By Greg Ninness

It became slightly easier for aspiring first home buyers to get into a home of their own in many parts of the country in January, thanks to a modest drop in prices at the bottom end of the market and an even smaller fall in mortgage interest rates.

According to the Real Estate Institute of New Zealand, the national lower quartile selling price dropped back from its record $550,000 in December to $525,000 in January, ending seven straight months of price increases.

Around the country lower quartile prices declined in six regions - Northland, Waikato, Hawke's Bay, Wellington, Canterbury/West Coast and Otago, while lower quartile prices reached record highs in five regions - Bay of Plenty, Taranaki, Manawatu/Whanganui, Nelson/Marlborough and Southland.

In the country's largest market, Auckland, January's lower quarter price was unchanged from December, with both months being down very slightly from the record high set in November.

Mortgage interest rates also fell marginally, with the average of the two year fixed rates charged by the major banks declining from 2.58% in December to 2.56% in January.

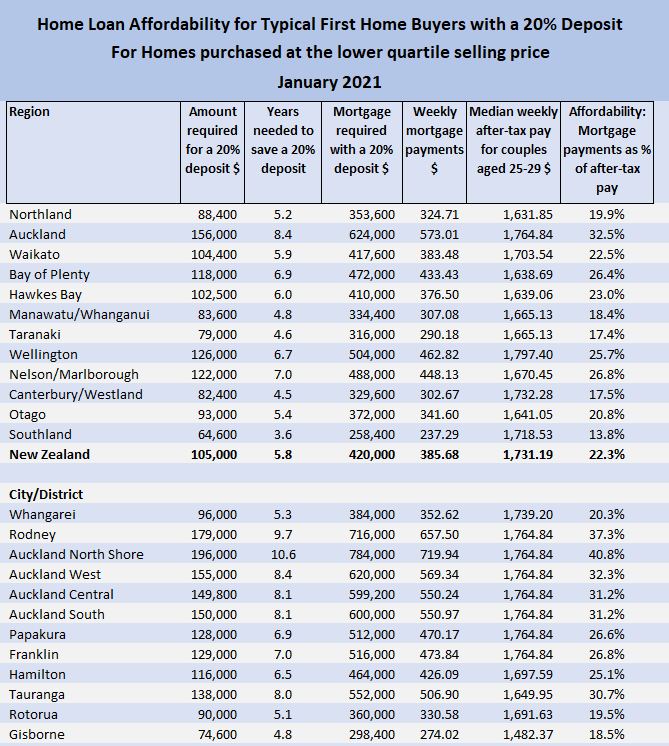

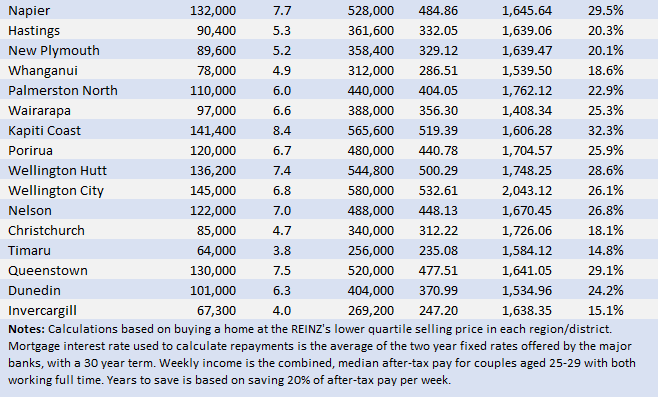

The dip in prices meant the amount that would need to be stumped up for a 20% deposit on homes purchased at December's national lower quartile price, dropped from $110,000 in December to $105,000 in January.

While that's a welcome step in the right direction it may be of little comfort to many aspiring first home buyers, because the amount needed for a 20% deposit on a lower quartile priced home has still increased by $16,000 over the last 12 months, rising from $89,000 in January last year to $105,000 in January this year.

That means that over the last 12 months, the amount needed to be saved for a 20% deposit has increased by an average of $308 a week.

In Auckland, where the lower quartile price has increased from $688,000 in January last year to $780,000 in January this year, the amount need to be saved for a 20% deposit has risen from $137,600 to $156,000 over the same period.

That's an extra $18,400 a year or $354 a week first home buyers would need to have saved just to maintain the purchasing power of money they had already saved for a deposit.

That makes it likely that even those saving hard out for a deposit would have gone backwards over the last 12 months, with the extraordinary rise in prices pushing their dream of home ownership even further out of reach.

Interest.co.nz estimates a couple working full time at the median wage for 25-29 year olds, would need to save 20% of their combined after-tax pay for 5.79 years before they would have enough for a 20% deposit for a home at the national lower quartile price.

That's up from 4.95 years in January last year.

In Auckland the time needed to save a deposit has increased from 7.51 years to 8.44 years over the same period.

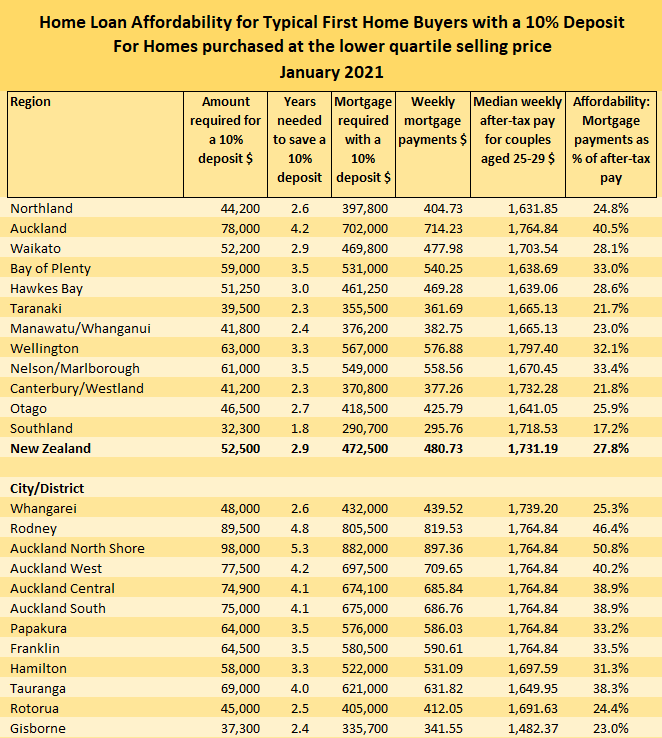

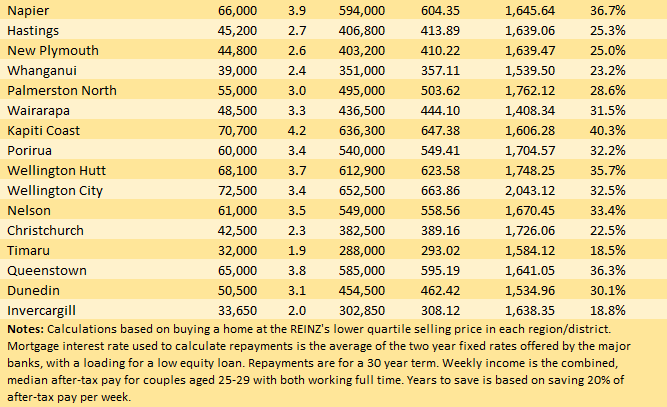

The tables below show the main affordability measure for typical first home buyers, with a 20% deposit and a 10% deposit.

91 Comments

“Over the last 12 months, the amount needed to be saved for a 20% deposit has increased by an average of $308 a week.”

Did you know most people had to revert to reduced hours for reduced pay due to the lockdowns. Did you know majority of us did not get any form of pay rise and a lot of them had to take a pay cut?

Did you know that the government and the Reserve bank, when they thought house prices will fall, took mere seconds to introduce counter measures.

Did you know that when these measures did the exact opposite and fuelled the prices, they continued to add more fuel with other insane lending measures?

When the people have had enough and demanded that they do something to quell the house price rise, they are now thinking about it. Thinking and thinking and thinking and thinking. They receive very good advice from others including the treasury but surely they know better. They will probably call a working group and pay them extraordinary amount of money to “talk” about housing issues. In the end they will no nothing!!!! Absolutely nothing all while they and their families invest in property with their inflated salaries and reap benefits of capital gains.

We live in a sick society lead by sick people who campaign on something and do the exact opposite. We say NZ is not corrupt, oh please just look at Grant’s ego driven smirks these days when he announces about announcements that might be announced in the next quarter. Pathetic government. Head tilt everyone, be kind. Aroha xx

Yes. But it's a good problem to have!

We aren't fighting the military in the streets and being clubbed and shot to keep us in our places.

We aren't scrapping the gruel from the bottom of a communal cooking pot and deciding which one of our 10 children will live or die.

We aren't fighting a plague of locusts so large it would be twice the land mass of New Zealand.

We aren't wondering if one of our neighbouring countries is about to drop a bomb on us and obliterate all of our people.

We aren't freezing to death in our beds as the global climate changes sweep across the country.

No. We are lucky to have the insignificant issue of home affordability as our singular concern.

(NB: Being told we are lucky to only have lung cancer and not AIDS doesn't give us a good problem to have)

You also forgot that finding out that the sentence is only life imprisonment rather than execution is also a better outcome.

IE, all your comparisons are pointless and are strawman arguments.

And is no excuse for not acting correctly to produce the right outcome for housing affordability. If you don't then that sets us up for the mindset for all those things you have listed as worse outcomes, to happen.

(I think you've missed my point - which is your point! ie: Your first line and my last?

As we all know, it was Adrian Orr that told us "it's a good problem to have")

I note that the people that say "it's a good problem to have," are not the ones with the problem and are not the ones with any solution.

It is not an either or problem, your reasoning is a fallacy called false dilemma.

https://en.wikipedia.org/wiki/False_dilemma

Plus it is a very bad problem to have indeed, except for a few wealthy milking the most of us.

I thought bw was being sarcastic there

Same. A form of parody to show just how absurd the line 'a good problem to have' is and the absolute insanity of continuing to do nothing about the housing crisis, simply because 'things could always be worse!'. I think that was unfortunately missed.

Fair enough, we should have comic sans available to use in this case ;)

Do you hear the people sing?

Singing the song of angry men?

It is the music of the people

Who will not be slaves again!

And so on and so on etc..

bw.. I would much rather have AIDS than lung cancer (in the developed world) these days. And it is only due to border closures that we are not fighting a plague of locusts. We will be doing so again soon enough.

Very corrupt, the central bankers of the world have had the hand-break on loose money removed "because covid" and NZs RB governer and govt seems to want us to be No. 1 at bubble blowing. However bubbles are bursting see NZX, ASX, Dow Jones, Nasdaq. What are they doing to do now?

Print and put more money.

Yes, Schiff is saying as much about the US in his latest rant:

https://www.youtube.com/watch?v=Z7bBURKmYHI

QE to infinity

Honestly I'm not surprised the government is not acting. If prices drop existing homeowners will lose hundreds of thousands of dollars, new homeowners will enter negative equity and be stuck with the house they don't want for life, banks may suffer from increased defaults, first home buyers will continue to sit on their hands and wait til the house they want reaches budget.

The urge must be overwhelmingly stronger to instead offer help to FHB's, including using your retirement savings, low interest, excess debt and grants to help them buy a home, all the while keep house prices going up. That way you've given the baby what it needs, right? And nobody else suffers?

But let's face the facts. Home ownership used to be a safe, boring way to invest in your own retirement. From what I've seen it's pretty far from safe and boring. Something must be done NOW, the longer we put this off the worse it will become.

That’s just MSM fear mongering. Stress tests have shown banks would do fine if a 40% drop in house prices eventuates. As for those that bright recently. House prices rose 20% last year. Those that brought in the past couple of years would be breaking even. Not to mention negative equity doesn’t matter for the vast majority that don’t need to sell their home.

Agreed, it's used as an excuse. The paradox is that the bigger the bubble gets, the less efficient the economy so the fear becomes justified. When interest rates are forced up and the bubble does pop, who will have the means to swoop in and buy up all the cheap houses? Mom and pop investors?

I think the figures you are quoting are based on the extent to which price drops drive owners into negative equity, creating problems for banks.

I don't think it takes into account the impact rising interest rates would have on servicing high levels of debt. I've read many times that "they" can't let rates rise. Well, I don't have that much faith in their control at this level of madness.

Interest free deposit loan for FHB, 20% in main centers 30% for the regions. Go crazy.

My kids will be keen on that. Can they buy million dollar homes with the free deposit money?

Once you've wasted years of your life chasing the moving goalposts for the deposit you can then spend the rest of it attempting to pay down the principal as interest rates rise.

Cradle to grave housing debt servitude.

Aroha. Let's keep moving.

Totally spot on!

We must press this government the same way banks did last years, which is what got us here.

Housing affordability improved slightly for first home buyers in many parts of the country in January, but the outlook remains grim for those on average wages.

AND WHAT PERCENTAGE US ON AVERAGE WAGE.

To say affordibality improved for FHB is making fun of them.

When median house price has increased by appox 20% any advantage of fallen interest is setoff instead now have minimum 20% more debt.

If no action to be taken to control the ponzi where house prices have been rising on a weekly basis - is gine but atleast do not make fun of FHB who are struggling.

Is this somekind of lobbying to get government of the pressure so do not act as it is government wanted an issue to deflate from housing crisis and now have got one in another lockdiwn.

Real Shame

Yes, need to look behind the numbers.

Giving median wage of 24 to 29 year olds must be making the assumption that they have been saving at the same amount for the years needed to save a deposit, which we know cannot happen.

And that both are working, no kids etc. etc. and will continue to do so.

While these stats. may be correct academically to make comparisons between regions, I don't think it has much real-life practicality as to what is feasible for many people in this Covid environment.

Well maybe an emergency rate cut is in order next week..

Yes, that will NOT help. As harmful as the FHB grants Jacinda is hinting while ignoring the advice she's got.

https://www.newshub.co.nz/home/politics/2021/02/jacinda-ardern-forced-t…

Depressingly familiar articles trotted out about twice weekly. As soon as the borders open there'll be a surge of people heading to Oz and we'll be opening up the immigration tap to hold up prices here.

Hold prices up but keep wages down*

Don't worry about housing. People won't have jobs soon as a number of businesses will struggle with these lockdowns. There will be a lot of poor people. Luck has run out of this incompetent but kind govt. I have a feeling this outbreak will really hurt us economically.

House prices will crash.

Not so chessmaster!

The gov has a good solution to your problems. They just make more money and all the problems go away.

Only a rockstar economy could do what we are able to do in nz!

Fully agreed, my advise is the same.. for any variants of Asian ethnicities in NZ. Buy all those properties, rent it out to govt. sponsored/preferential ethnicity doctors, nurses.

They're a very good tenant! - stable income as per guaranteed by govt, avoid the one with fully grant $ but less production/brain works activity, and once the capital is large enough.

If you wish so desire to contribute? the best place is OZ for more meaningful societal contribution by own self skills, training, passion etc. Just leave that land of the long dark drop.

I would advocate vesting ALL land in New Zealand with the Crown. This would knock land speculation on the head. I would probably exempt farms run by their owners. Farmers deserve special privileges because our standard of living depends on them.

The Chinese ruling party could help us bring this about.

I appreciate you're trying to be funny. It's not. Can you point to a definition of communism that is factual, and then match it up to any political party in New Zealand?

NZ is doing the same as all the other countries. Printing money and watching asset prices increasing. We are not different. Our lockdowns have been effective, that is our only point of difference. Central bankers around the world are playing the same debt game - debt is the only game in town. At some point it will break and when it does we will not be immune and those with massive debt levels and falling/no income will be hardest hit. Better to think bigger picture ie worldwide rather than just limit your knowledge to NZ. Once people realise that policy today is to get you into debt at 18 until the day you die.

I was at an auction for a 50s 3brm house in original condition in forrest hill the other day. Would have been a great first home for a young couple with a few kids.

Went for 1.5mil to a lovely chinese gentleman over the phone. A bit of a bidding war with another lovely chinese lady.

Truwy a great time to be a property owner!

I went there too. a bit of overpay still an excellent buy.

With some renovation, the property could sell at over 2M easy.

Would have been around the corner from my old place built in the 70s, brought for less than 50k on a single junior clerk wage in the 80s now sold for over a mil to overseas owners. But when they come stay in NZ there are mandarin only child care centers in the area now so the area is still family focused. It is just more the only young families affording to live there are those coming from outside of NZ from a wide set of countries that pay higher. The retirement homes in the area are still growing and the mandarin speaking classes are quite handy if you are looking to pick up a new language. Strange though that spot in Forest Hill that used to have horses and could fit more than 20 homes is still left untouched by the owners. Forest Hill was a great place for the kids to grow but none of them can afford to live in the country anymore.

ssssh. immigration has no effect on rents or house prices.

Was it likely purchased for the land?

Old houses can also need a lot of money spending on them, but many will just be bulldozered and multi dwellings built on them.

607m2 section with moderate slope. (In wellington it would be considered dead flat) suburban zoning so can't subdivide.

Good summary to read, as how the govt try to shift the real technical issue and just enjoy the populist stand:

https://www.stuff.co.nz/national/politics/opinion/300240050/reserve-ban…

2018 employment shifted to RBNZ, 2021 housing shifted to RBNZ (as I predicted correctly), next will be as per 2020 hinted by Mr.Orr & JA about the climate emergency. The recent report of largest 2020 insurance claim is the background catalyst. Lab/JA will sound the romance of carbon neutral, climate urgency (sway away from economic/pandemic) and coastal erosion insurance cost.

The way the intended final puzzle to works is: More QE for the Insurance business, expected to kick in around 2023-25, NZ provide a sounds good 'frame work of governance' then opening border targeting any easy $ from Asia to buffer in/park for awhile.. to maintain the ponzi numbers. NZ below average collective IQ stands just cannot be more obvious than their bottom line wealth expectation from F.I.RE economic mind set.

Great article.

The carbon neutral stance will start to fizz out in about 10 to 15 years when people start to realize:

1. That it is unachievable without significant lifestyle changes that will mainly affect the middle class and poor.

2. That countries whose governments aren't 'woke' like china, india, african nations, etc. Don't really care about the whole climate change ideology and just want to catch up to devaloped countries at any cost.

I can see the backlash becoming a torrent as the various effects of the paris accords begin to roll out. No more gas cooking will be the least of our concerns.

Chinaman 1 good comment. I would add:

Will the populations of these anti-woke countries you mention still be scrambling to increase their standard of living at any cost as the temperature rises to the level where trees and other flora begin to emit carbon dioxide instead of oxygen: not all that far away by all recent accounts?

As Benny Hill would say: "Not a lot of people know that".

In short yes.

Once again, we need a total BAN on housing investment. It is just something we cannot afford as a country and it got us way, way to far into a hole already. Happy to see some mainstream media has started supporting the measure, about time.

https://www.stuff.co.nz/business/opinion-analysis/300233796/investor-ba…

This can be introduced for a period of time and monitor individual regions until affordability goes back to reasonable levels of 3-5 times average household incomes in the area.

A market intervention to try and fix the unexpected impact of the previous interventions.

Would be interesting to see how the black market would adapt - I guess the obvious are investors buying through relatives and paying strangers to use their names for further purchases. A market emerges for people to sell their right to buy a house (may as well if they can't afford one). Measure and countermeasure. But money generally gets what it wants.

The lack of intervention on the right side of the scale is what got us here, not intervention itself. The rules of free market did not apply the moment ew allowed to tilt the field on favor of those with higher equity.

https://www.benjerry.com/files/live/sites/systemsite/files/whats-new/51…

{kind=link}

Sure some may try to get around the rules, this always happens, even right now as we speak investors are avoiding LVR restrictions the way you say. Bottomline is that t would be much harder than it is now which is free lunch for all.

So where do all the retirees with cash who need income invest their money?

Total ban on housing investment? How ridiculous just so a few FHBs can have the market all to themselves. How many more draconian regulations can we come up with why we are at it

Prediction

Reserve Bank will offer digital accounts by September 2021. Orr will cut rates to negative in April. He will order window guidance and instruct banks to lend lend for housing only. Blows up a massive bubble of biblical proportion. Eventually with more lockdowns businesses will collapse as will the economy and your bank.

The next day you will get told to download a rbnz app on your mobile. The 117k you had with ASB that you can't access will appear in your new central bank account. All of the foreclosures and properties left with the banks will be transfered to the govt to house the population... Because you will own nothing and be happy right?

Even the RBNZ knows better than doing this, they are aware of the civil unrest and danger to the country this would pose.

Fun prediction - thanks. I certainly would not be surprised by a CBDC being introduced in a rush as the Old Switcheroo.

I've put a copy on my calendar for 1/9/21 and will post a reminder so we can check back on how close you came.

If you nail this you can have your own youtube channel, fer sure.

I have also read similar examples of how this situation could play out. It would be sudden and totally unexpected. Reading the “it couldn’t happen here” type comments makes it entirely plausible to me.

I agree about the digital currency at the RBNZ idea. I wonder if John Key and ANZ have figured this out yet. I was talking to someone about this idea the other day, they suggested that there is too much other work that a bank does that the RBNZ wouldn't be able to take onboard. Thoughts?

Yeah, there is a bunch of bread and butter loan application processing work the RB won't do. Could be contracted, including to the existing banks.

1986

Central banks are coordinating a takeover of the banking system. Germany had 2700 banks in 2011 it now has 1700 for example. They have the best banking system. The fed and it's global counterparts will first drive small banks out of business then have a few big boys and then crush them. One bank left.. The soviet union only had one bank. Once the regulator offers a product identical to the retailers then it only ends one way..

This action would likely drive any sane people straight into the arms of crypto-currency. The choice between Big Brother CBs, or a decentralised global free market is a no brainer. Any attempt at draconian regulation would go the way of Nigeria where the Vice President has recently capitulated https://cryptopotato.com/vice-president-of-nigeria-tips-cryptocurrencie…

I have heard this prediction a few times before on youtube. It is an interesting idea. But won't they just print money and give helicopter payments before anything like that happens? But financial crisis's happen, and it feels like we could be at the beginning of one.

But I think this is one reason many people seem to be taking their cash out of the bank and buying a property, to actually have something physical as an asset incase the worst happens.

ThEy ShOuLd JuSt tRy cUtTiNg BaCk oN aVoCaDo AnD tOaSt.

They would need over a hundred years and a lot of plague in the world for that to work though.

Saving for a deposit: what % has any research shown actually save the deposit themselves?

8.5 years to save up eh , in Auckland

Average marriage lasts about 9 years, and co-habiting a lot less than that.

parents contribution needs research and parents with that sort of money to hand over, loan or not, do not tend to be parents of average earners.

Just as the people streaming out of Auckland on SH1 past our place last night to their holiday "Bach" are not average either.

Thx Greg. Another good article. If it take 8.4 years to save the deposit in Auckland wouldn't that mean (according to many) house prices would have doubled after 8.4 years so you would be no further ahead and still need another 150K to get the deposit?

Yup. The article says that the table shows what people would need to save, but more accurately it's what they would have needed to save had they started years ago.

I am not in a couple. I started saving 40% of my take home over 5 years ago. I then arranged a work transfer to the cheapest area I can still do my job. In the five years since I started seriously saving for a house, house prices doubled in that area.

A life in debt is exactly what the central bankers are aiming for. Once people wake up to this reality the fun will really start. It’s the same central bank debt expansion policy the world over. To keep the financial system running needs more and more debt. As asset prices go up more and more debt needs to be taken on by countries and individuals. You are the latest in the debt ponzi scheme and your generation will be forced to take on eye watering debt in the hope that it will be inflated away like it was for your parents and grandparents. Need to upgrade your car - here’s more debt. Renovations needed - here’s more debt.

There is little chance of saving up for these things from your salary as too much is being used to pay your debts.

Enter trading and crypto..... these are being used by Gen X and Gen Y in order to grow their money quickly. Self taught from social networks. Were your parents and grandparents forced to take on this high risk savings strategy at such a young age? No, they got 15% in their savings account at the bank. Times are changing and faster than people realise. Be self educated and realise what’s happening. We are probably coming to the end of a massive debt bubble. More debt = Less options when it does finally blow.

If you are single or already have kids and don't have Mum and Dad to help and are saving for a house you are totally screwed unless you are in the top 5% of earners.

Sadly I have to agree. I feel as though it won't be long before we see all these young people (with no sense of hope for their futures) marching in the streets.

Do you hear the people sing?

Singing the song of angry men?

It is the music of the people

Who will not be slaves again!

You don’t need mum and dad at all.

Someone with good salary should easily be able to have accumulated 150k Kiwisaver with 10 years of compounding in an investment fund. With a partner you have a 30% deposit on a decent house in this market.

I see people with 2 cars each, a motorcycle and 3 different bbqs etc. still renting and complaining that they haven’t saved enough for the deposit.

I see a troll with comments lacking in fact or reality

Good for you. With that attitude you will probably never see a property either

you're hilarious

As I predicted several times (and ridiculed by someone who doesn't visit these fair pages anymore), Auckland CBD rents are dropping. Availability is high for this time of year, given lack of international students. https://i.stuff.co.nz/life-style/homed/renting/124366968/opportunity-be…

You were right.

It's nothing that open flood gates won't eventually fix.

Fritz.. I am guessing even New Plymouth will be minority NZ born by about 2050. I will likely be not mobile enough (at best) to enjoy the diverse, multi-cultural environment that will exist. But my kids may not be able to find a job or afford rent or a mortgage (nothing to do with the foreigners here. Foreigners do not take jobs kiwis can do or need anywhere to live) so at least I will have people to live with me and look after me in my old age. I will just sit in front of the TV watching reruns of Married with Children and Alf Garnett till the end of days.

That’s hardly a revelation and only temporary of course

This is the type of distraction that everyone was commenting yesterday that government was waiting to deflect the attention from rising house price....BUT.....for how long ?

So just cut back by 20 odd servings of avo on toast a week?

Whenever GR finally gets round to getting a deposit insurance scheme up and running he's going to have to up the cap a bit if he wants to give these stranded FHBs assurance that their loan deposits don't suddenly shrink on them if an OBR event unfolds.

In any OBR event, the first people to feel the heat will be those who have a mortgage with the failing bank.

Those debts will be the first in line to be called in. Wouldn't you call in money owing to you if you had creditors knocking at your door? Keeping the funds you have already borrowed (depositors funds) does nothing to give you the liquidity to repay debt, because you've already re-lent them out!

"Look Hamish. I know you have 25 years left to run on your $1 million mortgage with us, but if you read the fine print you'll see that we can demand you repay it under notice. So. You have 30 days to repay your loan"

What will you do?

Refinance?

With whom? And at what % rate.? Or will you have to sell-up to make the payment?

By the time any OBR gets to depositors every other line of credit will have been called in.

Under those circumstance, any asset financed by debt will be worth what?

(That's why the most likely course of action will be a forced merger with another bank - think Bear Stearns; Merrill Lynch; even BNZ to NAB here etc.)

The bail in happens straight away so the bank can open its doors in the morning? Depositors would take a haircut.

Easier for for first home buyers! That's a joke right? Ask them how easy it is in not long to come when interest rates are on they way up, I absolutely feel for the people today that are having to borrow extreme amounts in these inflated markets.

Interest rates could double and we would be then paying about market rent for our place.

Every first world city has expensive housing and as much as you wish for it day in day out that isn’t going to change.

Nobody will take a haircut... The banks will be replaced by one bank!

Poor FHB and average Kiwi are hoping that government will take step to help them but in reality are out to screw them royally.

"Housing affordability" Improved slightly for first home buyers" is an absolute lie if you are comparing the same house this year to last year and what the banks are willing to loan out.

Example say this time last year the bank was willing to lend you $800,000 for a $1,000,000 house.

That house now costs $1,200,000. The deposit requirement has increased from $200,000 to $240,000 but also the required loan has increased from $800,000 to $960,000. The bank isn't going to increase the loan amount because it is tied to your income (which likely hasn't changed) therefore you can no longer afford that house.

"The bank isn't going to increase the loan amount because it is tied to your income (which likely hasn't changed) therefore you can no longer afford that house."

Only if serviceability was your limiting factor. For many FHB it's the deposit that's the problem, not the servicing.

2020 Lower quartile price $688,000 less 20% deposit of $137,600 = Mortgage $550,400. 1 year fixed Interest rate last year 3.39% = fortnightly payments of $1,125

2021 Lower quartile price $780,000 less 20% deposit of $156,000= Mortgage $624,000. 1 year fixed Interest rate last year 2.29% = fortnightly payments of $1,106

So you would have had to have saved an extra $18,400 for a deposit however your fortnightly payments have gone done by $19 a fortnight.

However if you look at the median weekly after tax pay for couples which is $1,764. this would roughly put them at an annual salary of $60,000 each. So combined income before tax would be $120,000. Banks will not lend you much more than 5 x your pre tax income. In this case they could therefore borrow $120,000 x 5 = $600,000. Mortgage now required is $624,000.

I would still say serviceability is now becoming a limiting factor for FHB in Auckland.

$1764.84 is the stated median weekly after-tax pay for couples 25-29 in Auckland. It's unlikely that it's also the median after-tax pay of FHB in that age group since unemployed, underemployed and low income couples are unlikely to be the ones who are buying their first home. Therefore median income of actual FHB in that age group would be higher than the median of all couples within that age group. How much higher, who knows... let's estimate 10% higher. Therefore at 5x pre-tax income those couples could afford home loans of around $700K which means that it's the deposit rather than the loan size that's the main limiting factor.

In reality many FHB won't be in the 25-29 age group so would have higher incomes. But that's another topic.

So basically you are saying it is only just affordable if you are one of the lucky ones earning higher than the median income of your age bracket?

To your last point are you suggesting FHB are actually older say in the 30-33 range, the age where you typically start to have children? and drop to one income? Banks love that.

Well the banks' servicing tests are at interest rates much higher than what you'll be offered. So as long as the FHB was honest on their application, then if they were approved there will be a decent amount of leeway to handle a change of income. Just make sure to apply and be approved before having kids else it will be much harder. Also normally one partner earns more than the other partner so just be sensible in keeping the higher and/or more stable earner working. Loss of income from the non-working partner will be partially offset by WFF credits.

Finally, it mostly takes hard work and smarts, not luck to earn a high income. Though "above median" is not necessarily high.

To your last point yes I'm aware of that, but what an inspirational for the next generation. Hey kid work hard, get smart and one day when you're near your thirties you may be able to afford one of the shitest homes in the worst location of your city. O by the way you will need to have a partner earning a decent salary too!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.