First home buyers in almost all parts of the country have benefited significantly from the sharp fall in mortgage interest rates since the COVID lockdown in March, particularly in Auckland, according to interest.co.nz’s latest home loan affordability analysis.

That’s because the drop in interest rates has had a bigger impact on mortgage payments than it has on house prices at the bottom end of the market.

In March the average of the two year fixed mortgage rates offered by the main banks for buyers with a minimum 20% deposit was 3.31% and by August that had fallen to 2.72%.

Lower interest rates generally help to push up housing prices and that has been the case over the last five months, with the REINZ’s national lower quartile house price increasing from $480,000 in March to a record high $492,000 in August.

The lower quartile price is the price point at which 75% of homes sold in a month are above, and 25% are below.

It is a proxy for the lower end of the market, which is generally of most interest to first home buyers on average incomes.

Around the country, record high lower quartile prices were also set in seven regions in August – Northland, Waikato, Hawkes Bay, Wellington, Canterbury, Otago and Southland.

However a closer look at the lower quartile price rises over the last five months suggests they have been more tepid than they might appear.

The national lower quartile price increased by $12,000 (+2.5%) between March and August.

Of the seven regions that also achieved record lower quartile prices in August, two of those, Hawkes Bay and Southland only achieved record equalling prices, matching record prices achieved earlier in the year.

The lower quartile price of one region, Southland, was unchanged between March and August, and lower quartile prices actually declined between March and August in three regions – Auckland (-1.0%), Taranaki (--1.1%) and Nelson/Marlborough (-4.8%).

The decline in the lower quartile price in Auckland was particularly significant because it is the country’s largest market and the most expensive region in the country.

So how have first home buyers fared overall in all of this?

Firstly, where prices have increased, the size of the deposit and the size of the mortgage needed to buy a lower-quartile home would both have increased.

In places such as Auckland, where the lower quartile price declined, the size of the deposit and the size of the mortgage needed would both have declined.

Overall, a 10% deposit for a home at the national lower quartile-price would have increased by $1200 between March and August.

Over a five month period that should be reasonably achievable for first home buyers on average incomes.

In Auckland, where the lower quartile price declined by 1% between March and August, the amount needed for a deposit declined by the same amount.

However, falling interest rates don’t just push up prices, they also push down mortgage payments.

As well as lowering interest rates, the Reserve Bank has removed Loan to Valuation Ratio (LVR) restrictions on new mortgage lending, making it easier for first home buyers to get a mortgage with just a 10% deposit, rather than the standard 20% deposit, although they will pay a premium interest rate for it.

Interest.co.nz estimates that the average mortgage interest rate for low equity loans has fallen from about 4.61% in March to about 3.77% in August, although there can be significant variations in low equity rates between banks.

According to interest.co.nz’s calculations, the mortgage payments on a home purchased with a 10% deposit at the national lower quartile price of $480,000 in March, would have been $511 a week (at the average two year fixed rate of 4.61% for low equity buyers, on a 30 year term).

But at the August lower quartile price of $492,000, the mortgage payments would be just $474 a week, down 7.3% compared to the March figure, due to the fall in the average low equity mortgage interest rate from 4.61% % to 3.77%.

That’s a saving of $37 a week, even though the lower quartile price increased over that period.

Falls in mortgage payments on the lower quartile price occurred in all but one region of the country between March and August, with the biggest falls occurring in Auckland, where they were down by a whopping $82 a week, followed by Nelson-Marlborough -$78, Wellington -$52, Waikato -$47 and Bay of Plenty -$44.

Those were substantial reductions in the amount typical first home buyers would net to set aside each week to service the mortgage on a lower quartile-priced home and more than made up for the slight increase in the amount they would have needed for a deposit in the areas where prices have increased.

The one exception was the Hawkes Bay.

Hawkes Bay had the biggest increase in the lower quartile property price between March and August, rising from $399,000 to $441,000, an increase of $42,000, pushing it up by 10.5% over the five months.

That pushed the amount of money needed for a 10% deposit up by $4200, which could have proved problematic for first home buyers on average incomes.

And the amount of the price increase in Hawkes Bay cancelled out the benefits of falling interest rates on mortgage payments.

So typical first home buyers in Hawkes Bay were likely worse off in August than they were in March.

But apart from Hawkes Bay, typical first home buyers in the rest of the country appear to be better off overall in August than they were in March, even though prices have risen in many regions.

That is particularly true in Auckland, where typical first home buyers are substantially better off thanks to the fall in interest rates that’s occurred since March.

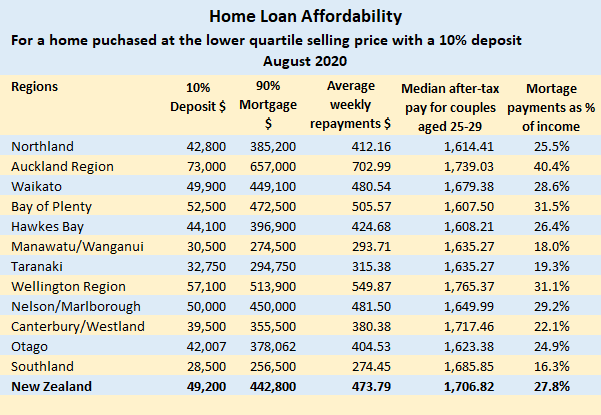

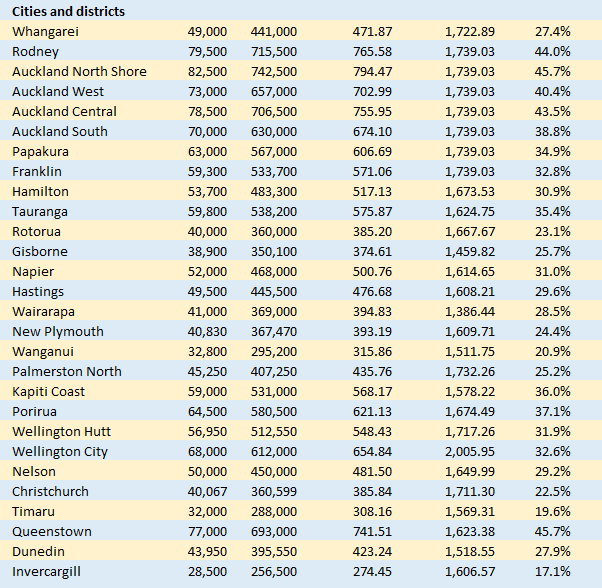

The table below shows how much would be required for a 10% deposit on a lower quartile-priced home in all regions and main urban districts throughout the country, as well as the amount of the mortgage that would be required with a 10% deposit, what the mortgage payments would be (weekly for a 30 year term), as well as the median take home pay for couples aged 25-29 (working full time) in each region and the percentage much of that money would need to be set aside for mortgage payments each week.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

81 Comments

Not much benefit if the house price has risen and they need to borrow more to buy the same house.

If you end up having to refinance at a later date at a higher rate you get stuffed both ways.

If we can get some really good unemployment numbers perhaps 15% or even better 20% and no wage subsidy's to provide increased welfare for the middle class we may be able to see some healthy decreases in houses prices.

As no matter how low Orr makes the OCR if you they cant pay back the principal many will loose their inflated houses. If we can get a healthy reset on house prices it maybe imprinted in the memory of the next two generations not to speculate on houses. Feeling optimistic.....

...said the hyena to the vulture.

No, I have not been banned from Interest, I'm just limiting my involvment in the comments section as it's clear the comments section is detrimental to one's prosperity and well being.

Point in case, BW's incessant warnings about house price deflation and the "terrible situation of owning a house that goes down in value with a mortgage". It's catastrophic advice which cost $ hundreds of thousands and the chance to own one's own house to whoever listened to it for the last few years

Patience, grasshopper.

The secret of success is seeing what others don't see before they do.

You don't appear to realise what's coming. Even the RBNZ do - why else do you think they are doing what they are? Fun?! They KNOW what's going to happen. I think they are going about sorting the problem in the wrong way, but it's the same problem we both see.

By the time you see it.....that catastrophic advice will be your own.

bw - Many people die waiting for the said catastrophe, its so easy to be pessimistic, optimists see through the BS and build a future that is not based on some feeling ! What's that look like e.g. ? - in the last 20 years I have had 3 sets of tenants out of 30 odd who have had a feeling about ' what's coming ' and sold then rented off me. All 3 held on until they could not afford to buy back in, still believing their ' what's coming ' was true and consequently complicated their lives very badly 2 of 3 ending in divorce. My point is that such comments as yours - 'you don't appear to realise what's coming' should be dismissed as gossip from your local hairdresser.

But I am Optimistic!

I see a New Zealand where tenants such as yours don't have to 'wait' but can afford their own home earlier than they can today.

I did. At 23 I went out with my 21-year-old wife and bought a new home for a new family just like we all did at that time. It was just normal.

At 21 now, my daughter has no show of doing that; neither does her 31-year-old step-sister.

There is a place for owners, tenants and landlords in our society - for many reasons. I support all of that.

But what makes no sense, and hasn't for probably that 20 years you mention, is the mathematics of those things.

We have Finacialised one of the most basic elements necessary to live in a way we haven't since probably the late 1800's - shelter.

And if we want Dickensian economics to return, and the societal problems that accompany that, then we have gone about it the right way.

Thank Lord (sir) Key

Well said.

Yes BW's post is "well said" and I do not disagree that it paints a better picture of what NZ could be. BW addresses another very common line of thought present in many comments on Interest, ethics or fairness or what is right. Unfortunately many commenters don't make the difference between what they would like to happen and what actually is. Sure, it would be nice if house prices were half the price they are now so most people can own one but the reality is that house prices are getting ever pricier and by hoping, waiting, wishing them to come down in price, people simply miss out and those FHB who listen to that advice also miss out, possibly for a lifetime

The ponzi requires people to play.

Yvil, you keep pulling out this line about people not being able to tell the difference between what is and what they would like to be, but that seems to be largely a figment of your imagination. What people disagree about here is not what is the case, but what the future holds. And it's misleading to try to paint things as though people don't have reasons for thinking prices might go down and are instead simply hoping or wishing that that will be the case. Didn't you yourself at one point predict a fall in house prices due to Covid?

He did, and cemented that view by selling his house.

Shoreman, you make a very valid point. What makes me think this time MIGHT actually be different is when I consider what support mechanisms stopped the previous predictions coming true. Big ones for me are interest rates and immigration. To stop housing market declines previously the RBNZ would just lower interest rates however we're now at a point where there very little ammunition left in the interest rate cannon and it's clear they're happy to use it all up soon. Immigration has essentially halted for the next couple of years which never happened previously. Also unemployment is a big dark cloud hanging around mortgage/rent servicing and will likely be worse than previous crises. My point being that the life jackets that previously saved us from drowning look like they're low on air and this time we might actually drown. I hope not.

Serious fall is coming, IMO at probability of 90%+ by 2026, 95%+ it happens this decade. Truth is nobody can predict it within a narrow time frame but make no mistake applying the old 7.2 chestnut to property this decade is very likely to end very badly. "The ability to clearly see the past creates the illusion of being able to predict the future".

I think they are going about sorting the problem in the wrong way,

They're doing what they do in the only way they know how. Greenspan admitted he was wrong. He's ancient history now. Even though he was the godfather of it all.

Yvil - Quite rightly said, very similar to the terrible predictions made by RP, hopefully younger people saw such comments as RP's as coming from someone with a chip on their shoulder, very bitter that the market wasn't doing as they believed it should. I'm please to report 3 of 5 off-spring over the last 18 months have bought their first homes, are settled, and are really loving home ownership and getting on with their lives.

Agree with you Yvil

In past 12 months Auckland and national house prices have increased by 16% - that $650,000 Auckland house is now $754,000 and that nationally priced average house of $500,000 is now $580,000.

While there were some of us reading the signs and providing substantiated reasons as to the likely movement there were those making unsubstantiated calls of "bubble burst".

Great to see RBNZ data show FHB were over 25,000 mortgages (500 per week) likely involving over 40,000 people - really great. They have seen their houses rising in value and the outlook is for falling mortgage rates and costs. Can't describe them other than being winners.

Those on this site that were calling very vocally "bubble burst" and have done so for the past few years now need to "own it" - they were wrong and need to suck it up that they made the wrong decision - it was their decision so live with it. Can't describe them other than being losers.

Despite the reality of the likelihood of falling interest rates providing upward support for the market, they are still crying the same. The reality is that provided FHB have job and income security, and are prudent, they have nothing to fear regarding market fluctuations - something bw in his post above can't see.

I am going to enjoy showing you this post again in a year.

Apex

Yeah; that is what they were saying last year, and the year before that, and the year . . . .

Do you not see the difference between predicting price falls last year and predicting them now?

The outlook isn't exactly sunny and calling anyone who points out the storm clouds rolling in a DGM seems like the behavior of someone with a vested interest clouding their judgement.

Just spruiker logic. "It hasn't happened for the past X years so it's never gonna happen"

CourtJester

Personally never supported the notion "It hasn't happened for the past X years so it's never gonna happen" - that's a mug's rationale when it comes to any form of investing. Also a cheap dgm accusation.

You need to look at the current drivers and what they mean. Currently very much factors such as a likelihood of lower interest rates, or increasing affordability for FHB are likely to drivers over the next year.

As to me, I was posting that the increase in house prices through 2016 was not sustainable so not a spruiker. Also posted I see flat to some fall in prices as we exit Covid and necessity for RBNZ support - due to rising interest rates and the disconnect between income and house prices.

lowercase

No vested interest at all - and anyway I wouldn't claim that my comments here are able to affect the market.

Just don't like unsubstantiated comments - generally having simply an emotive basis.

Well, in FACT, as you know, prices do fall some years and sometimes for a few years in a row, even if they do rise if you look at 7 year periods overall.

Prices fell from mid 2016 to mid 2019 for instance, as did sales, in Auckland.

Prices have been rising in Auckland since last November, which is 9 months.

Early days yet to see if this will last, ditto with sales rise.

Mike

I have no problems that prices can fall and I have posted that I have experienced falls on three occasions.

However never been one to anticipate on the basis of some sort of cyclic pattern but rather current market influences.

Covid is clearly a factor that is not part of any seven year cycle but through NZRB response is affecting the market considerably. I leave relying on cyclic patterns to things like phases of the moon and tides.

All life is cyclical. WG Gann made a lot of money using planetary cycles to forecast stock market in USA in 1925 to 1945 for instance.

"They have seen their houses rising in value"

Sounds good - if they are going to live there forever.

But what do they do when the next 4 children arrive; they have had a 5% household income rise and the cost of the next home has gone up 16% p.a?

That household income rise is coming compliments of lower interest cost no doubt?

If there's one lesson coming to many that others have learned in the past it's:

Valuation is intangible; debt is certain.

bw

Just rent then - lose out on your property going up 16% and that next house also going up 16% .

Pretty basic really.

P.S. Surely you can do better than that! :)

Hi Printer,

I take it your price rises cited for last 12m refer to August and median?

August is a little over the top (as in, it was top) but I will give figures for it any way.

Auckland August 2019 v 2020 median rose from $815 to $950k or 15%

Auckland HPI however rose from 2820 to 3121, or 10.7%

For NZ excl Auckland, the HPI went from 2770 to 3033, or up 9.4%

The median rose from $499k to $570k or 14.2%

July and June were not as high as August. June HPI rise for Auckland was 7.7% YoY

July was + 9.2% YoY

"The reality is that provided FHB have job and income security...."

Clearly you cant see that its only leverage has been providing the INCOME you refer to (from a financial system point of view)

So that prudent income .... its anything but

While there were some of us reading the signs and providing substantiated reasons as to the likely movement there were those making unsubstantiated calls of "bubble burst".

Only very few people accurately call the timing of the bursting of bubbles. And then, there is an element of luck to get it right.

It is common practice by those who make mistakes and don't the maturity to own it is to shift the blame - a behaviour common amongst six year olds.

I note that in the current blame game the scapegoat is Orr. Actually the target should be RBNZ but blame shifters love to pin it on an individual - by personalising it it makes the blame shifting more tangible and self-effective.

The reality is that by the Act, RBNZ are charged with trying to achieve economic stability. Of course these anonymous gumboot keyboard warriors think they know better.

From an individual's perspective, what RBNZ deem to be the appropriate action results in the conditions we live with. Personal success or failure is about our personal decisions - - that is the only thing we can effectively control.

The current environment - Covid, NZRB decisions and all - is the environment we live in. Unfortunately a number of posters on this site self-entitled, blame shifting Quade Coopers.

:)

How have Kiwi high-school students and those coming up to graduating university made mistakes? Or, just no regard for them?

This is a pretty lightweight justification for continuing to transfer wealth from the poorer young to the wealthier older asset holders.

So in your opinion we shouldn't express disagreement or complain about whatever decisions are being made by govt or RBNZ?

Some of you people (for example Yvil and that new troll account that showed up recently) like to think that

1: You're so smart because you were born 10-20-30 years earlier than some of the other commenters here and thus had a lot more time and much better opportunities to buy your own home,

2: People who complain about RBNZ policy are unsuccessful, poor losers,

3: People who think the extremely unaffordable NZ housing """"market"""" is unsustainable in the long term are depressed about life in general and just have a negative outlook on everything

4: People who raise concerns about govt / RBNZ policy are just crying and not doing anything to make their own lives better.

Well flash news, commenting here is (for most of us) not the only thing going on in our lives. We work hard (I'd bet that most DGM's here are in the top decile by income), we invest in various things, we vote in order to at least try to affect policy and we try to find a way to achieve our goals in an environment that is currently very unstable and unpredictable.

Well said. It does seem to be prevalent that those who want to cheer price rises and state in Panglossian terms that all is well in the garden, whatever the facts on ground and reasons for phenomena in housing market, like to cast those disagreeing with them in less than flattering terms, or with a degree of disdain. This is of course, totally unnecessary as these contributions are meant to be contentious and informative but not disdainful. As Jacinda puts it, it's not )or should not be) a blood sport.

No Court Jester

I feel for FHB - like the 25,000 last year who purchased homes - who are face with affordability issues but bite the bullet.

I struggle to accept unsubstantiated emotive based comments by those who have been - and continue - to claim bubble burst, simply moan, and scaremonger or use dgm as a reason to appease themselves and justify inaction.

Just being blunt - yes, as I have posted I was concerned about RBNZ action and that increases risk of a correction. However, there is nothing you - Court Jester - can realistically effectively do about that. What potential FHB should be concerned about is the implications for house prices and mortgage rates over the next year and be prudent to protect themselves in the eventuality of any correction.

Your absurd comment in response to my comment the other day indicates that you are in the Quade Cooper camp. Just being blunt here.

Cheers mate.

"What potential FHB should be concerned about is the implications for house prices and mortgage rates over the next year and be prudent to protect themselves in the eventuality of any correction." - Finally something we agree on. Despite all your assumptions about me, that's exactly what I'm doing. I could buy a property in the ballpark of $1.3-1.5 million right now if I wanted to - but I'm being prudent and protecting myself because I see a gigantic downside risk. I feel safer not jumping into a very unstable market.

Also, I have no idea what 'Quade Cooler' means - mind you, I'm an immigrant and a millennial.

Good for you CJ, I think if you can get in now and intend to hold for the long term you should be ok.

Stay with 80% LVR to get a good finance rate and look to buy in a good location and I especially look to where you can easily add value, whether it’s landscaping, painting, a deck or an internal redecorate (even if that’s done over a few years)

Good luck, I realise it can be daunting and a little scary

Blame? I thought those citing effect of QE, LVR and rate reductions, were citing contributory causes, not attributing blame, for prices rising and sales too.

perhaps you are referring to specific individuals

No one really listens to either side do they ? People make their own decisions. Then the social media algorithm kicks in and feeds you the necessary disinformation to keep you engaged to buy that ab king pro.

I think it’s wise to consider a range of perspectives.

But you’re more than likely right, common sense isn’t common

Hard to see all those FHB's jumping up for joy -- Usually they need to fix for at least two years for security of payments -- so anything bought this year will still be at higher interest raates and most of that for another 18 months or so - If they have not already bought -- concern about security of income and trying to actually save a larger deposit - woosh -- Investors however - more equity more liquidity much more likely to be on short term rates or have tranche like mortgages one of which expires every 6 months --

But as Yvil says -- there is never a bad time to buy your first or any home you intend to live in -- as long as you can make those payments for the first two years and dont overstretch - matters not up or down int eh short term - just as long as you can make payments - which will be WAY cheaper than renting in Auckland anyway

I have no problems with anyone wanting to buy their own home whenever they can afford it. But renting....should ALWAYS be way more expensive than owning. We have been brainwashed over recent times into the thought that as soon as the B/E line breaks in favour of owning; even just a tad more than renting, we should hit the showroom and buy.

Anyone who's been, or is a landlord, knows the cost involved in being such. And absent the speculative promise of capital gains, those costs need to be covered and make a profit (or what's the point!) from rental income.

Once CG disappears, watch what happens to landlords who didn't realise the game was over.

Where in Auckland is buying cheaper than renting? Auckland is still a very cheap market to rent in!

March 23rd was a just a precursor to what's coming. Hold on tight everyone. Make sure that money is somewhere safe come 3rd November. NZ banks are possibly the least safe place to be with NZ housing a close second. Ozzy banks for me. Just waiting for better exchange rate, then over it goes. Good luck all.

What is happening on 3rd November?

Donald Trump gets re-elected.

Only if he rigs it.

My guess is he'll lose, claim that postal votes were rigged, call for the Praetorian Guard to encircle the Whitehouse to prevent him being chucked on the street, and the Guard will be whistling and looking the other way.

Yes, evidently its cheaper repayments for FHB in Auckland.

Young people are also more likely to lose their job in next 12m than people over 30.

Buying is likely to moderate in last 4m of the year and Auckland sales will come in about 6% higher than 2019, at 24,000.

Interesting that Interest has indicated that lower quartile not rising as much as might have been expected in price. Whereas lots of commentators have stated that prices for property in $1.3 - 1.7m bracket are going nuts.

By the way, average annual sales in Auckland from 1992 to 2019 inclusive: 26,775 pa.

The average from 2012 to 2019 was almost bang on that average: 26,528.

Roughly it seems to go up for 4-5 years and down for 4 years. This is last down year, if so, relative to prev 5 year average (which was 2012-16 = 29,031.)

Pop increase and price increase seems to make v little difference to the trend or the 4-5 year up/down.

Last time we had 6 years straight above 30,000 pa was 2002-07.

From Sept 19 to March 20, sales rose 3.9% compared to year earlier.

In June, July and August is was 33%

12m sales to August 2020 so far are 23,735.

2020 sales so far are 15,198 to end of August.

Demographically, there is nothing to support sales over 24,000 until late 2022.

Does the lower quartile (and the overall figures) include leasehold apartments? If that's the case, that could distort the actual price changes by a big margin. There's a reason why the cheapest (leasehold) properties sell for peanuts... and the real cost is not included in either the price or mortgage repayment figures.

You're joking ( pun!)

You mean the statistics deliberately leave out those sales figures that don't suit the narrative - even if they're factual?

I'm shocked; shocked....(NB: I'll bet leasehold Apartment X/999 Smith Street, Nowheresville, that sold in 2010 for $500k went into the figures but when it sold last week for $5k it didn't!)

Some very sensible commentary in this article. It does however go against the narrative of the pessimistic and poorly informed individuals that have infested this site's comments section. No doubt the sookie babas will come out in force.

You've been reading Hot Copper again, haven't you?!

https://hotcopper.com.au/threads/director-selling-so-what.4233157/page-…

Everyone who disagrees with RBNZ policy is a "sookie baba"? Pessimistic, poorly informed? "Infested"?

I don't understand why a supposedly successful and happy person would come here every day to attack people and belch out so much negativity.

The words some of you guys use (you, TTP, MadMax) does not paint a very pretty picture of your personal well-being.

Money does not automatically equate to happiness.

Namaste Deepak Chopra..... This is a financial journal Fritz, if you want mindfulness you're in the wrong place.

Is common decency too much to ask though?

no

But it does give you options.

See ref above to "disdain"

"Infested". Sounds a little Eugenicist to me.

God forbid anyone should offer alternative positions to yours, and be supported in their views

I find these articles somewhat bizarre in their supposed efforts to paint a rosy picture for FHBs, when prices are 'ludicrous' (correctly used this week by ANZ economist).

The benefit for a FHB in terms of smaller deposit and mortgage required is miniscule with a 1% price drop on a lower quartile home...

I agree.

Poster Yvil is right about one thing, I have been posting on here for years that:

• The price of all things will correct and

• Interest rates will continue to fall.

So much so that about 3, maybe 4 years back, I wrote that :

“The terminal 2-year Fixed Mortage Rate will fall to 1.99% p.a.”

Whilst many back then thought rates would indeed continue to fall from about the 4.5% they were at the time very few, if any, thought 1.99% was probable.

So who will tell me today that I was wrong on where interest rates will go?

And if so, and as my views were in tandem, that my view that prices will correct is also not probable?

Low interest rates aren’t a sign that everything is peachy! It’s the opposite, and the lower they go, the worse things are and the more people will instinctively save.

One of two things is going to happen either:

• Interest rates are going to rise, all by themselves or,

• Asset Value are going to fall so that the cost of finance justifies the asset price ( LVR’s, if you like , coming down)

I doubt if interest rates can rise in the short term, but they won’t fall forever, and neither will asset prices rise, so it’s not a matter of ‘if’ but ‘when’ the most likely alternative to today’s markets distortions happens.

Appreciate the deep conviction of your investing insight.

Do you follow it yourself, and how’s it been going for you?

Genuine question

What you forgot to factor in bw the same as me is government intervention. House prices should have already gone down the toilet but they didnt because the government stepped in and started throwing money about so price discovery was null and void. I have come to the conclusion that the opposite to what should happen is now the name of the game. So now expect the mortgage holiday to be extended and interest rates at 1% and asset prices still going up.

Unfortunately there has been no savings in interest costs if you are on a floating (as opposed to fixed) mortgage - unless you are with Kiwibank whose floating rate is over 1% cheaper than all the other banks!

So don’t float then?

The big banks are also doing substantial discounts off their floating rates, I have a portion of my mortgage floating at the moment as a construction loan with ASB, and I’m paying 3.99% on that. I didn’t get a special deal either, it is their unofficial official rate it seems.

When will lower interest rates start to reduce rents then? Landlords main cost is reducing considerably.

What is happening now is that anyone who can raid their KiwiSaver and scrape together a bit of a deposit is much better off buying rather than continuing to rent.

Yet landlords are always whingng about their increasing costs...

Such a bunch of 'sookie babas'

Sales brackets seem to show that FHB bracket is not doing much better than last year.

For category of "residential only" (ie no apartments, units, sections sales incl)

Comparing June-August 2019 with 2020:

650-850k: sales up 4.8% from 1370 to 1436

850 -1.2m: sales up 43% from 1389 to 1987

1.2m - 1.5m: sales up 75% from 278 to 579

1.5 - 2m: sales up 108% from 219 to 345

2m +: sales up 57% from 219 to 345

Yes I know prices have gone up so people have moved up brackets, but that does not account for the huge difference in % increase in higher brackets compared to FHB bracket. Yes, I know some FHB buy stuff over $850k but that is not the range used in lower quartile comparators on this site.

Another relevant thing for looking at FHB market is how many 3 beds are sold relative to 4 or more.

FHB would be expected to be more after the 3 beds, one would think.

The trend from 2013 to now is for fewer 3 beds to be sold and fewer in relation to 4+ beds.

In 2013 in Auckland there were 13,010 sold of 3 beds and 23,706 of 4 beds+

By 2019 it had deteriorated to 9192 of 3 beds (- 29%) compared to 17,801 for 4 beds + (- 25%)

The ratio of 3 bed sold to 4+ sold was 182% in favour of 4 beds+ in 2013

By 2019 it had widened to 200%

In the June-August period, 2020 sales of apartments rose 21.7% in Auckland, cf 2019.

Section sales rose 56%

In June-August in Auckland, 3 bed sales rose 29% on 2019.

For 4 beds+ it was 32%

FHB are paying more each year and getting less space in square meterage.

This is inflation and is not shown on face of the price paid.

When people are having an average of 1.8 kids in NZ, why do we keep building and selling twice as many 4 + beds than we do 3 beds. Answer: because it is more economic and profitable to build bigger places.

More big places you build, less space there is for needed places that are smaller.

$37 a week dont really cut it ....wages stagnant to falling, job security gone, non discretionary inflation and demand drivers fallen off a cliff....you should preface this article with "this is not financial advice"

Perhaps you're all wrong in forecasting UP! or DOWN! and house prices on average will stay much the same. We could see house prices in desirable suburbs with a good proportion of debt free retirees and professionals continue to climb while prices in certain suburbs with a high proportion of new homes on small plots of land with highly indebted owners get slammed as unemployment rises and banks force these people onto the market.

Can we all bear in mind when considering value, valuations and price, as well as price "inflation" that people are paying more each years, for less room, that is floor space and land area. In Silverdale v Red Beach for example the price of new builds over period 2015-2019 did not ostensibly rise but the section size shrank 20%. This is rarely mentioned. Expense is more than price, it is what you get for your money.

Greg Ninness.... Could you please provide us with some analysis about the effects for somebody who will enter the workforce and begin the path to home ownership starting say 2021 or 2022. My strong suspicion is that lower interest rates and everything they entail will have a catastrophic impact. Am I wrong?

Late last year Orr announced to keep on spending, threatening the lender part for: CAR, TD guarantee, LVR & possible DTI tool back on the table. Then Covid came visit January, US & OZ decided something massive. It will be no knee jerk reactions he said for NZ, but yet couple months later his response to is precisely outshine US, UK, Canada & OZ in comparison to GDP, myself felt less confident now about his moves. He can be genius/clever at both ups or downs.. is he or his OCR team? in planning to save NZ economy, this way but instead actually pushing the snowball up over the cliff with supported by 5 millions team now, good if that ever increasing mass of snow ball toppled to the other side (unknown).. But what about if it's rolling backwards? - the confidence can reach crisis point at some stage, when large masses behaviour is no longer conform to any govt & RBNZ expectation, pretend that the massive inflation is hidden behind the RE value, is not happening. Imagine if those NZ bakers banded together to inflated the price of bread to say $100/loaf, those with poor performing savings, can still afford it. But it will be difficult to those with paper wealth. CPI pfft..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.