At first glance the latest Reserve Bank lending figures suggest recent increases in mortgage interest rates and tighter lending conditions have been disastrous for first home buyers.

In July mortgages were approved for 1837 first home buyers, down a whopping 37% from the 2925 mortgages approved for first home buyers in July last year.

The June figures were just as bad with 1885 mortgages approved for first home buyers, down 38% compared to the 3018 approved in June 2021.

Which suggests first home buyers have been crushed by current lending conditions.

But if you stand back and take a longer term view of the figures, things may not be as bad as they seem.

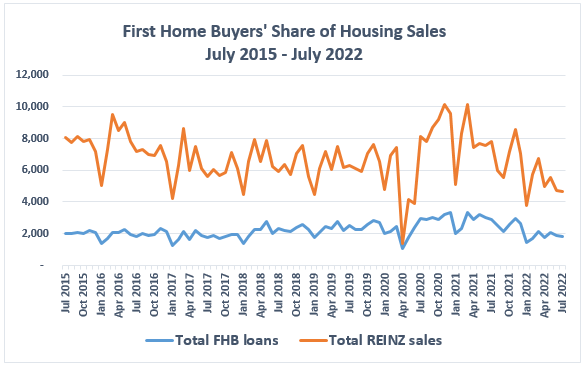

The first graph below shows the number of mortgages approved to first home buyers each month from July 2015 to July 2022, and compares that with the total number of residential sales recorded by the Real Estate Institute of NZ each month.

One of the most surprising things about the graph is how stable the first home buyer mortgage figures are.

They bounced along around 2000 a month right up until the housing market was hit with a massive tsunami of stimulus from the Reserve Bank in early 2020, which in turn unleashed a flood of irrational exuberance among house buyers, including first home buyers.

Whether the irrational exuberance was limited to house buyers, or the Reserve Bank's actions were the result of some irrational exuberance of its own, is the subject of some conjecture.

Perhaps there was a bit of both.

However there is no doubt about the effect such measures had.

Between mid-2020 and late 2021, there was a significant increase in buying activity by both first home buyers and in the overall market.

Now that the Reserve Bank is unwinding the stimulus, that brief burst of activity has settled back down.

What the figures suggest is that mortgage lending to first home buyers, and by implication the number of them that are purchasing a home of their own, is now returning to its longer term norm.

Other changes are also afoot.

The rate at which lending to first home buyers has declined is slightly slower than the rate at which overall housing sales has declined, suggesting first home buyers' share of housing sales sales each month is slowly improving.

In July 2021 the number of new mortgages approved to first home buyers was equal to 36.4% of all residential sales recorded by the REINZ.

In July 2021 that had increased to 37.4% and in July this year it was 39.3%.

That suggests first home buyers are slowly but steadily taking a bigger share of the housing market.

The nature of their borrowing is also changing.

The most dramatic decline in mortgage lending to first home buyers has been for riskier, low deposit loans, where the mortgage was for more than 80% of the property's value.

In July last year these low equity loans accounted for 35.1% of mortgages approved to first home buyers. In July this year that number had dropped back to 25.3%. That is affecting how much first home buyers are paying for their homes.

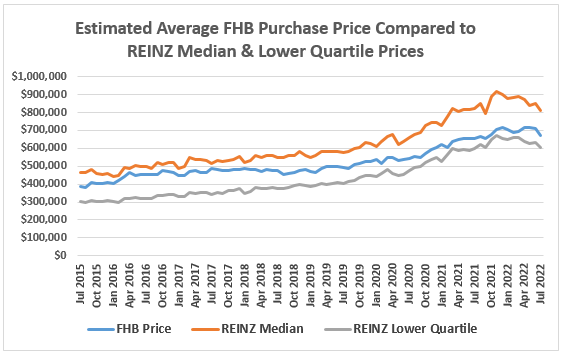

Interest.co.nz estimates the average amount first home buyers throughout the country pay for their homes each month.

Comparing these figures to the REINZ's median and lower quartile prices also shows an interesting trend, which you can see in the second graph below.

It shows that in 2015 the average price paid by first home buyers was very close to the median price of homes, but it has now moved much closer to the lower quartile price.

That, combined with the increasing share of the total housing market first home buyers are achieving suggests they are consolidating their position at the bottom of the market.

Affordability will likely be one of the main drivers of that trend, but changes to the tax rules rules for investors have probably also had an effect.

So while affordability remains a major issue for aspiring first home buyers, the figures suggest there are some things that are moving in their favour, such as taking on less high risk debt and gaining a bigger share of sales at the lower-priced end of the market.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

23 Comments

I guess it is good time to buy the first home.

I guess it's a better time to buy a first home than it was in 2021. It is a good time to buy a first home, though? I doubt it.

If grocery shoppers were buyer similar amounts of food as before - but were now purchasing more of the lower end cheaper products, does that mean its a good time to buy food?

First home buyers are always buying the lower end cheaper products - so in your grocery example, the grocery shoppers are still buying the cheaper products as they always have done, but more. AND, the supermarket may be willing to offer a further discount on those cheaper products! Surely if a Buyers' Market is not a good time to buy, then when is?

From the article - it shows that FHBs used to buy more at the median rather than lower quartile. While total loans have gone back to bouncing along 2000 level - so no they are not buying more either.

It shows that in 2015 the average price paid by first home buyers was very close to the median price of homes, but it has now moved much closer to the lower quartile price.

Looks like the Bank of Mum n Dad keeping a few in the race. Still picking further declines.

All house pricing charts are on a downward trend, it would be slightly crazy to buy now as pace of downward arrows are getting steeper.

I disagree. There are so many good deals to be had in the market at the moment, with lots of vendors willing to price in drops considerably higher than where the market is currently at. There is a reason why it's called a Buyers Market!

Is that the advice you would be giving friends and family. All the charts and key indicators point to market downturn, rates up inflation up NZD tanking, house prices way overpriced compared to incomes. You must looking at different data than the rest of us

Define a good deal? The market froth in Auckland is circa 30% due to RBNZ "exuberance" and that has not yet been rinsed away.

Costs are still increasing due to monetary tightening. The HPI shows a steady month on month decline driven by those costs. Buy it today for 800k or buy it next month and save 16-18k according to stats. A buyers market it is, because vendors have run aground as the financial tide has gone out and they are not getting the interest they would like. Does that mean it's the optimum time to buy. I doubt it unless the thought of watching a 20% deposit melt over the coming months is palatable.

It would only be someone inexperienced that would not consider that they could offer and potentially buy a property advertised in this market for 800K for 700K, or perhaps less. The point is that given it is a Buyers market, which means that as a buyer you have the power in the negotiation. You don't need to wait to try and time the market to drop as you say 16-18K. That is foolish. You are more likely to get a better deal now by negotiating with the uncertainty in the market as vendors will also negotiate. It is only a buyers market until it isn't - and at that point in time you have lost your negotiating power.

I doubtit in Auckland prices are falling 20k to 30k per month the market is at start of journey down will be buyers market for years all that is going to happen if you buy now is the deposit you put down will disappear and then the next number of years in negative equity.

We are not buying in this market, investing in our business. The housing market is so volatile at the moment its to hard to read. Inflation, higher mortgage rates, people leaving NZ ridiculous prices with high DTI. Will wait for our business to truly work, while we watch prices drop. May be a few bargains popping up in a year or two when things start biting these investors who have over leveraged. I have invested in popcorn though.

Your comment tells us exactly where the market is heading - down!

with lots of vendors willing to price in drops considerably higher than where the market is currently at

Yes!! That's the point - take advantage now of the uncertainty! No-one is suggesting you go out and pay full price unless future drops are already priced in!!

I think that vendors are generally more optimistic about the potential future price drops ("it's a correction, not a crash"-kind of optimism) than those with the means to buy. Time will sort this problem out to the advantage of those buyers with patience. (You're welcome to buy as many properties in the meantime as you'd like, of course.)

But their forecast is not realistic think most will need to relook at what their price is and drop it by more. Most won't though, so better to wait for stability and then offer lower price, see what happens.

Give us a like for those who know of or are fhb's who are sitting back and waiting for the price drops to really take affect ?

This is me - Returned from overseas mid last year with the intent and means to buy our first home, but refused to participate in a market propped up by emergency interest rates and herd insanity.

We're renting a nice enough place, and are keeping an eye on the market in case a unicorn opportunity pops up, but are otherwise happy to sit tight until more vendors have moved past the denial phase.

..exactly the scenario of some of my family - and some of their friends (apart from the poor sods who purchased recently with a dose of fomo).

It was their overseas experience of the housing market that made them shake their head when they came back to NZ and say wtf is going on here!!??

....and walk away.

Yes, agree. I've got one who watches the market here with disbelief. He subscribes to the 3:1 house price to income ratio, as he can buy at that sort of level in the States - but admits he'll likely head back when it gets to around 5:1.

He thinks he might be an old man by then though!

Instead of a house rainbow and balloons feelgood pic for FHBs - would be better showing investors running for the exits with their bags of swag.

If total loans to FHBs hasn't gone up but their market share has - that's got to be the only conclusion to draw.

FHB should stop buying old properties of 60s and 70s, this will drop the house price and rent to great extend.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.