By Greg Ninness

The Government's efforts to rein in house prices may be starting to produce results, with early signs prices at the bottom end of the market are stabilising, according to interest.co.nz's Home Loan Affordability Report.

The Real Estate Institute of New Zealand's national lower quartile selling price rose only marginally to $592,500 in May, from $591,000 in April. And both figures were lower than the record high lower quartile price of $598,000 set in March.

Of the REINZ's 12 sales regions, the lower quartile price was down in May compared to April in six - Northland, Waikato, Bay of Plenty, Hawke's Bay, Wellington and Otago, and unchanged in Southland .

The lower quartile price was up compared to April in five regions - Auckland, Manawatu/Whanganui, Taranaki, Nelson/Marlborough and Canterbury.

However the changes, whether up or down, were mostly small, and suggest an overall flattening of lower quartile prices rather than any significant shifts. And the spectacular price gains evident in the second half of last year and early this year appear to be over.

So while upward price pressures may have eased for first home buyers, they won't be getting any bargains. Nor will they be getting much in the way of extra help from movements in mortgage interest rates.

The average of the two year fixed mortgage rates offered by the major banks declined marginally to 2.52% in May, after sitting at 2.53% for the previous three months. That's a record low since the Home Loan Affordability report was first produced in 2002.

Any further falls in rates this year are also likely to be marginal at best and longer term mortgage rates have already started to rise, with shorter term rates expected to follow them up next year.

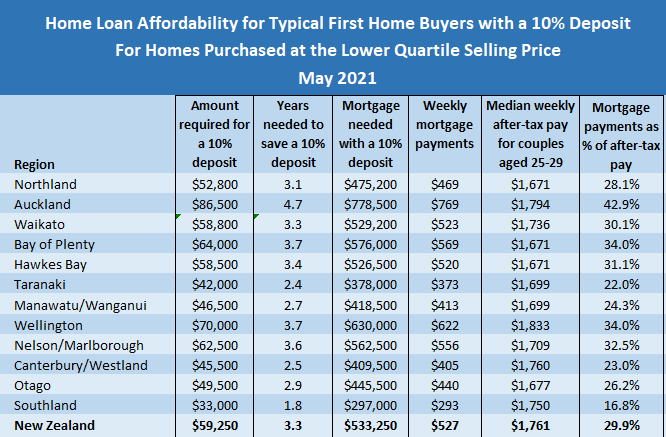

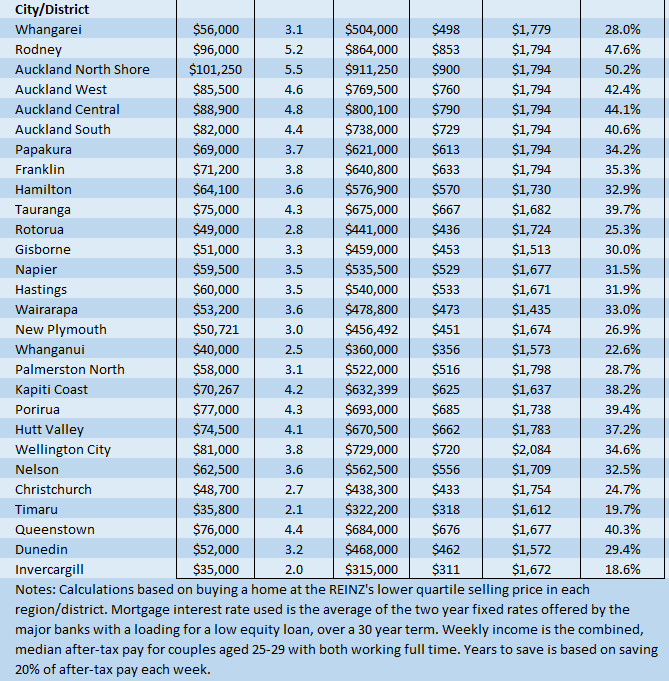

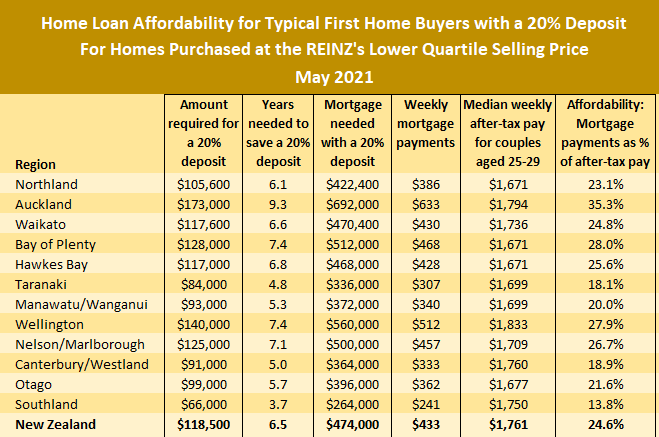

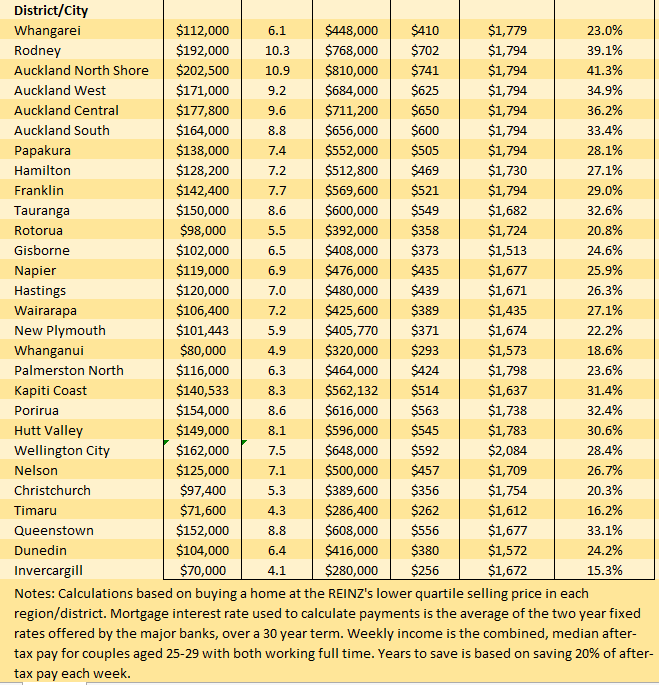

The tables below show the main measures of housing affordability in each region, based on a couple both working full time at the median rates of pay for 25-29 year olds, and purchasing a home at the lower quartile selling price in each region. Separate figures are provided for making the purchase with a 10% deposit and 20% deposit.

The striking thing about these figures is that the numbers for Auckland stand out from those for the rest of the country like a sore thumb.

With the exception of Queenstown, first home buyers outside Auckland should find the mortgage payments on a lower quartile-priced home relatively affordable. Their mortgage payments are likely to eat up around a third or less of their take home pay, even if they purchased the property with just a 10% deposit which would mean paying higher interest rates for a low equity loan.

But in Auckland, the mortgage payments on lower quartile-priced home bought with a 10% deposit would eat up almost 43% of a typical first home buying couples after-tax pay, pushing the city well into unaffordable territory even though interest rates are at historic lows.

Anyone in that position would be left especially vulnerable to interest rate rises or a loss of income.

And it would take a typical first home buying couple 4.6 years to save a 10% deposit for a lower quartile-priced home in Auckland, assuming they could save 20% of their after-tax pay every week.

If they wanted to save a 20% deposit it would take them 9.3 years.

So although the figures suggest the housing affordability beast may have been contained for the time being, it has certainly not been tamed.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

54 Comments

Keep North Shore expensive. Keep the riff raff out.

Gang activity has been rapidly growing on the North Shore in the past year or two. Selling drugs is as lucrative as ever, no problem affording a house on the Shore.

Haha gang activity is everywhere have you seen Remmers and Orakei lately?

Or Grey Lynn and Pt Chev last weekend?

Sorry too late by a decade..keep the riff raff in

It's not increasing prices that are the problem. It's is the level of prices.

You have to wonder what planet these people live on sometimes. Hey, we temporarily stabilized the median wooden tent price at 1.3 million dollars. Work is done, great job guys! Mission accomplished!

Meanwhile back in reality the damage is done.

True. There is little commentary from 'experts' on the 'social costs' of average FHBs entering the housing market at such elevated prices.

What does borrowing a million dollars for a mediocre property do to a family's mental health and wellbeing? What about the added stress among by recent borrowers from the constant media chatter on higher interest rates, maintenance becoming costlier and an inevitable property crash?

It is now too late to stop a mass exodus of young people to Australia. I spent the weekend with a younger generation of the family in Auckland and even those who own homes are thinking about selling up and going to Australia. Cashing up at the top of the market and leaving for far higher salaries and lower house prices.

Many of those who do not own homes now, are unlikely to ever do so now in NZ; especially as the government has stated that it will only ever allow the prices rises to moderate and never fall. They have no hope or option but to leave.

very sad but you are right

I wish I was wrong. But wishing doesn't achieve anything.

Yes you are right, but sooner or later the market will have to adjust itself - the laws of the market apply to the NZ housing market too, and Orr and the other clowns at the RBNZ can only postpone an inevitable and significant adjustment downward, once interest rate normalize and once people start to understand that current house prices in NZ are ridiculously over-inflated, utterly unsustainable, and with no relation whatsoever to economic fundamentals.

But you are right - if I was young and skilled I would not think twice before leaving for AU. Why subsidize some house speculator nonproductive parasite with my real work, or be the next sucker who keeps the housing Ponzi alive ? Nope.

A bit of caution on saying anything negative about RBNZ or Orr, you might be on the receiving end of P8,s wrath.

Fortune- I'm no fan of Ardern/Orr and what they have allowed to happen and Aussie will call for many young people but the same thing is happening in major Aussie cities Sydney up 15% since Xmas ! Waiting for a change/crash in the market is not a certainty, many calls over the years are still waiting. If young people already have a property and are moving to Aussie I would strongly recommend they keep the NZ property. I say that through having seen many friends over the last 40 years chase the bigger money overseas and if /when they want to return all their hard work has been negated through not being in the NZ market. Clearly not all want/will return but home is home and family ties have powerful influence as we age. It's a sad fact history shows that when Labour are in office house prices always rise significantly more than under the other lot check it out it's a fact.

rubbish, always suspicious of people who reference "someone they were talking to" especially when young people spout views that suit better to Newstalk ZB. If there is any semblance of truth it certainly isnt the majority view from young people.

Up 20% in a year and then dropped 592k to 591k

https://encrypted-tbn0.gstatic.com/images?q=tbn:ANd9GcSrEoGcCZLicplXWdw…

sorry to be blunt.

Any NZ government can talk big but deliver sxxx.

The breather in the affordability trend is a powerful signal for potential buyers to act before the next take off.

Great fortunes are seldom made in a certain market.

Act now!

Honk. Honk.

that's why the young kiwi generations more and more heading off to Australia,they would never be able to buy roof over their head in their own country,probably my kids would do the same once they grown up...very very sad time for nz and nzders and thanks for ruthless governments(national and labour) ruin this beautiful country,bet you won't see much proper kiwis here anymore in the near future,only rich emigrants

the country has been run by incompetent ppl for more than three decades thanks to its poor political system.

I disagree. John Key wasn't particularly incompetent. His priorities were just himself and his mates instead of the country.

On the bright side, he didn't imprison me and harvest my organs when I called him names.

The problem with winnie the pooh isn't his competence.

Is it the genocide and disapearing political activists? Of the many reasons one has to at least be genocide. But then for some reason the NZ govt is totally happy with it by their actions so perhaps we should follow suit... Oh wait we can disparage leaders incompetent and insane actions here.

From what I could make out they were agreeing that failure on their mission would require their re-education with a potential add on of an organ removal, that or he was asking them to grab some milk while they were out.

Fun link. First comment in English I saw:

"Pay them highest salary so that they can focus on their work! May China be strong and win the conspiracy of the west!"

Social Credit +2

Haha love your work Brock.

So winter kicks in and prices steady.... Que yay we did it hahaha idiots

What a joke. It is all about propaganda. It is just sad...that is it.

And the government could cherry pick any figures like this that it can, to show their policies are working. But the main effect from the policies seem to be rent rises

"Tentative signs government moves to rein in house prices may be starting to work for first home buyers.."

Seriously, visit any auction room which have become suction room.

A person who does now swim may not drown in five feet of water but than every inch is fatal. Same applies to house price - FHB are drowning and now even a slight percentage rise is killing, who ever is left in the market.

Talk about price level and not price rise. From here on any rise is meaningless for FHB as most have given up, specially with in Auckland where median is 1.3 million - is it a joke on NZ wages despite low interest rate unless you have an house and upgrading or rich daddy.

So this is making fun of FHB, when any experts suggests that houses are more affordable for FHB.

There is hardly anything worth buying on the market at the moment with record low inventory. The Brightline test seems to have had the unintended consequence that is preventing investors selling. So we can't really read anything into the figures. But prices need to actually drop 30 percent to be at a level that is sane.

More like 70%.

I've seen this language a few times. The bright lines test is not locking anyone in, or preventing anyone selling. It simply means you are likely to have to pay tax on your profit. Not a terribly big deal if you've owned the property for a few years - just puts you in the same position as wage earners who pay tax on every penny they earn.

It was being discussed on stuff here. It is also a big deal as it could be tens or hundreds of thousands of dollars. http://www.stuff.co.nz/life-style/homed/real-estate/125525933/wouldbe-h…

The other point is if they sell, what would they then put that money into, that could get as good a capital gain?. Certainly not bank TDs

What would be your reasoning for the record low inventory levels in NZ

Here in chch it seems to be everything that's put up is snapped up. Still a lot of money chasing the market, for now.

Winter and build speed. Plenty of fresh land plots coming onto the market if your willing to wait for a new build.

Ageing pop owns too much of stock, % wise and are selling less often.

This issue is slowly increasing and is ignored by analysts.

Also, as prices rise and inequality too, who will buy when old do sell, as prices too high for young cohort.

Probably the children of the rich and old will buy with parental help, but not the serfs.

I think a contributing factor is that it's very hard for people to trade up properties at the moment. I'm sure many like me can't get open bridging to buy a house while keeping the old one so can only make conditional offers. This means we inevitably miss out.

We could sell our house but then if prices keep tracking as they have been recently we would end up being lucky to buy back our old house. The low levels of stock mean finding something suitable are remote so like us I'm sure people just stay put, perpetuating the low stock levels.

Common reason I have heard is that you can't afford to move up the "Ladder" so are staying put.

All very well that the house you bought for $400k is now worth a $1.2mil. But that house you were looking at that was $500k, is now $1.5mil. It turns out that extra $300k is real money that people simply don't have.

It is not just the FHB being locked out.

Its the same in Christchurch. Absolutely nothing to buy, even if you wanted to upgrade. In the $600k - $1M bracket its now mostly brand new townhouses crammed 6-8 of them on a single section with no garage and maybe one off street uncovered car park if you are lucky. In the sub $600k market there are a lot of obvious ex-rental homes - run down, mostly units or student flats that require a lot of work to make them reasonable. Even if I wanted to spend $2M in my preferred areas there is literally nothing to buy. People can't afford to upgrade, so they are staying put, and maybe renovating. The lack of movers reduces inventory even further, and combined with investors hanging on due to the 2018 Brightline extension, its no wonder that the few reasonable properties that come on the market are furiously bid on at auction driving up their price to stupid levels.

Friend of mine (66 years) is thinking of following his children over.They have been in Hervey Bay for about 10 years'He says that comparable houses to the one he has in Hamilton are far more affordable and if he sells and buys should leave him with a surplus.Don't know how his super is affected but no doubt he will find out before rushing off.

Is this really news?

“The Government's efforts to rein in house prices may be starting to produce results, with early signs prices at the bottom end of the market are stabilising.”

The real news that fails to get reported is the rental crisis NZ will be facing as rents escalate out of control forcing renters to go into emergency accommodation.

The media & government seem to applaud First Home Buyers displacing renters as FHB mop up their rental properties.

Supply of lower end rental properties will continue to reduce as Mum & Dad investors abandon this type of investment due to the tax changes & risks around getting good tenants. For renters this will be a crisis never seen before in NZ.

If the government had carried out due diligence with a benefit/cost analysis on interest deductibility it would have never introduced the new tax because of the negative impact on renters.

Mum & Dad investors are needed to supply rental properties as the government can’t do it by themselves.

The new tax law provides almost no benefit for First Home buyers & a huge disbenefit for a large number of renters.

It doesn't seem like that rent increases are happening though: https://www.stuff.co.nz/business/125543691/rents-flatten-after-governme…

After the 6 month rent freeze imposed by the government many landlords increased rents at Xmas time by only small amounts. This is the data that Stuff is reporting on.

At the end of March the new tax rules were introduced. NZPIF then did a survey to find out the intention of landlords. The vast majority intend to increase rents significantly.

Expect this to occur this Xmas as landlords can only increase rents once every 12 months.

No, it's not data from Xmas time. Stuff is reporting on the Trade Me Rental Price index for May, which according to trademe is: produced from Trade Me Property data of properties that have been rented in the month by property managers and private landlords. On average over 11,000 properties are rented each month and the report provides a comprehensive insight into this part of the property market for tenants, landlords and investors.

So if we want to know whether rents are actually increasing, then data about new rental prices from last month is more useful than data from early April about what landlords intentions were.

Rents in May 2021 were much higher than May 2020. In some regions average increases were above 10%. This shows the rent market is getting out of control. See Regional chart in link below. It is erroneous to compare Mar 21, Apr 21 & May 21 with each other as landlords can only increase rents every 12 months.

https://www.trademe.co.nz/c/property/news/good-news-for-tenants-as-rent…

Yes, they are definitely higher than last year. But lack of increases over the last quarter are a good indication I think that the trend is slowing (because here is something that could be true: rents were rising, until the government announced changes in early 2021 - that's consistent with the data). Though I suppose you are right that we will have to wait a little longer to be certain. I reckon we'll probably have to wait til Jan/Feb next year to know for sure.

Come back when there is the slightest shred of evidence that Mum & Dad have stopped hoarding properties.

Or that they've declined to charge as much rent as the market will bear, before now.

3 years plus to save over 50k for a 10% deposit in the lower end of the scale? I think that needs a reality check. What young average family can save that?

The game plan for most young people should be leave having a family to later, go to Australia and save for a deposit, then come back if you still want to (though many end up staying).

How much later would you like people to leave having families? We're already pushing into the realms of western population declines due to lifestyle and living cost factors, surely the 'game plan' should be to actually fix the problem rather than ever-narrowing the window in which people can actually have families?

My project manager went to Bunnings to purchase framing timber for a residential housing complex, They had no wood, had to buy H3 (3 times the price)instead as the project must proceed. Affordable housing is a dream when there are no materials to build with and its run by a minister who is so out of her depth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.