Construction giant Fletcher Building is reporting strong results in its New Zealand residential construction business - results that would appear consistent with the current heated state of the NZ housing market.

And the results in the residential side in New Zealand for the first four months of the current financial year to October 31 would appear to at this stage have the company running ahead of its own targets for the year.

The Fletcher share price rocketed by 60 cents to $5.10 in early market trading on Tuesday - though the whole market was very sharply up on positive news around a Covid vaccine.

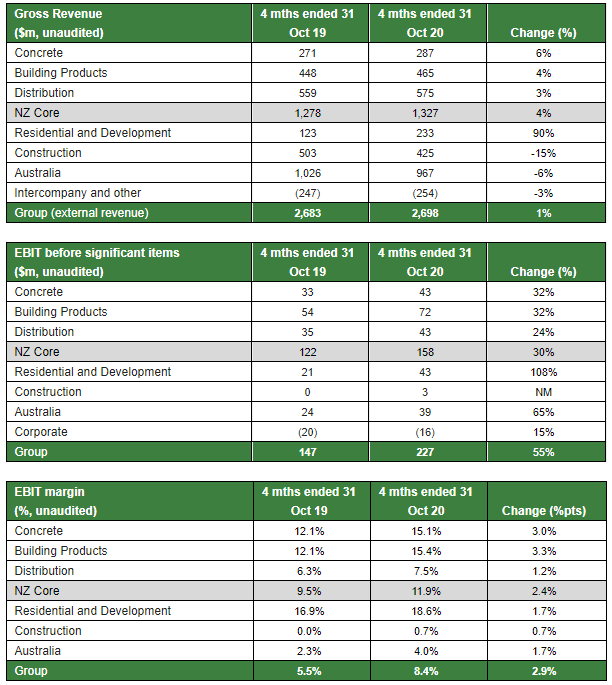

The company said operating earnings in the residential and development division for the four months were $43 million - compared with just $21 million at the same time a year ago. Earnings in what the company describes as the "NZ core" operations were up 30% to $158 million.

Operating earnings are pre-tax and don't include any write-offs or one-off charges - of which Fletcher has been incurring plenty recently.

Fletcher chose to update the NZX on Tuesday about its trading results despite the fact that it will be holding its annual meeting of shareholders in just two weeks and one day's time. It continues a recent pattern of the company preceding official announcements with unscheduled updates, having done something similar prior to the official announcement of it s results for the year to June 2020.

In the Tuesday announcement Fletcher said group revenues for the period were 1% ahead of the comparative period, supported by resilient trading conditions in both New Zealand and Australia, "especially in the residential sector".

"Revenues in the New Zealand Core were up 4%, with businesses exposed to finishing trades particularly resilient," chief executive Ross Taylor said.

"Demand for new houses has been robust, with 342 units taken to profit in the residential business, consistent with the Group’s objective of achieving 700-800 house sales for the full year.

"Residential and Development earnings were materially higher due to strong house sales, while planned Land Development transactions remain on track for completion in the remainder of FY21."

Fletcher has previously indicated that the first half of the current year might turn out to be better for trading than the second half.

In the latest update Taylor said the company was "pleased to have begun the new year well".

"As we look ahead, our customers are pointing to volumes remaining at current levels through to the start of the new calendar year. However, there is uncertainty in the second half of the financial year, with the impact of broader macro-economic factors on our markets in New Zealand and Australia not yet clear.

"Also, December and January are always lower trading and earnings months for the Group. At our Annual Shareholders Meeting on 25 November 2020, we intend to provide earnings guidance for 1H21. We will update further on trading conditions at our half-year results announcement on 17 February 2021 and at an investor day planned for May 2021."

This is the detailed breakdown of the results to October 31 provided by the company:

6 Comments

Housing is going to save the economy after all!

Fletchers; another company that should have been nationalised. Just like this one:

Air New Zealand is drawing down on a $900 million Government loan and has been paid wage and freight subsidies of more than $130m. "... it seems this public money is now being spent on lining the pockets of the senior management,"

Seems like a no-brainer, eh? Adopting a 'Temasek' model makes more sense rather than pawning off these return-generating assets of strategic/national significance to foreign investors.

Worst of all is that Air NZ is 53% owned by us. Should the Government do nothing about this would mean they are 100% OK with it.

See Boeing, United, General motors, etc, etc

Hardly any of these 'big corporations' that received govt/tax payers funded subsidy NOT reporting any profit results, all reporting a jump in their profit, more for shareholder dividends (If holding up pattern? is just like that a temporary 'rent freeze' announcement... means just that 'temporary/delay') - Even AirNZ has announced those no brainer bonuses.. indeed NZ has more elevated IQs than we thought initially, or is it collective cunning? - Those returning Kiwis from abroad (usually not receiving medical cover & wages subsidy in UK, US, OZ, Canada) soon will find out the next 1-3 years max - what it's all about in this little Aotearoa NZ.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.