A surge of new listings onto the residential property market suggests an early and vigorous start to the summer selling season.

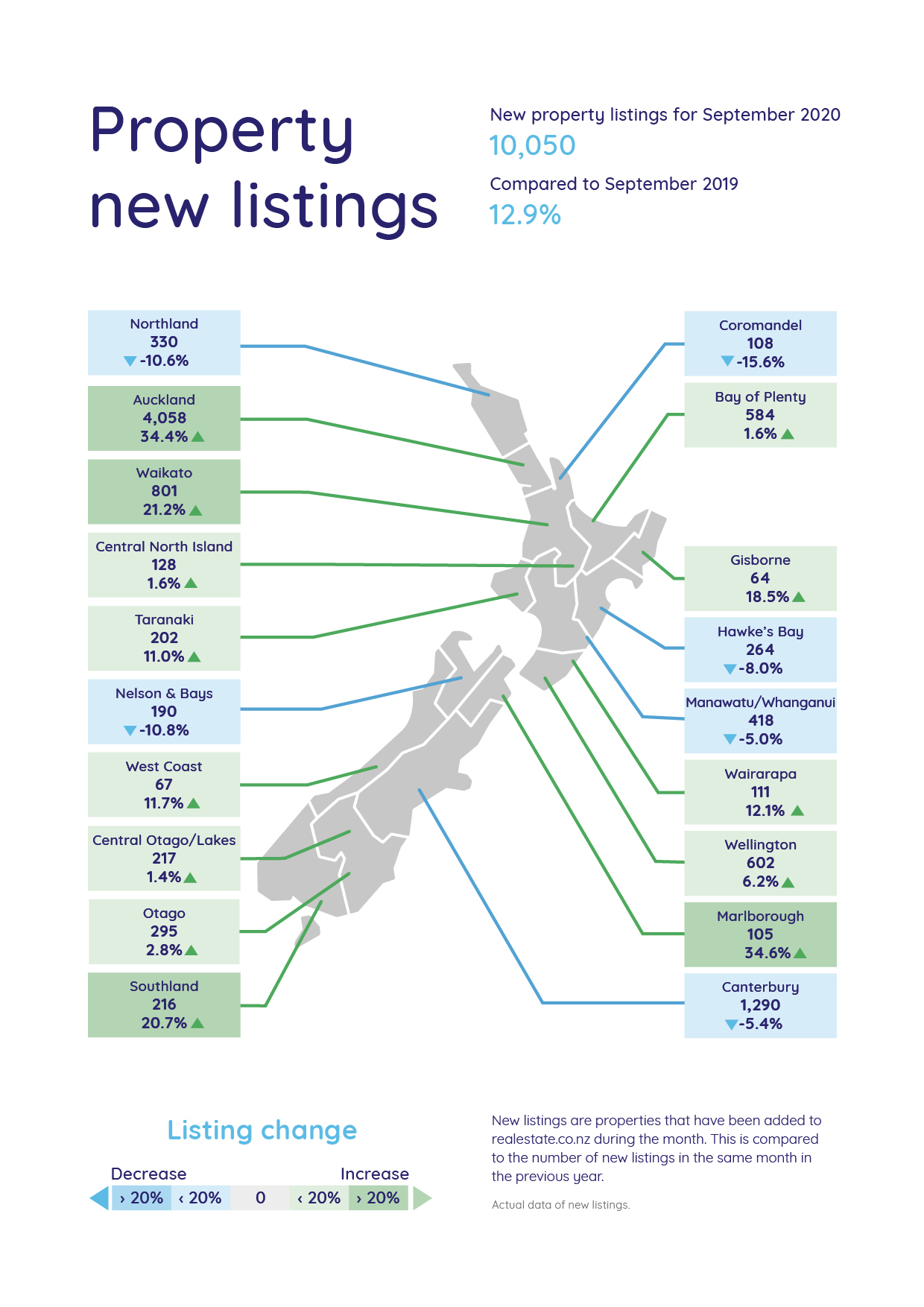

Property website Realestate.co.nz received 10,050 new residential listings in September, up 12.9% compared to September last year, and almost back up to the levels seen in the peak summer months of February and March this year.

The rush of new listings was particularly strong in Auckland, where 4058 residential properties were newly listed for sale with Realestate.co.nz in September, up 34.4% compared to September last year.

There was also a strong increase in new listings in the Waikato where they were up 21.2% compared to September last year, and in Taranaki +11.0%, Gisborne +18.5%, Wairarapa +12.1%, Wellington +6.2%, Marlborough +34.6%, West Coast +11.7%, and Southland +20.7%, (see the first chart below for the full regional breakdown).

Those figures suggest that potential vendors have been watching the strong sales results being achieved in the market over the last few months and have decided the time is right to sell.

While vendors may be optimistic about their sale prospects, their price expectations are more mixed.

The average (non-seasonally adjusted) asking price of properties advertised on the Realestate.co.nz website in September was $769,769, down 4.9% compared to August and down 12.0% compared to the record high of $874,886 set in April.

But in Auckland the trend was reversed, with the average asking price hitting a new record of $1,010,727, up 5.6% compared to August and the first time it has risen above $1 million.

Movements in average asking prices can be affected by changes in the mix of properties listed and are not necessarily uniform across the entire market, so should be treated with caution.

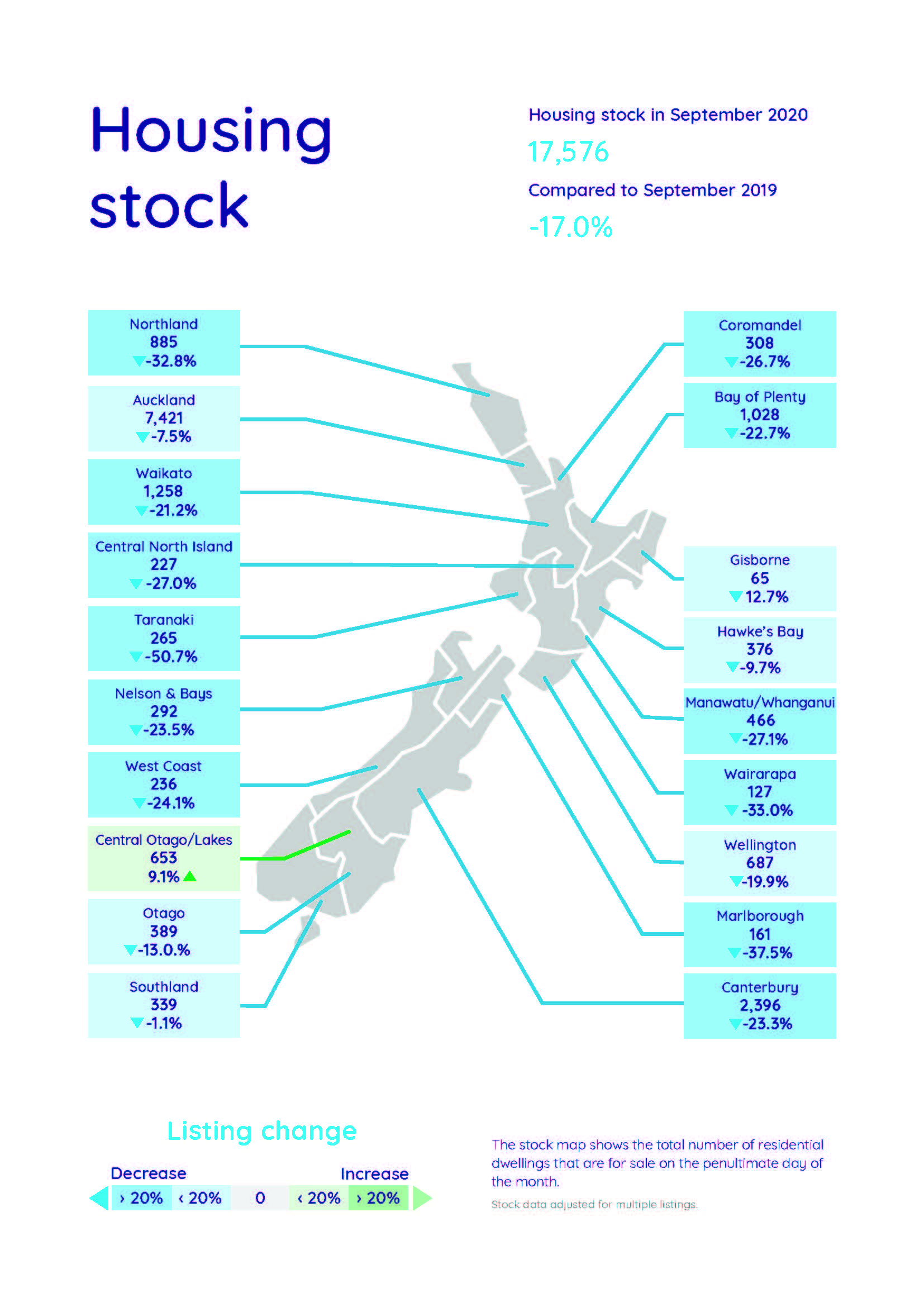

However even with the significant increase in new listings in September, the total stock of properties available for sale remains tight.

At the end of September, Realestate.co.nz had a total of 17,576 residential properties available for sale on the website, down 17.0% compared to September last year, and stock levels were down compared to a year ago in all regions except Queenstown/Lakes, where they were up 9.1% (see the second chart below for the regional breakdown).

Lower stock levels are generally supportive of higher prices, so all in all, the latest figures suggest a strong start to this summer's selling season.

The comment stream on this story is now closed.

106 Comments

Rats leaving a sinking ship.

Rats leaving a sinking ship.

I hope people are not laughing at your comment because it's a useful analogy. People on the Titanic saw a rat scurrying along and were disgusted. They would have complained to the next crew member they saw. Some people saw another rat 10 mins later. As Vernon Smith says, property bubbles burst, even though people are unaware of what's going on. 99% of the rats still haven't moved. People (not the rats) don't understand property bubbles like they would understand a sharemarket crash or the ABs losing a World Cup quarter final. The realization doesn't become obvious until things are in full swing and it's too late for them to react.

Heavy G

So they sell . . . . and where do they then live? Under the Mangere Bridge?

Maybe this rush is due to people considering selling with the idea of trading up.

As I have posted previously - there are "Covid winners". Those who bought homes five to six years ago, who have seen their house appreciate in value by 40% and their mortgage interest rated decline by 3 to 4%.

Now have great equity, lot more money in the pocket, most likely that interest rates are going to fall over the next year. Property has been great for them and the perfect conditions to trade up one step up the property ladder for that more desirable home which is now definitely within their grasp.

On RBNZ data, you are looking at about 704,000 or more in this situation who purchased just between Aug 2014 (earliest data) and July 2016.

They live in their owner occupied home because what they're doing is selling Air BnB's or surplus rental properties that historically housed foreign students?

Nzdan

By your previous posts; You are one of these "Covid winners" . . . you must be feeling a "happy camper".

Yes, a "Covid winner". The 50% increase in my property value in 3 years is of little practical use except I can now toddle off to the bank and borrow more money if I like? Or I could sell, lock in the gains and enjoy what renting doesn't have to offer.

The only good thing in hindsight is that I did purchase 3 years ago, which meant I didn't have to pay 50% more today. Had house prices not moved, I wouldn't have been at all concerned.

Nzdan

Yes, and you will also be pretty pleased with those fall in interest rates . . . and as RBNZ actions with the proposed FLP (possibly in November) and OCR possibly in March onwards it must be looking pretty good.

Be able to put that extra money into paying down the mortgage quite quickly as you must be at least a few hundred dollars a week better off.

Yes, those boomers aren't the only lucky ones in life. :)

Cheers

I checked in with my account manager yesterday and she was saying they were expecting to drop their rates in November due to the flp. This would be putting special rates down to around 2% now because of the lower borrowing costs they will get of the back of the rbnz. Crazy.

I really can't get my head around it. Short term drops are off the cards it seems but at some point the music has to stop.

PoppyC

Agreed

Reliable source of information is that ANZ expecting it likely that base mortgage rates will be between 1.5 and 2% mid next year.

Most things in life are uncertain and that is dependent on RBNZ expected action on FLP and OCR.

However seemingly best not fix beyond one year.

But if that is the case, they'll be buying into the same market? Which will negate the rise?

YDB

No.

When trading up one always sells and buys in the same market.

House may be up 40%, but increase equity far, far greater so importantly in a position to do so.

Simple calculation:

- Bought $500,000 house, 20% equity was $100,000.

- Sell house now $700,000, their equity now $300,000.

- Mortgage rate was 6.5%; annual interest cost $26,000pa approx $1,000 per fortnight.

- Mortgage rate now 2.5%; annual interest cost $10,000pa. That's $16,000 pa in the hand - over $600 per fortnight.

Its obvious:

These dudes now have equity of $300,000 and are $600 per fortnight better off.

Why not sell that $700,000 house and buy that $1m desirable home. Their $300,000 is 30% equity on new home (better than original 20%) , and at 2.5% interest on the $700,000 is $17,500pa - only very slightly more than the $16,000pa interest they were paying five years ago.

And (due to available RBNZ data) this is only those who bought six years ago . . . . those that bought much earlier - well you probably don't want to know as they will be far, far better off.

Remember:

These people have done very well out of property in the past five years or so and are upwardly mobile and they will be looking to continue to do so. Those who have been claiming bubble burst for the past five years well they are languishing while they have enabled their landlord to go out an buy another property at their expense.

Its a tough world for some . . . . but that was their choice of decision.

Cheers

But hasn't that $1 million house increased 300k (~40%) over that same period, meaning that no equity is gained when buying up?

It's just shuffling cards

YDB

No.

Its pretty obvious their increase in equity is giving them a far better house in which to live . . . and currently still paying about the same $ amount in mortgage as they were five or six years ago. They can't but feel pretty pleased - far better house, same mortgage costs as five years ago.

P.S. Note that RBNZ use of FLP quite possibly from November - and possibly OCR from March next year - is just going to make that mortgage interest rate fall and payments less.

That's one line of thinking. However, there may also be those who decide to stay put and retain the equity gains with extra weekly surplus $$.

Their increase in mortgage and payments you mean.

Lets rephrase the above transactions

- Bought $500,000 house, 20% equity was $100,000. Mortgage $400k

- Sell house now $700,000, their equity now $335,000. Mortgage $365k 30y amortization after 6 years.

Buy $1m House with $335k equity, Mortgage = $665k, amortized over 25years to hit the approx same mortgage free date.

Payments on the original mortgage (from the interest.co.nz mortgage calc) were $2518/month, Payments on the new 25y mortgage @2.5% are $2983/month, (if they extend their debt servitude to the bank to 30y again, its still $2628/month.. and god help them if interest rates start rising back towards 6%, then its $4k/month in mortgage payments over 30y.

Pragmatist

One only needs to look at those boomers in their very nice and mortgage free home - and irrespective of their value - they are not the house they could afford as a FHB.

Are you telling potential FHBs to look forward to periods of 10%+ annual wage inflation like the boomers enjoyed, followed by two decades of decreasing interest rates? We have reached the pushing on a string point with interest rates, halving the interest rates again to 1.25% will only drop 15% off your mortgage payments, unlike the previous halving which dropped 27% off your payment (on a $600k mortgage)

Pragmatist

No . . . just look at Nzdan. As he says FHB three years ago; house is worth 50% more and mortgage rates probably 1 or 2% lower already.

In a nice position to trade up with confidence and being prudent if he so chooses. His choice. . . . to or not to. However boomers with nice mortgage free homes choose to do so . . . and weathered increases in mortgage rates (in my instance going from 8% to 22.5%) and I have experienced three periods of property downturns.

It’s up to what one wants to do.

I can tell you that those of my generation who didn’t buy a home are now living pretty pitiful lives in council provided social housing (find out where and take a drive around them) and those who traded up the property ladder are now very comfortable- those who didn’t don’t seem as well off (and I’m not just talking materially).

Other than one who made some poor business decisions, I don’t know if any of my acquaintances who faced a mortgagee or bankruptcy.

While you talk of financial issues - high interest rates etc - the biggest hit to myself and friends came in the form of marital splits: half of comfortable is not comfortable at all and it took those who had splits some time to recover.

The easy risk free in life is to stay stay single, and stay in bed.

I wish young FHB all the best.

More like property snakes and ladders there p8. And remember that the whole ladder has been moving up - so are people moving up the property ladder or is the whole ladder moving together and leaving the bottom rung out of reach? Note that this ladder can also move downwards, so one should be very careful if they're near one of the bottom rungs.

IO

I know that you are apprehensive about the future of the property market . . . but has been commonly posted, RBNZ has been cutting OCR, recently removed LVRs, and introducing a newbie, FLPs. as they certainly seem to be stimulating the market for economic stability reasons.

Equally it seems unlikely that they will want to see a significant crash in the market for equally but negative Reasons.

Nothing is certain, but having RBNZ playing with you is having the likes of Johna Lomu playing with you rather than against you - it increases the likelihood of a positive outcome.

Important to make the effort - no mater how difficult- to get on that bottom rung rather than consoling one’s self and waiting for the bubble burst.

Cheers

Yes and if you haven't noticed Lomu is dead...much like the centrals bank ability to stimulate a market with more debt that the productive economy can't service.

Pick him on your team but make sure you don't solely focus on him as he may die an early, unexpected death!

Cheers . . . time will tell.

NZdan doesn't seem keen to take on more mortgage just to play keeping up with the Jones'. Looks like he has a house that meets his needs and sees the value in not signing up for longer periods of debt servitude to the banks.

Temptation is there, but why double or triple the size of the mortgage now? I'll just be doubling or tripling the interest dollars to the bank, would rather put those against the principal.

Instead we're paying the equivalent of a mortgage 2 - 3 x what we currently have, and once we're down to the right level we'll upgrade (50% deposit on upgrade).

Nzdan

Good to hear - nothing wrong with being prudent and protecting yourself as much as possible against a shock.

Right, but there are very significant differences largely due to being able to buy earlier and cheaper. This whole 'property ladder' idea doesn't really apply any more.

Take my parents experience - first home (a small one, not that suitable for kids) at 22, 25 year mortgage. By 27 their equity and income had increased enough to afford a house big enough for kids, also on 25 year mortgage. Had 2 kids. By 32 their income and equity had increased enough to buy a house big enough for kids, in a good school zone, close enough to family for mum to go back to work part time and have zero childcare costs, plenty of time to pay off 25 year mortgage before retirement.

Now consider a millennial couple. If lucky and on two good incomes, they might be able to afford a first home at 35 on a 30 year mortgage. What they cant do is buy a home not suitable for kids, if they want one. If they do upgrade in 5 years, they cant afford to take out another 30 year mortgage if they want the house paid off before retirement. They aren't likely to have massive salary growth, as that mostly happens in the early part of a career. So almost all of the factors that make it possible for people to move up the ladder dont exist- having to wait those extra 10 years or so before buying because prices are so high makes a massive difference to whether or not upgrading is a realistic prospect, as does longer mortgage terms

al123

Rubbish (as in a smiley face “rubbish”)

“Covid winners” taking a step up the property ladder currently.

Nzdan has that option if he so chooses.

What exactly is rubbish about it? Just making an assertion that there are 'covid winners' currently taking a step up the property ladder doesn't show that anything I have said is false. There are always exceptions, and you haven't actually provided any real life examples, apart from the example of an anonymous commenter here whose full circumstances you don't actually know.

So the point still stands - people are buying their first homes a lot later than they used to, and that means a lot of the factors that make moving up thr ladder a realistic possibility aren't in play. Simply saying 'rubbish' doesn't actually refute anything I've said.

al

See Nzdan’s response above. A FHB 3 years ago, an option currently of stepping up, but being prudent.

Printer8, do you not even bother to read the comments you are responding to? It's very frustrating when you reply, seemingly ignoring everything that's just been said. Again, one example from an anonymous commenter whose full circumstances you don't know doesn't say anything about general trends.

And again, people tend to be a lot older when they buy their first home than they used to be. Do you dispute this? Again, being that bit older, for all the reasons I identified, means that the idea of moving up a property ladder is a lot less feasible. Do you actually have anything to say in response? Please actually read what I've before posting any response this time.

But similarly, that $1m house was worth $715,000 5 years ago, so they are now paying $285,000 more for the same house. If they had managed to scrape together an extra $43k for their deposit, they could have bought that dream home then and would have been living in it for the last 5 years. Plus still be in a good position now. In fact, their bank would probably be telling them to buy an investment property or two with the $428,000 equity they have.

As I have posted previously - there are "Covid winners". Those who bought homes five to six years ago, who have seen their house appreciate in value by 40% and their mortgage interest rated decline by 3 to 4%.

Nobody really wins in a property crash whether it was caused by Covid or not. It doesn't matter if you think your house was worth 40% more yesterday than today. In fact, that's part of the problem. The perception of value is little more than fantasy.

J.C.

When I largely got out of investment property in 2016, "The perception of value is little more than fantasy" was definitely not the case . . . it was more about $$$$ in the bank.

Posters have been saying bubble burst for the past five or six years . . . keep hoping one day, one day, one day,

Cheers

When I largely got out of investment property in 2016, "The perception of value is little more than fantasy" was definitely not the case . . . it was more about $$$$ in the bank.

Posters have been saying bubble burst for the past five or six years . . . keep hoping one day, one day, one day,

Incorrect. Perception of value is 'fantasy'. An index does not represent the value of a house. And that is what people don't understand. People define 'value' in monetary terms. But if an index increases 40%, it doesn't mean that the monetary value of someone's house has increased by 40%. If 10% of housing stock was dumped on the market tomorrow, the probability of selling those houses at a level that satisfies value expectations would unlikely be met.

As for bubbles bursting, the NZ public, govt, and banks are woefully ignorant on the dynamics and nature of bubbles. I would say that the RBNZ is also ignorant on the how and why bubbles burst.

You should write to the ignoramus’s and explain their ignorance to them.

You could save the nation JC (hence your initials)

Reading Shillers work on 'Irrational Exuberance' and 'Animal Spirits' should be compulsory reading for anyone that sets policy (or an interest in behavioral finance/economics). What people fail to see, what you're pointing out, and what I witnessed in the US when their bubble burst, is that a tipping point reaches and suddenly greed is replaced by fear. You can feel it in the air and see it in peoples faces. They were bold and loud one month, the next they look like they've been hit by a bus and find themselves locked in negative equity in a dodgy jobs market with the bank hounding them. You think its impossible before hand, then can't believe how its turned and how bad it can get.

As I say I've seen it first hand in the US during the GFC. And it would appear NZ, despite all the money printing, really could find itself in very deep trouble if negative sentiment enters the market. How could that happen? Have you ever watched one sheep run across a road then wonder why a herd of 100 follows them when it makes no sense to follow? When enough go across the whole flock decides its going. Its best to go early or you might be hit by a car or be the last one left behind. Well that's how irrational/herding behavior works and that is part of the psychology of a bubble. We're not that evolved compared to sheep when it comes to some things (surprisingly?)

It will be people selling the additional home they have P8 that would count. I.e. 'lets just get rid of the rental/airbnb now'. If a flood of homes on the market with investors trying to get out could have downward pressures on prices. And how many homes in NZ are owned by non New Zealand residents? i.e. they don't have a footprint here but want to cash up and won't buy another home here so increase and supply and decrease in demand.

"So they sell . . . . and where do they then live? Under the Mangere Bridge?"

Easy, in the house the actually live in.

Are you actively adding to your portfolio p8? You seem very interested in it, and bullish.

Fritz

As you know, I posted some months ago I was cashed up watching and waiting for that 30% to 50% fall many on this site were calling (I thought more like 10% in line with bank estimates).

As previously posted I got out of property in 2016 for lifestyle reasons (travel mainly) but my wife bought last year as term deposits were rapidly falling. My retirement income is from a defined benefit Government scheme but have some surplus funds on which I don’t need or rely on.

My son 33 was keen to get a second rental and I I was looking to go halves with him as an investment on my part. He now has a property but after we jointly signed a purchase agreement on the property he decided to go it alone - not because he loathes me but rather he sees too much upside to doing so.

He is a case in point and has never been given help by bank of Dad.

As previously posted he was working in Auckland. Saw the prices of Auckland houses; five of six of his team at work moved out of Auckland and all now own homes while remaining one still in Auckland is still struggling to be a FHB

Moved to rural town - great weather and surf; has all the necessary basics - Hallenstiens, Farmers, Maccas, selection of Indian and Thai restaurants, three minute drive to work (yeah, yeah I know that isn’t on for some with their tastes).

Bought his first rental two years ago for $200k (not a typo) which is cash flow positive, bank now values it at $350k, buying again cash flow positive largely leveraging off that and unfortunately decided not needing Dad.

P.S. Anyone got a sister wanting a good looking astute partner with excellent genes? :)

So short answer to your question - still interested and see short term with continuing rise in property prices but probably missed the best. Currently still cashed up but now buying shares in a company that is pretty secure and doing ok (just returned the wage subsidy) and likely to have a better yield (and some capital gain) rather than term deposits. Will look at property though.

Best time for investment for housing may have passed. Medium to longer term (2 to 3 years) Post-Covid I see housing possibly having some minor correction and/or being flat as RBNZ address affordability issues (note no bank economists committing beyond 12 months).

However, for FHB it’s not simply a financial investment - it’s about a home. Quite a different scenario.

Clearly there are young out there - such as Nzdan - doing well. Appreciate the difficulties of FHB . . .

Agree with the rural town lifestyle, if you can make it work then it's well worth it. We got in with our purchase just as the lift doors were closing, same as what has happened with your son's rental. Except there are no jobs, my day consists of 4 - 5 hours of commuting predominately via Train but at least I can get work done.

Story as old as time:

"For in the days before the flood, people were eating and drinking, marrying and giving in marriage, up to the day Noah entered the ark. And they were oblivious, until the flood came and swept them all away." - Matthew 24:38-39

"At the end of September, Realestate.co.nz had a total of 17,576 residential properties available for sale on the website"

Interesting, when I search for 'any region' under the residential category, the website shows 25160 results. It showed 25143 yesterday. Why the huge difference between our numbers? Is a big proportion of the properties listed multiple times?

Edit: A quick search in my area revealed no duplicate listings.

Playing around a bit - excluding sections, boatsheds and carparks from the results, it comes back at 18,926. Maybe excludes non-livable listings?

Playing around a bit - excluding sections, boatsheds and carparks from the results

It would surprises me if people were not living in boatsheds already. I'm surprised we don't have shanty towns. In fact, shanty towns are really not that much more desperate than the state of many houses in NZ.

J.C.

Quite possibly . . . but those currently living in boatsheds are those who were crying bubble burst five years ago.

Those now living in nice homes well . . . they thought differently.

Impressed with your persistence.

Cheers :)

Or more likely mid late 20s early 30s couple now starting to earn decent salaries and wanting to start a family.

Those couples are starting to forgo having children

Save for retirement, buy a house, have kids: seems like its not even 'pick 2' now - its pick one, if you're lucky.

We chose house and we do consider ourselves lucky - although sometimes you make your own luck.

Most of these are likely to be ex-rentals and Airbnb's, that people have put on the market since they realize that the international tourisms and students won't be returning any time soon due to covid-19.

It is probably expected that the surge would be a bit late this year, with lockdowns hampering preparation and an upcoming election (albeit look like a fait accompli).

It would be interesting to see a breakdown of the listings by district within Auckland and property type. Anyone know if re make that info available? Or do you have to mine it from poring through the listings?

You're onto it

Meaningful comparisons can only be made on a suburb-by-suburb basis

Similarly, publication of the number of consents is meaningless on a region-wide basis

All the consents issued last month could have been 100% out in Pokeno

Consent numbers also include high-rise apartments making evaluation difficult

New listing up as RE agent are advising to sell potential sellers to sell sooner than later as now the market is high and in future may change.

Have been approached by RE agent to consider selling the investment property, if planing to sell as soon as before end of the year but definitely before March 2021 and was so confident that was advising to sell now at premium and can buy later at a discount.

He may be doing business as trying to get listing but is not wrong.

Anyone sellers, having doubts should get in touch with RE agent and should hear the same. They try to create FOMO for both buyers that price may go up and sellers that price may fall as in both they get their commission. Best time for RE agent as panademic and fear of reserve bank and government has helped them to boost their business.

Sounds like a stock RE agent spiel. To the seller sell now as the market may drop. To the buyer, Buy now before the prices go higher

Ban on foreign buyers does not work.

If you are aware of foreign buyers flouting the ban, the OIO would love to hear from you.

The Foreign Buyer Ban is irrelevant when you have let as many proxy buyers into the country as New Zealand has.

But agents are anticipating an upswing in interest from Chinese buyers as the new lunar year begins, with many buying property through family members living in New Zealand.

"Many have family here in New Zealand and they often buy property through them. The hardest part is not in fact the legislation, but getting their money out of China." - Peter Thompson

nz-it-worker

Recent ANZ (Australia) $1.3b fine suggests that banks are going to be treading very, very carefully not only in Australia but also in their NZ subsidiaries.

Why would a bank . . . or real estate firm or lawyer . . . try to circumvent or not be very, very diligent re FFB for the sake of a customer????

I haven’t heard of Barfoot and Thompson being hit with a massive fine, or even being investigated, despite Peter clearly stating in the national press, “often buy property through them”. Are you saying he’s lying, or it doesn’t happen?

You taking REA, One Roof, and Trump at their word?????

Clearly B&T are not in a position to be selling to FB.

Also, presume you mean Westpac (Australia). Wouldn't want to besmirch the good people of ANZ.

Worker

Correct my error. :)

It was Westpac dude!

Surely you aren't that naive p8?

Fritz

Not that naive to believe conspiracy theories.

A young Chinese couple paid $10 mio over reserve at a house auction in Sydney last week. They'd never participated in an auction before. I wonder who the real owner is. A provincial Communist party leader? The Triads? I wonder how the settlement will be paid.

https://www.domain.com.au/news/sydney-auctions-vaucluse-house-smashes-a…

Could be Taiwanese running away as the army is preparing across the strait? Perfect timing if the US is in the turmoil of who will be POTUS.

Unfortunately I had to change my position and move out of the DGM camp when I bought back into the market a couple of weeks back. All logic suggested a property crash but its just did not happen due to the government and media pumping the market and they are still pumping the market. Essentially they simply cannot let it fail as we have an "Economy" based on housing. Its all crazy stupid and must be as annoying as hell for FHB but thats just the way it is.

Carlos

Great on you - that is both buying and acknowledging change of heart.

RBNZ (rather than government and media) seem intent on keeping house prices up at least in the short term - the extent and effect of that wasn't appreciated in March-April. .

However, in the medium term post Co-vid (two to three years???) RBNZ may have a change in heart and accept some correction as they look to address the affordability disjoint between incomes and house prices . . . . however, as property is long term any short term fall in house prices will be irrelevant. Those who can service their mortgage have little to fear.

Can you disclose your interest in property p8? Are you an RE agent or a multiple property owning investor? You are on here an awful lot and with quite a pro- property angle.

I am not asking in order to bash you, but rather just curious.

Of course he’s owned or does own a lot of real estate

You can’t build up that much knowledge any other way

Def an investor(successful) over an REA

Forum should be grateful for his contributions and learn a bit

Most investors couldn’t be bothered with some of the silly commentariat here

I do embrace some of the contrarian views to moderate my bullishness, but my word there’s some deluded bears here

You don't need to be particularly smart or savvy to have made money from real estate in the last 20 years. The fact that someone has doesn't make them some kind of genius - it just means they've benefited from decades of government policies designed to enrich them at the cost of the generations coming after.

Your first part is 100% right

I’m dumb as f$#k, and still self-made millionaire(on paper) from real estate

Second part 100% wrong, I’m 2 years from being a millennial, gotta learn to adapt man

We much better off than 200 years ago

Stop making silly excuses

Not making excuses for anything, silly or otherwise. Merely stating facts.

It's just in the past I think he said he owns just his family home, which seems a bit hard to believe.

A bit like Ttp saying he wasn't in the RE game...

There's both silly and sensible comments here from DGMs.

Def agree Fritz :)

Fritz

Retired, enjoying a comfortable lifestyle, need to tap away at the iPhone to fit in with the young while at the cafe over my daily extended latte time, share some the postings to humour my mates, keeping the grey matter active . . . and I do actually care about the struggles of young FHB.

You are correct, I just own my own home now but the wife owns a rental (as sped are property). I do manage a low effort rental held by a trust of which I am not a beneficiary.

But do you own multiple properties? You denied this in the past, but it's hard to believe as you seem to be very motivated to pump up the market

Fritz

There is nothing I can post on this site to pump up the market.

One can actually take an interest and comment on the All Blacks without actually currently playing for them (not that I ever played for them).

Yes, essentially out of property since 2016 but continue to take an interest.

Have to say that sometime this sort of situation is not controlled by Government and RBNZ. If they can prevent this kind of things happen, then we wouldn't have Japan great recession and GFC. Both countries have elites and talented people with this sort of expertise but they didn't prevent it from happening. Why? Because they can not control people's behaviors. I don't like DGM and I don't think we have many on this website. But you need to know when to enter market and exist market to manage risks. Blindly following anyone's theory will do you no good.

heroes

From my understanding the trigger of the GFC was the sub prime mortgages packaged by US banks and sold gloably (especially Europe) - unfortunately the result of abysmal and ineffective regulatory oversight.

So yes, "elites and talented people" - but unfortunately some of the "elites and talented people" were baddies creating sub-prime mortgages, while the "elites and talented people" responsible for regulatory action were complacent or tainted.

Have you ever tried herding cats p8? If sentiment turns, attempting to control the downside of a bubble is like herding cats. The more you try, the harder it gets.

I made the same mistake mate, waited for the "drop" in prices for a couple of years. Finally accepted in 2018 that the system was too invested in high property prices & protecting the interests of the 1% investor class than an entire generation, so brought in then

I (FHB) bought a townhouse off the plans early last year. As a result of a nervous partner and other DGM opinions close to me I went back and forth on the decision many times. Completed just after the first lockdown. Bank valuation came in 150k over purchase price and the neighbour just sold for 250k on purchase price. There is value to be had and I am glad there are people on this website presenting both sides of the coin.

That caption picture is a great analogy. Housing market has many bubbles (balloons) and if one has a leak or bursts (Covid, unemployment rises, lockdowns, etc) then government have a endless supply of balloons and a big fat helium tank to keep the housing market rising!!

I have to ask how much of the increase in listings is simply an increase in activity overall... some of the figures do not bear out the narrative. On Wednesday 16 Sept there was 242 auckland residential properties added to trademe BUT yesterday Wednesday 30 Sept only 221. Similar results for sections 8 vs 3. The total residential listings on hand is also falling fast and is far below totals for this time last year... result more buyers chasing fewer and fewer properties. I wouldn't be too worried about a oversupply of houses.

Flying...

What is clear from months worth of comments on this site is that most posters admit something is wrong with the system around housing (govt & policy).

When studying revolutions one of the key factors determining a revolt in societies is the perceived legitimacy of the system. These comments hint and rapidly dropping perceived legitimacy... This is one of the biggest risks to housing in NZ and entirely overlooked.

Li quid

Revolution is likely only when a majority of the population are disaffected . . . . currently the vast majority of New Zealanders are not disaffected.

But yes . . . the housing issue needs to be addressed.

The disaffected may not be a majority, but they are a large minority. Half the population are renters now.

Yes and its a growing number. It will eventually reach a tipping point and the serfs will revolt - power in numbers. You just have to decide if you want to be Marie Antoinette or the guy with the pitchfork.

If you consider what prices have ignored, Covid, mass layoffs, airline and tourism at a near standstill, it will take direct policy action to turn the worm. The only policy being presented that would have an impact is TOPs tax base change. Away from product tive work, and onto land speculation via a flat land tax.

Eh, TOPs tax is not a flat land tax by any reasonable measure. Its a tax on equity in the land AND the improvements, levied at a rate pulled from thin air.

Yes its fortunate that we have a few generations of people who don't give a shit about their children. What a relief eh p8!

IO

“ . . . People who don’t give a sh*t about their children . . . “.

I don’t see myself as one of those.

Two things:

- that at the individual level one can debate about what the market is doing and personal decision making, and

- at the wider level debate what needs to be done to address the current affordability issue (and I have expressed options as to how the lack of a CGT is immoral, the ongoing free market attitude since then Rogernomics reset an the need for another one . . .)

I care keenly about my children and grandchildren and for that reason have often expressed concern at the falling homeownership for younger people.

However, it is not a conflict to argue both points; one is arguing about the reality of what is currently happening, the second arguing about what one believes should happen.

How do we know these figures aren’t reflective of more or less people using this website rather than the alternatives?

A YouTuber posted a letter that banks in USA are sending to people who are in arrears to pay their mortage

Can this be the thing to come in future even in NZ

Another doomer video on YouTube.

Do not think is happening now though possible.

Hi Richard, Do not know about future but as of now in NZ market is very hot.

A friend who had bought a house in Takanini for $750000 in 2017 was happy to see another house next to them / similar went for $945000 which since last few years were between $700000 to $750000 and to top it up they had bought a house just before lockdown in Manurewa for $630000 and have got an standing offer of $790000 by an agent that is profit of $160000 in just 5 months though he is not selling it as can built another house at back or remove the house and built 4 townhouse.

New trend in NZ, many are planing to turn into builder and only will know in future if they have been just lucky till now or will make a fortune from their new venture in future.

So no doom in NZ - Only Boom BOOM

Agree no doom for now but one should not forget that this boom is not based on fundamentals but on fiscal and monetary policy, so is wait and watch.

American Airlines to furlough 19,000 workers as aid program set to expire

It could be beginning the end...

I'd cash up as well. Demand is there. At the current interest rates it's like buying leasehold land. If rates return to the long term mean at some stage your toast.

An arm wrestle will develop between lower rates pushing prices up and unemployment/inability to pay pushing prices down.

At present the lower rates are working...........but my money remains on the deteriorating economic conditions pushing up unemployment and thus house price declines. Each to his own.

Lower rates can do just as much, I would be surprised if we haven't seen the full extent of it already.

b21

RBNZ feel they can wring a bit more out of their actions (e.g. FLP, OCR and LVR). Government also have a war chest still budgeted for to fund further action.

However agree; the critical factors are how long will Covid be an issue, and for how long are RBNZ and Government actions sustainable.

Another doom video

Wondering if the process has started as stimulus coming to end

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.