First home buyers have received some relief over summer, with significant price falls at the bottom of the market in Auckland and prices in the rest of New Zealand mostly flattening out at the start of the year, according to interest.co.nz’s Home Loan Affordability Report for February.

The most significant change has come in Auckland, where the Real Estate Institute of New Zealand’s lower quartile selling price peaked at $966,000 in November last year and has dropped back in every month since, slipping to $900,000 in February.

That’s a 6.8% price fall in the space of three months. Although $900,000 is still an eye watering amount of money to pay for a home at the bottom end of the market, the $66,000 reduction would have brought significant relief for anyone shopping for a home at the so-called affordable end of the market.

First home buyers would have been further helped by the fact that although mortgage interest rates are rising, they took a breather at the start of the year.

The average of the two year fixed mortgage rates offered by the major banks bottomed out at 2.52% in May last year and then rose steadily to peak at 4.21% in December.

The average dipped slightly to 4.19% in January and crept up to 4.20% in February.

In practical terms, the two year fixed mortgage rate has remained flat over summer, and although it has risen from its lows, it has only gone back to where it was in February 2019 and remains well below its long term average, although further rises are expected.

So how would this combination of a drop in house prices at the bottom of the market and a lull in mortgage rate rises have affected typical first home buyers over the summer months?

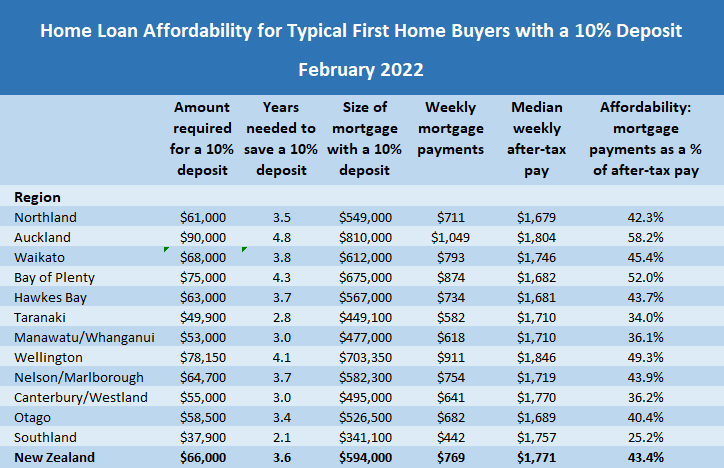

Firstly it brought down the amount they would have required for a deposit on a lower quartile-priced home, from $96,600 for a 10% deposit in November last year to $90,000 in February this year, saving them $6600.

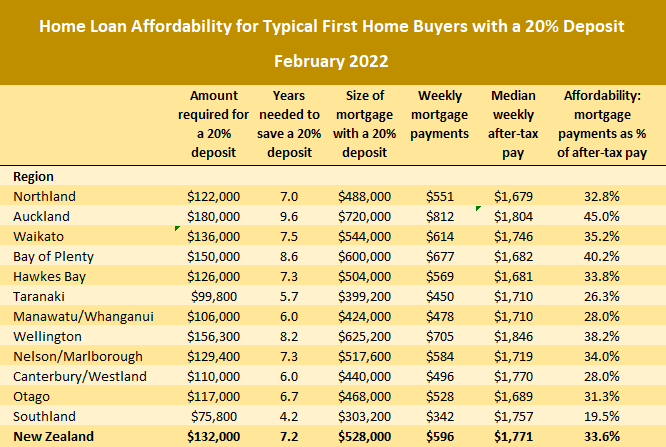

You can double those numbers for a 20% deposit.

Secondly, it reduced the amount they would need to set aside for the mortgage payments on a lower quartile-priced home purchased with a 10% deposit, from $1115 a week in December to $1049 in February, a reduction of $66 a week.

However, even though those reductions would be useful, house prices in Auckland remain at such high levels that the prospect of home ownership is likely to be well out of reach for first home buyers on average incomes.

Interest.co.nz estimates that a couple who both work full time at the median rate of pay for 25-29 year olds in Auckland, would be taking home $1804 a week after tax between them.

That’s without allowing for any other deductions such as student loan payments.

That means that the amount of their weekly pay packet that would be eaten up by mortgage payments on a lower quartile-priced home would have declined from 62% in December last year to 58.2% in February this year.

The traditional rule of thumb measure is that mortgage payments are considered unaffordable when they take up more than 40% of after-tax pay.

By that measure, achieving home ownership in Auckland is not a realistic possibility for young couples on average wages without winning Lotto, finding a pot of gold at the end of a rainbow or receiving a visit from a generous fairy godmother.

However what the latest figures do show is that house prices can fall at a rate which more than negates the impact of rising interest rates. This could lead to a gradual improvement in affordability over time.

A different picture elsewhere in NZ

Outside of Auckland the situation is different.

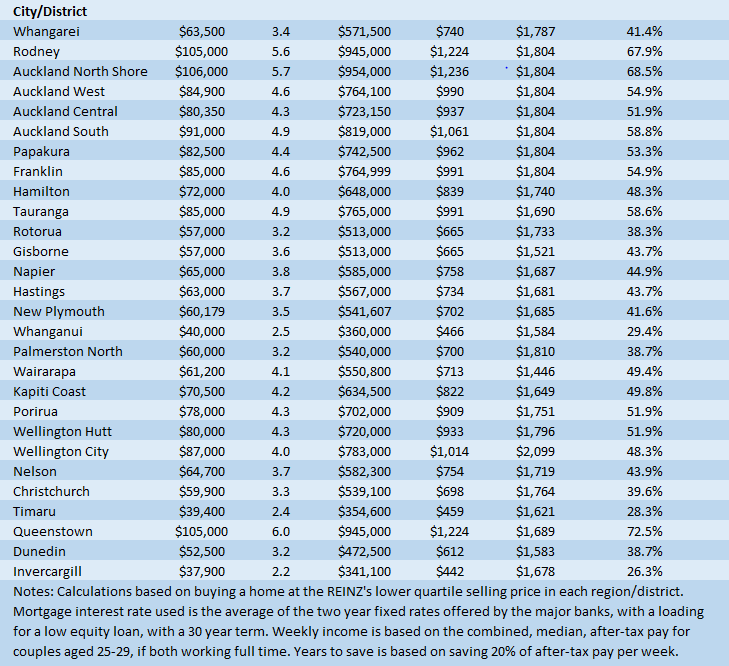

There haven't been the big price falls seen in Auckland over the last few months and prices are still going up in some regions, although at a much slower rate than previously. Four regions – Waikato, Manawatu/Whanganui, Canterbury and Otago hit record lower quartile prices in February.

The overall trend outside Auckland has been for lower quartile prices to flatten and that has been reflected in the national lower quartile price. This peaked at $670,000 in November last year, then declined over the next two months to $650,000 in January, before bouncing back up to $660,000 in February.

Those monthly movement were small, so the overall trend for prices at the bottom end of the market for properties in regions outside Auckland is for them to have settled near their recent peaks.

The big trends for prospective first home buyers to watch over the next few months will be whether price falls in Auckland continue, whether those price falls begin to spread outside of Auckland, and whether any price falls will be sufficient to offset ongoing rises in mortgage interest rates.

The comment stream on this story is now closed.

119 Comments

So lowest quartile Auckland houses still cost 6.5 times the MEAN Auckland household income.

Long way to fall yet.

Probably not possible for a single income earner Tbh

Yeah I noticed that too, have to be a DINK to buy a house and really tight with money. Presumably these DINK's are not living with parents so saving a deposit while renting won't be much fun either.

The evidence mounts that house prices aren’t going to collapse…….

Those who yearn for a crash 💥 are bound to be disappointed.

TTP

TTP The ship is already sinking but you already know this at what point do you admit you got it wrong.

Housing doesn't sink, it's a sub. Goes down but comes back up. You actually think that property is going to collapse and never recover. Play the long game, you can't lose

This is very one-dimensional thinking - as if the decision we are all faced with is 'do I buy property, or do I not'.

What about diversification, what about alternative investments, what about risk-adjusted returns? If you already own a home, the time to consider more is when you have balanced your overall portfolio with some diversify in terms of asset class and geography. Putting all your eggs in one leveraged basket is insane.

that's the problem though, how do you diversify? Equities are also expensive, not sure how to trade commodities, don't know much about fine art and precious metals will get spanked as the war in the Ukraine gets resolved, cash is being eaten alive by inflation. what to do?

The ASX offers exchange traded funds (like FOOD and FUEL) that might provide a hedge against inflation and diversification from the housing market. You can buy as much or as little of those as you wish (with a $30 trading fee).

#notfinancialadvice.

NFTs are where it's all at.

Not untrue. The point of note is whether the sub can survive crush depth of debt whiles its submerged.

How long a game are you talking about , leaving kids a property or grandkids.once this drop is completed it could take 15 years just to break even , not good for investors but fine if you just want live in a house and pay over valued mortgage.

Lots of could do's I'll stick with reality. If this property market tanks for 15 years I'll give you a house for free.

I think it was around 10 years in UK back in the 1990 I work for large bank so did not bother me as my interest rates was fixed

So true, Japan's fell but is just coming right, only took how many years?

If you bought a house in Tokyo in 1989 you might be wondering actually how long is the long game...30, 40 years?

Tell that to the millions of Americans who lost properties during the GFC ...not so long ago

Actually they are heading very very south, like a lot, really a lot.

It's very delusional thinking otherwise.

There will be losers, as always, but also winners.

Govt will most probably not intervene (there are only 18 months before next election) as they are supposed to pretend to care for lower income people, so bailing out property owner is not a good PR excercise.

I would be very nervous today in being too much into property investment.

On the contrary, Lucerna, buying in a slow market can make a lot of sense......

For a start, there's far less pressure to make quick purchase decisions. One can put more time and effort into the due diligence process. Plus, one ought to be able to bargain down the price.

People who buy in market downturns are known as counter-cyclical investors - and there are heaps of them about.

TTP

Yup, that makes sense, but implies to agree that the market direction is down.

On "how much down" I think we have really different opinions.

I am pretty strong in maths and stats (it has been my job for 27 years) and I have seen these things happening in several parts of the world.

What every country had in common is that they were thinking they were different.

I am not putting whishful thinking in this, is just logical consequentialism: this housing market is bound to retire almost 50% from the point it started to grow linearly. The last part (the last year) will recede much faster than that.

This is what I believe

But you are free to bet your money in me being wrong :D, it's your money, not mine

Comments like the above from lucenera are what gives me a good belly laugh before I go soundly to sleep knowing my property investments are "as safe as houses". The new commenter on the block thinks he knows stuff and has something new to say :)

Consequentialism - hahaha

Predictions of 50% drops are only slightly more silly than the prediction of small gains made by Ashley Church and Tony Alexander late last year.

HM If average wage earners can only afford to borrow max 450 k who is going to buy houses at a million, also need 20% deposit.with interest rates raising and inflation up a 50% drop is well on cards. Some places are already down 15% from Peak.

I think he meant that my prediction is not too crazy, in response to HW2, as he claims it's impossible and ridicolous

Sorry but where are you getting 450k max capacity from? Median weekly after tax income is $1,770 (per above article) so very roughly $120k pre tax that's borrowing capacity of more like $720k max so that's plenty of capacity in theory just below the $1m mark.

Comments like this from HW2 just show how worried property investors are, over leveraged and about to see little empires vanish.

"The new commenter on the block thinks he knows stuff and has something new to say"

This is a delegitimization excercise. Common and pathetic.

I could define you an old biased commenter, not worth to be read, following the same.

I tell what I think, you tell what you think.

I got no idea why the term consequentialism make you laugh too, but well, if that is how you have fun it's your business.

I don't like this kind of behaviour, and I find it inappropriate.

Welcome to the Interest comments section. This is why there is so little diversity of opinion here. And why I never comment ("make me a sandwich" being the response when I have).

I like diversity, please comment. Looks to me that we need more colour around here. :)

Yup. The internet rule 'never let them know you are a woman' does seem to apply round here.

Lucenera, You may find your c-ism word in the dictionary but... to me it is as original as the rest of your argument is unoriginal. That is why I said that what you think are new ideas actually are not and has no credibility

HW2, perhaps you need to be reminded that people from different backgrounds and cultures use language differently, and for some, English is not even their native tongue. Enlightened folk see this as nuance that adds richness to the discussion, the substance of which is what really matters. The least you could do is apply some common sense and consider the obviously intended meaning of the post - which was thoughtful and well-reasoned - rather than having a crack because you don't agree with a particular word choice.

Go back and read my comments... to repeat, I totally disagree with his unoriginal comments the sort of which have been spouted by DGM for over ten years on interest. Nothing new. Btw I do not know how you arrived at anything to do with non-kiwis. Half the people who live here were not born here. I welcome anyone new who has good intentions

I get that you disagree with his/her comments, no problem with that. But your response seemed to mock the poster, who you noted is new to the forum. You're entitled to do that, just as I'm entitled (but for the grace of the Ed) to tell you I think you've come across as a bit of a tool.

No problem with that, I am happy to not follow the crowd, especially this misguided crowd. We have done Extremely well by that pattern

HW2 - You sound like you are desperately overextended with interest rates about to destroy you. Not to mention tragically late with missing the top of the market in November last year.

Yes, I agree, if you look at stats, a 50% drop would need to happen to revert to the long-term mean, and I have worked out that approx. 50% of the price of any NZ house price are non-value added costs. ie unnecessary costs that only exist because of restrictive Govt. policy.

BUT without removal of these restrictive policies, it is unlikely prices will fall that much but could fall some and then gets caught frozen in time like Japan, with wage inflation over the next decade or two, restoring it to the correct median income multiple and trending to the long term mean.

Just an old bugga looking back over 80yrs. Think I can understand how some folk think the recent past = the future. Sadly we all have to learn in our own way and in our own time.

You mean unlike what they have been doing to date ie not enough time to proper due diligence and paying top dollar.

I think you are underestimating how much the institutions and government will react to counteract a house price fall. After all, JA has promised that every homeowner can expected to gain from owning houses. A NZ government, of whatever ilk, will sooner see our young people emigrate than see house prices fall. It is a type of corruption of institutions, the leaders of government institutions are generally highly invested in property so inevitably and naturally will take decisions to support their own interests.

This is fundamentally why property has become more of a welfare scheme for the wealthy than a market. In a free market downward price discovery is allowed and speculators aren't bailed out or propped up at the drop of a hat. We have folk ranting at beneficiaries yet completely lacking in self-awareness when it comes to what handouts they have received.

But they are "hardworking" "mum and dad" investors who "provide housing" and are just trying to "look after their own retirement".

It would be wrong not to bail them out <shrug>

TTP... Anyone would think you DON'T run a nationwide RE agency

we've barely started our descent, never mind landing. I'm not willing this crash to happen because so many people will get hurt.

Remember, bear markets are not a 3 - 6 month thing. This bear market will be a 5 - 10yr thing, by which time TTP would have stopped commenting since the debate will be over and only the cold hard facts will remain.

Many on here want to know when is the right time to buy back in. answer - when there are no more property bulls on this site, wait a further 6 months and then buy. you will still likely miss the bottom, but it will be much better than having bought now.

I'm not willing this crash to happen because so many people will get hurt..

Really??

.......in case you haven't noticed most of NZ society (bar a few landlords) have been significantly hurt already.

A big drop is needed and the sooner the better.

Exactly - when talking to property investor types they keep telling me that its not in the best interest of society for property prices to fall because of the widespread pain it will cause.

I think ask them why we have record numbers of people needing welfare and food bank assistance when the average house price is about $1,000,000 across the country.

No answer. How then has house prices going up 30% in a year or 40% in a few years been beneficially for society? It simply hasn't been. Its created a massive amount of financial risk and social division/instability and large amounts of stress and pain for people who don't own property.

A reset of house prices will cause short term pain, but in my view it is probably the best possible outcome for society in the long run - when viewed from an independent/utilitarian perspective. Some individuals will suffer more than others....but that is the risk one takes when loading up with exceptionally large amounts of debt...especially in times like the last two years where there should have been warnings and cautions everywhere (which there were.....including from the RBNZ leadership).

I am a property investor type (although not leveraged) and I think house prices are too high, stop grouping us. Seriously if you speculate in property you take the risk, if it goes up you win, if it goes down you loose it should not be the governments job to protect people investing in houses.

I agree that the house prices are far to high and its the governments job do what is best for society, not property investors.

Investor says property market 'tanking' and auctions have had their day. Even stuffed.con have given up the spruiking.

https://www.stuff.co.nz/business/128090978/investor-says-property-marke…

...except then he goes on to say that he sees prices "tumbling" by 10%, or maybe 20% at the lower end. This is not "tanking", it's a soft landing, and should be considered a best-case scenario for recent FHBs.

-20% is considered a Crash.

It is in the sharemarket.

And the property market.

Okay. It's an informal definition, I guess you can use it however you like.

What's your definition of "tanked"?

Half a bottle of Gin.

...so 50%?

Auckland City median house price falls 19 per cent since peak in November. The MSM are not holding back.

https://www.stuff.co.nz/life-style/homed/housing-affordability/12811007…

Yikes. They're going to have to start coming up with new verbs soon.

Also, is that literally the only photo of Nick Goodall in existence?

Young Dr Evil.

The market is Tanking.

As they note, median values can be a bit distortionary.

HPI, although not perfect, is the one to watch.

Suspect it's down 8-10% in Auckland City.

Auckland City down 6.4% in the three months to Feb per the HPI. Although I suspect you are closer to the truth as not sure I buy the HPI numbers with Wellington City supposedly only down 0.8% in the same period and that definitely doesn't seem to be the case

Not good for the bubble if the prices of the shacks and rats' nests are starting to head south.

Indeed. How much longer will greed continue to drown out the fact that the music is stopping. Specubox owners seem oblivious, even after its in the main papers, radio and on blogs. Smart money exited late last year or used the recent artificial lows to hammer their debt ready to stack in better conditions.

Yep its playing out so far just as I said only yesterday.

Granny Herald reporting that up to 30% of agents will move to other work. Other words for fired, shoved, starved, mortgaged etc. Perhaps they could just ditch their leased cars, cut coffee and advo on toast. GFC showed it was a great time to pick up a bargain on interesting cars. I recall Aston's and Ferrari's going for less than half their "market" value.

Just inked an outstanding deal on an Audi. Good times.

The could pick fruit or help out on farms.

Another 50% decline is needed before average wage earners will consider buying in Auckland.

There's a question here around whether your 'average wage earner' is still employed if house prices dropped 50%. Everyone assumes they'll still have a job but if discretionary spend falls off a cliff and mortgage holders slam their wallets shut then it's not hard to figure out who will cop it.

If prices dropped by 50%, the ‘average wage earner’ will probably be worrying about something more serious than getting on the property ladder.

Where's the -7?

But even in a bad recession, the unemployment rate only rises to about 10%.

The majority of people who want to work still have jobs. Even in the worst recession.

You havnt lived through one have you

If average wage earners cannot afford to buy who will, it is set to fall as rates start to climb from emergency levels people who made money on way up will be giving it back on downturn if reinvested at high levels in last 2-3 years.

I'm not sure average wage earners are the ones propping up the market though are they?

Our economy is largely an export one and discretionary spending has pretty much halved already thanks to COVID. If house prices dropped 50%, we would still be exporting milk/meat, we would still be selling wine and software overseas, we would still be doing all the things that builds real, long term wealth. We might get a finance system shock and a bunch of luxury item stores might disappear, but we will still need to buy food/power etc. New home building might stop as the cost of building is compared against cost of existing (good time to shake up the broken industry anyway) and we might wave goodbye to a few hundred thousand people overseas, probably lots of tradies.

Our economy is overwhelmingly an import one......manufactured goods, services and labour....not much left really.

For all you Auckland FHB's out there, stop "feeding the machine" and if you can work remotely or get a good job in another area in NZ - go for it !

Otherwise, if you know good people in Aussie have a crack over there - always best to go where you know someone.

Why should you "finance" these greedy Auckland baby boomers, politicians, property investors, developers, banksters, RE agents, media, lawyers, accountants and all their "hangers on" , just so these groups can carry on with the "financial style they are accustomed to" - all at YOUR expense.

I don't say this lightly - this Auckland market is not the most expensive in the OECD compared with average incomes for nothing !

Seeing plenty remote working into Aussie and getting paid Aussie rates. Good gig that one.

It is starting to bite.

NZ companies still not able or willing to match Aussie rates and struggling to get anyone with some specialist IT skills here.

I have two different friends moving back but getting their Ozzie firms to keep them on at current wage. That's interesting but probably not sustainable. I imagine their employer will ditch them at some stage.

Everybody knows that the dice are loaded

Everybody rolls with their fingers crossed

Everybody knows the war is over

Everybody knows the good guys lost

Everybody knows the fight was fixed

The poor stay poor, the rich get rich That's how it goes

Everybody knows

Thanks for the well worded ditty

Full of grief and lots of pity

A poet youre not, maybe youre flirty

Please have your say but dont get shirty

Great song that one

Another few months and guarantee stuff front page will be full of wailing underwater people needing government bailout.

Good pick.

The tones certainly changed on One Roof - articles such as: 30% RE agents will quit, the economy a big worry for housing, Jacinda needs to do more for FHBs etc. It wasn't long ago they were saying the opposite...

Yep, there will be a lot of unemployed RE agents soon. And a bit of a lag before we see a lot more unemployed builders, architects, surveyors, planners, tradies etc etc.

"It's time for socialism, please send help!"

I would say FOMO pushed prices up with emergency low rates these people will soon lose deposit and be in negative equity, some would have made heaps on way up.

Entirely likely. If you've sat on the sidelines while the government blew prices out of the water and the RBNZ looked like it would do everything they could to stop house prices from actually falling, you could be forgiven for thinking it might never happen and getting in while you can. But I'm guessing the migration tap will go back on full-bore and we'll get a softer landing. But still pretty awful for recent FHBs who are looking at losing all of their own equity and a bit more after years of being told not being able to afford a deposit was because they spend too much or were too lazy from snarky elders.

Winter hibernation starting earlier than normal, and maybe going longer?

It's great to see commentary vs. the peak price, rather than constantly comparing to YA, which is largely irrelevant at the moment, given the crazy spike in prices last year.

Median prices are down significantly more than this in certain parts of Auckland, as per REINZ data.

Auckland City Spike NOV $1.540M FEB $1.250M -19% from peak

Franklin Spike JAN $1.050M FEB $1.015M -3% from peak

Manukau Spike NOV $1.235M FEB $1.150M -7% from peak

North Shore Spike NOV $1.555M FEB $1.370M -12% from peak

Papakura Spike NOV $1.173M FEB $0.960M -18% from peak

Rodney Spike JAN $1.350M FEB $1.270M -6% from peak

Waitakere Spike NOV $1.199M FEB $1.075M -10% from peak

People are seeing years of savings disappear as deposits vanish and this is just start as rates rise from emergency levels.

Add 6% inflation to the mix for the year and real prices are certainly on the retreat. Question is whether this is the start of a longer term trend or not?

Yield curves are inverting across the board (bond market is picking recession/deflation) and the Fed/RBNZ based on history will probably keep raising rates right into the recession. Could be the perfect storm for further falls in prices are people struggle to maintain employment and pay rising mortgage rates.

Be interesting to see what the RBNZ's response will be if/when the recession starts....drop rates back from 1 to 0? But if housing price downward momentum is mainstream and there is no confidence in prices rising again....will people be willing to step in and risk losing their fingers in a falling market?

Bonds will make sure rates will continue rise as FED need to keep inflation under control,so no chance of RBNZ lowering rates as this would crash NZD and make NZ inflation skyrocket.

Not surprised. Last two years have been totally artificial with crazy levels of debt passed to the banks an pumped into speculative property. It is rolling back.

These figures illustrate quite nicely why I don't understand some people's predictions of a 5-10% fall. Plenty of places have already fallen more than that, and we're only 3 months past peak. Many other places aren't far off.

I said 5-10% fall in 2022 as my central prediction. I gave scenarios at the end of 2021, preferring these to a 'firm prediction'.

My second most likely scenario was a 10-20% drop.

Prices are about 5% down on average in the 2022 calendar year so far. Let's see what happens, but if I was betting the house on this I'd now be saying 10-20% falls are more likely.

So yeah perhaps about 10% down overall on average from November 2021 peak. Ashley Church and Tony Alexander are going to need to need the falls to stop soon, and reverse to gains to have any chance of their predictions of 'small gains' in 2022 being right :)

Funny how no one from the property "Bull Shirters" et al, has come on here to rebuke any of our comments ? .....interesting times ahead. ....*edit* whoops I was wrong - see above.....and now presenting for your entertainment ! ......"taking the proverbial"

what the heck happened to CBGB when he went to the basement to see his boys?

They're in the basement now, planning the next media spin "onslaught" as to how property will never actually decrease and "get in and buy now" ! .....it's never been cheaper ! ....with those immortal words "BE QUICK" !

Maybe he was too quick with the boys.

To be clear, prices in Auckland are falling across the board and not just in the lower quartile band, correct? I can't find a breakdown of the bands in the REINZ report

Totally anecdotal, I know - but this is from my own experience. I've been watchlisting everything for the last 2 years that matches my criteria on TradeMe. My watchlist has gone from hovering between 12 and 20 properties at any one time, to (currently) 47 - peaked at 50 about a week and a half ago.

Prior to January the vast majority sold on/about the 4 week mark, now I still have listings from November/December active. Other interesting observations:

- 7 out of the last 10 listings to drop off were not sold. 6 of them delisted (i.e. the listing withdrawn, and the corresponding realtor website listing just disappeared) and 2 withdrawn, then relisted as a "new" listing.

- 2 have gone from upcoming auction to PBN in advance of the auction date

- 1 has gone from upcoming auction to an asking price in advance of the auction date

- 5 have gone from PBN to an asking price

- 1 has gone from auction to PBN (after auction) to asking price to PBN (quite the roller coaster since listing on 12 Jan). Also fairly sure I saw it with "Under Contract" in the description for a while, but it no longer does.

- Properties that have been delisted very quickly disappear from Google search results. Unsure if this is just Google being efficient or whether there's some deliberate SEO massaging going on.

- Several price drops for those that have had an asking price. Very modest levels, but an indication of the direction that vendor expectations are heading.

All in all there certainly does seem to be a bit of a freeze going on. Lots of discussion here about the CCCFA, and interest rates. Very sudden, though, so my money is on CCCFA taking effect being the greatest driver. Shame we don't seem to have any good independent surveys/analysts to shed some light on the reasons.

A few years ago articles from Rodney Dickens would sometimes appear on this website, I quite rated him.

He's got subscription services on his website.

I would be interested to know what he thinks of it all.

The following graph going back to 1960s shows how far out of kilter NZ house prices (relative to the CPI) became after year 2000. Historically (such as in the 1970s) they have corrected under pressure from high interest rates.

See here: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Fthepolicyobservatory.aut.ac.nz%2F__data%2Fassets%2Fpdf_file%2F0005%2F78593%2FBrian-Easton-House-prices-relative-to-inflation-FINAL2.pdf

Big adjustment coming folks. It will likely play out over a number of years now that high CPI) and therefore high interest rates have become embedded.

Play out over a number of years.

Yes, similar to your slow descent :)

R-P .....and if you add the "world" situation into the NZ mix ??? ...... interesting times ahead.

While I think there are many on this thread that have never witnessed a real "property downturn" .....it ain't pretty !

The 80s/90s, the 90s/00s, the 00s/10s

Maybe you were out of the country when these happened

More to the point, where are you right now (what planet)? This money printing experiment has delivered us gains from the next life and beyond. Still you take it for granted - lol!Ip

From an investment perspective, interest paid on an asset that has just started trending down in value over the medium term is DEAD MONEY.

I just hope that property falls enough as food prices rise that one day I can say landlords and baby boomers could have avocado on toast if they hadn't been spending all their money on houses.

The 30 year (extended by the covid anomaly) property cycle is upon us now. SO WE CAN EXPECT 30 YEARS OF DOWNSIDE in nominal terms.

Time to be out of property before many head for the exit as inflation & interest rates & geopolitics grind you property folk down

That other equity investment - shares - will do the same

Cash & bonds are no good for the same reason

Hell looks like investors in general are in for a prolonged period of negative returns

OneRoof are a bunch of rear vision mirror viewing losers aren't they?

All sorts of DGM articles appearing there now.

Some of us on this website have been saying for quite some time that this was coming. So no surprises for us.

The smart operators have arranged their finances and investments accordingly, by late last year.

Here's my 2cents...

Watch USA interest rates, watch USA inflation.

Also the reserve bank should be shot. They have engineered this crisis.

And when the borders open all the young kiwis will leave. They will not be bidding for houses.

And final point.... If inflation is not brought under control, it will be very painful. Interest rates must rise above inflation rate to bring inflation under control.

A house is only worth what people can afford to pay. Everything else is speculation and greed.

10+ folk with Asian sounding names living in a 4 bed Mt Roskill leaker, and working at various Big Barrell's in the area will be able to pay the rent to own. The immigration taps will be turned to full in the near future especially if Luxman gets the gig.

Speculation and greed has been enabled by the governments and Reserve Bank / Treasury for the past decades.

People have been living beyond their means, confident they can do so off debts the following generations must pay. These greedy people cannot pay their own debts under their own steam.

Is this Govt on drugs, yes prices have come down. How will this help the first home buyers? Lending is still hard. another problem is investors, no investors no house to rent, rent goes up and then people will cry cant get rental. WHY? thxs to this Govt. The problem with Labour is they see the now, Which looks good but long term is a big disaster.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.