insightful viewpoint of a current or former bank CEO like David Hisco, or a current or former RBNZ governor or chairman.

That would be akin to you with your experiences in architecture when looking at say a Norman Foster or IM Pei designed building. You would have an informed opinion and be able to see dots that others don't see and make connections between those dots. In that situation, I don't even know what I don't know.

Good advice Yvil - I can see where you're coming from and appreciate the words of wisedom. Thanks!

Thanks back IO, it's very rare someone is open minded enough to others views, can I know how old you are?

I’m 35 - we all have our reasons that shape who we are and our views. I get where you’re coming from - but just suggest we should be cautious going forward. Risk at the right time and in the right amount is a good thing - I agree.

Jesus Yvil, that was actually quite moving and probably the most insightful comment I have seen in the 3 years. You are absolutely right, the friends and acquaintances I know who have done really really well all have huge risk appetites.

I am not exactly DGM, because I think now is a good time to build a new house. But do think Auckland house prices will fall relative to other investments for the next few years.

Between 2011-17 Auckland Council restricted land supply to much less than normal and houses had windfall capital gains based on a soaring land price. Then in 2018 Auckland Council opened up greater land supply than normal, land prices have fallen since and Auckland now builds much more housing. The current situation is that the replacement cost of Auckland housing is substantially lower than the price of existing housing - which allows a clear indication of where Auckland house price is likely to head, downwards.

The current situation is that the replacement cost of Auckland housing is substantially lower than the price of existing housing

Can you give me an example of an existing Auckland house that could be rebuilt for less than the capital improvement value specified on homes.co.nz?

No, I don't think that is much chance of that happening.

Due Diligence,

In the past few years, there have been some property owners who sold and potential first home buyers in Auckland who have chosen to wait.

Some of their decisions have been a result of having a fully informed decision - i.e both the property price bull side of the discussion and the property price bear side of the discussion.

Some people who come to mind are Carlos67, & Milkyone. Not sure if there are any others - if there are others, then they should feel free to comment if the discussion of property price risks in Auckland have been of any use to you.

People should be entitled to hear both sides of the discussion to make a fully informed decision. The mainstream media, property market promoters, REINZ, property mentors, property development companies, real estate agents, bank salesman masking as economists who are employed by banks, mortgage brokers, banks, non bank lenders, have a vested financial interest in promoting the property price bull scenario.

Then there are a handful of property price bears, who have no vested financial interest whatsoever (with a few possible exceptions), in discussing the risks of a property price bear scenario. The viewpoints of these people are clearly drowned out by the huge vested financial interests of the property price bulls outlined above who get large amounts of mainstream media time and audience attention and have large marketing budgets promoting their businesses. There have been some property price bears who have made comments on the mainstream media sites, only to have had them removed by the editor (so that silences the viewpoint of property price bears from other readers and the readers then only get the one sided narrative on the property price discussion promoted by the mainstream media).

Should owner occupiers know all the risks before buying real estate in Auckland? Absolutely. One of those risks is the risk of overpaying for a house. CAVEAT EMPTOR.

Readers are free to choose to ignore the information or they can choose to take what they consider to be useful. They can then bear all the risks and benefits from having made a fully informed decision.

Otherwise without discussion of the property price bear scenario risks, potential buyers are at risk of being informed of only one side of the property price discussion being promoted by those with enormous vested financial interests. And if owner occupiers get caught out with property prices falling significantly below their purchase price, and are forced to sell for some reason, they then may start looking for someone to blame for their partially informed decision.

Many contributors on Interest.co including Bernard Hickey, were stating that house prices were grossly overpriced back in 2010, 9 years ago.

Have prices dropped since then in NZ?

No, they haven’t, quite the opposite and those that took absolutely no notice of the people that thought they knew everything, have come out on top without doubt.

The last 9 years or so has probably been the best time to be investing in property whether it be for owner occupation or as a rental investment.

Professional investors that have done it right have now set themselves and their families up financially for life.

What I do know is that every property market has its opportunities, but then there are just so many on Interest.co just are not prepared to take advantage of the opportunities that present themselves.

Here's the thing about any long term trend - those who blindly follow it have to be right, every day. Those who see it changing only have to be right, once.

Get caught with a large property portfolio if ( or as you suggest, when) the market corrects and it's "Goodnight, Nurse!". I know property developers ( ex-property developers now!) who 'got caught with stock on hand during what turned out to be a mild correction when the GFC hit, and even before the EQs ( and, no. not Serapisos); in Christchurch, actually - out north - Kaiapoi/Rangiora and Pegasus Bay way. Before that, it was some in Queenstown in the late 80's and late 90's - ditto. It cost them all more than money.

Yep, it's not widely known because people don't want to talk about it, but many people took hits around 2008/2009 that they are still recovering from.

I know a couple of guys in their late 50s who got severely burnt in that period.

And as you say we only had a moderate correction here.

All we ever hear of here and in the media are the success stories. Of course there have been many of those, but there also been a not insignificant number of failures.

People that invested in Pagasus weren’t exactly that bright to be fair.

It was an overhyped subdivision that is in the wop wops and was never ever going to take off.

As for Kaiapoi and RAngiora, also probably not the safest and best to invest in.

There are always different levels of investors just like in any business or sport etc.

bw, the fact that you are comparing property developers to property investors shows you do not understand the very large difference in risk.

Interesting assessment. I have several friends who bought 2-3 years ago in Auckland, and I think that if they had it to do over again they would have waited, and others that have waited and are glad they did. I certainly have seen several higher-priced properties (e.g. not FHB territory) which sold in 2016 and resold in 2019 at significant losses.

So, unsurprising that we can't agree on predictions of the future, we can't even agree on what has happened in the recent past!

In the past few years, there have been some property owners who sold and potential first home buyers in Auckland who have chosen to wait.

Some of their decisions have been a result of having a fully informed decision - i.e both the property price bull side of the discussion and the property price bear side of the discussion.

Some people who come to mind are Carlos67, & Milkyone. Not sure if there are any others - please feel free to comment if the discussion of property price risks in Auckland have been of any use to you.

People should be entitled to hear both sides of the discussion to make a fully informed decision. The mainstream media, property market promoters, REINZ, property mentors, property development companies, real estate agents, bank salesman masking as economists who are employed by banks, mortgage brokers, banks, non bank lenders, have a vested financial interest in promoting the property price bull scenario.

Then there are a handful of property price bears, who have no vested financial interest whatsoever (with a few possible exceptions), in discussing the risks of a property price bear scenario. The viewpoints of these people are clearly drowned out by the huge vested financial interests of the property price bulls outlined above who get large amounts of mainstream media time and audience attention and have large marketing budgets promoting their businesses. There have been some property price bears who have made comments on the mainstream media sites, only to have had them removed by the editor (so that silences the viewpoint of property price bears from other readers and the readers then only get the one sided narrative on the property price discussion promoted by the mainstream media).

Should owner occupiers know all the risks before buying real estate in Auckland? Absolutely. One of those risks is the risk of overpaying for a house. CAVEAT EMPTOR.

Readers are free to choose to ignore the information or they can choose to take what they consider to be useful. They can then bear all the risks and benefits from having made a fully informed decision.

Otherwise without discussion of the property price bear scenario risks, potential buyers are at risk of being informed of only one side of the property price discussion being promoted by those with enormous vested financial interests. And if owner occupiers get caught out with property prices falling significantly below their purchase price, and are forced to sell for some reason, they then may start looking for someone to blame for their partially informed decision.

Read this comment on the real estate industry spin.

The 4 takeaways from every real estate industry press release ever.

- Prices up. Buy before they go higher.

- Price down. Buy before they go up.

- Interest rates up. Buy before they go higher.

- Interest rates down. Buy before they go up.

In short, "Buy now!"

Hi Te Kooti

I totally agree.

However, rather than admitting themselves as wrong, some have just disappeared.

Retired Poppy was an excellent example of this with comments specifically directed at FHB advising against buying and, in his last most positive comment, suggested that they put their lives on hold and wait "eight years" for the bottoming of the Auckland market. Not only did Joe Wilkes predict a crash in 2019, he had all the analysis to back it up. We had those who vehemently argued - as their chief reason - that Auckland was going to follow Australian cities down; but now that Australian cities have shown some recent growth any link to the Australian market no longer seems to apply.

It wasn't surprising that the Auckland market showed small decline after its peak in March 2017 after six years of substantial growth often in double digit growth; however that Auckland prices now seem to be firming.

Three years after the peak, there are a number of drivers still in the Auckland market, but we still have those for the last three years claiming an imminent crash . . . because, because . . . . but without reason.

The outlook is that RBNZ for economic stability reasons are clearly going to use OCR and LVRs - rightly or wrongly but as indicated they will do so - to counter any increasing wider economic downturn with the global economy which will both indirectly and directly further add impetus to the housing market. But, despite this and the current drivers, we still have those claiming crash, crash, crash because, because.

The positive is that many FHB don't seem to have listened to these negative claims and over 110,000 FHB have purchased homes in the last three years. So pleasingly it seems that the bleating dgm are a very small minority and not being listened to.

I agree thee are affordability issues and that is very sad. However, as home ownership rates decline as they are, we are going to have a growing cohort - while paying off their landlord's mortgage - will sadly becoming a "renting middle class poor". There is good reason why this is so, but unfortunately to say so will fall on deaf ears.

We will be hearing of crash, crash, crash indefinitely and some time in the distant future this may be true - but by then current Auckland prices will look ridiculously cheap.

I hope you're right, and Joe WIlkes/Retired Popppy's timing is not wrong.

Money has flowed to the regions simply because Auckland prices are stagnant or falling. Once Auckland starts booming again, all that regional money will dry up overnight and investors will flock back to Auckland.

The Christchurch 'anomaly' is instructive. As the 2010-2015 quake sequence settled, insurance money flooded in ('reinstatement' not 'indemnity' payouts in many cases), land was opened up for subdivision inside of and adjacent to the city, TLA's competed with each other for residents and business (e.g. iZone) and it's still possible to get an FHB-style new house+plot a half-hour commute away for the low 400K's (e.g. Ravenswood). This happy coincidence of events is unlikely to occur elsewhere, hence the anomaly. The instructive bit? the sidelining of stupid TLA planning restrictions, and an occasionally benevolent dictator to drive it all....

The Christchurch sequence is not a complete anomaly and is instructive for the current Auckland market. In the 2011-17 period Auckland had a very restrictive land supply (caused by the idiots at Auckland Council) and this resulted in a large infusion of speculative capital to reap generous easy capital gains. Then in 2017 Auckland Council doubled the amount of land supply, undoing restrictions and pushing forward with greater supply in locations remote from Auckland City, basically doing what Christchurch did about 3 years previous. Thus on a supply basis the Auckland market in 2019-20 is due to track like the Christchurch market did in 2016-17.

First home buyer subsidies more recently introduced by Labour to get re elected next year is whats driving this market surge. Historically low interest rates also.

Auckland, Tauranga, Wellington & Christchurch prices are too high already for these subsidies to work.

Not the time to invest sorry, and subsidies cant and dont last forever. Politicians care not for the long term consequences they sow, but for their short term grip on power; for the lucrative pension that follows.

The banks are the ones who make money on property. Ever worked out what you've actually paid the bank in interest alone over the years? It's not a pretty exercise. All we end up with is having a (nice?) roof over our heads for when we get old.

Sorry LJM this is poor thinking, my parents used to say the same to me, worse they said, "wether you pay rent or you pay a mortgage, you pay it's all the same". Now, 50 years later, they are still paying rent and have nothing to their name, if they bought they would have at least $1 million to their name, what a terrible advice! Why care what others make? Care what you make, I am so, so happy to pay my banks hundreds of thousands of dollars because it allows me to make great money too.

Yvil

That is the most appropriate posting this year.

Over the 50 years your parents have sadly simply paid your landlord's mortgage off, and their landlord would be pocketing a very considerable capital gain. There is only one winner here - and sadly it is not your parents.

You say "They have nothing to their name" . . . . . that is what I mean in my postings by the coming "renting middle class poor".

https://www.interest.co.nz/property/73140/accountant-matthew-gilligan-c…

In the comments sections, 5 years ago, I made a bet with Matt Gilligan of GRA accountants that PN would outperform Auckland over the next 5 year period.

As the last 5 years teaches us, the idea of 'high growth' areas is rubbish and eventually it all evens out - meanwhile i've been enjoying 8%+ yields along the way. And there's much more to come from PN going by those on the ground:

https://www.stuff.co.nz/business/property/117391880/housing-pressure-ra…

Just to recap from 5 years ago:

by Simon | 2nd Dec 14, 2:57pm

0

up

I've been posting here since 2006 so I'll likely still be around in 5 years time.

Lets get clear on our differing points of view so we could look back in 5 years time and see who turns out to be correct.

I'll take P.N values based on QV index Vs. Pt Chev values using the same QV index.

in 5 years time I say P.N index will have increased in % terms by more than (or not decreased by as much as) the Pt. Chev QV values, taking today as a starting point.

EDIT REPLY REPORT COMMENT

by Matthew Gilligan | 2nd Dec 14, 3:34pm

0

up

I'll take Auckland Vs Palmerston North : IE Auckland gets more growth in average house price over Palmy.

You have the advantage, because Auckland has already boomed and is arguably peaking. You get the counter cyclical investment. But I think Auckland (rightly or wrongly) is going to go up further, and Palmy will stay flatish. Auckland is going to get it, because the media are thrashing " Auckland Auckland Auckland" into NZ, and it is driving kiwis to Auckland. They are buying and investing, driven by speculation and greed. We are going into a bubble and there is no stopping it.

So I'll take the bet. I would be more confident if we made this a 10 year bet.

"by Matthew Gilligan | 1st Dec 14, 12:36pm

During 2004-2007 Auckland got beaten by the provinces. But it was a one in thirty year event."

WRONG!! Huge lack of insight there.

Thanks for the recap Simon. Did you back yourself and invest heavily from then till now? Well done if you did

Simon. You might have already said but where do you see the future for the regions and for auckland property. Bearing in mind that the regions have already experienced a longer up cycle than the 04 to 07 period.

8.2% compound over the last 5 years is still an impressive 48% increase in house values !

Yes it is. It's also consistent with Church's 7-10 year hypothesis.

But in reality, many asset prices have increased by similar magnitudes, such as the NZX50.

That's why some like to describe these times as the 'everything bubble.'

One of my concerns is that we have generation of investors who think they can do no wrong (they are super investors) but in reality interest rates have been falling for 30 years and its a con.

Actually during the heights of the Japanese economic bubble, the level of arrogance displayed (particularly in corporate circles) was palpable. What made this worse was Western academics and KOLs were quite sycophantic towards the Japanese success story. One of the key economic journalists and thinkers to question what was going on was Eammon Fingleton who was summarily dismissed as a crank and someone who didn't understand the uniqueness of Japan's economy. I'd imagine he's the equivalent of a 'DGM.'

Interesting post JC - its concerning that we're so deep in it now that things like even a capital gains tax get pushed off the table because it doesn't fit the agenda of those who have gained from recent events. This is where I can see the link that Dalio has been making to the 1930's and we know how that ended up in Europe. Rise of populist leaders to give hope to those who were struggling. What we've known the last few decades could very quickly change if not managed well - it will need utilitarian leadership. Trump like leaders I don't think are the answer.

Indeed. Whereas governments in the past (and society) were greatly concerned with achieving affordable home ownership for Kiwis, too many at the moment are completely self-absorbed and seem to see it as the central powers' responsibility to ensure prices keep going up. The complete opposite of Burkean conservatives.

too many at the moment are completely self-absorbed and seem to see it as the central powers' responsibility to ensure prices keep going up

Well yes. But I think the central banks' actions (globally and not just NZ) should be a pretty good indicator to everyone that they're terrified of the implications of falling asset prices. The only issue is how the ruling elite and the central banks communicate to the wider public. They're also terrified of sentiment falling off a cliff. The ol' DGM spreading like a virus.

Interesting that we now have an 'Ok Boomer' narrative emerging among those in their 20's/30's - which shows that one generation now has little or no respect for the older generation. This to me is quite concerning. Do baby boomers deserve more respect than they are getting - or are the younger generation arrogant? (or both).

Given that boomers appear to only want to fill their own coffers with little consideration for future generations - I can understand why the Ok Boomer narrative is taking off.

I am of the opinion most generations have had scant respect for other generations, but before the advent of social media we talked mostly to our generational peers and no-one paid much attention what the weird old/middle-aged/young twits were on about.

... what about the majority of us who get up in the morning and don't identify with the " generation " we're supposedly born into ... what if being " Gen BB/X/Y/M " doesn't cross our minds as we go about our daily activities ...

Am I a traitor to my BB roots ? ... where are the BB meetings , so I can explain to them why I've failed the BB cause ... being not property greedy , oil polluting , climate change denying ...

Man ... those BB's are gonna lynch the Gummster !

Respect is earned.

J.C.

"Actually during the heights of the Japanese economic bubble, the level of arrogance displayed (particularly in corporate circles) was palpable."

The Japanese in the 80s lacked ONE thing. Interest.co.nz and its host of negative posters to keep their feet on terra firma.

"One of my concerns is that we have generation of investors who think they can do no wrong (they are super investors) "

That is how investors increase their confidence levels, & are willing to take on large amounts of debt to purchase real estate. Investor confidence continues to increase the longer the asset price increase. That is also how asset price bubbles are formed. There are a large number of negatively geared property owners of Auckland residential real estate. The recent generation of residential real estate investors in Auckland have not experienced any financial pain, and as a result they believe that prices can only go up. Then something happens, and they get the opportunity to learn their lesson firsthand.

Look how many got burned in the 1987 stock market crash, many never to touch the stock market again. Then some discovered residential real estate in Auckland ... (and realised that they could leverage up against the equity in their home to buy a residential real estate portfolio with 0% down and 100% financing by the bank)

Auckland closer to 6% compound last 5 years - next to nothing last 3 - less than half palmy 13% compounding over 5 - all with double, triple yields - last 2 or 3 palmy getting closer to 20 % gains - simple catch up - matt G was simple talking his own book at the time try as keen to offload overpriced rubbish in auck.

I never sell so don't really care - already got enough equity for next moves -

bottom line is Auckland is not the growth machine everyone makes out being completely owned by lil old Palmy over last 5 years as Palmy grows at double auck pace.

Put aside the values for moment and open your eyes , if you think the price to build quality in NZ is justification for the valuation, either your ingesting something illegal or very cheap, and you had better get out and see the rest of the world. It's no secret, just google it! Like driving a car with no heating, mold under the seat, framing damage and all that for TENDER or POA ....WOW! Settle for garbage or demand more for less and make a change folks, for yourself and future generations.

Nz is full of a lots of small town, parochial attitudes. Many don't realise what a Ripoff the country is in housing and other things.

What do you mean? Property in New Zealand only goes up. 4 walls, a floor and a roof. Yer sorted.

The push for better housing through insulation (started by National) and now better ventilation and inprovements is having a deep effect to take homes off the rental market.... many are removed for good and left vacant or are demolished. There are housing shortages for good, genuine tenants now (not just the ratbags) and that will take a long time to come right. So the quality of homes is getting better and homes not getting cheaper.

Continue to increase the land prices, continue to land bank driving prices further, continue to increase council fees and deduct all that from affordable pricing based on income levels and your have no choice but to make the build quality cheap. There is a big difference between building science and building. Many people are crying out there, I have seen it first hand, travel the country and you'll find out, and all trying to pass the buck to the next unsuspecting, uninformed buyer. Sad state for all....

Housing if not mistaken it's not something being discussed heavily in our daily lives in previous decades. Some distortion occurs for sure the past decade and half.. that ones could say lead toward obsessions, but the underlying parts is that very damn expensive for both renters & those FHBs. If you got skills? your best bet is to move to OZ, sad reality it is.

One of the blood lines for the country is their productive workers that actually gave services to the property industry owner in this little NZ. The like of low wage workers, Teachers, Police, Nurses, Doctors, Professors, Pilots, Scientist,.. etc. - Rarely, I liaised with them during conversation that they're obsessed with this housing issue, as such.. that they become a staunch adviser of ..yes, buy now, borrow loan, spend. Some staunch RE supporter in this site, even said 'work/study/research is underrated' it's a 'game of winner/looser'- What is the most important things in Life? is actually your Health NOT your Wealth. Even the wealthy property owner terminally ill patients cried in pain & shame when the bottom need to be clean out by health care assistant.. still in rental place & work for living. Got special skills? Needed? NZ too expensive? - simple, just move out.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.