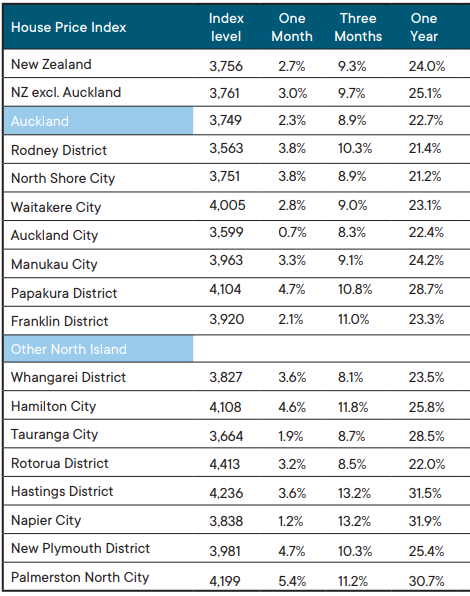

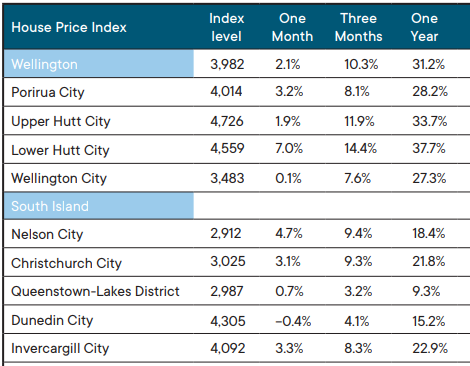

Annual house price growth ranged from 9.3% to 37.7% in the country's main urban districts in the 12 months to March, according to the Real Estate Institute of New Zealand's House Price Index.

The Index, which was developed in conjunction with the Reserve Bank, adjusts for differences in the mix of properties sold each month, giving a better indication of overall market price movements than either median or average prices.

The greatest annual price growth occurred in the Wellington and Hawke's Bay regions, with prices rising by between 27.3% in Wellington City, and an astounding 37.7% in Lower Hutt over the 12 months to March.

Prices also increased by more than 30% in Napier and Hastings.

Price growth was more restrained in Auckland where there was an overall increase of 22.7% throughout the region, and in Christchurch which had annual price growth of 21.8%.

Perhaps unsurprisingly, the lowest prices growth occurred in Queenstown-Lakes at 9.3%, which was the only major urban district to record annual price growth in single digits (see the table below for the full results).

However in a normal year, even Queenstown's price growth of just under 10% would have been considered substantial. Annual growth of more than 20% and even 30% is gob smacking.

With the migration taps turned off over the last year and the supply of new homes continuing to increase, the underlying reason for the eye-watering price growth must be laid squarely at the feet of the Reserve Bank and its decision to cut interest rates to record lows and remove loan-to-valuation ratio (LVR) restrictions on new mortgage lending last year. LVR restrictions have since been reinstated.

While this may have had a stimulatory effect on the economy, and in the short term helped to ward off a possible pandemic lockdown-induced recession, it has also created serious longer term problems such as reducing housing affordability for first home buyers in particular, and in the growth of the country's mortgage debt.

The comment stream on this story is now closed.

REINZ House Price Index - March 2021

97 Comments

Not changing the LVRs would only have slowed the surge because people make buying decisions on what their money in and out each week looks like. It suddenly became drastically cheaper to buy than to rent and everybody acted accordingly.

Anyway, surge over now. Call your local agents and ask how much inquiry they are getting from out of town buyers. If they say loads and aren't pushing new builds I have a bridge to sell you.

"It suddenly became drastically cheaper to buy than to rent" - Got any numbers to support that claim?

Sure, at 2.2% interest rates the cost to rent is more expensive at around 2.75% of capital value. This approach considers principal savings rather than a cost but that is the correct approach in appraising a cost relative to a balance sheet.

Yeah... the best rate you can get at the moment is 2.29% for 1 year, at <80% LVR which many first home buyers won't have in the current market. At a DTI of 5, 80% LVR, Westpac would give me 3% at best.

And what about costs such as rates and insurance? A few thousand a year makes a big difference to a couple who makes, say, 150k per year combined.

CJ

Friend here in HB just sold his home to a FHB. We thought the price obscene (here as the data shows HB properties up 31% YOY) until as the FHB said, the mortgage including principal was cheaper than rent and although added costs such as rates and insurance he was still better off financially buying than renting.

Week to week I get it. But man, owning the place can be tough when a $50k new roof bill comes through. Good thing they bought new though so hopefully no big maintenance costs for some time.

If you can afford a house big enough to have a $50k roof ( $50k roof would be about 300m²), a $50k bill shouldn't worry you.

That’s it exactly. So these “obscene” prices still mean that your weekly costs are less than renting.

As I’ve said before it doesn’t really matter what the capital value is doing if you are an OO what matters is that your weekly costs are better than they would be renting the same property.

And principal repayments were rightly pointed out as effectively savings.

"At a DTI of 5, 80% LVR, Westpac would give me 3% at best"

Try another bank. 2.29% on DTI 5 LVR 80% is possible if your income is viewed as good quality and stable.

rates and insurance is the reason the required yield is higher than the stated interest rate.

Thats not the case, 2.29% may be the best carded rate but you can get 2.2% easily enough.

I suspect you are generally right but for some reason the numbers never stacked up for me - always looked like I would be even more skint each month paying a mortgage than rent.

But the main reason I've stayed out of RE is the interest rate risk. I guess I'm just a pessimist and should have buried my snout in the "cheap finance...for now" trough with everyone else.

Agreed, it's funny to see that they don't include many years mortgage commitment and changing of interest rate when they make the claim. Rents can go up and down by market value. Same as mortgage depends on the interest rate. The difference is that renting gives you more freedom, no commitment. But for paying off mortgage, you'll be tied for long term and have no control of how much you need to pay for your mortgage. The control is on RBNZ and banks' side.

The interest rate risk applies to everyone in this country. If rates go up it is because of inflation and as such everything is up including rents.

Far better to be owning.

Invariably these claims are backed up by calculating just the interest portion of a mortgage on a property, and comparing that to the costs to rent, but Ignoring things like rates, insurance, maintenance.

Bottom line, either way it is currently very, very tough being either a FHB or a renter. I do not envy either FHB or renters - both house prices and rents are obscene in terms of incomes.

False, those costs are the reason the yield is stated as needing to be higher than the interest cost.

Not sure why its hard to grasp, even if your mortgage is slightly higher than the rent you still way better off. The mortgage is paying down an asset and paying rent is like flushing the money down the toilet.

I would rather rent, it gives me financial freedom. Flush away.

It may give you financial freedom in the short term but you will be a financial prisoner in the long term.

Our mortgage/rates/insurance was slightly higher than rent 4 years ago. There's a property currently for rent that's the identical footprint to ours, 50% higher than our M/R/I.

Nzdan

Yes, like most others as a home owner, a definite winner over time.

In the short term, just as rents can go up so too can mortgage interest rates. However, over the longer term, a renter walks away with nothing whereas a property owner will most likely walk away with increased equity.

I know which I would prefer and that isn't even considering the advantage of intrinsic value and security for one's family of home ownership.

Would love to know who is paying these eye watering prices.

I’m in Wellington, I re ran my numbers, and without the interest deductibility my numbers have become cash flow negative - for future purchases. So I’m guessing investors are only going for capital gains now, at least in Wellington.

Investors out there - are you guys still buying in Wellington?

Yes. Strategy is to add value, remodel, add dwellings. Same as always. I bought a 2-flat property in Mt Cook in November... peak froth. I'm completely doing it up, adding 2 bedrooms etc. It'll be fine.

What sort of yield do you expect to generate once completed?

6.3 gross, 5.4 net

I have a property in Wellington (our first home, was never intended for investment purposes) but it has a minimal mortgage so is cashflow positive. Even so I have no plans to buy more property there, if anything I'd be more likely to subdivide and build if the council would deem me worthy of their spit.

As I've said in the past, I find the value being placed on the property quite embarrassing and I can't sell in case work ever asks me to move back, because while I can afford to buy there now I might not be able to if the market insanity continues much longer. And I'm a high earner.

ETA: The excess income from that property is largely being put back into it for continuous improvements such as double glazing (old villa) and oversized heat pumps. We always keep in mind that the tenant is also a human being deserving of a nice home.

Glad to hear it.

Just got a newsletter (email) from an Auckland agent saying (to paraphrase):

Investment has slowed a bit - investors considering options. Home buyer market is still going very strong, especially as available listings is reducing heading into winter. A more settled market, which will give buyers and sellers an opportunity to review their options.

So could be further volume drops on the way, and therefore the prices achieved not mattering so much with most players on the sidelines through winter.

Well paid WETA workshop/film industry, Govt policy wonks, and developers looking for up and coming high density build areas. The plan is herd the sheeple into little apartments with no car space (for most FHB from now) on so the oligarchs can indulge in large swathes of NZ forest and beaches in relative peace

I work at Weta, and trust me it's not all of us buying them up. Some buy for sure, but most of us are priced out. There's been internal rumblings about it already. Work is intermittent and we've had pay freezes. Some of are quietly planning our exits out of here. New hires are remaining remote overseas. I'm also scratching my head as to who's buying.

Your average policy wonk is priced out too. It's a curious situation in the capital isn't it?

It really is. I don't know what's next. One way or another, the future doesn't look bright for Wellington.

But as a couple that's >$200K combined income so $1.25M houses are within range.

Yep senior wonks should be earning circa 100k, or a nudge over

Yup just dont have any kids and sweet

Somewhat depressingly, $1.25M wouldn't be enough to buy our small 3-bed, 2 bath villa within walking distance of the CBD. Not too many years ago it was a prime faceless public servant buying suburb, now it's a prime faceless public servant rental suburb.

Well the problem is what you can get for your money and how long until you can pay the whole mortgage.

There's a large commercial building been converted into apartments by Wgtn city council specifically for public servants and highly paid middle income earners priced out needing to rent in Wgtn. Already 80% occupancy and fit out not even finished. 1 and 2 beds were more popular than 3 beds. City council couldn't be seen via property rates to subsidize below market rent although it's slightly below market. The building owner gets a guaranteed 15 year lease so the council effectively act as a property manager.

They did this because there are so many people on good incomes unable to get rentals let alone buy in Wgtn. Can't see much of a future for Wgtn at that rate but they still think there'll be another 80,000 people or so moving there in the next few decades.

Yes, also bought in Wgtn in Dec, building 2 more dwellings, all to be sold thereby adding to supply.

I am still very optimistic about house price in population centers because the median price to median household income ratio still fall far behind 20.

Why have the clowns that signed off the removal of LVR's not been fired.

Orr, Bascand, Hawkesby and especially Yuong Ha.

Mind bending incompetence. Zero accountability.

Yes, I was calling for this last year, stupendous incompetence, putting the entire financial system at risk, directly against their mandate.

Shocker and with zero accountability, they still claim it was the right thing to do!

Globalists and have to do right by the oligarchs who've bought up vast swathes of prime real estate in recent years - have to be fair!

A bit of a contrasting picture between the house about to fall off into a cliff and the photo from yesterday's REINZ article, showing the house taking off into the stratosphere

Don't worry, it will be fine. The rocket engines are just about to ignite.

Comments this morning March was the peak - FOMO turning to FOOP

https://www.newshub.co.nz/home/money/2021/04/growing-hesitancy-in-housi…

FOMO is baked in. Are people really going to keep watching every train whizz past when they see the charts zooming up for last 40 years with only a tiny dip in 2010

Yes they (buyer) - especially if its the new Hamilton to Auckland passenger service.

Its just industry noise to try stop the ban on interest only and DTIs

Yvil

Rather than take-off, I saw yesterday's picture being a gentle controlled touch down - i.e. coming back to earth.

Maybe my perception is strongly influenced by my view regarding the outlook for the housing market. :)

"While this may have had a stimulatory effect on the economy" on parts of the economy primarily housing, and very limited in other areas, but the end result is one that is extremely unbalanced. Inflation has been rampant in the housing market for 15 years or more with no Government taking any kind of action to realistically rein it in, and now the effects of the economic impacts of COVID are starting to tick up inflation in other parts of the economy. But the RBNZ is still in denial as past reluctance to take action comes back to bite it, and the hold the OCR at record lows. Too afraid of the consequences now if they shift the OCR up, despite telling us in 2019 that the banking sector is secure.

I guess we can all breathe a sigh of relief that they didn't go negative. The power that would give the banks is frightening ...

It was gobsmackingly stupid of them to lower rates for the past 5 or so years, often for spurious reasons. I mean, look at this graph: https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/what-is-….

From 2015 to 2020 was boom time, the OCR should have remained flat if nothing else, instead it dropped from 3.5% to 1%, basically for no reason (oh they will claim it was to try and push inflation, but we all know how that worked out... it had no effect). At the same time the drop in 2009 should have been either temporary or not as big, instead they cut in half almost overnight. 4-5% likely would have been plenty "stimulatory" from the 8-9% it was previously, instead they went overboard.

RBNZ is just following what everyone else does. A series of inept governments have made the situation worse and in many ways forced the RBNZs hands into trying to add stimulus, as is this one.

It's largely a currency war that no one is allowed to talk about. I also don't like where rates are but when there are few other reasons for such low rates I conclude that it's about keeping the currency low. I'm beginning to think that we don't really have an independent monetary policy since central banks are following the US to ensure their currencies don't appreciate. This is a large part of why bitcoin is booming.

Good comment, totally agree.

That does not capture the full picture, although I agree it is a factor. If it was just about keep the currency low they could have dropped rates, but kept in place (or ramped up) banks capital requirements and used macro prudential rules to curtail excess credit growth. They did neither. Instead when covid hit, they threw both out the window in fear of the housing bubble unwinding.

Why? In part because RBNZ's mandate was changed to factor in "maximum sustainable employment". This change was a far bigger risk to the RBNZ's independence than the weak request to consider house prices. It aligns a government's incentive to stave off recessions with cheap credit.

And be prepared to hold your breath again.

RBNZ won't make arrangements for negative interest rates if they don't intend to use it.

It would be the opportunity of a lifetime to be the first to witness it in NZ history- our forebears don't even have the opportunity to think of it.

Can't wait for the next event, what a privilege it'll be!

That's how I feel - nothing would surprise me now.

"the underlying reason for the eye-watering price growth must be laid squarely at the feet of the Reserve Bank and its decision to cut interest rates to record lows"

Absolutely Greg, that is the root cause, all other reasons given are just "noise". Instead of tinkering around the fringes with a multitude of new rules, the RBNZ could immediately stop the the whole house price increase with one simple statement:

"Given the unexpected resilience of the NZ economy, we will return the OCR to it's pre-Covid level of 1% from the 7th of May"

That's not the case, it is certainly a supply imbalance. Once you have a supply imbalance then the rest is pure mathematics and interest rates will drive the show. But I assure you if we build more houses, in places people want to live, than people can buy, prices will fall no matter the rate of interest. The problem is supply. Given the supply, the cause of prices rising is interest rates. But the government was explicitly warned about this twice and did nothing. #pay-as-you-go capital gains tax coupled to huge infrastructure spending.

100% correct.

Extraordinary price growth is a symptom of monetary policy, but is fundamentally caused by inelastic supply.

Yes. For someone to borrow hundreds of thousands of dollars at low interest rates, there needs to be demand. Will investors pile into property if there is nobody to rent to, and prices are static? Even if mortgage interest rates were 0.5%?

I am tired to hear the only problem is supply, there is not a supply problem, we are building at a rate of +1000 homes per month in Auckland alone where we also have around 40K empty homes (look for the data, I have shared it many times). The problem is that since private builders buy already overpriced land they build whatever they think will bring them the highest profits which are usually standalone 3-5 bedroom homes, what is causing an OVERSUPPLY of unaffordable housing and poor land development. This highlights the necessity of public-private collaboration to build the homes people NEED, which we can do and can be done well.

"the underlying reason for the eye-watering price growth must be laid squarely at the feet of the Reserve Bank and its decision to cut interest rates to record lows"

Agree that may be interest rate cut was required but WHAT WAS THE NEED TO REMOVE LVR as purpose at that time was to support the existing buyer from default and not add more debt in uncertain situation BESIDES even if you did lower interest rate WHERE YOU NOT AWARE THAT WILL LEAD TO BUBBLE and even if you knew and had to THAN WHY NOT STOPPED INTEREST ONLY LOAN IMMEDIATELY TO NEW PURCHASES TO STOP SPECULATIVE ACTIVITY TO AVOID UNDESIRED / UNWANTED CONSEQUENCE OF LOW INTEREST RATE or IS IT ON PURPOSE AS MAY BE THAT WAS DESIRED AND WANTED CONSEQUENCE - Congrats. Is the mission accomplished now with appox 30% to 50% growth in a year OR are you stil not happy and have another secret milestone that you are hoping to achieve.

Throw your ego aside and for once look what you and Robertson has done to ordinary kiwi and FHB. Social unrest and it's sole responsibility is with you and more as did everything knowingly under the garb of panademic to satisfy some sort of deep dark fantasy.

an astounding 37.7% in Lower Hutt

Glad to see the data I collected being validated - and the rent price rises (by my account) averaged up by 13% in the six months to end December. Worst rises were in the lowest end of the rental market - up in asking prices (versus bonds lodged) by 24% in that same period.

#rentcontrolsnow

#reducesupplyofrentalsnow

Your mentioning of rent freezing was the thing that prompted to lift all of mine to market levels!

Didn't want to be frozen $80 or more under market.

The bond data is all the new tenancies. Often they are new as a new investor has just paid a stupid amount for it, the banks said we will only lend this stupid amount on a property that brings in X amount of rent, they get an rent appraisal, whispering the amount needed for the deal, and funnily enough it comes in at that, and then they try to rent for that amount - some well presented get it, I know of several that went out at rent asking of $150 higher than previous LL was asking, then had to drop it $20 or so to get tenants.

So its these newbie investors pushing market rents up.

And fear of things like rent freezes or other random unconsulted labour policy that cause old-time smaller property investors to rise all 5 or so of there's up to market.

(the big ballers with 20+ already keep right on the heels of market rent via active and good property managers).

Anyway. That's how it is. Perhaps consult investors who supply 80% of all rentals accommodation in NZ instead of treating the like criminals in which case fear of what's crazy labour going to hit us with next will mean market rents all round!

In the same post, you

- blame the OP for you raising your rents

- blame new investors for you raising your rents

- declare it's just "how it is"

Do you ever take responsibility for your own actions?

"Someone on the internet suggested we make things fairer, so I decided to punish them and take more for myself. Look what they made me do. Next time they should consult with me."

Very accurate. Their reasoning often goes like this...

A Narcissist's Prayer:

That didn't happen.

And if it did, it wasn't that bad.

And if it was, that's not a big deal.

And if it is, that's not my fault.

And if it was, I didn't mean it.

And if I did...

You deserved it.

Rent control is necessary for many reasons but two that immediately come to mind are:

1) Discourage housing investment to shift capital to more productive areas of the economy.

2) Make more income available to other expenses increasing velocity of money from which business will benefit.

Still Mr Orr and Mr Robertson are waiting before taking action on interest only loan and DTI.

Script for Announcement in May has already been written and locked ( as biased and vested, end result is decided first and than find excuse and reason to support and in this case REASON AND EXCUSE WILL BE WAIING AND WATCHING.

Watching WHAT.....Waiting FOR WHAT............

Want to target Speculators - Target interest only loan. Full Stop as by targeting IO Loan it is mostly and if only speculators will be affected.

Have a look at the live Central B&T auction today, taking place right now. Looks like more than 70% passed in. Some with no bids. Finally the frenzy is easing. Might even has halted. https://www.barfoot.co.nz/auctions-live/sessions Is anyone attending today? Are there actually people in the room? The camera only shows the auctioneer.

Yeah it's crazy, crickets for days...

It does look grim. Looks like only 2 out of 22 sold so far at the city 10am session.

LooooooooL. Hopefully just a blip.

Passing them in left right and centre at the moment!

Why only blame the Reserve Bank for "the eye-watering price growth?" Surely it is the government that sets Reserve Bank Policy?

The Reserve Bank is required to; maintain financial stability of the banking system; keep CPI between 1-3% & maximise full-employment. Unfortunately CPI doesn't include asset price inflation such as housing prices.

Focusing on full-employment has led to an expansionary monetary policy resulting in the lowest interest rates ever & the largest debt ever. This strategy has no consequences while interest rates are low but will be hard on the economy when interest rates increase.

NZ is now having to negotiate the start of "stagflation" as the relatively small productive base in NZ will struggle to grow GDP.

Property taxes, interest expenses & increasing social welfare costs will weigh heavily on the economy. NZ is already experiencing inflation pressures from a shortage of skilled labour & materials.

The government needs to take responsibility for; not changing Reserve Bank policies , discouraging rental property investment & the resulting increase in rents as well as the unprecedented growth in social welfare costs.

Median price in Wellington fell last month

As a property investor the New Zealand economy is really fascinating to me. I lived through Ireland's 'Celtic Tiger' but even that was not like the situation in New Zealand because that boom was fueled by Irelands rapid economic development with per capita income (Ireland went from one of Western Europes poorest countries to one of its wealthiest in less than 30 years), disposable income and productivity rising rapidly. Also it very much became a building boom with supply eventually surpassing demand.

In New Zealand there isn't really a broad base of economic growth to support prices and nor is this really a building boom. It appears entirely a bubble of our own making supported by a range of measures from stringent zoning that economically prohibits low-cost mass development of affordable housing to very favourable tax treatments.

Perhaps even stranger is that publicly governments admonish this while essentially maintaining the status quo through sucessive governments of all varieties.

Yes Kiwis can also fight and make toilet paper a premium product specially if have support of Prime Minister and Reserve Bank Governor.

'appears entirely a bubble of our own making supported by a range of measures from stringent zoning that economically prohibits low-cost mass development of affordable housing'

A very succinct summary.

As you will know by my comments on almost any thread, our land zoning policy is the underlying clause of this. Everything else is just a reaction to this.

Think you've got the nail on the head. It does seem predominantly driven by land prices in residential zones, building a house is only marginally more expensive in New Zealand. It'll be interesting to see if the RMA refresh effectively opens up more green and brownfields opportunities.

There is a lot of pressure on government from special interest groups wanting to maintain the status quo however. It is far from guaranteed that the RMA refresh will deal with this as anything more than a cursory or fringe issue.

What if we didn't have/are not having the COVID triggered stimulus?

My guess is that they would come up with stimulus anyway.

QE and whatever other magic these clowns come up with produces no goods or services...nothing zilch. It just diverts what is currently produced into different pockets.

That’s all you need to know....the rest is just bs.

Agree that in order to try and solve the problem, have to look at increasing supply and equally important to decrease demand, specially speculative demand.

Anyone if only emphasising on supply is for vested biasedinterest knowing fully that supply will take time but speculative demand can be controlled immediately, if want to.

All eyes now on RBNZ though know that are playing to a script of wait and watch to delay being fully aware and knows what delay by each month does to housing prices otherwise their approach of act fast to be sorry later on would have apied and not go with policy of wait and watch.

It's like watching that one drunk guy at the frat party blowing up a balloon, knowing it's going to burst in his face, but unsure exactly when. The tension is palpable, almost unbearable, because the balloon ought to have popped already.

Interesting to note the sea of red on the auction results page over the past little while. Today is particularly striking. The house on the cliff might be apt after all.

https://www.odt.co.nz/business/property/house-prices-continue-soaring-s…

Would be interesting to see what this thick skin manipulators come up with in May announcement.

Have full faith and confidence that they will find some excuse or reason to deflect despite all fingers pointing in one direction - housing ponzi. Normally also April is little quieter and may us that as an excuse or will find or manipulate some data to read out the air scripted announcement.

If were serious would not have even waited till May.

Just heard Michael Rehm, a lecturer in property at Auckland University, talking on Radio NZ. He's adamant prices will fall back. He can't see any chance of us talking about $2 million medians in Auckland in the future.

Good to hear from an expert without vested interest.

https://www.rnz.co.nz/national/programmes/ninetonoon/audio/2018791658/e…

When the experts was asked, were clear that it is the government that has to take the call and ask for DTI and RBNZ on its part can go for regulating Interest Only Loan.

Anyone and everyone is talking except ..(would be deleted by editor - so please us your imagination)

Unfortunately is not common, most people that get attention on the media are real estate cheerleaders. Hard to make any sense of what's going on if you listen just to their ill advice. NZME and the likes should be ashamed of the manipulation they have been doing to the NZ population and in part are responsible for FOMO creation and bad financial decisions a lot will regret as soon as interest rates start climbing even slightly.

You must admit most are much better value than what you would get for 1M.

Current property market has the feeling of a blow off top. How can one of the main drivers like migration be spinning in reverse while the market powers forward. I guess credit acceleration for housing is still locked in high gear. If borrowing for housing slows then it’s going to get nasty.

The price increases have simply been to big to fast fat pat. Had this been spread over 3 or 4 years it would have gone under the radar. Things simply have to hit a brick wall, it cannot continue. There is now a strong possibility of the DGM's coming out and saying we were right but I don't think anyone at this point would be surprised if there was a small market correction. The thing is any government we have cannot wait to reopen the boarders so when the vaccine passports come online and the boarders reopen to them then its going to be off to the races again for the property market. Good chance this will coincide with next summer so expect any short term dip to disappear.

"borders"....

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.