A dramatic fall in house prices at the bottom of the market last month considerably improved the prospects of first home buyers, according to interest.co.nz's Home Loan Affordability Report.

According to the report the Real Estate Institute of New Zealand's lower quartile selling selling price dropped substantially in most regions of the country in January. The biggest fall was in the Bay of Plenty where it declined by $96,000 (-13.9%), falling from $692,000 in December last year to $596,000 in January this year.

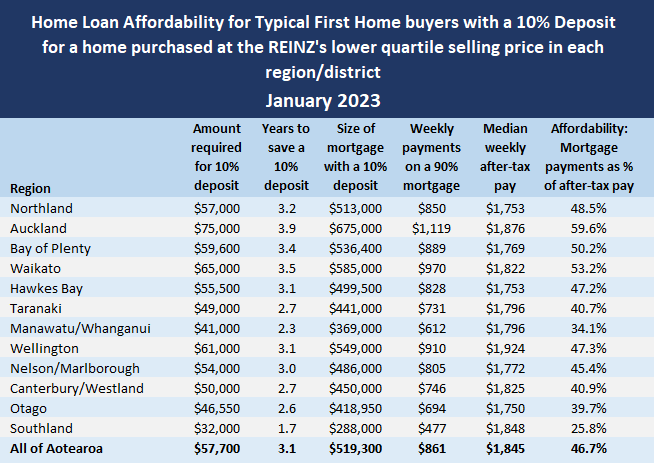

The lower quartile is the price point at which 25% of the sales in a month are below and 75% are above, representing the most affordable end of the market that is of most interest to typical first home buyers.

Following close behind the Bay of Plenty was Manawatu/Whanganui which recorded a $70,000 (-14.6) lower quartile price drop in January from December, followed by Auckland -$62,000 (-7.6%), Nelson/Marlborough -$42,000 (-7.2%), Southland -$31,000 (-8.8%), Taranaki -$30,000 (-5.8%), Wellington -$27,000 (-4.2%) and Canterbury -$20,000 (-3.8%).

The only regions where the lower quartile price increased in January were Waikato +$50,000 (+8.3%) and Hawke's Bay +$15,000 (+2.8%).

The latest drop in prices means there are now six regions around the country where the lower quartile selling price has declined by more than $100,000 since prices peaked in November 2021.

They are: Auckland -$216,000, Bay of Plenty -$104,000, Hawke's Bay -$107,500, Manawatu/Whanganui -$105,000, Wellington Region -$165,000, Nelson/Marlborough -$117,000, while the lower quartile price decline in Otago is just under $100,000 at $99,500.

Nationally the lower quartile price has declined by $93,000 from its peak in November 2021.

As well as benefitting from lower prices at the bottom end of the market, aspiring first home buyers were also helped by the fact that mortgage interest rates did not increase, with the average of the two year fixed rates offered by the major banks staying at 6.58%, the same as it was in December 2021.

However that pause in interest rates may not last much longer, with the Reserve Bank set to review interest rates on Wednesday.

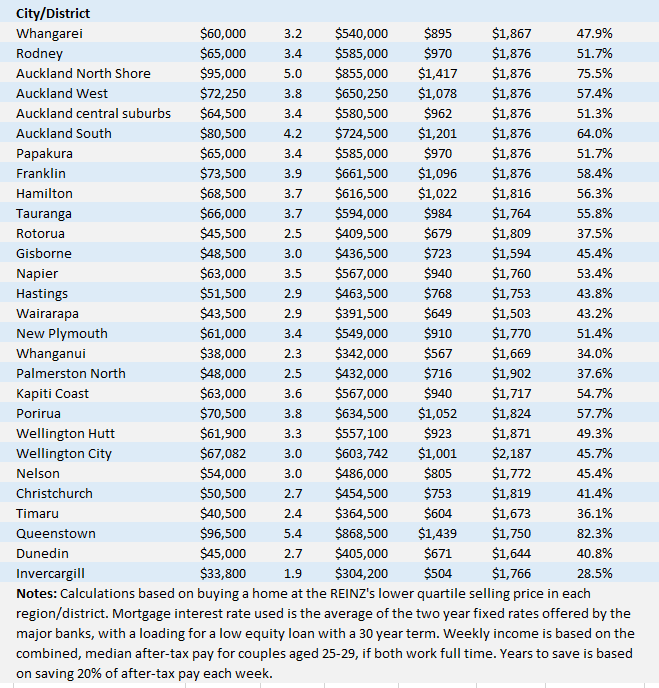

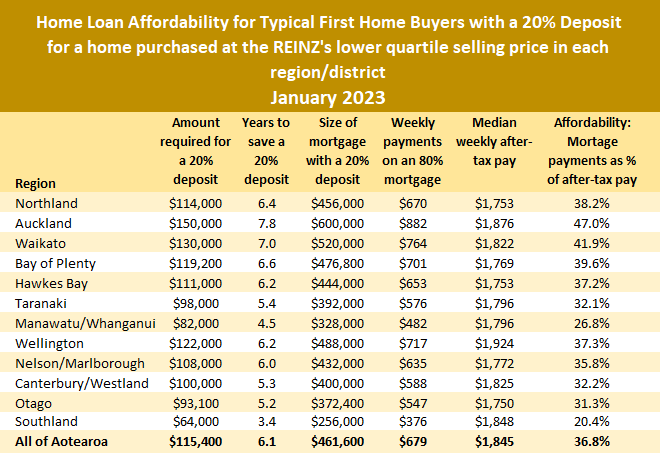

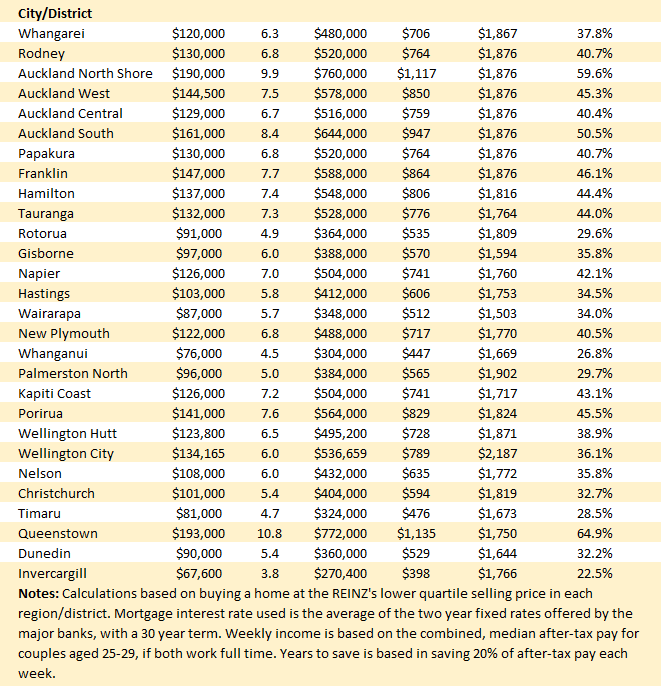

The tables below give the main affordability measures for typical first home buyers with either a 10% or 20% deposit, by region/city/district.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

96 Comments

Only about a trifling 11 years to save the deposit and ~65% of after tax income to pay for whatever you might then be able to buy in Queenstown....

"The bigger they are, the harder they fall"

In tall glass towers, they sit and scheme, Their eyes aglow with investor's dream, Their pockets lined with stacks of cash, They build their empire with a lightning flash.

They buy up houses, one by one, With every deal, they think they've won, They raise the rent and watch it soar, They care not for the tenants anymore.

Families struggle to make ends meet, They skip a meal, they barely eat, While the investors count their money, The tenants live in pain and agony.

The market booms, the profits grow, The investors reap what others sow, They see no harm in what they do, As long as their wealth keeps breaking through.

But what of those who have no choice? Who lack a voice and have no choice, Who suffer for the rich man's greed, Who pray for help but get no heed.

Housing investor, heed this plea, Think of those who look to thee, Build not for wealth, but for the good, And you'll be remembered as you should.

- SMG.

Everything is meant to be even if you “work hard”. That’s life and it isn’t fair.

Incredible 👏👏👏

I recently visited Queenstown and stayed in two airBnB places in town. one is a 2020 build townhouse, only 38m2 big, looks new and fresh, but it was a very cheap build.

the second one was not far from the first one, also a townhouse, small kitchen, pipes noise so loud, and shower poorly planed.

I was disappointed, not because those are small but just feels cheap build, and they are everywhere. I wonder how Queenstown will turn out to be 10 or 20 years down the track when those new builds became shacks. shameful really.

Someone will tear them down and build something new there?

Probably 10 townhouses on site with freehold titles, so cannot tear it down as 10 owners with different priorities. Just a future of low maintenance ahead.

Not just Queenstown, in Auckland many new builds are “cheap builds”, they look very nice and modern but poor workmanship most likely will have issues in 10-15 years. No one cares as young builders don't give a damn even if they turn up to work and experienced builder retiring..etc

Things have gone down hill since 2017…

The bubble is bursting for sure

I personally know one or two ‘permabulls’ who now think a crash is well on its way. Quite a shift.

I have no idea how certain people can argue it’s not, and keep a straight face…

The spruikers normally log in about 6:30 am to fill Gregs posts re auctions with trivia and spruiking, but now almost every day here and in the MSM the falls are slapping them in the face. 90k in Turanga is a lot in the 25% lower quartile mark. Remember buying to early is DEAD MONEY.

The collective morale of NZ has taken a real beating this year. As I keep saying H2 is going to be well ugly.

There's the prospect of significant job losses combined with the rollover of fixed interest mortgage repayments to navigate through yet. The prospect of additional taxes to aid the recovery looms large too.

I have no idea how certain people can argue it’s not, and keep a straight face…

This is somewhere near the anxiety - denial stages. Not sure how the media will deal with the dreaded panic - anger stage.

As one particular/peculiar individual here tried to spruik it, "rent increases are a "cue" to an imminent recovery in house prices". Now lets get back to reality where the true facts are undeniable. The prospect of endless capital gains attracted the greedy, capital losses will do the opposite. Especially now that they're paying double the interest! Rental yields will soon reflect multiple risk factors. Term deposits are very attractive.

The interest deductability is a huge factor

For the small investor interest non deductibility will be the death knell this year.

With double whammy of the tax bill ,provisional tax along with higher interest most small investors will not have the cash flow and will be forced to sell.

The stats are showing this with the lower quarter sales.

With 660k rentals owner 80% by small investors is 528k houses.

As we get closer to the elections the selling may accelerate is labour is up in the polls.

Keeping interest deductibility is probably the only reason I'd consider voting Labour. It's the best initiative Labour has done, and Act/National want to get rid of it, but I want my kids to be able to buy their own home.

Same here.

Hard to get too excited about a term deposit earning substantially less than inflation.

....until its used to purchase a cheaper house with a smaller mortgage.

Ideally yes. But when I suggested that to the missus, she nearly tore my head off! I was told "NO MORE MORTGAGES!" So I'm stuck with sub par returns!

They are not really all that attractive in absolute terms, as the net returns are still less than inflation. However, compared with housing they do look very attractive indeed, in relative terms. Well, at least they do not rapidly depreciate, as it has been happening (and it will keep happening for quite some time) with residential housing.

Still waiting for the permabulls in my life to admit it... perhaps more pain is needed

Some will always be in denial..

More pain is coming for the specufestors, lots of it.

2023 is going to be a year that many of them will remember for sure.

I’m not too sure about a full crash, but definitely a continuation of the slide - jobs or jobless the key metric to look out for in terms of a crash and the labour market is still pretty tight, plenty of work for builders/ tradies with storm damage up in the big smoke and lots of the grey haired brigade with plenty of cash supplies and a willingness to spend

Define 'crash'. I wish I could take credit for this, but a comment I read a few weeks ago adds some context to what we view as a crash.

People just have entirely the wrong mindset when it comes to timing. A 1%/month decline is basically free-fall when it comes to housing prices. Even 0.5%/month is a collapse if it continues.

Put it in context: Between Q1 2008 and Q1 2009, US house prices fell 6%. That was during the damn GFC and was the fastest rate at which house prices fell during that period. Peak-to-trough house prices fell a total of 20% (nominal) over a period of 6 years. What we're seeing now is that house prices in Melbourne and Sydney are "only" falling at about twice the rate house prices fell in the US during the GFC.

Even in Ireland, where house prices absolutely plummeted, between Q1 2008 and Q1 2009 house prices fell 16%, or a monthly rate of about -1.4%. That's 1.4% per month in one of the biggest housing crashes the world has ever seen. Houses ultimately fell in Ireland by 50% over a period of 6 years. Now - I'm not suggesting that that's going to happen here - but people gotta realize that house prices just don't move that quickly and this is actually quite a drastic change going on right now. The market was never going to collapse overnight.

It’s definitely a crash

And then some

looked at buying a house early 2021 to move into. Sold for $960k in March 2021 ( we offered $820k so a bit under the final price!)

18 months later, the house is back up for sale. Nothing new has been done to it. Asking price is BEO $750k. The vendors need a fast sale due to “job opportunities” elsewhere.

That is a massive loss of equity. One can only surmise the purchase price was buffered with a sale elsewhere, and not 80% mortgage given the asking.

We built a house in Waihi in 2019-20, and kept out property in wellington as a rental for 6mths because the bank would let us carry the debt. Sold it in early 2021 for 855K, and paid off all debts.

The same property is now quoted online as having a value between 650K and 785K. assuming the mid point of say 720K, the new buyer has only 36K of his 171K deposit remaining. This is a story that we will hear a lot about. The people late to the party, if forced to sell, will never be in a position to get back into a house again.

The market was never going to collapse overnight.

but it is..... NZ was the biggest winner on the way up and will be proportionately the biggest looser on the way down.

This ^^. I am incredulous that despite some of the fastest falls ever, globally, we are still trying to pretend this is not a crash

By July there won't be a New Zealander (who doesn't sell property) left under any illusion, this market is about to GAP down on low volume.

OCR tomorrow.

Doesn’t at all suit the dominant narrative to call it a crash.

I'm still picking 2027 as the bottom.

Still late 2023 / early 2024 for me. But the tick back up will be slow…

I’m in a similar camp. I think next summer will be a buying opportunity.

I would pick mid/late 2024. There is a long way to fall before prices start making any sense in terms of fundamentals, and residential housing is not a liquid an investment class as others, and not as fast a market when it comes to reflecting the changed situation.

Immmmmigration....... Nats won't leave that alone!

IF they get elected. And right now I would give them just a 50/50 chance.

If we had an impartial MSM it would be widely reported as a crash - instead, we've got our No.1 newspaper sponsoring Oneroof 'propertyganda' stories as news

I'm picking we're still about 6 months away from MSM reporting it as such - once the Auckland/Wellington index is down circa 30%, and there are wider mortgagee sales etc

Circa -1% a month is textbook crash - and we are nearly double that in places, so there will be people looking to point the blame of how it was allowed to happen

We were repeatedly warned it was a bubble, even before Covid - and every time we were warned by those not vested (IMF etc), MSM wheeled in Ashley, The Comb & Co as 'experts' to tell us to ignore the risk - it was negligent reporting

https://www.newstalkzb.co.nz/on-air/mike-hosking-breakfast/audio/ashley…

I just hope FHB's are doing their numbers and realise if they buy now they will pay back less than 7% principle in the next 5 years on 30yr table loan.

https://www.interest.co.nz/calculators/full-function-mortgage-calculator

As much as I dislike those two, I point the finger more at Anne Gibson. She’s the one synchronising them and the wider, destructive narrative that OneRoof has peddled for a number of years.

Shameful.

By the time this crash is over 50% from the top will be the minimum fall in some areas. In Auckland million dollar 3 bedroom 1980’s house’s in run down areas were common. So many just borrowed as much as possible now rates are higher the monthly payments will be hard to find when refinancing. The crap is hitting the fan right now any investors or people who are over leveraged will find next number of year’s very hard financially.

Does your after-tax income calculation take student loan repayments into account (given the target demographic of 25-29 couple)?

Great question. Many of that demographic would have significant student loans.

It doesn't I have asked this a long time ago. It assumes median income, with no kiwisaver deduction and just uses the tax rates associated (no student loans, allowances, etc) so it is a bit blunt but nice and simple. Look at it as more or a metric than accurate representation for the population in question.

What I find encouraging is how few comments 'house price drop' articles are getting now. We must be back on the road to realty reality. Deals are falling over everywhere with buyers remorse.

Indeed. Those with time to run on prior 5 years fix at under 3% will be ignoring reality. I have a workmate who is an interest only "investor". He has sold a couple in recent time to increase equity and prepare to ride reality out. Even Yvil sold something recently and stated his intention to wait. Perhaps DGM is is simply a "reality check".

Yep. Mine falls due November 2026. I’m in the 3s till then. Luckily I have over 80 equity and the readies to pay it off in full when rollover time comes if necessary.

Hope springs eternal.

You can't say that on int.co 😬

Its all that you have left now.....

Great thank you

Yes you can. Its only the continual spruik postings clearly smoking hopium in the face of significant market evidence to the contrary that becomes tiring.

Something for those who are expecting hordes of migrant and international students to arrive.

Why New Zealand is no safe haven from the climate crisis | CNN

Something for those who are expecting hordes of migrant and international students to arrive.

Reality check.

That means the average cost of going to college has increased by as much as 2700% in some cases — about 4.6 times the rate of inflation during the last 50 years.

Does anybody know where the REINZ lower (and for that matter upper) quartile prices are published? A quick search of the January HPI Report and accompanying Property Report doesn't seem to contain this data.

'Money's hard to find': Houses failing to sell under the hammer | Stuff.co.nz

priceless comment

“I don’t want to minimise or make it sound like these situations are the same as people giving up their lives to jump out of the trenches at Gallipoli,” he said.

“But it’s a modern day version, where agencies keep listing properties for auction despite the chance of having one bidder is pretty low, and the chance of having two bidders is even lower.”

Ryan said that during a depressed market, like the current one, auctions were only good for vendors who had to sell.

Quote of the year....describing them as like a modern day Gallipoli, where vendors’ homes are sent “over the top” by estate agents in the hope some might be sold...

So much truth, it hurts.

I just hope that this ANZAC day people remember the sacrifices that property speculators have made.

It feels somewhat bittersweet seeing this happen. The last two years of pricing personally got me in a dark space about staying in NZ as a young person. There is nothing attractive about realizing that a subpar house is 8x your post tax (couple) income and that's before evening considering kids. That on top of saving 20% while renting in a high inflationary environment.

I don't have that much emotion for those who "got on the ladder" in the last two years. A few hours of understanding OCR, inflation, basic economics would've provided writing on the wall that a hangover is on its way. I'd be feeling guilt or shame if I was one of the people that sold them the idea that property only will ever go up and you'll be fine. Seeing some of my peers being celebrated for buying their first home at 10-15% deposit at 2.5%, never sat right with me but I wasn't going to be the one to bring down their happiness.

Property in NZ is cult like. It's the dream, celebrate it when people take bankrupt potential risk at a young age to get in, hoard holiday homes because no other asset is treated the same taxwise.

In what other situation is it normal to borrow 5-10x your annual income to buy something when you don't understand how basic economics will affect the value of that something. Clown world.

In 10 years time those who got on the ladder in the last 2 years will be thinking how cheap property was back in 2020.

Ladies and gentleman, a perfect example of the cult mentality ^

I can already hear the nostalgic musings of those who purchased property in the last 2 years, reminiscing about the "good old days" of 2020 when property was supposedly cheap. I'm sure they'll gather around their holographic fireplaces and regale each other with tales of how they were able to purchase a tiny, dilapidated shack for only a few million dollars. Oh, how times have changed! /sarc

I wonder if those who bought SPY in Dec 2007 have regrets now...

The difference is that the bad stocks fall out of an index , its always the best news story......

Impossible to compare a major world share index with a residential house investment.

I don’t think prices in 2030 will be much if any above 2020. All that buyer will have to look back on is all the interest they’ve paid over last 10 years.

A useful reference is Ireland, whose 2006-2011 downturn we are closely following. It took until 2022 for prices to recover 2006 levels.

I wouldn’t be so sure. The new sub-par builds in the ugly town house subdivisions in the pull down a decent ex state house and whack up poorly built 10x townhouse builds will lose their value faster than a stand alone ex state house. When people need to paint the exterior and fail to get agreement with the 9 other neighbours (and absentee landlords) and the houses start falling into disrepair, the standalone houses with lawn will look more attractive than ever. It’ll be the townhouses that will become the next building disaster given the poor quality of the townhouse builds and the terrible underlying covenants on the purchase agreements e.g you can’t paint just your exterior. The entire exterior has to be painted. And there are no body corporates to arrange for that.

I agree. It’s the masses of quickly-built townhouses (all mushroom grey) that have gone up in the last three years that will really depreciate massively. They were radically overpriced in Auckland and build quality is often questionable. I think in a few years people will realise that well-built apartments eg Ockham are superior and prices will reflect that.

Yikes that must be the most bitter thing I’ve ever read. Has your basic economics factored in a growing population of wealthy individuals escaping various things such as climate change, war etc

...realizing that a subpar house is 8x your post tax (couple) income and that's before evening considering kids.

Bearing in mind that many of the older generation bought their houses at 3x a single income.

A mate of mine is a RE agent in Wellington. Sales have dried up and he is currently selling vehicles etc to try to reduce debt and save the house. Problem is that he joined the game during the absolute hay day and like many thought it would never end. Unfortunately for him he likes the finer things in life and although he has made very very good money in the last few years, he only has toys to show for it.

Unfortunately for him he likes the finer things in life and although he has made very very good money in the last few years, he only has toys to show for it.

Easy come, easy go.

Soon enough, many will be throwing their toys (Mazda BT50s, Ford Couriers & Holden Colorado's) out of the cot.

I think that would be a "Ford Ranger" :-) I have a '91 Ford Courier done 350 000k. Offers?

....ha-ha-ha, yup, I stand corrected :) Thanks for that.

Those little white range rover sports make you look a dick, selling it is a wise choice.

A fool and his money are soon parted.

any thoughts on tomorrow RBNZ decision? 0, 25 or 50 bps?

I think 50 (for what it’s worth!)

I think 50 too, but I think they should go 75 because Robbo is shaping to do some serious inflationary spending, especially as he is now in charge of the finances and the cyclone recovery.

100. If we don't get ahead of inflation rate then its going to be a very drawn out car cash like the 70s and 80s.

Agree entirely, but I still think it will be 50 in typical Orr fashion.

Prob 50 but should really be 100 if we're wanting to make things better long term

A month ago I was a coin flip on 50 or 75bps. I’m probably 90% 50bps now.

Obviously should be much more though..

No doubt: 50 bps, but with a hawkish stance.

Still a ways to go I suspect. I've been noticing more and more with crosslease properties that weren't selling in AKL that they would be taken off the market and later relisted as freehold. It seems people are doing the old conversion to Freehold to make the properties a bit more attractive. I've noticed such services being marketed more and more lately. https://www.subdividesimplified.co.nz/convert-cross-lease-to-freehold-f…

Yes I had noticed those services being marketed a lot more too.

probably a few factors at play. What you mention, plus business slowing down for surveyors and conveyancing lawyers

Yes. Govt phased new cross lease out a while back and laid a path for conversion to either unit title or freehold.

The world stocks have been much to strong and are very much out of sync with a Hawkish FED......who are getting much more hawkey with US FED FUNDS RATES ARE SET TO BE IN THE 5.5 TO 6.5% BY LATER 2023/24.

CORRELLATIONS AND BEWARE NZ......the housing ponzi has been skewered and frying on the BBQ since 2021.......the heat is going up now.

The Debt levered specuvesters have now lost all hope as we slip into an Irish Esk housing collapse!

Hard hats on!

I'm a buyer when rent yields are well north of 8%.......buying at lesser return is playing Russian roulette. We all know now, to not ever trust anything Russian, ever again!!

Debt should be supported by income. Its a long way back to 8%, a very long way.

A very good start in the right direction. Still some considerable way to go though.

I am picking Labour will return this year, recession in mid 2024 and the sliding will be for another 18-24mths,

There are strong sympathy feelings out there for Labour bacause of the natural disasters!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.