The decline in house prices that began at the bottom of the market is now spreading to top end properties as well, according to property valuation and data company Quotable Value.

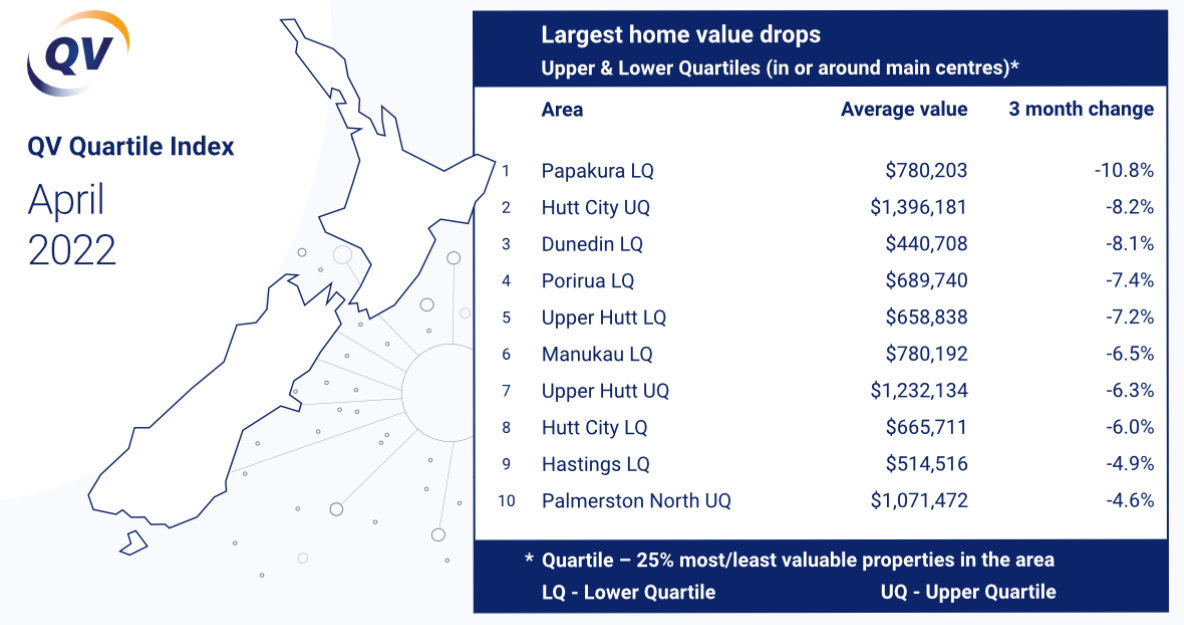

The QV Quartile Index tracks housing values in the upper and lower quartiles, that is the bottom 25% of homes by value and the top 25% by value.

It found that across New Zealand, the average value of lower quartile homes declined by 1.7% over the three months from February to April while upper quartile homes declined in value by 1.2%.

QV General manager David Nagel said its was the first time since the pandemic lockdown in 2020 that upper quartile homes had posted no value growth whatsoever, while lower quartile values posted their first decline in more than two years.

"It appears that what began as a tightening and then a reduction at the more affordable end of the market, predominantly as a result of rapidly rising interest rates, affordability constraints and a significant tightening of lending criteria, is now beginning to impact on home values much further up the property ladder," he said.

"Although seven out of 10 of the biggest declines in home values still occurred at the lower end of the market this quarter, what we're seeing now is a growing number of main centres experiencing declining values at both ends of the market."

The biggest declines in values at the top end of the market were in Upper Hutt, where the upper quartile value declined by 6.3% in the April quarter after averaging similar levels of positive growth for the previous four quarters, and in central Auckland, where upper quartile home values declined by 3.4% in the three months to April.

The biggest declines in value overall were in Papakura in south Auckland -10.8%, Lower Hutt -8.2%, Dunedin -8.1% (the table below shows the biggest percentage declines in value.)

"The first four months of this year could not be more different to the last four months of last year," Nagel said.

Back then, none of New Zealand's main centres were showing any declines whatsoever.

"Now most of them are, with the few exceptions, most notably Whangarei, Christchurch and Invercargill, most likely to join them in the coming months."

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

65 Comments

I guess we start calling QV doom globins as well now?

But from my perspective, a return towards historically accepted price to income ratios (and debt to income ratios) is good news for the country both from financial and social stability perspectives. I don't see this as doom or gloom, but instead a positive. Its an opportunity for younger people to get established and have some hope of future prosperity in NZ. The last 10 years or so, that hope has been eroded and for what benefit? People don't appear happier now than they were 10 years ago. If anything its the opposite. Perhaps the doom and gloom is here already and its because of overpriced houses and the associated lack of social cohesion that has caused.

... we risk losing a chunk of the younger generation , what hope do they have of ever owning a house in NZ ... opportunities overseas will draw them away , better wages , cheaper houses , cheaper groceries ... why stay here ?

We will be fine, we can export all the commodities we produce and let the population eat cake..what's not to like?

Due to globalisation and the world wide appreciation of asset prices to induce the wealth effect, there will be nowhere to hide from the inevitable clusterf#&ck.

Financial adventurism has reached its limits and we will require another planet to consume if we want to “grow” any more.

The game is up. The physics of the situation is inescapable.

B-b-but apparently we can grow things in moondust?!

I believe the correct term is regenerative.

High house prices have been devastating to the younger generations and hold back the economy as one essential good takes up more and more of our focus.

I'd celebrate cheaper houses in the same way I'd celebrate cheaper food.

Amen to that.

3.4 percent is not exactly a staggering proportion...... especially for 4 months.

The tight labour market will prevent the downturn from making the housing market the bloodbath that so many doom goblins here fantasise about.

The long-term issue is not how slowly and infrequently house prices fall - but how quickly and frequently they rise. (But you already know that.)

TTP

Lol - the tight labour market is more evidence for the RBNZ to keep raising rates....which is what is causing house prices to fall.

You should be praying for deflation and rising unemployment TTP as those are the factors that have given reason for RBNZ to keep pushing the OCR to zero and to save the housing market/asset prices 2008 - now.

In this odd (fake) financial world we have created the last 10+ years, it is bad news, not good news that has resulted in high asset prices.....that is in order to avoid deflation and rising unemployment the central banks have continued to reduce the cost of capital/debt so that future cash flows could be discounted using smaller and smaller numbers each year....resulting in even higher asset prices.....so high asset prices were and indication that things in the economy were getting worse not better....that is pretty messed up right? And oddly now that things are better (lower unemployment) they will start lifting rates in order to increase unemployment back to the maximum sustainable level....which will increase the cost of debt....which will reduce asset prices....how bizarre....

In an ironic turn of events it seems as though the investor market is dependent on the FHB market to compete for house price inflation. Not going to regurgitate the same statistic response I gave to this similar comment over the weekend, however a combined 40% drop in volumes over these two control groups speaks a lot louder than what the remaining buyers still believe they need to pay.

Only an ostrich would confidently predict an aggressive rise in house prices over the next 2 - 5 years, hoping for an uno reverse virtue signal from the government or RBNZ any time before inflationary pressures ease is an interesting game to play. The obscene height of the bubble gives us all a slow motion playout similar to a spaceX landing. A risky return from space.

I love that TTP is still here, it means we still have a long way to fall. When he stops posting, then we have to wait another 6 month minimum for the cycle to bottom out. That's when you buy back in. We need every property perma-bull to capitulate, then you know the bottom is in.

I think he's the only perma-bull left commenting on this website?

Or maybe Carlos is in that category too.

Oh how we love our little perma 🐂💩'r

You might find it enlightening to go and look at how Housing bubbles in other countries have deflated. In the US house prices were falling at less than 1% per month for the first year. The rate of falls never exceeded 1.8% MoM.

In Ireland it was similar. Prices flattened for the first few months, followed by falls of just less than 1% for the next 6 months and eventually MoM falls peaked at 2.9%

In 4 of the last 5 months NZ has seen MoM falls of 1% or more. Prices in New Zealand are falling considerably faster than than two very severe housing bubbles at the similar time from the peak of the market.

NZ:

2021-12 -1.0%

2022-01 -1.5%

2022-02 0.5%

2022-03 -2.1%

2022-04 -1.9%

that is good insight, i never realised that. So its a slow burn kind of thing that just grinds away.

Great insights

The stars are aligning for a significant downturn in the New Zealand economy and property market. A perfect storm is an understatement given what is unfolding with the global economic and geo political situation. Obviously anything can happen and conditions can change but if these trends continue expect far more downside to come for Auckland property. Many property markets globally were in bubbles pre Covid and the reaction of Governments and Central banks just blew them up even larger. It will be interesting to see if they can gently let the air out or keep these bubbles inflated but right now it really does look like their hands are tied.

Tell him he's dreaming ... am referring to yourself Adam

significant downturn

I haven't said it is set in stone but that the stars are aligning for one. All depends on how our Government and Central bank reacts and many other variables in the global economic and geo political situation.

The changes in last weeks budget were quite clever. Designed to give the market a kick pre election 2023. That is when interest rates will get their first cut. By then 875 K will probably buy you something reasonable in Auckland and 925 K in Wellington will be viable as well. Potential buyers should be using the next year to position themselves for maximum advantage. Keep renting and try to moderate expenses to save some income. Make sure you can align with the first home buyer income caps when the time comes. Devote some time to open homes and auctions over the next year to get a good idea of what properties are actually selling for. Wait for the signaling of the rate cut then move on the property you want. The first year or two will be hard. But the government is going to give you 10K towards your interest payments. 5% deposit is doable if you have some reasonable Kiwisaver money to contribute. I hate the way the property market is manipulated for political gain in NZ. But that is not likely to change anytime soon. 2023 may be the last chance to get a house before prices start to move up again. Don't expect 20% per year ever again. But 5%capital gain is enough to eat most of your interest cost and you have the security of a home you cant be asked to leave with 90 days notice.

What a great perspective, save for two ??? years to 5% deposit then extend yourself as much as you can and slave away for 30 years to repay the banks.

Then after that you can die all good, but at least you have you name on the house ownership paper.

44 K would be the deposit for an 875 K home. A couple with 5 years of Kiwisaver each can use that plus 10 K grant for the deposit. There will be a temporary glitch in the matrix to allow a couple who don't have well off parents to take advantage of the 20% market correction by Q2 2023 and buy a first home. No one is forcing anyone. But the chance may never come again. A lifetime of renting is the alternative.

Maybe for some, but it’s going to take big household incomes to service 820k mortgages at 5% plus

Westie the fall of house price’s will be a lot more spectacular than 875k for reasonable house in Auckland you will be looking at 450k for a 3 bedroom house. If the world does goes into a recession bigger falls will occur as assets depreciate.

A big part of the falls will be inflation not actual price.

This would be be an ideal outcome, as long as inflation reduces the debt burden before rising interest rates become a significant burden.

Agreed... you can bet that there will be those who bang on about negative real returns.

Same as the 1970s.

We are approaching the capitulation phase of the bubble, which will be brought on by the 50bps rate hike. When those 60% of all home loans refix at 6% the unwinding will happen. Whether the powers that be decide to step in is the question now. Be quick.

Yep agree. Still tonnes of mortgages to be written this year, and many of those, from next week will start with a 5.

prices to drop at least another 5% over the winter months

Agreed. Stagflation and 6% plus interest on debt...

Yawn 1.2% to 1.7% percent falls, its obviously a crash. Unless the RBNZ cranks the OCR another 2% at least the effects are going to be minimal.

Thanks Carlos you never fail to disappoint in the comments section.

Still early days. I'm hearing about a lot of properties in Auckland already selling for 200 to 300k less than what they would have achieved in the 2021 peak.

It's impossible to really know but I suspect those reports are correct.

This isn't an honest assessment out of QV. I have a private python model tracking current price on TM and RE, which is cross compared with sale data a month after the listing is removed.

The data is messy, but lots of these sales are -10 to -20% or more below the asking prices more often than not. You don't eat that sort of loss unless you are desperate to get out. As far as I can tell, the remaining people in the market are trying to buy after selling their existing properties. The volume of sales is down massively.

Asking prices on TradeMe have only recently come back into vogue though, pre-Christmas almost everything was going to auction so there was no asking price for you to compare sale prices to. It could be that most sales go through at a discount to asking prices. I've seen a few come through at some steep discounts but it seems most sales are going through at nothing like 10%-20% discounts. Volumes are down massively though.

QV will be based off actual sales, TM ads haven't sold yet, so it's possible that a current market support is lower than both.

Here are three examples from my area. This (market 'correction', if you will) is happening right now, and quickly.

1. Listed for auction - either didn't go to auction or didn't sell.

Changed to 'negotiation' - didn't sell.

Changed to listed price of $1.495million. This is FAR less than it would have sold for last year when I was looking to buy. I wouldn't even have looked at it.

https://www.realestate.co.nz/42151273/residential/sale/69-owairaka-aven…

2. Exact same process as above (auction --> negotiation --> listed price of $1.19million "urgent offers")

https://www.realestate.co.nz/42153761/residential/sale/83-st-georges-ro…

3. Finally, huge drop on this one.

Auction --> listed for $2.49million --> listed for $2.05million.

https://www.realestate.co.nz/42148331/residential/sale/13-quest-terrace…

How loooowwwww can you goooooo?

Yes, I am seeing this in my area as well. Winter is coming.

Yeah I think many are either trying to convince themselves that what is happening is just a 'glitch' or are just simply dreaming, but reality will sink in sooner or later. I believe we are on the verge of real panic from people finally realising the facts and wanting out.

In my neighbourhood there is a property that's been for sale for probably 6 weeks. Same process as above with many different selling techniques employed and finally just a listed price with 'offers over'. They want double what they paid for it 5 years ago having done nothing to the property. Needless to say people aren't exactly lining up!

Their asking prices aren't particularly low being around the mid figure of the estimates given on the various websites that estimate these things. I noticed last week that the houses that sold generally fell around the lower estimate. Not very scientific but these properties don't indicate a crash yet.

Exactly, perhaps people need to start looking at what the property is actually worth on various sites giving estimates. The "Asking" prices of properties I have been attending open homes for were never realistic in the first place. One I visited was on for $1.495mil and I told the agent it was worth $1.35mil and a few weeks later the price dropped at $100k to $1.395 and its still sitting there. At this exact point in time its worth $1.3 in a falling market.

Not really sure what your point is here. You're basically agreeing that prices are falling because expectations have been too high, which is exactly what I'm saying.

Are you talking about a brick and tile property in Onehunga? I told the agent the same thing

What some people don't seem to realise is less desirable properties aren't going to sell quickly anymore and will need to have realistic price expectations...

That Owairaka property is on a main road opposite a skate park... not a great area of Mt Albert.

That Avondale property is opposite high rise apartments and close to a commercial area... + it's just in Avondale.

I didn't look at the last one given its 2 million.

Times have just changed, buyers have more selection of properties to choose from. The properties that don't tick the boxes will sit on the market longer... these people should have sold when FOMO was in full effect.

Papakura LQ - 10.8% is huge, for a 3 month period. $500,000 changed to $446,000.

Still trying to figure why the national average for LQ was -1.7%.

Has to happen, OCR increases will accelerate it. RBNZ/Govt has the option, save tax payers and tax paying businesses, OR save the tax avoiding speculator.

Should be obvious.

Should be obvious.

One would hope so!

Indeed. Its hard to operate the Labour lolly scramble with no tax revenue.

Well over 50% of that lolly scramble to the old and wealthy too.

And in 10 years time the house prices will be double what they are today.

People need to realise New Zealand was truely discovered in 2000 by the internet. There is no going back to the old days.

Global interest in this little piece of paradise will only grow and grow.

Delboy -lol very droll

you right, its amazing - I particularly love the low wage economy, emigrating young people, lack of opportunity, unaffordable low quality housing, grumpy ageing population, returning expat crims and large amount of beneficiaries. I love it! i also love our socialist left wing government crushing our personal liberties and our amazing climate which is the planets second second worst after England. Forgot to mention, I also love paying massive rates bills to a council bloated with bureaucrats that can't even deliver a separated stormwater and sewer system. First world we are here, and I love it! Better not let the rest of the world see, we are a beacon of hope!

Not to mention we shouldn't drink the water, high pollution of the soil and cancerous exposure to the sun. Still good for a braai at the beach at least!

Depends what the interest rates are, and what peoples wages are during that period

are we in for a 25 or 50bps rate hike on Wednesday? I'm picking 25bps and drop in NZ$ cos everybody is expecting 50bps. interested to know your thoughts . . . . . .

50bps takes the OCR to neutral territory. Hard to be convinced 50ps will make a dent in inflation in the long run. Haven't considered 25bps for this reason, and instead thought it could either be 50bps or 75bps. 75bps seems unlikely (has it ever been raised by this much?), I'm picking the unconvincing 50bps followed by another 50bps next round, then consistent 25bps until the tipping point. Not putting money on it, just a stab in the dark as much as anything.

I find it funny when people refer to a neutral OCR level and assume its 2%. 2% as the neutral rate makes sense if inflation is roughly the same.

But if inflation is 8% and the OCR is 2%, then we have -6% real rates, which by history is extraordinarily stimulatory......nowhere near neutral!

Yea definitely, reference to neutral territory in my earlier comment was made in the broader sense (neutral OCR/inflation target of 1 - 3%).

It's interesting the slowly slowly approach seems to be to save face in the housing market more than anything. Ripping out 3 - 4% OCR and a sharp increase in swap rates would likely result in high volumes of mortgagee sales, potentially increased unemployment rate due to recessive industries (construction being one)... to be honest - I'm lacking knowledge in the OCR -> swaps relationship, so a little bit of telling stories here.

I guess the only reason they can get away with slight increases is that this is off the back of an over inflated housing bubble so there's good bang for buck for the massive amount in mortgage debt taken out over the last two, three.. six years........ who's counting?

I keep saying watch the commercials (banks) they're the ones with their real lolly on the line. They've got 70% of their books in residential. If it gets to minus 30% from peak (Nov/Dec 21) then I'm picking they'll be scrambling as well. Which could be fun to watch... if you were renting.

Up until a couple of decades ago you could always swap your over-priced house for a dairy and earn enough to come out ahead after a few years. But today the supermarket duopoly has gobbled up discretionary income and those non-skilled immigrants who came in via the 'business' immigration portal are still paying back their expensive loans to the immigration loan sharks, so the corner dairy is tightly held and is not the saviour it once was.

There is another way to not lose too much on an untenable mortgage on your home, and that is to 'leave money in' via financing the purchaser into your property by leaving in an interest-only first or a second mortgage over say 3 to 5 years by which time we should be about to come out of the recession that will hit us next year and the purchasers will be able to refinance with the banks at lower rates. If the banks' mortgage rate then falls from a predicted 7%+ to say 4% your purchaser would be happy. Meantime, you've been collecting say 4% or more interest on your mortgage. Of course this method would only be open to those that have another home to live in, and the purchaser would need a sizeable deposit to encourage them not to default.

The other benefit would be you could probably fetch a higher purchase price using this method because you're enabling the FHBs or whoever to acquire their own house and they would be less inclined to haggle.

I wouldn't be surprised if we start to see multi-property investors quitting their portfolios using this method.

Note that this scenario was extensively used from the 1960s to the 1990s and has only fallen out of of favour because the banks have been offering lower and lower interest rates from those times. But now that banks are being ultra-conservative who they lend to, and interest rates are trending up, then who knows?

Banks have to hold the first mortgage and tend to want another 40%, they hate your idea......

Isnt that just setting the buyer up to fail?

If the new owner defaults under the rising rate environment, and bank sells at market there could be little left for you and the new buyer. You would be facing at best suing someone who is physically bankrupt, but not technically.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.