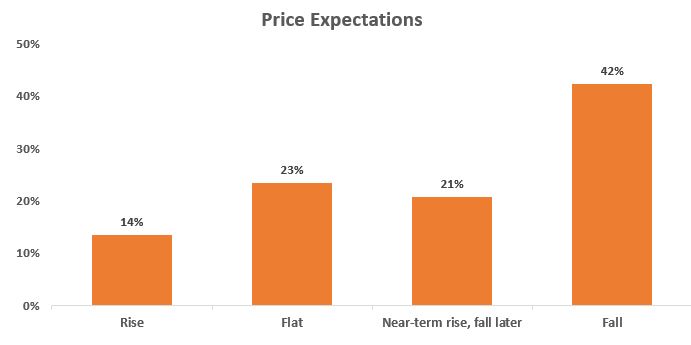

Nearly two-thirds of real estate agents are expecting residential property prices to fall, according to a survey by property data company CoreLogic.

The survey of users of CoreLogic's Property Guru data service taken in mid-June, mostly real estate agents, found 63% expected prices to fall, with 42% expecting a fall now, and 21% expecting a fall later after a short term rise in prices.

Another 23% expected prices to remain flat, and 14% expected them to rise.

Additionally, about a quarter of the respondents expected prices to drop by at least 10% this year.

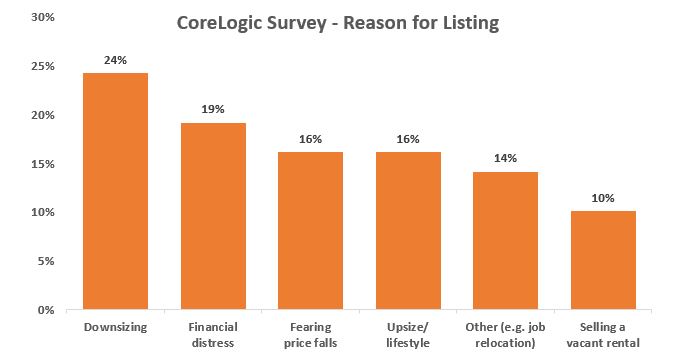

A clue as to why agents appear to have a reasonably downbeat view of the market can be seen in their responses as to the reasons why vendors were listing their properties, with many selling because of financial pressures.

The biggest group (24%) were selling because they were downsizing, while another 16% were selling because they were upsizing or for lifestyle reasons.

But 19% cited financial distress as a reason for new listings, while 16% of respondents said vendors were motivated by fears of price falls and 10% said vendors were wanting to sell a vacant rental property.

Additionally, when asked how demand from buyers for properties now compared with pre-Covid-19, the biggest group, 43% said they thought it was lower while 26% thought it was about the same.

"All in all, it's important to note that our survey was taken at one point in time (mid-June) and mostly covered one audience i.e. real estate agents," CoreLogic Senior Property Economist Kelvin Davidson said.

"However, the results are still a reality check and reaffirm our view that the property market isn't out of the woods yet.

"Spring remains a key period to watch, as wage subsidies and mortgage payment deferrals potentially wind down and the General Election possibly creates some extra uncertainty in the economy."

The comment stream on this story is now closed.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

131 Comments

Bracing for well over 100 comments

by Yvil | 30th Jun 20, 8:34pm (about B & T's auctions holding up well)

Only 35 (39 now 3 days after the article) comments as house sales were good, if next week news comes in that houses are not selling well, there will be well over 100 comments…..

So what? A useless prediction, and even more useless pointing out to anybody that you predicted it.

104 LOL

Why are you so proud and parading around such a paltry prediction? Sign of a fragile ego.

118

Pay attention when the great Oracle speaks! Or you won't know ahead of time, how many comments will be on articles next week...

I mean the article yesterday about sales bouncing back and steady prices had 94 comments if that's your key indicator.

For me, I think there will be mixed signals until we see the end of the subsidies and mortgage holidays - everything until then is artificial. So not paying much attention ¯\_(ツ)_/¯

Challenge accepted. I predict well over 101 comments! Let's see who gets it right this time.

Just mention something about the Greens and you're guaranteed 20 disgruntled posts from Boatman. That could pad the numbers up a bit if it's looking iffy. Good luck.

If you need more posts to hit your numbers, just imply the greens/labour are going to tax something.

Odd day today so bad news stories it is.

This is not a bad news story, it is a survey of what Agents said. Facts

This is not a bad news story, it is a survey of what Agents said. Facts

Wrong. First, what a real estate agent said is not necessarily a 'fact.' Secondly, this data shows their subjective 'feelings.'

Oxymoron

President of Property

Still getting email from RE Agents spinning how booming the housing market is and will be so act now trying to create FOMO.

Its good that you sought help from us Richard, before you did something nuts.

That's an oxymoron !!! Agents & facts in the same sentence

The DGM have an implacable distrust (and hatred) of Real Estate Agents, as we all know. Thus, the DGM won't accept a word of Greg Ninness's story today.

Being undisputedly honest and ethical people, the DGM would never stoop to endorsing Real Estate Agents just because REA's happened to make a prediction which aligns with the DGM doom/gloom agenda.

We can trust the DGM - people of iron-clad conviction, bladder and bowel.

TTP

LOL

Fair suck of the sav! Paul Wright is one of my good friends!

(As is his daughter, Sally, one of our daughter's closest from STAC)

DGM. Debt Grafting Middleman, isnt that you TTP?

Thus, the DGM won't believe a word of Greg Ninness's story today.

It's not a 'story'. It's a descriptive report of 'subjective feelings'. And the DGM label perfectly fits those who were surveyed (based on their responses). So if anything, you need to direct your scorn at the real estate industry.

Bandying around 'DGM' adds no insight.

You'll need a refresher on Logic 101. The REA's aren't saying this to potential buyers. REA's always say "It's a great time to buy!" to their customers, while thinking the exact opposite in some cases.

There's nothing doomy and gloomy about making housing more affordable for more New Zealanders. That would be something positive for the country.

The DGM

These sorts of comments really drag down the quality of the commentary here.

Try engaging in discourse without resorting to labelling, tribalism and name-calling, this is not a kindergarten.

Property prices to fall?????

We all know REA lie through their teeth. So????? :)

See my comment to ttp above...

House prices going down is good news.

Sales are not just of property that is currently occupied.

A great slab of them are NEW builds.

This point is missed all the time. Survey of REAs is looking at why current owners are selling.

This Agent (me) expects prices and sales to be steady in June and start falling July.

Prices down by at least 10% by December and 25% by end of 2021, after the financial crisis (you know, the one our betters keep telling us is not going to happen this time....)

Westpac just announced 20% drop in profit in first quarter and NZ banks announced a 7 fold increase in provisions on bad loans. And that does not include 2nd quarter and all those on mortgage holidays. Just to remind folk, the share price of bank rests on its "assets" which means its debt (loans)

M29 - ' 25% by end of 2021 ' Have to say that's just ridiculous, the very opposite to the fed back I'm getting from agents on the North Shore, Kapiti, and Nelson where I own property.

I could maybe believe 25% in Queenstown and surrounds. And certainly some individual properties might drop by that much.

But the world economy would need a drastic turn for the worse for prices to get there on average. And of course a drastic problem in the world economy would see more NZers returning home, which would help to stabilise prices.

I think that would be the starting point for qtown. The end game is likely far worse.

Why would kiwis rush home because of an economic disaster that affects NZ too ? If there was a war and they were in mortal danger I would agree with you.

I don't understand why 25% drop in 2 years is so unrealistic when Auckland property prices increased by about 100% in the years between 2009-10 odd to 2014.

We have had an unprecedented global event, yet it's crazy to imagine we might experience the same effects in reverse, to effects we have very recently experienced positively, which at the time had no particularly pertinent causes?

This is true and I agree with your sentiment, but there has been huge monetary inflation since these periods, so I don't think you could ever expect reversals like that as it's all relative. I would agree though, if you look at prices normalized to inflation, we are still way too expensive. A 25% pull back may be possible, I'd say it comes down to kiwi's mentality, if the government keeps making it easier and more attractive to buy, people blindly will. Sigh

Have you not been following the grim economic news that is posted daily on this site? How bad do you need the economy to actually get?!

Any evidence of actual price falls right now?

Seems to be fairly buoyant with multiple offers on quality properties.

Remember a good proportion of buyers are older, no mortgage required, not overly dependent on wage income. They can't travel so are buying cars, upgrading their house, or moving up.

except when interest rates drop to the rate they are now term deposits become near meaningless. the 4-5% expected return has been practically wiped out, that leads to the more risk averse (older) people who will shy away from riskier equities to feel like they need to start putting away even more funds as their expected retirement funds have taken a mental hit.

That's a reason for why they would take their money out of the bank and buy a property.

The 80s stock market has left harsh memories for many in this country - if bank deposits aren't worth it any more, then at least properties don't vanish overnight in a crash.

If they were looking to term deposits for interest income, how much does a property with the prospect of capital gains in the pretty long term assist if rents have declined?

The answer to that is pretty simple. If you can secure a net yield of (say) 5% from rental cashflows based on 50 weeks per year AND you get capital growth within the five year briteline period - then stop winging and pay some CGT!

And when was the last time a property investor declined to whinge?

Lanthanide

Agree with you - I am in that situation.

Return on term deposits minimal.

Personally missed the 1987 crash, currently share market propped up by QE but likely to be volatile for the short to medium term - would look at exposure to a range of shares through a managed fund and a couple of selected ones. However in the medium term some uncertainty; surprised at how quickly markets bounced back - that was no doubt due to QE here and globally but some uncertainty remains as a number of companies not necessarily secure long term.

However, will consider property as an option. Personally I would be looking for a niche property that would attracted either working (preferably professional) couple or single mother - they tend (i.e. "generally" if well chosen) to have reliable income, reliable with rent, are over parties, and for solo mums, long term for children's security and schooling. I don't see falling rents for a number of reasons (e.g. accommodation supplements and housing shortage here in HB), potential for increasing yields if buy in response to any fall in property prices, and longer term 5 to 7 years capital gains.

Cashed up, siting in neutral, watching and waiting.

"Seems to be fairly buoyant with multiple offers on quality properties."

That very rarely changes

Yep. Do pay attention.

"The HPI for the whole of NZ peaked at a record high in March and then declined in April and May and is now 2.4% lower than in March."

https://www.interest.co.nz/property/105522/house-prices-have-been-trend…

Could be partly seasonal, but not sure I'd take that bet.

How many older kiwis without a mortgage would be trading up? The very fact they are trading up suggests they do need a mortgage. Trading down far more likely

Actually two-thirds of home owners in New Zealand have a mortgage and those without a mortgage continues to trend downwards every year.

So 3/4 of agents are not to be trusted.

From Barfoots published data it seems the Antipodean has only completed about 70 sales from 165 units and 110 odd pre sales.

It would therefore appear that about 35% of people have walked away from their deposits.

If this trend is mirrored in other pre sold blocks there will be a lot more than a 10% price reduction in the apartment market.

Interesting. Favourite restaurant booked out tonight and tomorrow. Waterfront rooms at Duke of Marlborough sold out in mid August. Two month wait for domestic rain water tanks. I'm not feeling the apocalypse yet.

I doubt we will see any real change until the wage subsidy runs its course. We have an entirely artificial economy at the moment.

"We have an entirely artificial economy at the moment", At the moment? Do you expect this to change any time soon?

When has an economy NOT been artificial?

Economics is a social science. Economies are largely the construct of people.

Go read Adam Smith's seminal work "The Wealth of Nations" (1776) and his description of the "invisible hand" and you will understand.

TTP

The world economy was a lot less artificial before the US abandoned the gold standard in 1971, unleashing the Fed to push things around as it wishes (until it doesn't work anymore). Have been following several foreign commentators. One is saying they can afford to go way deeper into debt and the money printing and asset buying is a good thing, all the others are Doom and Gloom agents expecting all sorts of repercussions, eg hyperinflation (and not just more asset price hyperinflation), or a collapse in confidence in the US dollar, rioting/looting.

Unless another currency becomes more popular than USD, the greenback will continue its dominance.

Yes, or could be gold/silver (or if the survivalist I watch for a laugh is right, shotgun ammo and canned food).

Shotgun ammo is canned (means to acquire) food. Or canned freedom. Or canned persuasion

Dryvil, try reading the first sentence.

Yes and will start about 1-2 weeks after the wage subsidy finishes and if we get a coalition of Labour/Greens NZ will rapidly descend into a deep depression , asset values will decline significantly as Banks endure a liquidity crisis exacerbated by falling asset values as Banks mark to market those assets further reducing Banks ability to lend.

As I've said before, the recession is hitting the young, the poor and people on working visas disproportionately. Yes, older and wealthier people are also being hit, but to much less extent overall, on average.

For those middle or high income earners who haven't lost jobs or had large salary cuts - which let's face it is probably more than 80% - it's kind of BAU. Also, no overseas holidays this year, so some of that disposable income not spend on that will be channeled back into the domestic economy. People who are refinancing mortgages this year to lower mortgage rates will also have a bit more cash to spend.

Most people will not be surprised about this. Those with vested debt exposure will make the usual noise. Agencies will be pushing agents to condition sellers to "take less money" to protect what is the most important commodity for agents/agencies. That being "actual sales turnover".

Popcorn.

What happened to The Man 2? Did he get banned? I've tried clicking on his profile link (on a previous comment) and I get Error 403. The same error for Eco Bird.

Presumably hes been banished to the land Joe Wilkes still lives.

Incidentally nobody seems to be commenting yet about the Americas Cup potentially being cancelled or postponed / downsized.

APEC going virtual was a huge hit to the Auckland hospitality businesses. We have a second one on the cards.

I'm wondering when the Chinabot XiaoWang gets his ticket to the great ether. That wont be a moment too soon.

Joe wilkes also got banned from Digital Finance Analytics .. or was boring and repetitive. I noticed Martin North had trouble holding back laughter.

No I think that is laughing, economist-style. Wilkes wasn’t banned by DFA, it’s an interview by invitation format anyway. He was on a few weeks ago and the story was he had been banned by his employer from commenting/publishing anywhere else. Until he was furloughed...

The Man 3 coming soon!

Should read as - The Man 3 coming soon!!!

Not enough caps.

How about The MAN. 3. - coming soon...

Today is turn of negative news/spin.

Tomorrow will be ...........

Wait till October .......

Interesting... I find the reasons for listing quite intriguing. Are these always the same options or is this a free entry field interpretted into categories? A lot of speculation can be made about the reasons behind the reasons.

Downsizing = personal oversupply of housing

Financial Distress = personal liquidity crisis

Fearing Price Falls = FONGO

Upsize/Lifestyle = Normal Churn

Other/Job Change = Probably partly normal churn, partly personal distress

Vacant Rental = Communal over supply.

This would be interesting data to see plotted over the course of a few years. Would be even more interesting if it each category had a few demographic histograms plotted against them.

Agents have tried FONGO tactic on us in the past which is fine but not if they give a totally different impression to the buyer. I call that dodgy

14 percent of agents predicted a rise in prices.. i think for Wellington and Waikato that's quite likely.

I don't think so, but Spring market will tell. All these doom and gloom comments based on what's happened this week, last week or this weekend are baseless speculation from idle minds. In Papua New Guinea Pidgin there's an apt phrase for some of the comments from real estate scribes with short attention spans "...mouswara"

.

Do real estate agents have any commercial interest in admitting they think prices will fall that I'm failing to see??

Sure. Agent to vendor: prices will fall, sell now, take this offer now.

Wouldnt that just flood the market, pushing prices, sales and comissions even lower?

Better than all the others sharks in the tank getting the meals that are left

Sure, but how does it translate into a benefit for the agents?

Pretty much what realterms said just above - if the agents don't lower seller price expectations now then it will be harder (for a while) to get the sellers to agree to offers in the sinking market.

I would not be surprised if a bunch of the agents are just being honest (Christ - did I just type that?)

But if panic ensues and the market is saturated then buyers can pretty much choose their price? It would be disastrous for comissions. Or are the agents trying to soften the market to help avoid a sudden drop?

Agents just need sales. They don't care nearly as much about the price. Look at the commission structure...

I thought they got a % of sale price?

Little incentive to work hard beyond getting an offer. Let's say the agent themselves gets 2% (the agency the test). As an agent are you really going to push hard for that extra $50k ($1k) if you can get a quick sale and move onto the next house? The agents opportunity cost is the next sale of $1m (20k commission), so motive is volume of sales

True! Now it makes sense

Yes. And beyond that many commission structures fade the wrong way, eg 2% on the first 500k and 1.5% thereafter. Even less incentive for the agent to fuss with the last little bit.

Really? Pretty good deal for the agents then

The only thing agents are interested in is keeping the market moving... sales, up, down doesn't matter. Just keep the market moving, keep the sales coming. Correct, volume is key.

There is no law against negotiating any rate of commission with a real estate agent. There are any number of permutations that could be agreed upon. For instance, in normal times, why not offer the agent 2% commission on the price up to the CV, and 10% for the portion over CV. Or better, 1% up to the CV and 15% or even 20% for that amount over CV. These strategies would encourage the agent to work harder for a maximized selling price rather than just a sale per se. I admit that I've never tried this strategy as I've always sold my properties privately.

I would be interested in hearing from anybody who has tried this.

I also like this idea. Align the vendors and agents interests. Don't know how hard it would be to get agents to agree. And of course it would be the exception and not the rule.

Further you could set the proposed structure so it's the same commission at the agent's estimated sale price. You'll find out if they mean it, or were over quoting.

Yes I did exactly that a while ago. You need to get one of the best agents in town with a huge ego, and most importantly they also own the agency.

The rate I offered was 20% above a certain price. If the agent achieved his (higher than other agents) price estimate then he would get a bit more than standard commission. The end result was an even better price. He even managed to squeeze another $5k out of the buyer after I had already accepted the 'final' price.

The best part is I believed in what the agent told me all through the process because our aims were aligned. I would do it again in a flash, especially for a hard to price property.

Good to hear your experience with it, thanks.

On at least one occasion my parents negotiated the commission with an agent, but I think they just negotiated the percentage fee down and the agents agreed in order to get the listing (would have been 20-30 years ago).

Everybody, after the market crashes:

"But your email said:

'Capital gains guaranteed. No market crash imminent'"

Real estate agents:

"Oh, they got this all screwed up. It should say:

'Capital gains guaranteed? No! Market crash imminent!'"

Real Estate Agent: "All I did was quote Tony Alexander [&/or Peter Thompson]"

The old following orders excuse at Nuremburg.

I know I'm one for ditching the pollsters 'findings' as media driven article click bait, but the reasons given (in this particular article) as are right as they wrong. As always the best part was the posts above & made me laugh. It is Friday after all. If we can't laugh on Friday's we're f...........!

Real Estate agents are the waiter and neither the restaurant owner or chef.

"However, the results are still a reality check and reaffirm our view that the property market isn't out of the woods yet.

“Out of the woods yet” as NZ is facing into a catastrophic crash and circa 10 year bathtub for any recovery

Served up as a survey... it’s hyperbolic propaganda

"NZ is facing into a catastrophic crash and circa 10 year bathtub for any recovery... hyperbolic propaganda"

100 percent

You know that when over half of real estate agents are predicting falls and big falls that an avalanche is on its way!!!!

They are the closest to the action and normally you couldnt pry a negative word out of them.

Stand by ladies and gentlemen....

I wouldn't count your chickens just yet.

Yeah, Labour Market Stats for the June quarter are due out 5 August. That's the next thing I'm waiting for.

Homes and oneroof seem to have bumped up their house price estimates. Bizarre.

Anything to avoid fall but crash it will be.

So many agencies and media work / lobby to support ponzi so will like to see fall only to see their reactions. Karma is a bitch and is playing now.

Reminder that these are some reasons given in the mainstream media, property market commentators, property market promoters, bank lending promoters masking as bank economists, real estate agents, property market mentors & other sources as to why property prices in Auckland will not fall by much and that there is a low probability that property prices will fall dramatically:

1) during the GFC, house prices in Auckland fell only 7-10%

2) over the past 50 years, house prices in Auckland have averaged 7.2% per annum (or commonly referred to as house prices doubling every 10 years). This trend can be expected to continue into the future - https://youtu.be/Agp9xFWoBX4?t=172

3) there is a shortage of underlying housing in Auckland, so property prices won't fall by much - https://www.interest.co.nz/.../auckland-councils-chief......

4) there is a growing population which means that there will be more demand for houses - https://www.stuff.co.nz/.../house-prices-have-fallen-but-...

5) we have inward immigration which means more demand for houses

6) Auckland is an attractive city with an attractive lifestyle - that makes it desirable and attracts foreigners to move to Auckland and hence raise the demand for houses

7) lower interest rates are supportive of rising house prices

8) lower interest rates make debt servicing easier for borrowers

9) Low interest rates were also forcing retirees and those nearing retirement to look for investments that would produce income, such as rental property. "Plans of the baby boomers to retire and live off a conservative yet well-yielding portfolio have evaporated with low interest rates," he said. "[They] are seeking assets and buying investment properties. They are also seeking assets they can hold and live off of for three decades in retirement rather than just 15 years given advances in health and medicines." - https://www.stuff.co.nz/.../all-predictions-of-an-auckland...

10) we mustn't forget either the vested interests in ongoing stability. No government, central bank or trading bank with mortgage exposure wants materially lower house prices. Nor does an incumbent Beehive want falling house prices going into an election campaign https://www.stuff.co.nz/.../think-house-prices-are-going-...

11) the economy is doing well, with low unemployment - https://www.stuff.co.nz/.../think-house-prices-are-going-...

12) there has been insufficient construction of new builds to meet the housing shortage - https://www.stuff.co.nz/.../house-prices-have-fallen-but-...

13) there are high construction costs to building a house. House prices cannot fall below their construction cost. - https://www.stuff.co.nz/.../house-prices-have-fallen-but-...

14) people don't sell their houses at a loss - https://www.stuff.co.nz/.../house-prices-have-fallen-but-...

15) continued inflation means that house prices will continue to rise in the future

16) The fact is, debt levels have barely changed from the beginning to the end of those 10 years, compared to GDP levels, compared to household assets, compared to household disposable incomes. And much more importantly, debt servicing is very much easier now, an item that is almost universally overlooked. We are not pushing out to unsustainable levels now, and even if they creep up a little, we are far from that point. https://www.interest.co.nz/.../if-you-think-new-zealands......

17) in aggregate household debt servicing is low in New Zealand - currently at just under 8% of disposable income of households - https://www.rbnz.govt.nz/.../key.../key-graph-household-debt

18) property market participants & commentators who have been correct in their predictions about recent property price trends have more credibility and hence their predictions of upward prices are believed by a wider audience (such as Ashley Church, Tony Alexander, Ron Hoy Fong, Matthew Gilligan, etc). - https://www.stuff.co.nz/.../all-predictions-of-an-auckland...

19) previous warnings about a house price crash have been wrong - property prices have continued rising upward significantly since these warnings were given, so there is little reason to believe these warnings.(such as Bernard Hickey) - https://www.stuff.co.nz/.../all-predictions-of-an-auckland...

20) its unlikely Auckland prices collapse. I think the main two reasons though are:a) Affordability has been this bad, and worse, in the past and it only resulted in about a 10% drop. b) The number of homes built over the last decade has been too low and will take some time to recover - https://www.interest.co.nz/.../housing-market-continues-hibe...

21) returning New Zealand expats will buy houses in NZ -

22) NZ is a safe haven from COVID-19, etc - expats will buy houses in NZ - https://www.theguardian.com/.../why-silicon-valley...

23) More QE, lower interest rates, mortgage holidays, interest free loans, wage subsidies, no LVR... it's getting harder and harder to see house prices falling

Hi CN, Hope coronavirus understand all the reason and spare NZ housing market while taking down the world.

Every single source you mention has a vested interest.

1) This is not the GFC, this is a completely different beast and affecting NZ in a very different level.

2) Past trends are do not predict the future, also your trend is cherry picking the period that interests your conclussions.

3) Shortage of housing is not real, you can just go around to see how many new developments are going on, many of which are not selling in addition to the large number of vacant houses we have.

4) Population grow is pretty much stagnant.

5) Immigration is zero.

6) More people will start moving outside the larger cities since remote work is starting to become more popular.

7) Lower rates will be given to a very reduced number of people that meets the conditions.

8) Same as above.

9) Since the outlook is for prices to fall property investment will become less attractive for retirees.

10) The government also wants people to afford quality and healthy housing, which has become an issue these days.

11) What are you talking about!? 1K unemployed a day just a week ago, and there's a second wave of unemployment coming.

12) There's plenty of construction going on on an oversupplied market with plenty of vacant homes. The issue being that builders are making the homes that people are not asking for but investors instead.

13) Housing prices are not high due to construction, most of it is due to land prices.

14) People will sell if they need to when they get into financial stress (currently 1 out of 5 for sale)

15) Where is the proof of this?

16) You are ignoring unemployment and financial stress.

17) It is the third time you made this point ;)

18) All of them with a vested interest, even a broken clock is right twice a day.

19) Not true, prices are stagnant since 3 years ago, if you take into account associated costs and inflation that makes is a poor investment.

20) This is an opinion, don't think they will collapse either, but I could be as wrong as you.

21) There isn't a significant number to support this.

22) Again, not a significant number to support this.

23) QE is going mostly to the stock market, mortgage holidays will be over as well as wage subsidies.

No 5... "immigration is zero" absolute rubbish

Tens of thousands have been pouring through the border and more who want to come back (Visa holders) are being stopped from doing so.

The total number of arrivals was exactly a 0.64% in May compared to the same month last year (1,533 vs 238,004), if that is rubbish to you good luck in your own reality. This has already become a trend BTW, not bad I guess that only point you considered rubbish from all I wrote is the only one that probably does not have much effect in housing sale prices anyway. If you would know the realities of the vast majority of migrants, which mostly rent and in many cases share with others, not to even consider buying their own house. Furthermore those returning kiwis will likely have accommodation of their own of at some relative's.

Yes still rubbish, you ask how, everything has changed including PCP comparisons. The comment was also made that population growth was stagnant ... false. There are over 1000 births per week and the population is natural increase is growing.

Yeah cos all those 1000 babies are in the market looking to buy a house. What about the death rate at the other end of the life spectrum ? just admit that immigration is currently zilch. What may change things rapidly is if the world goes to war, New Zealand will be looking like the best place to be on the whole planet and thousands of seriously rich people will be wanting to get here and fast by buying there way in or arriving on their super yachts so at that point house prices will go mental but best you try not to think about that as it may result in a wet dream.

You do make me laugh Carlos thanks. Btw natural population increase takes account of deaths but I'm sure you already knew that and were being obtuse. Enjoy.

Exactly.

B21,

Thank you for your rebuttal to the points raised above. Potential owner occupier buyers can choose which perspective to take to develop their future property price expectations and can then act accordingly.

Just for clarification, the points referring to immigration, low unemployment and a strong economy were the reasons given as recently as early March 2020 as to why house prices in NZ could not fall by much (i.e before COVID19 hit NZ) - and before the median house price in NZ subsequently fell 8.8% from $680,000 in April 2020 to $620,000 in May 2020. And before the property price risks became more apparent to the general public in regional local markets such as Queenstown, and central Auckland.

Just wanted to remind people of the common narrative that was repeated to the general public at the time before property prices fell and the subsequent property price fall. Will be interesting to watch how property prices play out from here.

Thanks for clarifying that CN

Interesting article with very useful information. It looks like everybody now can see what is coming, even those with vested interests. Most interesting data to pay attention is the fact that 1 out of 5 listings are due to financial stress, a considerably high number though it would be interesting how this compares to previous data. Thanks for your work Greg.

Yes I see trouble looming but even I am starting to reconsider how big the drop will be. What I did not factor in is the lengths vested interests would go to to prop up the market. If natural forces were let rip the crash would be epic but wage subsidies and all the free money being thrown about and mortgage holidays has either delayed or muted the crash. Prices have dipped for sure but I'm now looking to buy the right house at the right price and hold. Anything below say a July 2018 RV is as good as it may get. Fear of large falls my now play into my hand as I'm starting to think it's not going to happen.

If the govt truly wanted a reset they would not be writing out billions in payments. It's obvious they want the ponzi to continue.

Yeah, and I'm unsure why you're such an enthusiastic cheerleader for them to do so.

Seriously, does the idea that your kids/grandkids will still face this façade of a 'market' give you kicks?

That we distort asset prices so far beyond fundamentals that NZ is inherited by a landed gentry - the *exact* thing the founders of this country sought to escape.

You really want that?

"Fear of large falls my now play into my hand"

I hope IO frazz richard 1965 bw and JC keep stoking that fire a little longer for you (/s)

It will be hard to tell, what is certain is that economic stimulus is wearing out and the perception is that the majority of potential house buyers are not buying NZME's and their spokespeople fake narrative about housing shortage and (unexisting) immigration pumping up the market anymore, this change of buyer mentality plus growing unemployment rates is what will effectively drive the market in the short term.

I understand why you think that way,same thing happened in Australia ;however,how long can they keep this rollercoaster going,at somepoint it's gotta stop,my main concern is continued demand for our exports and its impact on employment, I watch martin north on the dfa channel and think nz isn't to far behind,let's see what September to November brings.

Thanks for that tip - will add these guys to my faves:

https://digitalfinanceanalytics.com/blog/

The other one third work for the Herald.

The three scenarios are down, flat and up. At the same time you have to factor in deflation, stagflation, inflation or perhaps hyperinflation. We all know that the system is not controlled by market forces but manipulated by central banks all over the world. Taking advise regarding the future from a real estate agent is probably not the best idea (doe this house leak - no it is as good as gold!). If there looks to be a dramatic fall in prices then there will be a dramatic response from the central banks. The real question to ask is - are the central banks going to get this right? Good luck everyone!

Agents predicting house price falls is a load of rubbish.They are desperate for sales ,the house numbers forsale are declining , we are watching closely , we are seeing more private sales being listed ,you do not really need an agent . follow the market on Trade Me and you can understand prices and trends .Go along to open homes look at the quality of the stock , check out new homes and prices . If house price's fall will building a new house be cheaper not likely ,be careful with agents pushing you into Auctions , they can work sometimes but not always . Best thing is to understand the value of your home. With so many Kiwi's returning home House Demand will have to get stronger .

The secret to making accurate predictions? Make them after the event.

I went to see a property and the agent told me 2 other parties were looking at it.

Thats just standard rhetoric from agents but the truth in Tauranga at present is you often find your the only registered bidder at the Auction. Clearly very different markets within New Zealand.

They cant be in Auckland. House prices that I recently seen go for are at all time high.

Agent told me $750K , went for $1.1M with 4 bidders all for a crappy property with a potential to add another dwelling on rear - this despite council advise of no extra dwelling allowed.

Another one sold for higher than the done up next door. Please wake me up when prices do fall.

The 7.5% fall you quoted the other day were mostly apartments and houses with leaky issues

Next I will be taking advise from my Uber driver.

Self-driving Uber?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.