Auckland's largest real estate agency experienced a dramatic decline in sales volumes in April, with selling prices also dropping.

Barfoot & Thompson sold just 615 residential properties in April, down from 1107 in April last year. That's a fall of 44%.

It was the lowest number of properties the agency has sold in the month of April since 2008, apart from April 2020 when New Zealand was in a Covid-19 lockdown.

Conversely, the agency's stock levels are rising.

At the end of April it had 4845 residential properties available for sale, up 45% compared to April last year.

That meant the amount of properties available for sale on the agency's books was at its highest level for the month of April since 2011.

Selling prices have also begun to fall.

Barfoot's average selling price was $1,212,376 in April, down from $1,234,572 in March.

The average selling price is now $66,271 lower than its December 2021 peak of $1,278,647.

April's median selling price was $1,141,000, down by $99,000 compared to December's peak of $1,240,000.

Barfoot & Thompson Managing Director Peter Thompson warned vendors against having unrealistic price expectations if they want to achieve a sale.

“With buyer choice remaining excellent and economic conditions unlikely to alter in the short term, to be successful in coming months vendors will need to focus carefully on their price expectations," he said.

The interactive chart below tracks Barfoot & Thompson's main monthly performance measures such as sales numbers, prices and new listings.

The comment stream on this story is now closed.

Barfoot Auckland

Select chart tabs

183 Comments

Down..Down.. Down.. but not according to the Clowns...Clowns.. Clowns

Indeed. Be quick....to bail out a specuvestor clown...hmmm no thanks. How long will it take for many sellers to realise that last year is now a lifetime ago for the finance ponzi that underpins speculative NZ realestate. Lets face it how far should houses drop in value before the rentable income gives a 5x Dti.

Spec town get you pepto pills...your gonna need them

Let's call them VCMs - the Vested Commission Muppet/Vested Confidence Man.

aka Ashley, Tony, every agent, broker, developer, banker, MSM spruiker etc who denied the NZ property bubble, and thus conned people that it would never burst, and that prices would only go up (or flatten off at the top)

When the next housing market upswing comes, the DGM still won't own houses - and they'll be none the wiser. Many of them will have frittered away their money on consumer items such as popcorn. (That's what they tell us here.)

Property owners who manage their affairs prudently remain unphased. They know the security and wealth that property provides over generations.

TTP

TTP is having security and wealth and property that important to you, do you really enjoy life why not go out waste some of well earned wealth. You need to relax the housing market is taking tumble but you will be ok others on here enjoy other things like family, others who you call DGM would like to have own home with family but because they were born in different era than you have no hope in achieving this because investors and speculators like yourself have push price’s way out reach.now they have a little hope that house price’s will come back to reality you are running them down. Why don’t you sell one of your properties go on cruise or long holiday with someone you care for enjoy life have some fun.

When the next upswing comes (in 5 years) I'll be debt free and in a position to take advantage of the bargains that are coming up. Or down? Lol

The people who are going to hurt know are those whose lively hoods rely on clipping the ticket. RE agents... Mortgage brokers...

The sacrificial calf has been greadily suckling for one (or two?) two many years. But It's all grown up now.. and the hungry villages needs to eat...

yes a whole lot of ticket clipping, driven by so many profiteers making hay while the sun shines at the expense of people who really just want a home for the kids...unforgivable exploitation

FHB’s looking for the median priced home (if they could ever afford it!) just saved themselves $100,000 by waiting 4months…

Those who purchased towards the end of last year might have lost half their deposit already and could be facing negative equity this year if price falls start accelerating from here.

... if this continues , the next 12 months could be pretty stressful for recent home buyers ... doubly so as the Reverse Bank is forced to raise the OCR ... got my popcorn , plenty of popcorn ... Sit back & watch the show ...

if this continues , the next 12 months could be pretty stressful for recent home buyers

Extrapolating 1 month over the next 12 is from the Ashley Church / Granny Herald school of forecasting. I know what you're saying but let's keep it level headed.

A recession and rising unemployment could make things very interesting - but it will depend upon what the Fed do. If we go into recession while the Fed are still raising their official cash rate and inflation is still rising (for a period…who knows how long that might be sustainable for be the drop in demand brings deflationary forces)

Or those who re-mortgaged to release equity

But they still have the home they wanted, at the price they wanted to buy it for.

Homes have an intrinsic value.

I doubt many acquired their home at the price they wanted it for (or even the price they thought was reasonable) but instead at the price they were prepared to pay.

Perhaps were able to afford as opposed to wanted to, that price incidentally is not fixed but varies with the interest rate on debt. The price of that home in actual dollars to be repaid goes up with interest as the market price of that home goes down. Ouchy.

The intrinsic value of a home is not worth an infinite price.

Mashed intrinsic value on toast anyone?

"Let them eat intrinsic value"

Gold!

But they still have the home they wanted, at the price they wanted to buy it for.

Well yes. As Adrian Orr said, housing is a 'consumption good.' But to be honest, I think most people want to pay as low a price as possible.

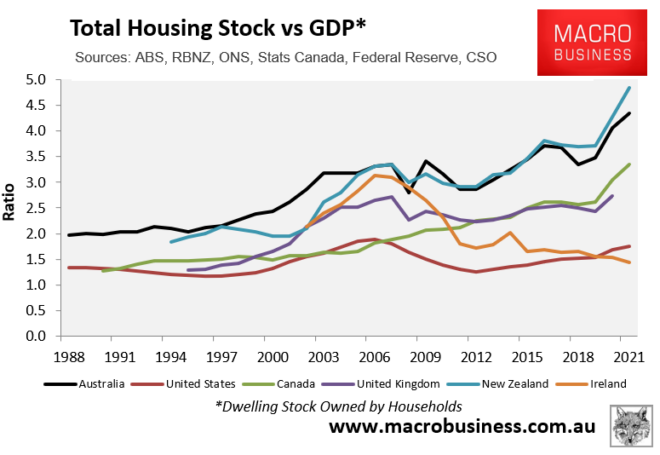

The intrinsic value of NZ homes, if we just look at fundamentals, should be at least 40% less than the current values.

please elaborate

Pick your metric.

House price to income ratio:

https://www.statista.com/statistics/237529/price-to-income-ratio-of-hou…

House price to rent ratio:

https://www.oecd.org/economy/outlook/focusonhouseprices.htm

House prices as a ratio of GDP:

https://www.macrobusiness.com.au/wp-content/uploads/2022/04/Capture-72-…

{kind=link}

Or you could just read a summary here:

https://www.macrobusiness.com.au/2022/05/new-zealands-housing-system-ea…

Great post. What a basket case we have created.

But they still have the home they wanted, at the price they wanted to buy it for.

Are you sure about that? This is only true when you assume no mortgage (or very low LVR). When deciding on the price those people were willing to pay, I'm pretty sure weekly mortgage payments were the key factor, and not the actual full price. Both from their and the bank's perspective.

If they "wanted to" buy a house for 800 per week and fixed their mortgage for just a year or two (like most buyers), then they could easily end up paying $1200+ per week come re-fix time. That's a 50% increase in the "price" they have to pay.

Very true.

Adrian Orr was complicit in making people think that rates would be "lower for longer". People really did believe that the RBNZ controlled rates.

If they had sold and repurchased in the same market, that is fine, for the first home buyers who purchased while the market was heated, that is a loss, how great is yet to be seen. If they had waited they could have saved themselves a lot of money. It has always been thought that property will appreciate value with in so many years, however, these are unprecedented times.

Agreed, anyone who bought in the last 6 to 9 months best case has no equity today (20% deposit).

I see a 50% chance of a complete bloodbath and 90% chance of a recession <2 years. I probably have one of the better track records here as well.

Now before DGM's get too excited you're probably going to lose your job, your rent's will go up and you won't be able to take advantage of lower prices.

Something for everyone there Te Kooti 😅

TK ....I have always struggled with this, as a landlord and a tenant, so can you tell me how does a landlord put up the rent, when the tenant has lost their job ?

Not sure I understand your question, in almost all cases I expect this occurs because their costs are going up (rising rates). There are good landlords who will help good tenants through a tough patch, and there are those that won't. Rents may go up in a falling housng market because potential buyers hold back and keep renting. Also, we are going to see developers pull the pin on new builds - that's going to hurt renters.

I was living in the states around the GFC times, back then rents dropped as people moved in with family after losing jobs, second houses or inner city bolt holes got rented out etc.

I would be suprised if landlord end up being able to increase rents enough to cover inreased costs.

Exactly

I think Landlords should put their money where their mouths are. All landlords seeking new tenants from now onwards should double the asking rent.

Since Landlord's costs are the sole determining factor in setting the rent price then they should demonstrate how easy it is to react to cost fluctuations. Since costs are generally commercially sensitive information, there's no need for them to justify their increases.

You would have thousands of renter just not paying, trashing property it will cost landlords more in long run government would need to put regulations in place to stop greedy landlords. Nzdan have you ever rented out a place as you are talking a load of bull.

He's being sarcastic, poking fun at landlords' idea that they can just raise rents as much as they want as they threaten when the government wants to makes rules for them that may increase costs, such as not allowing them to rent out unhealthy hovels.

Apologies if my comment comes across as bull, I'm just positioning myself on the extreme end of what landlords claim to be able to do.

What you have said highlights exactly why a Landlord's costs does not dictate the market rent, even if costs are increased collectively.

Tenants already don't pay and trash property, is this indicative of landlords overcharging?

Also those with spare rooms and struggling with increased mortgage costs start to rent those rooms out

Also there's a global skills shortage and people may decide it's the best time to leave NZ.

Precisely. I see council's use the same flawed logic all the time with things like building car parks. They work out their costs and then make a business which says we'll charge $x per day to recoup the construction costs over 25 years. Very little analysis on what the market is willing to pay. Similar here. Expanding supply means lower rents regardless of what the landlord needs to cover their costs.

Gosh you are sounding so much like me these days, apart from the rents going up bit.

out of interest, where do you see the OCR heading over the next 12-18 months?

The swap curve currently has the 90 day BKBM peak at 4.35% - this is why I have become so bearish so fast. If that rate hit's even 3% it's goodnight.

So do you see the OCR being cut by mid next year, after a period of hiking?

I don't think rates will get nearly as high as the market is forecasting, I think 2.5% will cap the OCR. There is a good chance they are cut.

You have to bear in mind the OCR was at 1% going into Covid and now, with less disposable income, it's going to 4.25%.

That's a bloodbath. Total ineptitude by the RBNZ (please don't blame Ukraine) and Treasury. CPI is far more about supply side and energy than demand pull.

This whole situation is a debeacle and the RBNZ is 95% responsible. Hugs and Aroha.

If we jump forward in time TK....and we quickly transition into a deflationary environment as demand drops....won't we just see central banks repeat what we did in 2020 (rate cuts/QE), which is what caused us to be in the current situation we find ourselves in.

So how does that even help?

And to be consistent...we must expect that RBNZ will very soon drop all LVR requirements...surely....if it was a sound decision then when prices were forecast to fall and demand drops were bringing deflationary forces, it must also be a sound decision now. If not, perhaps they should open up and say they made a regrettable policy mistake. But I doubt that will ever happen.

The OCR was NOT 1% going into covid in 2019. It was 1.75%, and had been at that level since the end of 2016. The first covid influenced cut (in May 2019) brought it down to 1.5%.

I totally agree though with your comments re: RBNZ/ineptitude.

I remember yield curves inverting in 2019....and then covid early 2020.

Really gives cause for Kiwis to ponder what house prices might look like without the abundant central government and RBNZ policy support over the last years and decades. They are high because they are made to be. A welfare scheme rather than a free market.

Im not sure your timeline is correct. 'Rona first cropped up in China, Dec '19 and was popping off worldwide around March '20

https://www.rbnz.govt.nz/monetary-policy/official-cash-rate-decisions

It had been at 1% since August 2019, Google is your friend.

Very similar to my views!

Te Kooti,

You and I seem to be in a very small minority. I am on record here several times saying just what you are. I have suggested that it will be no more than 2.25%.

If I am wrong and it does go higher, then that, in my view, will be yet another miscalculation by Orr and he will then have to reverse course rapidly as the damage becomes ever more evident.

Yes, I had noted your view. We should be out their receiving the swap curve....

Orr is finished. It was only 18 Months ago he was asking banks to prepare for negative rates, now we are looking at an OCR of 4.25%. He has completely lost control of the market. I notice the RBNZ are very quiet.

Agree that was Links position. Isn't the case you propose, getting to 2.25% and then having to retrench due to the car crash that will cause, simply underline the scale of the problem, that in that act would still avoid being resolved. More kicking the can so to speak. Would NZ not be better to allow the long avoided reset, and then quietly slip in a low DTi to stop this excessive debt speculation from reoccurring much like the Irish did?

I don't think anyone knows. But we can already see the exchange rate tanking despite the increase in rates. That's not an endorsement for NZ. It also means imported inflation has real legs.

They'll raise the rates until demand diminishes and to combat imported inflation and our dollar not totally tanking . It'll have to be at a premium on the Fed, who are signalling up to 3.

The sooner we enter recession the better off we will be at this point.

Ouch this is going to be extremely painful for many people.

Huge amount of people who want to sell but can’t at lower prices will rent them out putting more rentals on the market lowering the price.this housing market is going to fall and could take a 10 years to recover.this is just start rates are still emergency levels NZD is tumbling making inflation even higher. The people who thought rates were going stay low for ever or bought because of FOMO will be paying for listening to bad financial advisors, any one could see when prices get to 12 x average couple income the game is over.

I believe this is what you call a bagholder.

But many bagholders wont handle the rate stress and puke their positions.

Capitulation ensues

Now before DGM's get too excited you're probably going to lose your job, your rent's will go up and you won't be able to take advantage of lower prices.

Suppose that theres a bloodbath and prices drop about 50% to pre 'rona levels. Doesn't seem outside the realm of possibility given that interest rates seem likely to exceed pre 2020 levels.

The average house goes from around 1.1m to 550k, the newly unemployed DGM is 550k better off - its going to take a great number of years of being unemployed to be worse off, even if they have to go on the dole for a bit.

Love your maths.

Btw, while "interests => cost of debt => cost of unproductive assets" is a pretty direct relationship it is not the same for companies, not at the same level anyways.

If we have widespread unemployment, in any case, it would be a much easier case for UBI sustainers

Not going to happen. If it all turns to shit people want hard assets that you actually need not shit like Crypto. Many things could crash and burn before housing tanks significantly. Someone said here the other day 40% don't even have a mortgage so they will all just sit on the sidelines and watch the fireworks display.

Best case? LOL. We put down a little over 20% deposit ($400k deposit) and there's no chance in hell that our property has devalued by that much. It might later, but not yet. And then you go on to brag about your supposed 'track record'? You're out of touch.

When did you do that, where? I can promise you if you have to sell tomorrow you aren't getting that back. I'm no DGM btw, own multiple properties and will try and buy the dip.

I know of professional investors with 10+ houses who are now out of resi because of interest rate deductability. There is no investor bid on the way down now.

Agreed, the resi rental investor business model is done for the moment until housing costs come down a long way. Which is the intent of the new legislation, bad for the resi investor (I am one as well) but actually really good for FHBs.

Good to hear the new regulations are having the desired effect - maybe we can stop the madness.

Until Luxon and co win the election, he's planning to repeal those regulations, affecting his bottom line too much.

That's a real risk. Imagine running on a platform of trying to increase the price of many households' main expense, and not being laughed out of the room. Bizarre.

There's a lot of entitlement mentality out there and Luxon's talking directly to it.

As a investor sometimes you lose hopefully you made plenty on way up and have cash on hand as in next couple of years huge bargains to be had in housing market the only thing could be government could put regulations on market so this doesn’t happen again.

ah so you're one of those people my hospital cleaner friend is paying the mortgage off for TK...she cleans up peoples vomit at midnight...and when she ends her working life she's paid of your mortgages and has nothing...shameful kiwi exploitation...you should share any capital gains with the tenants of your houses, 50/50...

Probably not 20% in most cases, but probably 10-15% down from peak in many cases if you were to look to sell now.

So you borrowed about 1.6 mil for a 2 mil property. What interest rate did you fix at and for how long?

I split it multiple ways, but heavily weighted in 4 and 5 year terms. We can comfortably afford the payments. I plan to pay at least an extra 50-100K per year on top of that.

.

Sadly its true for the DGM's if you think your screwed now its only going to get worse, that's just the way its been happening for decades. Thinking your somehow suddenly going to get ahead by someone else's misfortune is a mental illness. You have to slowly improve your own life and those that are around you not try and drag everyone else down to your level.

"Thinking your somehow suddenly going to get ahead by someone else's misfortune is a mental illness" So you don't like landlords then?

Haha exactly - the landlord/property investors who all 'got ahead' did so at the misfortune of younger FHB's up until now....

The hypocrisy of the comment sums of just how out of touch with how many people are in society. And the inability to see issues from multiple perspectives and draw relevant conclusions.

yes...landlords should be required by law to share any capital gain 50/50 with the tenants...they pay the mortgage after all...otherwise its just more money making money which is why we left Europe in the first place...to ditch land lords

Carlos People would just like to purchase a house at 3 or 4 x income how is that DMG thats the way it was until idiots started bidding up places turning housing market into a Ponzi market, well it over now and people who were scammed will lose deposits and be in negative equity for years let just hope government put into place a law where house prices can only go up by inflation.

You have to slowly improve your own life and those that are around you not try and drag everyone else down to your level.

How great it would be to see NZ reward that slow hard work rather than just enabling wealth transfers from the poorer and working folk to wealthier asset owners. It should not be that we enable investors by dragging other working Kiwis down.

absolutely right, its immoral scumbag behaviour...endorsed by politicians who also have snouts in the trough....

But DGMs might have savings, during a recession, cash is king. And those investors who got out of the market before the price had peaked. They have money too.;)

Exactly right COH, I know of a few people who are cashed up, they have existing assets as well, and are waiting on the housing market to come down. Don't think everyone is shaking in their boots just because some of their assets have slipped in value. Of course there are the other ones which many people commented on here already.

"I probably have one of the better track records here as well."

You could possibly get a column with Granny Herald then

Oooh im excited.... The air is electric with impending opportunity.

Yep - first 5 years of principle payments gone, and debt remains the same.

It will be the first 10 years of principle payments gone by xmas (about 20%, maybe we are already there) - and debt still the same.

And cost of debt will be 2x (maybe 3) to service.

Anyone (always a VCM) that say's timing the market is not important is only talking about equities and dollar cost averaging where you have no debt leverage.

We're heading back to the good old days - look at 100 properties, make low ball offers on 10, maybe get 1.

Make money the day you buy.

But the time to buy will be when interest rates have stopped rising and you can calculate your cost of debt servicing - so who knows when that will be.

Surely we are now past denial phase, entering bull trap?

Yes but this time the impact will be very real (actual, significant increases in mortgagee sales and attendant bankruptcies) and given the too-big-to-fail nature of the market and the over-weighted book in residential loans for our Aussie banks the Govt de jour will unwind some of the moves made to control house prices. I think this will not be enough and the exercise of messing with policy so quickly will make investors stay out until the dead cat bounces.

They "saved" a hundred grand, but they spent it again on the interest rates.

That $100k saved offsets the interest payments. It has the opposite effect of this suggestion.

So in reality is $100k plus any compounded interest on that $100k over the entire loan period: saved.

Not necessarily. If you have a $1m mortgage and an interest rate of 3.5%, you will pay the same monthly instalment as if you had a $680k mortgage at 7.5% - based on a 25y loan p&i.

You are only better off on the smaller mortgage if you are able to make additional unchecduled principle reductions. Otherwise, it's just the ratio of money going to principle or interest that is different.

The problem is for those who got a $1m mortgage at 3.5% and find themselves rolling over to 7.5% a couple of years later. Starting your 25 year mortgage a couple of years early doesn't materially change the average interest rate you will pay over the term - much better to have bought at the peak in rates and trough in prices (obviously much easier with the benefit of hindsight).

I guess my point was more focused around the fixed term rates ending and the low interest rates on that $1m mortgage dissolving into the real world of rates.

Once all fixed rates of the past two years have rolled over (in the next ~3-4 years) and both examples are fixing at a similar rate, who would be better off?

Let's say interest rates leveled out at ~5-6% in 2025. Entirely possible. A 2020 FBH fixing 3% for 5 years coming out of their term may have paid ~$100K off their principal loan at $1K/week. The one who waited, paying 7.6% interest. Sure that $1k would be entirely interest on a $680K loan. But they are now on a level interest field as the 2020 buyer with 220k less principal (900k vs 680k). Who would you rather be?

This example is a ~25% price reduction assuming both buyers have the same deposit of $250k (20% deposit on that $1m mortgage). $1.25m -> 930K.

Sort of, lost say 10k in rent another $500 in interest rates in a month but sure, if they are buying in a suburb that has seen decent drops. (many have not) Wait another 6 months, put another 10k into a landlords hands maybe another $500 a month in interest rate fixed rates.Sadly not really a win for FHB to be honest

Luke83 what are you taking about people would be crazy to buy when prices are losing 25k a month and will be accelerating fast in downward direction for years.

Don't worry a Mr Ashley Church or one of his sidekicks, will be along shortly to allay all your property fears....... nothing to see here, move along and go back to your comfortable lives, leafy suburbs, well paid jobs, MSM news, Mike Hosking and those of a similar ilk.

... Bayleys ... Propeller Investments ... all the spruikers selling the " property doubles every 10 years in NZ " line ...

Time for a Tui : " Yeah , right " ...

In the Church of Ashley: "Let us pray."

And all the overstretched people said, "Ramen".

Hutt Valley Market Update W/B 2nd May

The number of houses for sale is starting to trend downwards with the peak reached of 670 houses on the 11th April. Didn’t quite get to my predicted 700 houses.

Meanwhile the number of houses for rent is starting to rapidly increase – with over 200 listings this is double this time last year when just 105 houses were for rent in mid May 2021.

Current Market Listings

646 houses on the market- down 2 on last week

Based on the REINZ data which showed that 96 sold in Feb and 104 sold in March giving an average sale of 25 houses per week– 646 houses means there is 26 weeks stock on the market.

House Price Reductions

303 houses have a listed price

53% of the houses listed with a price have reduced their price since listing

The average markdown has risen this week from 75K to 83.5K.

Of those that have listed prices (pool 303) 32 have reduced their prices by 100K (last week this was 24 properties)

6 have reduced their prices by over 200K with the biggest reduction been 350K (a total 20% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 648 listings is now 849K. (Steady on last week)

Most sales on the market continue to be at the 800K-$1 Million mark. The bottom quartile is still sluggish with very few sales. The top of the market ie over $1.5M (currently 47 houses listed) is also sluggish with the last few weeks only 1 house a week selling in this price bracket.

Houses sold vs houses removed

My records show 136 houses listed with a Price have sold YTD (up 6 from last week).

I have records of a further 107 houses (up 9 from last week) that have been removed from the market unsold YTD.

16 of those houses removed from the market have been listed on the rental market

The total number of houses removed from the market in the last 2 weeks is 21 (this compares to about 5 houses delisting a week over the previous 14 weeks).

The increase in the number of houses delisting is to be expected in Wellington where owners with cold damp houses try to avoid selling over Winter when this problem becomes quite noticeable. I am expecting more houses that listed in the peak of summer will be considering coming off the market for winter and relisting in Spring (for those sellers who can afford to).

Length of time on the Market

Given how slow the market now is – I’m adding a new Length of time – which is houses that have been on the market for over 90 days- effectively these houses listed in 2021 and Jan 2022 which remain unsold.

- 463 of the houses have been on the market for over 30 days - 72% (last week it was 447)

- 292 of the houses have been on the market for over 60 days - 45% (last week it was 297)

- 181 of the houses have been on the market for over 90 days – 28% (last week was 162)

The number of houses on the market over 90 days is creeping back up again – 90 days means these houses all listed before Feb this year – so in the peak summer and spring season – so having 1 in 4 houses unsold from this period is rather surprising.

Whilst I haven’t seen the latest time to sell numbers for the hutt valley – ¾ of the market has been on for over 30 days and with half the market on for over 60 days – you would estimate average sell time is at least 50-60 days at the moment.

For those thinking of getting a bridging loan when buying you would need to be calculating the costs of maintaining the loan for at least 3 months – 60 days to get the sale and then a further 30 days to settlement.

Rental Market

Meanwhile the rental market has 202 properties for rent (up 14 on last week), and 97 on this time last year – when just 105 houses were for rent.

Average rental price reduction YTD is $50 a week (up $2 on last week) and 40% have dropped their prices since listing.

As noted last week I have also been noting how many properties are listed for rent over $650 a week.

At the moment the percentage of properties listed at $650 fell this week to 43% - last week it was 45%. This is the lowest percentage of houses over $650 since the week of the 20th Dec when 42% houses listed were over $650.

Since then ie between Jan- March over 50% of houses were listed for rent at $650 or greater with the peak week been the 19th Mar when 54% of houses had a rent > $650.

More houses are coming to the rental market but at lower prices which would indicate there is an oversupply of rentals starting to develop in the hutt valley

The Wellington rental market may be the canary for house prices in the region. I'll admit I predicted the rental market would spike as prices fell but with the sales market as dry as it is people are scrambling for cash flow to pay the bills - moving their sales to rentals. It's looking more and more likely that there is/will be an oversupply of rentals and that prices could fall just to manage cashflow woes with rising interest rates.

It's becoming less and less plausible to simply raise the rent to cover the cost.

Ikimpaul Thank you for this detailed info

The downward trend looks almost vertical at this rate house prices are going back in time faster than the Tardis, this is with interest rates still close to emergency levels.

the govt should loosen policies to allow investors in and outside of NZ to buy properties and save the price collapse.

No.

Why would NZ want our houses to be more expensive?

Entitlement Mentality

xingmowang ....then even more people, that have lived here all their lives and want to stay here, won't be able to buy a home, as prices will just increase. We are not a dumping ground for an overseas investor's surplus cash.

I think our resident CCP troll might be looking for a bolthole or two for his kleptocrat overlords looking to escape the polluted, corrupt, autocratic nightmare that is China today.

but I was pleased to see the CCP sold Waste Management to an Aussie outfit

Honk honk 🤡

Xing, your last months posts have been good and thoughtful. This post is not.

NZ has added a million or more in the last ten years. No one voted for that, or elected politicians to make it happen. In fact politicians were elected to make sure it did not happen, and then completely failed on their election promise (WP). Now that everyone is full aware of the negative impact of over populating NZ without sufficient infrastructure and housing prep, no one in their right mind wants it to do it again. Accepted property speculators probably do, because they see this a a way of being bailed out of the high levels of debt they carry. I note they are a small group overall, with only one vote each. Personally we cannot do another million without properly preparing for it. Transport, schools, hospitals, housing, council services etc etc.

Interesting, the loudest voices I regularly hear against further mass immigration all arrived in the last ten or so years.

Why does China not allow this X?

nah. All that eastern cash can stay over there thanks. News im seeing from China aint flash either. You think we've got a property bubble. Lol. they have Mount Everest.

Surely I’m not the only one who looks at 99k and realises it was actually into six figures and someone backwards engineered a plug in the spreadsheet.

x.9% inflation!

What? Are you questioning the integrity of a real estate company media release?

I just don’t like people taking the piss. Sick of these .9s and sticker pricing techniques.

If you remove enough "outliers" from the dataset, then you can arrive to a desired result.

pffft please, that sounds like hard work, just change the measures mate. Just change the measures to measure anything you want (CPI) and apply it to a base case that can no longer be relevant. Easy.

Vendors won't be asking a high price for an old house now.

At least Rocket Lab are catching falling stages - well done!

They should catch their share price as well because I'm down 40% on RKLB :)

Ouch..house prices might match that at the end of the year?

Not sure if i am allowed to post this link or how accurate this data is but it makes for an interesting visual perspective of the madness https://www.reddit.com/r/dataisbeautiful/comments/ugn6mu/oc_house_price…

Wow,.....we are no1, but what a looser race to win. Good for bank profits though.

Wow. Just wow.

The best part is NZ is never out of sight and it is shame for Govt who ruled this country for the last 40 years.

Having the worlds most expensive houses is a good problem to have right? And we want prices to continue to rise from here, because nobody wants the value of their primary 'investment' to ever go down...

I think politically and financially we are in a bigger pickle that many realise or are currently willing to admit.

"Good problem to have", "sign of our success" - Bill English.

"Wealth effect" "lower for longer" - Adrian Orr.

Great link thank you. Comments in that thread show general alignment in NZ posters (turn us over we're done) and Int. posters (thought I might consider immigrating but now I would rather set myself on fire).

Once upon a time, not so long ago, there was a little country called New Zealand.

And they thought they were different.

The end.

Question is, what more welfare money can the RBNZ and government pull out of the hat with which to keep house prices up once more?

While there are plenty of factors continuing at the macro level with the ongoing war, global economy stresses, climate impact and covid, NZ has been relatively resilient. Within NZ there are many that will jump on the 'doom and gloom' bandwagon based on their perceptions and experiences. There is no doubt that 2022 will be a challenging year, potentially devastating for some. However, there is also room for optimism.

NZ in my opinion does remain an attractive country to visit linked to tourism, it is essential that immigration settings are partially relaxed to allow the needed workforce into NZ that enables the long-term work on infrastructure and housing, increasing productivity that is enhanced by technology, significant improvement within the education sector, and that research and development occurs and is ongoing. Yes, our labour force will move to greener pastures (in higher numbers at times), however, the majority will eventually return home...because there is no place like home. Employment remains high and at record levels. New Zealand, a young country, continues to grow and the current period we are in, is one of significant changes Globally. The housing market is declining/falling, but I don't think there will be a sustained crash that some are saying will occur this year. I just don't see average or median Auckland prices going under 850-900k ever. In the north and south areas of Auckland, there continues to be significant development (long-term) with Milldale/water/Wainui and Papakura/Drury/Pukekohe.

Peter Thompson's after dinner speech to his agents in December 2022.

Many of you guys have still got it wrong. Housing is a long game, you don't care about the short term paper fluctuations if your already in a house. What you do care about is the outgoings to keep it and the only real problem is the interest rates. Rising rates are going to be a huge problem for the marginal buyers who extended themselves to the very limit, those that can still afford 7% rates are not going to be the ones forced into a sale. Nothing really changes in reality only the width of the chasm between those with and without a house.

roughly 40% of homeowners do not have any mortgage.

Do you consider the interest only seminar worshiper, leveraged to the absolute max on sub 4% to be a "marginal" buyer?

Long or short-term game an intelligent investor will always buy bottoms, not peaks.

Now if someone bought in last one year and lost all equity and paying high-interest rate will always feel it was his life's biggest mistake and will try to sell as everyone doesn't have the power to control emotions and hold and wait for the next bounce back which dosen't seems possible in next couple of years until Inflation drop to 2%.

Carlos how long is long game ?

10 years to when you house price has doubled.

What if in next 10 years house goes down 50% and you have been paying mortgage at 7% and lost you deposit and still in negative equity. Could be another 10 years till you show a paper profit, Carlos are you still happy with your lot in life because this is more likely to happen.

Something something prudent smart investor yada yada yada

Well Carlos if the current system allows unlimited printing of FIAT you will get Inflation. One of the ways to control inflation is to set an appropriate interest rate - currently we are way behind the curve (we as in World). You cannot have it both ways - so whether you rent or own the dye is set. Luckily on the horizon is a solution to the pump and dump...stay tuned!

Been here before. I can still remember when the comment section was much quieter during 2011-2014.

When things went down hill during GFC, it slammed everybody not just home owners. Those who managed to hang in there and made it through the tough times know how the game works.

Back in 2003 no one dare to think the house price will double and it did. 2012 a friend put his house on the market and it took nearly 3 month for a buyer to show up. The market was “very quiet”. At the time I thought to myself “can the house price ever go up again?” I honestly didn’t think there were any room for any price increase and things started to pick up again in 2017.

Do what right for you. “Short term” is the name of this “Long term” game. Price and interest rate go up and down. You know you’ve made it to the other side when price fluctuation no longer concerns you.

This is nothing like anything anyone has ever experienced in their lifetimes....unless you can point out another time with similar characteristics....and the GFC isn't it...

“This time” is always different.

I've been around when interest rates were over 15%. I was working, but only 16 and it just passed me by.

This is different from 2009 for one reason - asset prices are so out of kilter to average wages.

I had a house that i bought in 2008 for 420k with no deposit. It crashed 10% within 8 months. I was on about 80k got in two flatmates and easily paid the 8% interest rates at the time, including some principal

A person or couple in the same boat now would have a 1m mortgage, paying 50k in interest with far higher life essential costs etc. Wage before tax maybe 110k. If you include dependents it's completely impossible.

How this ends, who knows - but it's going to be difficult. I really don't think that the employment rate is going to be able to keep things propped up.

But it's as necessary as cutting off a foot to stop gangrene and the sooner we get into this the quicker we get out. I'm heartened that it is accelerating.

Personally sold my home in January taking a hair cut. Almost nobody on these boards could see what was happening, which I find perplexing. But we're all mostly on the same page.

My settlement date is end of September. At this stage the plan is to rent for up to a year after that. I'll be walking away from some good rates but it's going to be worth it.

Yes but back then they dropped the OCR and mortgage rates fell around 5%.

This time is different.

When it hits the fan they will drop the rate. Now is like pre 2008 when rates were steadily going up.

That’s what people said last time.

Thing is “we” human are doing all these “different” things.

The Atlantic Financial Crisis wasn't even particularly global, and New Zealand barely got touched.

The only reason NZ got a whiff of it was because everyone overreacted. I was working in retail at the time and I remember it was a convenient excuse to freeze wages (not enough money in the "kitty") while the owners carried on piling money into expanding the business.

And getting rid of rubbish employees

Yep history pretty much just keeps repeating but many still cannot see it. Just when you think house prices cannot possibly get any more expensive, 10 years later the price has doubled.

This is a phenomenon that is particular to a few countries over a few decades coinciding with an systematic reduction in interest rates which appears to have run out of steam. I do not have much confidence in it continuing.

The burn on those who have bought into significant debt over the last two years will last a life time. Rising interest rates will force these people into bankruptcy. That is a lifelong challenge. For wanting to own a house and being born at the wrong time.

Don't get me wrong the force 10 victim mentality of a few of the posters here is abrasive (and generally disrespectful to those who actually are victimised) but in this case we are going to get a real set of very undeserving victims.

For those who believe in technical analysis of price charts (which I don't, but still find fascinating), the price chart here is showing a very nice 'Head and Shoulders' formation, which is a signal of bear market.

https://www.investopedia.com/terms/h/head-shoulders.asp#:~:text=A%20hea….

The best part of technical analysis of price charts is it's easy to see once it is formed but it's not that easy to predict. :(

Yes our housing market appears to be highly positively correlated to the US share market.....and yet many property investors say they won't touch the sharemarket because its too risky....but instead take leveraged positions on something with the same characteristics as a speculative sharemarket...

The only metric that counts when assessing value gain/fall is the resale of a property within a specified time period with no physical change in the interim. Constant talk of medians/means/quartiles/volumes/inventory and worse - anecdotes and 'expert opinion' - are both malleable and unreliable.

Fake news they'll say..

Interesting times for sure, FHB will be the ones to be burnt when the bank owns 100% of their house. Investors will cut the loss early or ride the wave.

Legit question - if you were a prospective FHB in Auckland, how long would you be waiting? (obviously crystal ball gazing, but genuinely interested in opinions)

Spring ....2023

There are two very important things to consider when buying a house:

1. Have an idea of what kind of house you want to live in (including location), and

2. Have an estimate of how much you'd be willing (and able) to pay per week.

These two things matter more than anything IMO (assuming you're buying a house to live in, not for speculation). Once you have #1, you can check the current median price for that narrowed down segment of the market. Then look at the interest rates and calculate your weekly payments with the current rates. Does that number look good?

Also think about what happens if the interest rate goes up. Do the numbers still look good if it goes up 100bps, 200bps, 500bps? If you'd go broke in case the mortgage interest rates went up 500bps then don't buy. Otherwise go ahead.

Now to answer your actual question, it really depends on your circumstances. If the equation above looks good for you today, then you waiting instead of buying is basically speculation. When the market will bottom out is anybody's guess... I'll start looking at the end of this year, but it's possible that the actual bottom is more than 2 years away.

I lived through the GFC and price drops in the USA....you'll know when its time to look at buying....because the spruikers (likes of those on this website) go quiet for months on end (6 months +), or will even come out and say that now is a bad time to buy.

So if CWBC shows up here again and starts saying that now is a bad time to buy, then its probably a good time to think about buying (because they are trying to talk the market down so they can buy themselves....such as they were talking the market up previously so they could maximise their profit). When the wolf in sheeps clothing, changes his/her clothing, then you know its time.

For me, looking like probably 3 years from when the market started to fall, so spring 2025

Be careful what sort of advice you get here... As you can see in the comments section it's dominated by DGM and isn't very balanced.

Is that sarc, or not? You seem to have a curious mix of DGM and pro-property mentality, I can’t quite work you out :)

Agree one minute the world is ending next minute anti DGM.

Won’t take long until we gain another half million in population. It is amazing how small we are in terms of population compare to the rest of the world.

Some left NZ and had to come back for various reasons have lost their spot and realised that things are longer the same.

The next 3 years or so provides a good window to buy while everyone else is focusing on overseas travel and new immigrants staring to gain momentum again.

Yes that and house prices double in price every 7 years so by 2020 the average house price in NZ will be about $2,000,000.....be quick before you move here and can't afford to buy or survive.

A lot of people can, often I see people around and think how come they got so much money.

People who can afford will move here those who can’t will move out. Look at Auckland.

Each to their own - I think Auckland has gone downhill substantially the last 20 years....

the 09 peaked mid '90's IMHO - good times, but hey they never last

If inflation keeps high in 10 years you’re house will be worth 1.2 million but loaf of bread will be $30 average wages 350k $25 litre petrol.the only item the won’t go up is house prices as already so over valued.

My comment was 100% sarcasm but I think small kev the spruiker thought I was being frank with him.

Don’t think McDonald’s has ever dropped their price on their meals, for some reason people still lining up at the drive through.

How much for a Big Mac back in the 80s?

In a comment on this site eight weeks or so ago I commented on how my daughter had been beaten by Auckland buyers who put a conditional offer on a property where I live. They have never visited the property to this day. Two weeks ago they withdrew their offer as they had not sold at that point. Subsequently she has bought the property which is near new and is more suitable for family life than her current one. When she missed out another agent told me she would eventually get it and he was correct. He knew more than me. The Auckland market had obviously turned for the worse.

"April's median selling price was $1,141,000,....".

It may be down but how many can even afford a loan of $850000. Weekly mortgage will be between $1100 - $1200 and may go up by couple of hundred dollars more per week.

This media selling by itself, does not help FHB but is this is just the beginning of the trend than is excellent news for FHB but should wait as should not try to catch a falling knife.

What percentage of the housing market was bought and sold in the last two years? Whatever that number is, that will be the limit of the damage and only if they need to sell. The majority of people can sell at today's market price and be quite happy. It is true that some made an absolute killing and some were suckered by the price spike last year. I was just quoted to replace a shower - quotes were $4500-$7500. Nothing is cheap in New Zealand!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.