The number of houses sold nationally in December was up +42% from the same month in 2019, reaching 8935 in the month.

But the REINZ claims there was a "lack of choice" in real estate markets nationwide at the end of 2020, resulting in sharply rising prices.

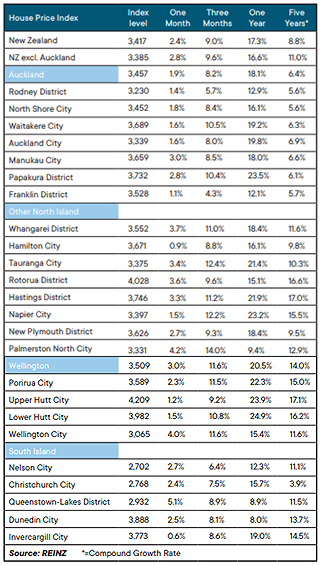

Nationally, prices were up +19.3% compared to the same month a year ago, but the median price was up +$4000 to $749,000 from November to December, only a +0.5% rise. (REINZ revised down their November median price from the $749,000 they reported last month.)

In Auckland, 3219 houses were sold in December, up from just 1932 in the 2019 equivalent month.

Additionally, Auckland’s median house price increased by +17.4% from $886,000 at the same time last year to $1,040,000 a new record high, and the fifth consecutive month where Auckland has seen a new record median house price.

Auckland central city area remains New Zealand’s most expensive district in the country with December seeing these suburbs reach a new record median house price of $1,280,000 – hovering extremely close to the $1.3 million mark. Not far behind, was North Shore on $1,235,000 and Rodney district on $1,005,000 showing how unaffordable the Auckland region is becoming – especially for first home buyers. The only district in Auckland now with a median under the $800,000 mark is Franklin district with a median of $790,000.

New Zealand house prices rose at an average of $332 per day in 2020. They rose at a slower rate in December, gaining a more modest $129 per day during December at the median level.

In Auckland, the December gains were +$323 per day, taking the annual daily gain rate to +$422.

On a proportional basis, gains were high in many other regional centers too. In total 11 regions saw record median prices during December 2020.

Technically, house price changes are better measured with a house price index that adjusts for factors like land area, floor area, number of bedrooms etc. Here is the latest HPI data from REINZ:

Median days to sell lowest in 17 years

In December, the median number of days to sell a property nationally decreased 4 days from 31 to 27 when compared to December 2019, the lowest in 204 months (since December 2003).

Across the country, 14 out of 16 regions had a median number of days to sell of less than 30 days which is the highest on record. Only Northland and the West Coast were exceptions.

For New Zealand excluding Auckland, the median days to sell decreased by 4 days from 30 to 26.

Auckland saw the median number of days to sell a property decrease by 5 days from 34 to 29, the lowest for the month of December in 17 years.

Taranaki had the lowest days to sell of all regions at 20 days – down 7 days from the same time last year. This was the lowest days to sell for Taranaki since records began. Additionally, Waikato (24), Bay of Plenty (27) and Manawatu/Wanganui (21) had record low median days to sell.

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

236 Comments

Shouldn't be too many leaky-homes still held by original owners. Problem solved

Leaky houses is a Wellington/ Auckland thing. EQ damage is the Christchurch nightmare. Take a look at https://homes.co.nz/address/christchurch/hillsborough/10c-grange-street… An EQ damaged house, sold for land value in 2015, plastered and painted, and resold twice, with a new driveway in there. A future insurance problem for someone.

The EQ took care of leaky houses and open fires in CHC, those houses and chimneys are gone.

Context, please. EQC stuff is at most 10K dwellings, 7K of which were red-zoned and demolished, leaving a few thousand only in the 'barely or badly repairable' camp. Total housing stock in the city is around 120K, plus the neighbouring TLA's have eaten Christchurch's lunch when it comes to land supply and new housing. The 'as-is' stuff is a drop in the ocean of Canterbury supply....

The "as is" stuff is everywhere, not sure where you get the 10k number from, there was a point last year where every second house sold was "as is"

Whoever would have thought low interest rates and printing billions of dollars would have such an effect, he said with a smirk...

Brrrrrrrrrr.

The monetary system is broken.

More to it than that. NZ's cap gains free status + heavily restrictive land use regulation play a huge role in ensuring low supply is added to that equation.

Interest rates are as low/lower everywhere else and house prices are not increasing at anywhere near the same rate... they've been falling even in Aus and their OCR is at 0.1%

They haven't constructed the same scenario of rapidly increasing population (until recently) and starving their councils of funding. We have created the perfect conditions for property to boom!

House prices are going up in Australia, especially in regional areas.

https://www.bloomberg.com/news/articles/2021-01-03/australian-house-pri…

Hi JRSNZ,

In fact, given the potential damage to the economy from Covid, the monetary system is working very well.

TTP

You'd hope record low interest rates and a small $100 billion+ would be "working very well"...

Google fed (m1/2) money supply. Last 10 years.

Google the 2019 stock market crash.

Then speculate what happens if nz base rates increase by 1%.

The global central bank system is not working well. All these Debt bubbles are well outside sustainable growth velocity.

If we all (global) need to print exponentially larger amounts of cash and grow debt, in order to maintain growth velocity. And we cannot politically deal with reversing this debt supply because it will pop the various capital bubbles. Its buggered.

Its like u loosing your job. But saying nah its all fundamentally OK, because I can just use my credit card to live off and when this one runs out I'll take out 3 more.

Debt and savings are opposite sides of the same coin and there cannot be one without the other as all money is created as debt. When debts are repaid the money is destroyed and that is just the nature of money.

Money created by the banks is private debt and money created by the government is government debt.

What we really have is massive currency devaluations and an attempt to create inflation to deal with the debt. None of that is, in itself a problem on its own (especially if it works). The problem is the wealth transfer going on. The labour/capital ratio is massively benefiting capital again. Working and Middle Classes under 50 are getting poorer each generation, while those who already have capital are seeing epic gains and increased influence.

Adrian Orr has made the life of the next generation extremely hard. Remember the name.

Great news.

Thank you, Labour party.

Have you been instructed by your superiors to target Labour with your comments?

This has been joint effort by both major political parties over the years as we all know.

Key 2.0 got this under control, just sit back and watch your capital gains grow.

Let$ keep moving New Zealand.

It's hardly breaking news that demand exceeds supply - resulting in higher prices. This has been the case for the last couple of decades at least.

Although I do get the impression David that you would have liked to put the word sarcasm in there somewhere.

That's an extra $590 a week people need to need to save to tread water for a 20% percent deposit, anyone keeping up?( I guess its only $150 for a 5%.)

Anyone want to argue this is sustainable?

https://www.rnz.co.nz/news/national/434554/escalating-rent-prices-forci…

"The reserve bank needs to support financial stability and New Zealand has maximized housing leverage. Housing can only go up." - Adrian Orr

Sustainable for who? First home buyers? I mean absolutely not sustainable for this group. But first home buyers arn't driving the current boom. It is the investor class, they are dumping worthless Fiat & moving into real assets which provide a natural hedge against inflation.

The market for everyone (its not sustainable politically, economically and socially). FHBs are definitely supporting this.

Do you think the market can be sustained solely on investors using excess equity to buy new houses (increasing values) allowing other investors with new equity to buy more cutting out the need for FHBs or savings?

?? First home buyers are making up a much larger percentage of the market right now than probably any time over the last 15 years.

It's a disaster. Unbelievable that this is being allowed to happen.

Just bought my 400th rental property. #work harder # dont buy avo on toast

Complain all we like and make snide remarks, but it don't fix the problem ....

/s. common mate, I know it's Friday but sharpen up. It's clearly a joke.

Low interest rates + no LVR's + $100billion pumped in = the most obvious thing ever

Oh riiight so that is what you are reduced to.

Thats quite a few, you end up needing to employ a team to maintain and manage at that sort of number, I know someone who did 50 on his own, and he was busy.

I hope he was complaining about how hard he has to work

Nobody owes you a house, stjohn.

Those who have a portfolio of investment properties have typically worked damned hard over many years to achieve that. So quit knocking them.

Frankly, as someone who rents, I wish I'd followed their example.

TTP

I never said anyone owes me a house?

Working hard through un-taxed capital gains to use unrealised leverage to purchase more. Ah such a hard job.

"leverage"

Leverage is the advantage gained by the use of a lever. Imagine a big rock you can't shift. You ram a crowbar underneath it, push down on the bar and the rock begins to move more easily. You now have leverage.

Define hard work.

Hard work = working like everybody else but being born 10-20-50 years earlier than you and/or having rich parents.

Immigrant. Working class parents (mechanic working 6 days/week) and a cleaner (schools and retirement homes). Saved, saved, saved, got a 2nd job. Sacrificed. Freehold at 42. I think I mentioned my 2002 Honda Jazz with 180k, and my buying 2nd hand clothing? Funny thing-never bought designer sunglasses ($5 from garage), smart phones, "brunch" (may be 1x/2yrs?). If you can't afford a deposit as a couple then you are failing. Acknowledge it is tough for single people. Put off kids, think ahead. Whine more about house prices, yawn. Why do I see low income people in Manukau outside our office eating take-out food, vaping, playing on the $1000 phone? No priorities.

Just because you've had to endure that, doesn't mean you should. That's the point.

Nice troll, full of assumptions. Just out of morbid curiosity, when did you buy your house?

He sounds like a pom. By his user name he might have been born in '66. Which means if he had paid off his mortgage age 42 then that was paid off in 2007, so he probably bought in the 90s when it was so much more affordable...

Alternatively maybe he's clinging on to England'a one and only experience of world football glory.

A bit of broken English in his comment. E.g. "playing on the $1000 phone?" Could be Chinese?

If you Google the username, one result is on a Chinese website with a whole lot of 8's in the URL.

*feels sad in Pom*

I always advise my young trainee Healthcarepro newbie (Pharmacy, Med, Nursing, Physio etc.), go to OZ to get rid of that student debt, leverage with more affordable (outside Sydney & MelB) living cost, grocery & surprise a guarantee of your TD savings! - then when the border open just suck up more property rental investment or land banking in NZ, they're by default the protected means of economic well being so suck them dry.

You are why we absolutely need a capital gains tax on investment properties, my choice would be 100%

"Technically, house price changes are better measured with a house price index that adjusts for factors like land area, floor area, number of bedrooms etc."

$ per bedroom would be telling - if our new supply of three bedders is priced where existing four bedders used to sit then not only are we paying more, we're getting drastically less. The argument of "people are having fewer kids so don't need as many bedrooms" doesn't seem to appreciate that people may have chosen to have more kids earlier if housing wasn't such an all-consuming, ever-escalating drain on income. I know I would have loved to have more than what I'll end up with, but adding a bedroom seems to mean an extra $250K on the mortgage these days.

On the flip side, if it's encouraging people to have fewer children then it's helping slow down population growth, thereby delaying resource exhaustion. Sad from a personal point of view but much better from a societal perspective.

That's an exceptional observation - except for the fact that at the first sniff of opportunity we'll continue to import 80,000 people per year to make up for the short fall. Aw jeez....

But, but our superannuation!!

Simply slowing population growth or even negative growth will do very little. Most of the consumption and over use of resources is by countries with no natural increase.

Sigh. Might as well buy a rental

Greater fool theory in play.

It's certainly been a spectacular run for those of us in property. I admit that I underestimated the Prime Minister and Government, I thought they'd buckle to some greater sense of fairness for New Zealanders but the woman absolutely is as ruthless and cunning as any New Zealand politician in my lifetime.

St. Jacinda, Patron Saint of Property Investors, we fall at your feet. You are working miracles for us.

She caught us all off guard Squishy. I was almost certain that some sort of property tax was in the cards. I guess so long as we are waging war against COVID then the property crisis can be conveniently ignored. But you are correct, superb politician. Secretary General of the UN potential if you ask me.

Squishy - St Jacinda, she made me an extra $2 mil capital gain last year that was unexpected and not needed.

I'll probably get nasty comments saying that but don't shoot the messenger !

Love to hear a comment from RP ? Come on it's been a while since we heard from you, I know you still read the column.

Shoreman.... here is a bit of advice that may help you immeasurably. Being wealthy and financially successful is not about increased equity in unsold property. Moving from a multi million dollar Auckland home to a retirement village in your 70s (which so many foolish Aucklanders do) is only financial success in theory.

In practice, financial success is still being young or youngish and living in a comfortable home with enough money to do whatever you want without selling any of your time (your most valuable commodity) by working. IMO that is real-world financial success in reality rather than on paper. Use your wealth to improve your life rather than to add a few worthless zeros to pieces of paper. I never saw a grave with net worth written on it.

Karl S - Thankyou for your un-asked for advice, clearly you are thinking inside your own constraints !

I have been retired for 8 years with a self funded retirement with so much excess cashflow I had to buy another property in last year.

Thanks to Jacinta/Orr my investment portfolio ( not counting my residences one in the city and 1 in the country ) increased from $13mil to $15+

Here's a bit of advice that may help you immeasurably !! Don't assume.

Happy investing !

Great effort mate. You'll get the knockers who hate landlords out of envy (or they pretend to have some wider 'social' conscience). If the latter they should hate cardiologists charging $57,000 for a TAVI operation (0ne night, <60min surgery), or QCs billing at $850/hr. Enjoy the retirement, I can actually state I genuinely envy what you have achieved.

Yes, because just like they need a place to live, everyone regularly needs the services of a QC or a private cardiologist.

Shoreman... nice one! After rereading my post I am still confused about what you feel that I assumed? With a net worth of $15M+ you have done very well and I sincerely hope that you are young enough to spend at least $12M of it (plus any additional money you make) before you are too old to enjoy it. Hard for most to spend much at 80+, for many it's 75+. Just out of interest, would you have preferred to retire 10 years earlier and only be worth $10m (plus 2 homes)? Or even have retired 20 years earlier and be worth $5m + 2 homes? We all make our own choices. #diewithzero.

PS: IMO leaving inheritance of more than a million per kid is selfish and even stupid as any excess money/assets should have been gifted to them earlier when they could best use it. Well done and GL.

I ask this exact question to friends, family and work acquaintances who have retired at 65. In hindsight, most would have gone earlier. The realization is that health won't improve and excess capital is worthless. None are "rich" but all travel internationally, afford meals out and replace cars periodically. Having watched 2 of my parents friends die from cancer in their mid 70s after a hard life in the motel industry, I targeted 55 for semi retirement.

Cheetah.... exactly. hope you get to retire early. Time is more valuable than money, no question.

I set a plan in 1998. Targetted 60 for full retirement. Amended to 55 with part time work several years ago. Ive just signalled with my employer I would like to go part-time from end of this year. I am very conscious that I will never run or ride faster than I did in the past. Time goes by and is irrecoverable.

Cheetahlegs...sounds like you have a good plan that will give you a better quality of life than the vast majority who post on this site even if some of them may have more net worth. Funny you mentioned running and riding. I googled myself yesterday (hoping to find nothing) and found only running and riding related things from another life time. Having the time to do the running and riding (rather than wasting your life spending excess amounts of life earning money) is the main thing, regardless of speed. Sounds like you have the right idea whereas I truly feel sorry for people with a mindset like shoremans.

Karl were you riding your high horse then, I'll bet you did extremely well

FH.. I was enjoying life and having fun so by my definition was doing extremely well. Being young back then I had to work a full time job while riding that metal horse 500km+ (and running 100km+) every week. Some would argue that it was almost as much a waste as spending excess time working to accumulate money and they may have a point. But IMO cycling and running is the time to fixate and think about money rather than boring everyone you come into contact with at the next Auckland BBQ. And hopefully all that exercise will allow me to do extremely well simply by living 50+ years beyond retirement and gaining some benefit from any money I may have made. 22 years retired so nearly half way.

I retired at 60 last March (I was 60 in late February). My plan during 2019 was to apply to work part-time from January 2020 until full retirement at 65. I worked as a nurse on a mental health inpatient unit. Started my part-time work in early January 2020 and it set me thinking. When my 60th birthday arrived, decision then made to hand notice in and retire in the March. I retired the week before lockdown. You can imagine how stressful it would be working in a hospital during lockdown. I have never looked back. How did I get to the situation of retiring? Hard work since the age of 15 AND property.

Cool. So how many 15 year olds today can go out and work hard? Sure some can, but go back 20 years ago when I was 15 I remember working 2 part time jobs (supermarket and McDonalds) and my work mates were predominately my age. These days when I walk into a fast food restaurant or a supermarket, I see people in their 20's / 30's with range of diverse ethnicity, assuming they're recent migrants. I suspect the opportunities for young to work hard these days do not exist like they did 20 or 40 years ago.

Nzdan you do have a point, but it is also about making your own opportunities. Where there is a will the is usually a way. I am not going to get into all the ways I did it but I am proud to say my own kids are doing it as well.

htp... I feel that it would be a pipe dream for a teenager to hope to make millions and retire early through property investment as some people from our generation did without serious parental assistance. The landscape has changed and it is much much tougher if not impossible.

Even back in the 80s it was not easy without help. I could have never done it without a 20K gift from my parents and more importantly. the ability to use (gamble) their home as security for my, probably reckless (but lucky), property investing. It is an insurmountable challenge for most of our young.

halfwaytoparadise...happy for you that you retired early. I'm sure that being able to do what you want with that five extra years will more than make up for the extra money you would have made. Doubt you will regret it. Property gave me the option to retire in my 30s and I have absolutely no regrets.

Worked from about 15 too, started investing age 12, left school 17, retired by 43. Could've done it much sooner if had got better job and occupation at 17 but never mind can't turn back clock. The whole journey required immense hardwork and sacrifice the likes of which I've met few people prepared to do, like going to live in horrible one horse town remote backward parts of NZ and do hideous jobs with zero social life.

So yep over 30 years grind and deferred consumption as it's called, worth it now... when I see mates in their 60s still slogging it out full-time... I think so, just wish hadn't been so hard and lonely at times but that's life.

Still waiting for my case of Parrotdog shoreman..I am assuming you are a scrooge and not paying up on our wager?

Hi Shoreman,

Yes - it would be timely to hear from Retired-Poppy (RP)......

In particular, RP, how about an update on how your term deposits are faring these days??

TTP

Well I guess RP would be paying tax on any profit so that makes RP much better than any PI in my book. Disgusting that we are still letting these pricks make all this profit at others expense and it’s tax free, makes me sick. Time for a small party (maybe Top) to campaign solely on a CGT, get 5%, and hold the balance of power.

TTP... have several TDs maturing this year and guess where they are probably going? Straight back into TDs. It may be a mistake but I hope you understand I have what I deem to be good reason and a good understanding of finance and risk. Who knows but I'm playing safe.

Might get a few more head tilts and frowns from her.

It's so much more fritz. It's like waching a magician using distraction and slight of hand, the media and public look exactly where she wants them to look. The patter on social media is just beautifully coordinated. I've never seen an interviewer get ahead of her, at best she is two steps ahead and at worst interviewers end up fawning over her in a slightly cringe worthy way.

She's charmed and conned both the centre-left and the centre-right.

Fritz.. I think most underestimate the power of 1.6M Facebook followers. That is about half our eligible voters and yes most followers will be NZers eligible to vote.

She's following an utterly trite, predictable playbook yet bizarrely people still lap it up like it's never been done before.

I guess it's that old advertising thing, sell the problem then the solution. Plus distraction. Turn the problem into a win. Focus on the positive. Or the ol naughty staff member sandwich technique... you see the manager coming think oh fuck here we go...the sandwich; good, bad, good. Job done so predictable, manager walks off to senior management, yep I admonished them, staff member gets wet bus ticket, happy days everyone back to work, doesn't need to be escalated. Fuck the sandwich!!

Yes it's been sensational alright, the woman has the midas touch for property buyers (I won't use the term investors). Biggest problem is how many more properties to buy? Or the other age old problem... have to buy a bigger property to house all the toys.

She's got the X-factor of unrivalled duplicitousness combined with homely Facebook approachability, feigning to her loyal followers that she's just like them, a crab-like ability to sidle out of tricky press appearances only to reappear from above in Saint like form waving the magic rainbow glitter unicorn wand.

Rethinking voting for her in 2023, keep the party going.

St Jacinda appears to be sitting on the sidelines - probably still at the batch.

we need to rename her Cha Ching St Jacinda....(for those with a property) hate to say what those without would like to call her

If you have Skin in the Game, there will never be a reverse in Govt Rulers taking a mile, if you give them an inch. It is a corruptive stance, hence why they become what I call pol-lie tititians. Aided by Cent-tral Bankers and Fiat Funny Money, of course. And Aussie Till dippers... Tax dogers are so prolific in NZ...plus a great deal, on Money Laundering...what could possibly go wrong, if they play their cards write and keep on printing.... Fiddling the Books is so last year...and goes on, adinfinitum.

Nothing new since the Dark Ages. The elite win, Middle class does the Hard Graft, Socialism never works...around and around we go. Tis a National past-time, taken over by Labour, never working. Foregoing wages, pausing Mort-gauges, all part of the new stratedgy......Funny Munny....zeros and ones...Elected and tronically.

Even the rest of the World has it off to a fine art. Even poor Countries, never seen a poor Polititiian. I do believ some would call it corruption of the means.....and they certainly have the Means.

Do have a nice 2021....Interest Rates to plunder....gotta go.....Past my prime.

....Oh and I did not get to mention my favourite song....Nelly the Elephant is packing his Trunk tomorrow....Plus his snuff box.

Trump, Trump, Trump. The Leader of the Pack is calling "Make me Great Again..." I only killed 400,000 mere bagatell in his estimations. And you ain't seen nuffin yet.

Maybe he is Biden his times.....not that he would recall...that Name. Megalamania, personified. Who would have thought it Presidential......Not I.

My thoughts for a new year.....No Capital required.....does not compute.

As the role of a “house” simply becomes more and more a means to store wealth then perhaps adequate supply in the traditional sense may be extremely difficult to provide.

Agreeing with you here.

We don't have a mechanism that allows an adequate stable supply, that is what we need.

What we have is a system that gives us an undersupply, and the Govt. counter to this will at best be an oversupply (they don't have any fine motor skills to control this), which will mean that some group will have to take a bath on the way down.

The reason it is almost impossible to have an adequate stable supply is this is the wrong time of the cycle to implement policy changes to achieve it ie it needed to be done at the bottom of the cycle and that opportunity has gone.

So we will need to wait for the next bust, which the way things are going won't be that far away.

Wonderful News! I'm so happy and so are the home owners in Auckland.

Your comfort with inequality is disturbing.

Team of 5 million my arse.

He might start to worry when it affects him, eg. When violent crime and homelessness soars

In 2004 when price growth also peaked at 20 percent , house prices would rise an additional 40 percent in the following four years. The impact of the significant RBNZ OCR cuts, alongside their recently introduced lending platform, has not yet fully played out in this housing market.

Cowpat - 4 more years of house price inflation in this cycle, rate of growth will tapper off !

I am not sure whether I understand your point, regarding rate of growth ?

Investors uber alles

There you're a simply 'supply & demand' which can always be distorted. No overseas buyer, no demand? dang.. wrong, Supplied with 'current market place affordability'.. dang Kiwibuild stock are still out there for grabs. Then the highest QE in comparison to country size, economic, population at the same time while no CGT assurances given, before you know it.. more demand created by multiple property owners/investors. Watch how NZ pan out 2021-25, when every levers being pull up, down, sideways intentionally/unintentionally.. and all goes sip into..?

I wonder what effect reducing the number of people in need of housing by 500 000 every five years would have? Brad Olsen wrote a piece on our housing shortage yesterday but typically not even a mention. Even the economists have to know it is a huge factor so why do they never mention it? Are we in such a toxic place that even questioning immigration settings risks falling foul of our cancel culture. It seems so.

And sadly, anybody with aspirations of UN grandeur would be extremely reluctant to lead the conversation.

The equation of wanting much lower rates of immigration = racism / xenophobia is ridiculous isn't it.

Obviously some people who are anti-immigration are bigots, but it's by no means an automatic link.

From my observation I think the equation is

Higher Immigration = Racism/Xenophobia

Visited my old hometown recently. I left there in my twenties and don't recall racism as a thing then. But it has since had a huge influx of hardworking immigrants that place a higher value on financial success through their stronger work ethic and commitment to higher education. They are quickly taking over the businesses and professions in the town and the more laid back kiwi locals aren't happy that they are tumbling down the social order. Racism is definitely a thing there now, both ways.

I can confirm that 100%. Shouted at yesterday whilst going for a walk with my wife. Local bogans are unhappy.

Every immigrant's experience is different, but my wife (Japanese) feels like confrontational racism has dropped quite a lot towards her since she arrived in NZ in 1997.

I think - generally speaking - Auckland is quite tolerant.

I can see another great improvement happens in the workplace in term of recognition and support of cultural diversity. More workplace leaders are of minorities these days. Meanwhile, as a Chinese, I have experienced more casual racism from other minorities such as Maori and Pacific islanders

Immigration shouldn't ever occur beyond the capacity of a countries infrastructure (and that includes available housing stock).

Fritz... in the good old days before all this PC/ cancel culture rubbish many Aucklanders started to refer to Howick as Chowic. That was a sure sign of what was to come regarding immigration so I mortgaged myself to the hilt and bought up large. Presently I could buy rentals without a mortgage but am choosing not to. I have a bad feeling about where things could easily lead.

Very wise. From time to time (eg now) there are little signals that interest rates are about to rise, driven by expectations of more real economy price inflation. There is so much leverage now, that small rate changes would be a big deal. Way too scary for me to go long on bubbles and debt, but good luck to those with more courage than me.

That's the main reason economists and other mouth-pieces have lost all credibility

Yep, boring and irrelevant.

Quite a lot of commentators here don't realise that the governments QE program does not give the banks money to lend out. It's purpose is to increase bank reserves and so lower interest rates, banks do not lend out their reserves they create new money when they lend.

The Bank of England explains here.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Delusion is deep seated.

If central bankers have walked softly all these years, the so-called big stick they told you they carried with them was what Ben Bernanke had openly talked about the government’s “printing press” all the way back in November 2002. People took him literally when he was really doing this as a way to more forcefully back up the rhetorical method of moral suasion. If you fight the Fed, he was saying, then you’ll be sorry.

So don’t fight. Please.

This thing is powerful that it can conjure the exact mode necessary at just the right time. Under threat of deflation, the very subject of his talk, that would mean a forcefully inflationary path back to growth and health; and if it gets to that, you better get out of the press’ way. As Bernanke put it:

"Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation." [emphasis added]

You no doubt recognize Jay Powell’s “digital money printing” and “flood” in what his predecessor’s predecessor was claiming.

The question, therefore, is why go through all the mess and bother? Why the need for this convoluted game of trying to get everyone to act on its behalf? If it’s so easy, then just use the thing, do it yourself! Link

In this market, Kiwibuild 3 bed townhouses in Auckland are an absolute steal at 650k. Unfortunately there's only a trickle of them via ballots. So it's literally a lottery.

Wild how National had four bedroom Axis properties going up for ballot at $650K but were accused of doing "nothing" for housing affordability by the mob who then came in and just light a rocket under house prices. Is the PM still dishing up ice creams in Tairua?

If I was a FHB struggling to get a home I would be entering every single Kiwibuild ballot.

Mayaswell buy a lotto ticket too...

Every month in 2021 for homeowners will be like winning the lotto division 2 ... payout $46300 last draw. It's not something I agree with but if you cant do anything to stop it then may as well be on the gravy train too

The cookie cutter kiwibuild houses are still very average even at 650. Pay a bit more and you get a far better house in a far better area.

This was the advice we took from our solicitor, and it worked for us.

Not KiwiBuild, but rather than competing with every other FHB and investor for properties in the wildly overpriced $400k to $600k range around Christchurch, we ended up buying a large 4-bed for just the 2 of us.

We'll be paying more than our rent per month for the mortgage repayment, which was our original goal, but it's still less than what our rent plus our deposit saving would have been, so we can pay off more each week or save to buy ourselves something nice.

What do you mean by 'a bit more' and by 'far better house in a far better area'?

In Auckland you would need to pay 900k minimum to do that.

Yeah they building them near us in Mt Roskill not that far from Mt Eden. I imagine you would be getting close to a $1 mil house now for $650k if you win the ballot.

Housing in NZ seems to follow the Rebel Sport/Briscoes business model of selling all sorts of over priced crap. Wouldn't it be fun though if periodically throughout the year houses actually sold for a reasonable value. Can see it now. Easter - Auckland 30% off! Boxing Day - Wellington 20% off! Wouldn't that be fun?

Time for AKL to downsize to Invercargill...only hour or so away from Qtown and central otago and you will have plenty of coin to enjoy the wineries.

Notice the massive 5-yr compound growth outlier: Christchurch at 3.9%. Thanks to the LURP, which effectively ended the City Council's Cluelessness when it comes to land release, it's still possible to get a small house/plot combo for a price beginning with a 3 in the neighbouring TLA areas, or a 4 in Christchurch proper. Read it and weep, Awklanders....

Demand exceeds supply in housing markets - result is higher prices

Demand from whom?

If NZ has a similar wealth profile as the US , only the top end of town can afford to apply for a bank issued residential property mortgage. The rest are on welfare.

Just 39% of Americans would be able to cover an unexpected $1,000 expense, according to a new report from http://Bankrate.com.

That's down from 2020, when 41% of people said they could cover a $1,000 cost with their savings. Link

.

Don't get sick in the USA as the medical bills will bankrupt you.

Depends where you live:

Dallas, Texas.

25yr old Teacher on $58,000, just bought a three-bedroom home for $155,000 (median income to house multiple of 2.67)

Interest rates at approx. 2.3%

https://www.cnbc.com/video/2020/12/17/58k-a-year-dallas-millennial-mone…

Probably happens in Invercargill too. I think it says more about the stupidity of paying public servants the same no matter where they live than anything else.

Well there are two ways to interpret that, 1) raise the wages and/or lower house prices in Auckland to give the same disposable income as they would have in Invercargill, or 2) lower the wages and/or raise the house prices in Invercargill, so Invercargill is the same financial basketcase as Auckland.

The amount the teacher is getting paid is about equivalent a NZ teacher gets paid, BUT look at the house price. You can't a comparable like that in NZ, even Invercargill.

Interestingly in Texas, because they have a higher-skilled workforce, the average total of all incomes is higher than many other States, but the relative price difference for skilled people is slightly lower in Texas compared to other States. What is important is the disposable income in the hand after paying for housing etc. so in Texas they can be earning less and yet still have more disposable income than other states.

Aren’t their state taxes quite high to pay for all those 30 lane sprawl induced highways?

If you look at that video link for the teacher, it does a break down of her costs.

Yes, they have higher taxes relative to their total costs, but their costs are lower, so the total taxes aren't any more than ours.

Plus the point of the right tax, is that they are meant to cover real costs, whereas the 1/3 to 1/2 of the extra cost we pay for housing in NZ above what they should cost, gets us what extra? Only more debt to pay of, but no more amenity.

Instead, wouldn't it be better if that extra money went to a worthwhile expense like our kid's education, health, saving for retirement, or public improvements like PT and roads?

And some folks still say - Oh, printing money is the answer, it doesn't cause inflation....

We don't call it inflation in New Zealand. We call it "Red Hot Property Market" Like in Zimbabwe it was "Red Hot Bread Market". The only difference is that the printed money in NZ is not released for bread - but for .... you guessed it... huts!

And it was more than likely stale bread, just like we get NZ building code minimums for what we have to pay.

It depends what the money is used for. There is plenty of spare capacity in the economy that the government could employ but it prefers to use monetary policy rather than fiscal policy which is one of the definitions of neo-liberalism.

NZ in the name of the Crown issued net new government debt to the value of $53.035 billion in calendar year 2020. I suggest the majority was monetised by the private banking system so not to crowd out the private business sector.

Government spending cannot crowd out the private sector as all of its spending is financed by the creation of new money via the RB. Borrowing is not necessary for a sovereign currency issuer and is a historical anomaly from the days of the gold standard and fixed exchange rates. If you wish to understand how government finances operate then you should study MMT and not neo-liberal orthodox economics. Economist Wynne Godley gave us this sectoral balance identity, (S-I)=(G-T)+(X-M). There is no identity there for government borrowing, look it up. Only the private sector borrows to finance itself. The government issues bonds to remove reserves from the banking system that its spending has created and QE returns them back again, it never finances the government.

Economist prof Bill Mitchell explains here why governments issue debt when they don't need to.

http://bilbo.economicoutlook.net/blog/?p=45106

The government issues bonds to remove reserves from the banking system that its spending has created and QE returns them back again, it never finances the government.

What happened before QE when sovereign debt was still being issued?

{kind=link}

{kind=link}

When we bought our house 15 years ago I remember a pie at the local bakery was $2.80. Now it’s $3.80 so about 40% increase. However our house has increased by about 300%.

I don’t think it’s the money printing, it’s the low interest rates. Coincidentally interest rates are about 1/3 of what they were when we bought, so the interest payments on the value of our house haven’t actually changed in 15 years.

I'm just glad I got the sale & purchase agreement accepted for our first home just before Christmas. The market valuation we just got done for the bank finance indicates we're already $10000 over what we paid, and we don't even own it yet. We go unconditional next week.

Congratulations.

Congratulation's to the bank (owner of house) or the person paying the the mortgage?

The person buying the house. I attended an open home on Saturday and saw many hopeful young couples. It was good to see one of them win the auction on Wednesday. Whether they paid too much is moot. I can’t afford to buy a second home for what they paid so am looking at a beach home instead. I can’t see this market changing.

Just reward for hard work (sarc). But congrats.

Same we bought just after Christmas and are in the same boat. Very happy to have got in while we could.

Good for you. It is a huge weight off though, isn't it?

For recent buyers yes because we don’t have to worry about a rising market diluting our deposit anymore but I do feel for those who are still in the position we were in for a long time.

Well put. Me too.

..good for you on you 3 week time horizon. Premature gladness at it's finest.

I wouldn't be so concerned if rents were falling like in Sydney as an example. But they are not...and landlords are creaming it both ends. Oh well better have a beer and watch the Prada Cup..

I really do think if they changed the Kiwibuild thresholds in Auckland it would help, especially if LVRs are brought in and retained.

Just did the calcs, for a 700k 3 bedroom townhouse or apartment, a 650k mortgage (30 year term) is $575 pw. That should be serviceable for a household on say 80-100k.

If the goal is to increase affordability then that will only increase demand much like the homestart grants and use of kiwisaver to buy a first home.

Use of KiwiSaver for a first home is always going to happen, and there are probably more FHB's coming in under the income cap for First Home Loan or First Home Grant due to loss of earnings last year, but they are unlikely to be able to buy an existing property in Auckland for under $600k. The majority of those are going to be straight-to-rental purchases by investors.

Depends who is earning the $80K. You'd lose $28K in PAYE/KS/SL payments. So $52K to play with, of which you'd be committing $30K of to pay your mortgage. So $22K to pay food, insurance, rates & utilities, vehicle costs, child-related costs (assuming one earner with the other at home looking after the kid to save on childcare costs)...

Or... you just move to Australia, where your $80K is probably closer to $95K + more generous super, houses AND living costs are cheaper... you can see where this is going.

But if you had gross income of 80k and kids then you would get topped up with WFF, potentially quite a lot.

Admittedly it's still tight, but doable.

I agree Aus is an attractive proposition. That's what I did for awhile until a family issue dragged me back here.

If you have $80K and you have one kid, you get... $17 a week.

3 kids is the magic number for max benefit ratio, enough to make prof jobs, ie fulltime teaching not worth doing. I personally know couples in that boat where the wife wanted to work but gets more on wff or wtf as I call it.

Thirty years of debt bondage to the banks, a frightening prospect. Something is seriously wrong with this country now.

Thirty years for a government-provided "starter" home, no less.

Yeah. But isn't it better than nothing???

It's effectively close to what we did just over a year ago. And it's way better than renting.

Plus there's always possibility of moving on to a better property over time, as many people do.

That only works if the prices keep going up forever, if debt stays cheap and incomes can stay ahead of inflation. Not just one of those things - all three of them. It might be "come what may" gamble I'd feel more comfortable making if we had similar default laws like they do in the US, but we don't, and people can't just walk away. At the moment, the 'better property' is going up faster in price than whatever you're living in - meaning more and more debt has to be taken on. We are rapidly moving from a situation where letting things continue at their current rate without intervention could be passed as negligence, to borderline treasonous.

Yeah buts what’s the alternative for a FHB right now? You can keep renting and watch your rents climb and move from place to place anytime the landlord wants you out in 90 days and in 7/10 years have nothing to show for all that rent or take on a 30 year mortgage put your payments toward something tangible and likely a massive capital gain and equity in the same period. Both situations are nothing like the dream times boomers et al had but one is clearly better than the other.

All true, but ignores the risk of interest rates rising, pumped by inflation caused by loose monetary policy.

How did you work that out Fritz? Less than 20% deposit you're probably paying between 4% and 4.5% interest due to low equity fees and exclusion from special rates. Certainly nothing like the 2.29% that WestPac just advertised. So the repayment is more like $730 a week. That would be a challenge even for a couple on $100k a year pre-tax.

That's a fair point, I hadn't considered the big interest penalty for low deposit. Point taken!

So maybe it needs to be a 120k household. So upper middle income households.

But maybe that is just a reality that needs to be accepted. And again isn't it better than nothing to have more home buying opportunities for those households? These are often households of the people that are really important to society - teachers, nurses, police etc.

The reality now is, sadly, home buying won't be an option for a middle income (or lower) household. It's not necessarily the end of the world if the rental side of things is better.

The point is though that it doesn't have to be the reality that home buying is out of reach for middle, or even low, income workers. It didn't used to be the case, and it doesn't have to be the case in the future. Why just sit back and accept something that could - and should - be changed?

But we need to be realistic. Even making housing affordable for young middle income or even upper middle earners is hard enough. Can't we start with that?

Also I just don't think it's realistic for it to be affordable for low income earners, without massive government subsidies at least.

I think it could be realistic if the govt didn't have such a massive state housing waiting list...

I think too much realism is the enemy of real progress We just need to look at what we did with Covid - we might have said, well, it's just not realistic to stamp it out, etc. But the govt decided it was worth spending billions of dollars to do so, and to keep businesses going and to keep people employed. Shows what we can do if we have the will. Imagine what we could do if we said right, let's just spend the money we need to fix the crisis. We've done it before with all the housing built immediately after ww2. No reason we cant do it again.

Maybe we could hear from Adern, Robertson, Woods, Orr about how this has all been part of a plan, you know, like something they have control over.

Or would that be asking too much?

Someone needs to seriously grill them. I expect the opposition will once parliament is back.

They are meant to be releasing some grand plan to make housing more affordable, but all it will involve is rebating a rent to buy type scheme which is keep the front purchase price the same, but take a rebate of the price at the other end, which is just smoke and mirrors, and more than likely increase demand.

Could also include some Bread and Circus inducements. Any guesses?

Well considering they don’t want house prices to go down that just leaves more subsidies or higher incomes. I doubt they can realistically achieve the latter unless it was via taxation changes.

I'm hoping ACT will have a lot to say. That's why I voted ACT, because at least David Seymour is not afraid of throwing punches.

How would ACT drop house prices though? They are hardly going to introduce a GCT or have govt build houses or allow appartments in Epsom are they.

Also act campaigned on removing the foreign buyers ban. Imagine what that might do to property prices post pandemic.

Inflation erodes debt. Inflation is coming.

investors know this.

So, its buy anything for silly money.

Esp stuff not even built yet. hence inventory crashes.

Off plan purchasing means pay fixed price now and end product goes up in value.

2016-19 it was opposite.

Plus, I see government let in a net 80,000 pre CV19 in year to feb 2020.

SO much for cutting immigration (demand)

Yes, but if much of the present demand is grabbing tomorrows purchaser today, the buyers won't be there on the future date when all the new off the plan stuff comes online.

Unless the immigration tap is turned on to fill the gap.

I don't think inflation is coming. I think we are entering a prolonged period of low inflation.

Normal economic rules and recent bond sales indicate low inflation.

.... but I'm with Mike Kirk. I think inflation is coming and it'll creep up slowly at first then suddenly when it hits people we won't know what the heck happened.

Just can't see how this much money printing can have any other outcome. Pity the people leveraged up relying on those low interest rates lasting forever.

Govt wants inflation. It wants it so bad and needs it to erode the crap mountain of debt it's now sitting on.

Sorry fritz but: dream on. Inflation is essential to erode debt that cannot ever be paid.

Bernanke said all this in 2002

Dream on? Says the man with an even poorer track record on forecasts than me!

There is no doubt that the FED have been trying to create inflation since 2002 but they have failed. They created asset inflation and a massive wealth transfer from labour to capital.

There is definitely inflation in food prices atm. And there are several possible reasons why the pandemic and post-pandemic world will be inflationary. But unless wages go up, what we are seeing might be stagflation.

#rentcontrolnow - Hutt Valley

https://homes.co.nz/address/lower-hutt/woburn/1-20-ludlam-crescent/4jD9l

Two-bed flat just rented at $500/week - against a Tenancy Services market rent of $385/week.

So, the government's own website is under-estimating market rents by 30%.

This has to be urgently addressed.

#rentcontrolnow

Kate I will explain this again, you really are slow... Only someone on the back foot with a bad rental history would agree to that rent... sure let's have rent control but you do realize that those untouchable types will never get a private rental. Govt rentals are non existent in that area so that's a wasted hope. Result more homelessness. GL with your lobby

You're dreaming if you think that there aren't hundreds of people with excellent rental histories and credit who are desperate for a place to live and realize the market is so tight that they are in no position to negotiate.

There are also hundreds in the other camp, and many of them would probably still look after your rental well most of the time. They are a risk so some landlords charge more and the tenant via winz will gladly pay it. Right now there is a surplus of rentals available but landlords will also wait for the right tenant rather than any tenant.

A surplus of rentals? Again, you're dreaming. On trademe there are a grand total of 12 rentals in the whole of lower hutt with at least two bedrooms that cost less than that.

And do you think rent controls will magically solve the shortage (just going along with your narrative) or create new rentals for all at lower cost for all. Ah yeah sure mate, I think its you who is dreaming

My 'narrative', if you want to call it that, is simply that you are wrong about the fact that people with good rental histories are able to avoid paying high rents (like 500 per week for a two bed in the Hutt) because there are are surplus of rentals (there arent) and only people with poor rental histories have to pay rent that high (not true). I didn't say anything one way or the other about whether rent control was the solution. But at least you now seem to be acknowledging the problem.

No, any problem of dramatic lack of rentals, if there is one is limited to select small areas probably. Certainly not the case in Auckland which is up 40 percent on average for the time of year or across the country which is up 36 percent. How many rentals is there usually in 'the hutt' and what do you put it down to and whats a reasonable solution. Don't just suggest everyone should leave or do a Kate and say landlords should 'be socially minded' and drop rents.

Where are you getting those statistics from?

Trademe... where do you get yours

Can you be more specific? Where on trademe does it give stats about the number of listings in an area relative to last year?

there is definitely a huge shortage of rentals in Lower Hutt right now. hard to find anywhere.

There's always a massive rental bottleneck this time of year because of the students, even without a red hot housing market

No, I don't expect landlords to be socially minded and drop rents, I'm calling for regulation/law to make rents affordable. I'm also collecting data on when these properties were last sold and at what price. The only landlords that will find my proposed controls make them unprofitable are those who purchased recently (i.e., last year). The problem is it is last year's price rises, that are setting the 'new' market rent expectations.

"... data on when these properties were las [sic] sold and at what price."

Secondhand homes are usually going to be high yield Kate, especially old homes from 40s, 50s, 60s 70s, 80s and 90s that's par for course... I included 80s and 90s as there were leaky homes building issues that need rectifying. The purchase/sales price is irrelevant in these cases.

That's my point - they are high yields and therefore won't find rent controls a real problem - whereas the high rents are a real problem for tenants in mid-low income brackets.

Rent controls (under my proposed formula) would have little/no effect on new build buy-to-lets. They are targeted at higher income earners - out of the scope of my research/concern. Generally, their asking rents are already within if not under the weekly rent maxima (under my proposed formula).

Have you ever owned a rental unit or house Kate. This may seem harsh but lower quartile housing is high yield for a reason that you either can't comprehend or wilfully refuse to accept. As its not a difficult concept I think its the latter. Its funny you say that new builds are "out of the scope of my research/concern." as previously you were citing new build examples as being overpriced and not affordable for rent. You have narrowed your targets

Never owned a rental unit, but yes, previously owned two rental houses - one upper quartile, one lower quartile. Oddly enough, the upper quartile home ended up with damage that I ended up having to go to the DT in order to get reimbursed for.

I record new builds (upper quartile rentals) to make the data set complete. So far, none have been let at the $700 plus/week asking prices. One recently reduced their asking rent to $680/week. A $700/week rent is affordable based on a gross household income of $123,000 pa. You can check out the calculator here;

https://www.calculate.co.nz/rent-affordability-calculator.php

"Previously" but not anymore eh Kate, I wonder why. Your problem Kate is you expect others to take all the responsibility while you bleed them dry....

Your problem is that rather than gracefully accepting when you're wrong about something you instead resort to being nasty.

Well dont you get "nasty"... I could pick you up on gaping holes in your argument but I can't be bothered.... I will leave you to focus on the lower huts "if you are OK with a bit of gun violence and gang fights." The area doesn't sound too appealing

Thats why he's already had his account banned 3 times, or is it 4?

Do you know anything pragmatist

I know that your current account will be banned sometime in 2021 just like the previous ones, and i know you'll pop back up like a case of herpes.

You would be the first one to accuse others of trolling.. never mind.. obviously you are still licking your war wounds.

Lol, you're just an obvious and tiring boor these days.

Feel free to not comment then if you think that way

Flyinghigh - I'm just dealing in facts - your point is speculative. These are pretty standard prices at the moment across the Hutt.

Of the six 2 bed rentals in the Hutt (listed since I started this exercise 3 weeks ago) the average percentage under-estimate from the tenancy.govt.nz site is 20%. Meaning, we are witnessing a rapid rent rise for the 2-bed (low end) bracket in this area. And that 20% average is skewed by 1 of the 6 being under the estimate by 13%.

In other words - here's the best bargain at $360/week in the Hutt;

https://homes.co.nz/address/lower-hutt/stokes-valley/62-delaney-drive/5…

And hey, you only need a household income of $62,000 per annum for that to be considered affordable (the average salary in Lower Hutt).

What have you been smoking Kate

From Trademe lower hutt area, there are 5 x 2 beds under 400pw ... and there are 7 x 2 beds under 500pw, some being freestanding homes that look very appealing.

The example you sight for 360pw is a very tidy example.

I would not call these rents excessive, you pay more than that for one bed flats in a block in some centres

Whatever makes you happy, or in your case unhappy lol.

I'm using the realestate.co.nz website and am gathering data on new listings only (i.e., the rentals listed in the last 3 weeks).

If you think the $360/week property is 'tidy' - well sure, anyone can sweep up a dump. A dump that was purchased back in 2011 for $115,000 and currently has an RV of $260,000. Under my proposed weekly rent maxima for the Hutt (RV/1000), the affordable (i.e., reasonable) rent for that flat is $260/week.

"well sure, anyone can sweep up a dump. "

That is very offensive I challenge you to present a house for rent. It takes a lot more time and effort and cost than your cursory comments suggest

The current standards require certain levels are met.

Wish I could post pictures here of my rotted out window frames (previously bogged, painted and since rotted out again). Bare barge boards that haven't seen paint in a longtime. Mouldy and damp - the basement floods in easterly rain. The list goes on. Atleast the whole package is worth 1.5 million now.

One can see all 10 layers of paint and old wallpaper from whenever the property needed a 'spruce up'.

I'm sure my landlords have put a lot of effort into making the property safely habitable (sarc).

Atleast I managed to get the rental property over the crowds of desperate people viewing at the time.

The norm is to have someone living in your garage in Auckland these days

I get the picture... thats not something I'd be happy with either. However dont worry I have been in your position many times, the house we just left after two years there was probably just as bad and yes it was our own house. It was the pits when we bought it and we just moved in and gradually worked on it but still not enough to get ahead of it

On the bright side for you, the new tenancy laws will allow you to make some minor changes and repairs to the house so it will be win win for you and your landlord... sarc

The norm is to have someone living in your garage in Auckland these days

Yes, so I've heard as well. I worry the country is losing its soul. None of us should accept this. Real pressure needs to be put on the government. The new tenancy regulations and the healthy homes initiative are a start, but a livable/healthy standard of accommodation needs to be accompanied by affordable rent, to my mind.

And from what I've observed so far, based on the prices paid for the rental properties, most landlords will make reasonable, as opposed to extortionary, profits.

I have a mate who lives in his daughter's lined and comfortable shed. Free rent in exchange for maintenance work around the house. Hes out nearly everyday so its a deal he is happy with and has done for several years. I hope you don't start making a big fuss and cause the govt to clamp down on people in sheds! Its his personal choice

Ah, rent free! How unaffordable is that?

I take it you are not very familiar with Stokes Valley if you think the 360 a week example on Delaney Drive is a tidy example of an 'appealing' house. This might help: http://i.stuff.co.nz/life-style/10346588/Lets-live-in-Stokes-Valley

Edit: or perhaps this, if you want something more recent: https://www.nzherald.co.nz/nz/gun-fired-during-gang-brawl-in-stokes-val…

I lived briefly in Stokes in 1967. Nice to catch up on how it is developing...

One of those 'under 400' houses you've mentioned is actually a three bed with one bedroom 'occupied by a single Male.' Three of them are in a very unsafe area. The remaining one explicitly states on the listing: 'Section is NOT fenced and on a hillside so not ideal for young children'. (Its also in an industrial area, right on a very busy road). So rentals in the Hutt under 400 appropriate for a family with young children? None - or I suppose 3, if you are OK with a bit of gun violence and gang fights.

Thanks for caring and for providing insight on the sum of all listings on TradeMe. I'm only looking at the past three weeks of new listings and the picture is also grim.

$323/day pure profits without lifting a finger- better returns than any other investment classes ever contrived by man.

The whinners blame immigration, then they blame Nick, Bill and John. Next they target the Asians, then they blame their grandparent baby boomers. After that they blame RMA and interest rates. Not satisfied, they blame Adrain, Grant and Jessy. Then they blame QE and their employers. Whilst the world moved on, they convolute on who else should be on their blame list.

Those who are responsible for their lives took concrete actions and are reaping the fruits of their labour while the laggards continue to spiral down the gutter with endless belches of blames.

People can either be A.) Responsible for their own lives and take action, or B.) Join the gutter flow.

What a horrible sanctimonious post

History is full of people who assumed they knew best, or who mistook their circumstance as purely the result of their own competence and unquestionable intelligence. More often than not, they were wrong. And that's about the nicest thing I can muster in response to this post.

@ CWBW ...."$323/day pure profits without lifting a finger- better returns than any other investment classes ever contrived by man."....and that $323 a day is going to be worthless when everything else goes up with inflation to match house price inflation....and you'll be back to square 1

CWBW.... so who do you blame then for what is obviously such a serious problem?

Thanks to internet and smartphones! Information travels fast, wealth is created/shifted fast!

Yeah to the Cayman Islands

Forget about the supply demand law argument for moment, wondering what's going to happen with the price? if LVR 40% still in place, suddenly RBNZ been given DTI tool, Banks must confirm with CAR, OCR is up as per housing inflation (not as per artificial CPI), RBNZ still rolling out the TD guarantee plan, then finally the Covid's QE initial program is just about slightly lower than OZ/economic/population size eg. around 60billions or by owe means stretch it to 80billions.. rather than straight to 100billions (OZ just last Nov. announced that amount, yet for population of around 5x larger than NZ) - something is not quite right there in NZ.

Wondering how sustainable this whole party is without a strong immigration

It probably isn't but I tell you this, it would be better to come off that high before there are too many more people to worry about. There is probably too many already given our fairly narrow range of activities that earn from exports.

I have quit working and have employed my house to do that job instead. Wow over $300 a day, thats insane. More than I ever made doing a real job. Still cannot believe it really, still the writing was on the wall after we got lucky with Covid, then the government started the money printers and then openly told everyone the expectation was that house prices only go up, what else did you expect to happen ??????. I went from predicting a 25% house price crash to buying a house in short order last September.

I know, our house has averaged $200 per day over the last 3 years. It's a shame it's not a property surplus to our requirements.

Nzdan... bought one for 780K in April and One Roof valued it at over a mill last week so if they are right that is about 1000 a day. What a messed up society we are creating.

Sorry to burst your bubble (so to speak) but its only when you sell and the dollars hit your bank account those amounts are locked in and realised, until then it's only a number on a screen, subject to fluctuation

#rentcontrolnow

Housing crisis now housing chaos

https://www.nzherald.co.nz/nz/housing-crisis-now-housing-chaos-emergenc…

Smith said families were spending anywhere between 60 to 80 per cent of their household income on rent- forcing many out of the private rental market.

Well at one point I was spending 80% of my income on the mortgage but what made it bearable was that your mortgage is paid off one day but your rent continues forever. I still think its about logic, if you cannot afford the rent then you cannot afford to have a family. Its not your human right to have kids and then expect others to pay for them.

This a Leaky Home...

Just leaked.....today.

https://www.thesun.co.uk/news/13792316/putins-secret-1billion-palace/

Freebies.......for Nowt..

This speaks volumes....No honestly. Pardon is a Tool, used by tools, for tools, inexpplicably.

https://www.cnbc.com/2021/01/19/trump-pardons-expected-day-before-biden…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.