Signs are emerging that people selling their homes are starting to become more realistic with their asking prices as they realise their properties are unlikely to fetch the high prices being achieved a couple of years ago.

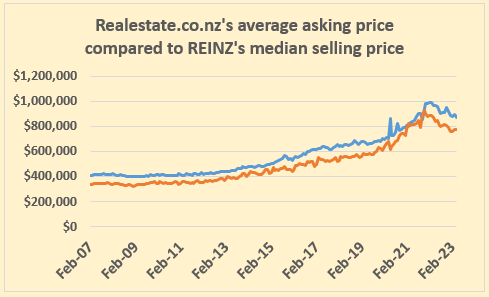

Comparing the asking prices of residential properties listed for sale on property website Realestate.co.nz with the selling prices reported by the Real Estate Institute of New Zealand (REINZ) each month, suggests the gap between the price vendors are hoping to achieve and the price buyers are prepared to pay, is starting to narrow.

The two figures are not an exact match because Realeatate.co.nz uses an average asking price and the REINZ uses a median, but the Realestate.co.nz average is an 80% truncated mean, meaning the top and bottom 10% of prices are removed before the average is calculated on the remaining 80%.

That should produce a figure close to the centre of the market each month, making for a reasonable comparison with the REINZ's median.

Interest.co.nz has compared the average asking prices on Realestate.co.nz each month since February 2007 with the REINZ's median price the following month.

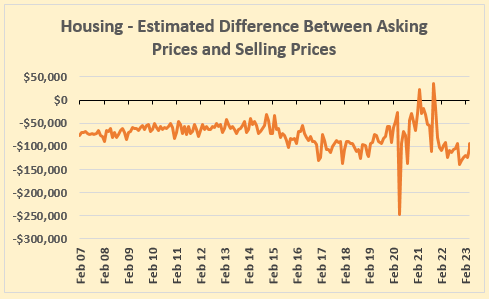

These figures show that once the market opened back up after the 2020 lockdowns, the difference between asking and selling prices narrowed considerably as the market took off, dropping to a record low of just $16,436 in November 2021, suggesting the gap between vendors and buyers was just 1.7%.

The figures also show that the market was running so hot in 2021 that there were two months - March and October - when the median selling price actually exceeded the previous month's average asking price, by $22,000 and $35,000 respectively, which were the only times this has happened since Realestate.co.nz was established.

However once house prices peaked in November 2021, the gap between asking and selling prices increased rapidly and edged above $100,000 at the beginning of 2022.

Although asking prices began to decline from March 2022, they did so at a slower rate than selling prices, suggesting vendors were slow to accept the full extent of the downward movement in the market.

By November last year, exactly a year after house prices peaked, the gap between asking prices and selling prices had ballooned to $139,636, a difference of 14.7%.

But it appears reality is sinking in and vendors are starting to adopt more realistic asking prices when putting their homes on the market and are more likely to accept lower offers.

The gap between asking and selling prices has declined steadily since late last year, and last month it dropped back below $100,000 to $94,352.

That has narrowed the gap between asking and selling prices to 10.8%. And although the REINZ's median price has increased by $18,000 since February, most of the reduction in the gap between asking and selling prices has been due to vendors lowering their price expectations.

Between May 2022 and May 2023 the average asking price on Realestate.co.nz declined by $90,526 (-9.4%) while the REINZ's matching median selling price declined by $60,000 (-7.1%) over the same period.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

155 Comments

Hang in there if you can vendors, prices are about to head north ...

Where would we be here without at least a few resident spruikers?

We'll be right one day...😄

Do you work for the Herald by any chance?

There was a one roof economist on the radio saying that price falls are over and now is the time to buy.

There was no disclaimer, no qualification, no recommendation to get financial advice. For the biggest decision most will ever make this is the Wild West.

this from me, a long time property investor, I thought it appalling.

Totally agree Te Koori, I wonder who is able to stop this, they are absolutely acting as financial advisors… and many ordinary people will be taking their advice, it really is the Wild West and no one cares about what is happening. Who can help? The FMA? the Commerce Commision? some Ministry such as IMBIE? Not the REINZ. Seems that all these guys have remits that sit outside of this kind of crockery, even groups like Consumer, who are quick to let the little guy know when there is a scam or bad information happening, aren’t getting involved in this. The proliferation of property based media programming and property mentors was a key issue in the Ireland crash, but noone here cares.

I have little hope the spruiker problem will be fixed. I'm adapting by teaching my kids how to recognise fuckwits.

There’s an awful lot of them around, and increasing.

Historically, more often than not, spruikers have been absolutely on the money.

True. That is until 2021.

You haven't got the memo yet ZS??

The world has changed.

That’s not the point ZS. The point is it is seriously leveraged financial decision and how on earth can they induce buyers on their view without appropriate disclaimers of conflicts and risk? You couldn’t do that with a stock so why a house?

True.....these toerags, were actively inducing more heavily leveraged house collecting today on the ZBs OneRoofie.

You really don't sound like someone in IT..

More correctly - the spruikers campaigns have been working.

Lister had a spruik today

Headline was a little misleading (of course). He did say housing was still very expensive but was bemused that Lister thinks he's an expert on housing markets - should know better.

I wonder if a directive has been issued. Also I saw an article from Anne Gibson yesterday and it listed all her ‘credentials’ at the end of it, as if it was trying to give credit to her Queen Spruiker positions. I am sure she is the ring leader.

Well said . Corelogic and Quotable Value are rear vision mirror data analysts. The former an American company acquiring all NZ property data.

The May HPI property article the Granny H forgot to publish:

The relentless downward spiral continues to wreak havoc on the nation's housing market, as evident in the latest May Real Estate Institute of New Zealand's (REINZ) House Price Index (HPI). The index reveals yet another distressing decline of 0.7%, pushing prices further into a deep abyss.

Nationwide, prices have plummeted by a staggering 18.0% since reaching their peak in November 2021. The REINZ HPI, which adjusts for variations in property types sold each month and is favored by the Reserve Bank, paints a grim picture of the market's current state.

Auckland and Wellington, the nation's prominent cities, have experienced the brunt of this catastrophic downturn. Both markets are now grappling with genuine house price crashes, witnessing jaw-dropping declines of 23.2% and 26.0%, respectively. The once-thriving housing markets have been reduced to scenes of despair and financial ruin.

In a cruel twist of fate, May's sales figures hit a 12-year low for the month, excluding the impact of the 2020 lockdown. The numbers paint a bleak picture, with sales remaining down by a staggering 23% compared to pre-pandemic levels in May 2019. The housing market finds itself trapped in a deep slump as the winter season sets in, intensifying the prevailing gloom.

As the market grapples with these challenges, homes are languishing on the market for extended periods. The median number of days required to secure a sale rose to 49 in May, marking an increase of six days from the same period last year. Prospective buyers are cautious, navigating the tumultuous landscape with trepidation.

Jen Baird, the chief executive of REINZ, acknowledges that high mortgage rates continue to cast a dark shadow over the market. The combination of climbing interest rates and a constrained economy continues to exert downward pressure, compelling buyers to exercise extreme caution amid uncertain economic headwinds.

To compound the woes, the economy has plunged into a technical recession, accompanied by a deep per capita recession. These troubling indicators further exacerbate the challenges faced by the housing market, dimming any prospects of a swift recovery.

Tony The Comb's monthly survey of real estate agents paints a grim picture, as a staggering net 58% of agents report ongoing price declines. The market remains entrenched in a cycle of falling prices, with little respite in sight.

As the negative trajectory persists, homeowners and market participants are left to grapple with the harsh reality of a market in turmoil. The prevailing circumstances paint a bleak picture, suggesting a prolonged period of uncertainty and hardship for the beleaguered housing market.

Lovely writing. Drop "Tony the Comb" and call him Tony Alexander and send to to Stuff as a guest article.

Great piece of analysis and writing 4D!

dp

The old Gran-rag (AKA: G Herald) would lose hundreds of thousands, if they even dare speak such truths!

They cannot speak these market fundamental market truths, as they are in the "Beholden Ones" grouping......whose prime objectives, are at all costs, to keep the property gravy-train-a rollin. They must suck in new FBHs as an imperative and repeat the Lies daily.

This was a nice piece, but you are sooo not going to get a job with Granny Herald.

Next!

People slowing starting to realise that leverage works both ways.

I feel sorry for those people that purchased in Auckland a house for 1.2m with 100k down. They now have a house worth 800k and have 1.1m owning, paying 60k-70k per year in interest.

Shares have performed much better once again. Mine doubled during the years 2018-2021, so we ended up with 1.2m+, no leverage. Took a hit of about 200k last year, sold nothing, bought more. Everything is back to being worth more than before the crash last year and getting 40-50k in dividends.

The property experts were wrong, diversified equity investments are much better than property. It was always the case, it’s just a bit boring and you have to really have your own actual money to do it, and take a long term view.

PS: The economists are going to be wrong about interest rates too. They are headed over 10%. There needs to be some accountability for these guys. People believe them, and it’s ruining people’s lives.

The difference between an illiquid property portfolio and a well diversified and liquid equities portfolio is the availability of cheap and historically tax deductible leverage.

58% of agents report ongoing price declines

So there's 42% bald-faced liars, 58% who realise they have to work for their money and be a little more down to earth with their clients

Plummeted by “staggering “ 18% since the market park in late 2021 ?

what about the “staggering “ 40% increase in the 18 months prior from early 2020 ?

Candyfloss due to money printing which will all disappear .

Nobody works at the Herald they just attend.

Hang in there if you can vendors

It's those Vendors that can't hang in there that will set the tone and the prices for the rest. One house in one street is forced to sell at a significant margin below expectations, and guess what the Lenders will assess the rest of the street/suburb/country as being worth? Much (much) lower. (See re John Key house, below)

And then we'll get the Snowball Effect. ("The snowball effect is a term that explains how small actions can cause bigger and bigger actions, ultimately resulting in a big impact.")

I think he means the prices are heading to North Korea values.

10% Interest Rates this Year, Guaranteed !

The Prophet is back 🍻🥳

Huzzah!!!! 🎉

Hopefully He/She/They have packed a fresh "I told you so" teeshirt to wear!

Don't forget the " manually modified " algorithms of homes and One Roof.

And the sudden realization by the RE scrotum that the Covid induced post 2019 CV's are now miraculously good indicators...

"Seling below CV"

You are absolutely right, prices are on the way to the north pole.. massive dip in temperature, I mean prices...

"to head north"... and off Cape Reinga into the bottom of the sea.

A minority of properties here have prices listed, they all tried it a while ago but have since reverted to “negotiation”….. the price when you ask is still way too high.

Who would bother unless there is a price? Why waste precious time if there isn't a concrete indicator of vendor expectation? Oh well, they can find out the hard way after watching their property gather dust for a few months on the market

Irrational purchase are coming home to roost. This will not be the first or last.

A Chinese businessman’s decision to buy Sir John Key’s former mansion (in 2017) for $23.5 million has proved to be the worst house purchase made in New Zealand in recent years, according to new data. That’s because the businessman suffered a $7.2m loss when he resold the former prime minister’s glamorous home in November, having never even lived in it.....12 per cent of all Auckland homes sold in the first three months of this year also made a loss.....it isn’t just Auckland homes where losses have increasingly been made in the past six months...

But it got a good wash. And got the money out of China

Spot on mate the washing machine goes round and round. You can bet it wasn't even his hard earned money anyway.

I gather you're already privy to his reasons for selling at a loss? Your post could be nothing more than uninformed Spruiker trivialization.

So much of that happening and not getting caught.

…and to reward someone for their stellar support perhaps?

The businessman would have said "money well spent"

Great example, so many other $23.5 million homes out there...

Yes - too many. That's why prices are plummeting.

He would have thought, as they do, that he was following that well-worn saying 'If you want to be successful, hang out with successful people,' without realizing JK's success was at his expense.

Other sayings, of course, are 'hospital pass,' 'useful idiot,' buyer beware,' etc.

As I recall, it was declared sold and then took a long time to confirm (and hence have a price reported). Perhaps that was just an extended settlement, but it seemed there was something else in behind. Was OIO approval needed, I wondered? The funds and/or purchaser might have been a bit dubious it seemed to me. And then never lived in it? Just speculation though. Maybe it was simply JK telling him that you can't lose on property in NZ - and there are no capital gains tax :-). Did the re-the sale occur just after the 5-year bright-line threshold had been met?

All very odd - the price, the circumstances and the timing :-).

The property was sold in 2017 and had two year settlement, and just after possession was taken in 2019 Covid hit and borders were closed. The owner had planned to immigrate here but border closures prevented that. The property sat vacant and became unkempt. Then Labour announced its IRD witchhunt into rich people's assets, and so they decided to stay put in China. Selling the property at a $7M loss is still probably less than any future wealth taxes he might have had to pay.

Kate - the first buyer (Chinese) who never lived in the property is likely the more dodgy, was the payment a deliberate over payment??

Well that should mess the Homes algorithm up a bit. I bet they tag it as an outlier.

Imagine if a Chinese businessman had paid our Prime Minister $5m WITHOUT buying his house.

Hey REINZ!.... how about some relevant and real data!

LIKE...

MONTHLY SALES PRICE V ASKING PER LOCATION eg papatoectoe v Remuera v Otaki...

It's not OK to just average the whole countries ( or regions) data because it looks better.

People buy and sell in areas.

Ì know you have this Data available to all the RE companies and it is them you serve. But these articles ae becoming irrelevant to most people except dummies and spruikers.

National and regional Data hides the detail, for example..local variances BETWEEN SUPBURBS, high stock areas v low stock, and coastal v inland etc?.. like the differences between porirua v waikanae Beach v Hutt valley... they are alļ Wellington area but waikanae is selling at different margins than thr hutt

On the face of it, the first resale of the Key house indicates that prices are 30% above where they were in 2017, and so that is their value in today's market = 30% below 2017 levels. Looks about right to me. And if so, there's a long way down to go to whatever a sustainable price in New Zealand should be.

(Let's remember even Key himself told us that price were too high way back in 2007, and it has only worsened since then)

How many people are in the market for a $15 million -$25 million dollar home? It's ridiculous to hold this sale up as some sort of comparison to the overall housing market...

The anti spruiking is sickening...

It doesn't matter. It's the reverse of what happened on the way up, and why we ended up in such a mess. High-end properties dragged along all those underneath them. ("Look what Key's house went for! Mine must be worth at least $X now" etc) And now - the opposite is about to happen.

To repeat mine from above, "One house in one street is forced to sell at a significant margin below expectations, and guess what the Lenders will assess the rest of the street/suburb/country as being worth? Much (much) lower." and this house may just be THE house that does it.

A 16 million dollar mansion in a prestige suburb ain't dragging up/down a $800k 3 bedroom home in a far less desirable suburb/city... I've never seen a valuer comparing JKs house to a 3 bedroom home being sold in Otara for example...

Time is about to tell us if that's right.

What do you think all the immediate neighbours houses are now going to sell for in that street? And now the street 2 away, and the rest of the suburb and so the rest of the city and then country.

That's how contagion sets in, in both directions. Isn't that what happened to Otara? The suburbs around it went up, so Otara did, and the ones around them and so on, right up to Parnell?

The number of comments in housing related articles would crash if it was just people on it that were all actually buying and selling a house. Loads of people here just angry and are here to vent that are not even in the market and never will be, total time wasters.

"..and never will be.. " - funnily enough, that might be what some of those people are angry about. The FIRE economy needs to DIAF - and we have whimpy complaisant politicians holding regulators back as they suck on the the teets of those parasites.

We could vote for change, but every party is the same colour - beige.

Are you referring to the spruikers progressing through the grief stages as they see house prices continue their decrease?

Don’t be too hard on them - best to let them get it out here in a safe environment.

You’re probably correct but why be dismissive of that percentage of kiwis who feel frustrated or angry with the housing economy? That division between entitled market participants and “time wasters” will eventually result in social unrest and gated communities. Nothing to be gained.

Zwifter, you seem pretty angry.

We are looking at buying, having a deposit, and good incomes. Looking for 5-6 bedrooms with at least 1000m² land in the Wellington region. Sure we could go out and buy now, it is a better time to buy than 2021, but it is soon becoming a better time to buy. I also know of another couple who are in the same position and doing the same. Maybe we wait a year or two, it doesn't matter because we are not losing rediculous amounts of equity each day.

Yeah fair enough - time the market when you, your friends and everyone else thinks it's a good time to buy again.

Good on you. But personally, hearing about people (who can buy) just sitting on the sidelines waiting for the prices to stop dropping always makes me feel uneasy because it shows that there is "pent-up energy/ammo" out there to prevent the prices from dropping too far and to potentially trigger another property FOMO boom at the first signs of the market turning, unfortunately.

I'm not sure, there are so many people saying prices will start going up from here, obviously saying so without any idea why they would go up.

Most who can afford to buy are buying now, they think now is a good time.

Once interest rates increase further, un-employment rises, and more weak hands fold and buy there won't be much pent-up demand, just supply from the over-leveraged.

Bang on got heaps of advice but are not in the market just looking at their screens and commenting what they feel. Imagine if we were talking about A2 milk and how if you brought at the top and had to sell now. Yet go back a couple of yrs ago and A2 was the darling of the NZSX

Agree. It's a long way back...back to reality.

The gap is starting to Reduce.

Wait till no one wants to buy in this land at the bum end of the world.

We are an over priced, paid media hyped country and our low quality shabby shacks are not worth they are priced. It's going to drop like stone in ocean. To the abyss.

Beautiful homes around where I live.

Painted and landscaped shabby shacks 🤣 just kidding

How come I've never seen this?

That's it - off to SYD. I'm going to be that guy raking the desert in front of his house.

REINZ's median price has increased by $18,000 since February

Really ???

Meanwhile the index has dropped hasn’t it? Higher market homes selling for less would do that.

Terrible time to sell. Unless personal circumstances leave you with no other option, I’m not sure why anyone would, with all indications being that we are at or very near the bottom of the market. Only justification could be if one is selling their home to upgrade to a more expensive one, which it could be argued is better to do in a buyer’s market.

"Unless personal circumstances leave you with no other option"

There are going to be owners of residential property who "have" to sell.

Saw a comment yesterday by a real estate agent. They stated that one property investor had half of their portfolio just listed for sale - that was 5 properties. We don't know their circumstances, but the real estate agent had in the marketing of the properties "Must sell" which might be just marketing for attention or it might be a genuine urgency to sell by the vendor.

This is how effective supply comes to the residential property market. The question is how many more owners are in positions / circumstances where they also "have" to sell.

If a large number of owners are in the "have" to sell category, then this could cause an imbalance with effective demand.

Remember that underlying supply and underlying demand do not effect property prices.

Yes. And who would sell before at least securing a conditional contract at the price you want tp pay for the next property (if re-buying). There is the risk that you are realistic in price in securing a sale, but may not find the right property for you has a realistic vendor as well.

And then, if selling and signing a contract conditional on suitable finance being secured by the purchaser - well.... who can say in this market that that condition will be met? You have then possibly revealed your bottom/lower price expectation, to no avail.

Not sure that there are any real indicators that we are at the bottom of the market, in my area ( the regions) we are only now starting to see price drops in better quality properties. So a lot to roll out yet.

I think Greg is right even with the 25-30% drop from peak sellers are will $100k or so off the pace. Have signaled several offers like that but no dice yet. The reality check squeeze is about to get worse.

I can waIt...wait untill the 2% loan rolls off to 3x that or more.

Agree we have made four verbal offers here but haven’t bothered putting it on paper as vendors are still $200,000 to $350,000 off and holding firm - that’s for property listed at over $1.5m. None have sold though.

Vendor price expectations and vendor circumstances matter.

From the May 2023, REINZ monthly property report

“Many vendors are still finding it difficult to adjust their price expectations and open homes have had an uptick in numbers in most parts of Auckland, weather permitting."

“Vendors are taking their time to adjust to realistic price expectations, especially those that purchased their property in the peak of the market.”

"Open home attendance has been on the rise and vendors are more realistic in their price expectations"

"Some vendors are still holding unattainable price expectations seeing some leave the market altogether"

"Local salespeople say the market has remained static with some vendors still reluctant to come to market due to their price expectations above the threshold of what most buyers are willing to pay.”

"Vendors are tending to meet the market or are deciding to not list at all."

He who asks the right questions gets the right answers

RE agents are not interested in verbal offers, you need to put it to paper and then they are obligated to present it to the vendors or they will just ignore it. Stops all the tire kickers.

Any sensible vendor would consider a verbal offer to be some sort of "cheap trick". An "offer" like this is not an offer, just a probing tactic. Imagine agreeing to such an offer. Next would come a much lower written offer.

If my memory serves me correctly, a verbal offer is still legally binding.

I very much doubt that in a real estate context it would stand up. Some people even get out of winning bids at auctions!

Often a verbal is couched in such a way that it wouldn't be binding, like a question, "would you accept such and such?"

But it could be dangerous, although they are likely to be lowball with conditions.

Agreed about verbal offers. We have never discussed things verbally with agents before, always written offers. Our intent was to put in a written offers but in all cases the agents wanted to check the “ballpark” as the vendors insisted that there was a bottom line that they would go below. All vendors are older people selling I guess with no strong drive to sell unless they get “their price”. They will be waiting a really long time.

Real Estate contracts need to be in writing to be legally enforceable.

It's not like the RE can agree to it, they are just a conduit. Until its properly written up on paper it's nothing but lip-flapping.

" vendors are still $200,000 to $350,000 off and holding firm - that’s for property listed at over $1.5m."

As they say in financial markets - that is a wide bid ask spread

and transactions are at bids not mids

“And although the REINZ's median price has increased by $18,000 since February” - that’s actually quite an increase, I can see why people are saying the market might have hit bottom.

If the middle price of properties sold has increased, but the index has fallen. More higher market properties selling for less during that period, fewer bites at the bottom of the market

I get that but many wouldn't. Although it must be quite a shift in the type of property selling to cause such a massive change to the median. Did this happen in Ireland where median value went up?

Yep, high school statistics

These people in the photo shoeless and standing awkwardly. The woman with clipboard suggests it could be a real estate auction. Maybe it's at a school waiting for enrolment. I would rather the second if it was me.

Restaurant or Cafe?

I am not making a statement on the state or future of the market. However, the initial statement on the data provided has a bias:

"Signs are emerging that people selling their homes are starting to become more realistic with their asking prices as they realise their properties are unlikely to fetch the high prices being achieved a couple of years ago."

The closing difference between asking and selling price may well be due to vendors being more realistic as argued, however solely on the basis of the data provided it could equally be due to purchasers are more willing to meet vendors price.

On the data provided, it really is a half empty - half full glass argument.

Before one gets too excited with a rebuff as to the housing market-sky falling, as stated, I am not commenting on the state or future of the market just the interpretation of the data.

You're right. And another thing that has more bearing (in a falling market) is the percentage that the difference is, rather than the absolute figure.

Sure, the values might have shifted for 100k under to 94k under - but as a percentage, that is a bigger hit going from 1M->900k vs 900k->806k. (a 10% drop vs 10.4% at those prices, but I believe the median values were lower to start with than those examples, so a greater percentage loss despite the lower absolute value).

The disconnect is actually greater, despite the absolute difference being lower.

So for every seller, there is a buyer - quite right.

But ask yourself "Why would a seller be selling at the moment?" and one very big answer is not "Because they think the price of their property is going to rise from here" - or they'd do as anyone would - they'd wait it out until later.

That's fine - IF they can wait. But as time tick on, that time is going to be up for anyone whose been waiting for higher prices and is now up against financial stress.

And let's also think why the seller of John Key's old place sold up now. Of many people, it's unlikely he needed the money right now. And if that's the case then the only answer might be as above - "Because they don't think the price is going to get any better from here" and a $7.5 million loss today is better than a $10 million loss tomorrow.

And when it all boils down to it, the capacity of the buyer to pay is what enables a transaction - whatever the asking price - and that capacity is falling in two main ways at the moment - the Cost of Debt (% rate) and Access to Debt.(LVRs, DTI's etc), and "getting a buyer whilst they can still pay" is crucial.

There could be plenty of reasons to sell other than financial stress. Divorce, rest home, upsizing, downsizing, etc.

"$7.5 million loss today is better than a $10 million loss tomorrow"

Exactly this. Get out while you can. Sunk cost fallacy.

Great time to buy. Nathan Rothschild said "buy when there's blood in the streets".

This is just a pin prick blood flow. There is no selling "must do" pain currently.......and we are down -25%!

Wait till the fingers and hands start flowing.........then the arms and legs......

Wouldn't think so.......I've been a property punter for decades and no property bear market has lasted longer than 2 or 3 years.

Taleb's turkey

Nice experience of the past 40 years......(100% an example of being a turkey in the headlights "Turkey of Taleb") edit.

- Since 2021, EVERYTHING has changed.

The period of forever cheaper money since the early 1980's is finished. Done.

Tighter credit and higher interest rates ARE the new normal.

"Since 2021, EVERYTHING has changed. "

----------------

You mean "it's different this time". I beg to differ.

No Not Different. Back to the 50 year average, common, everyday, NORMAL 6 to 10+% interest rates. I expect the NORMAL to resume 100%.

Your short term, required anomaly is finished, that is SUPERCHEAP COST OF FUNDS! Finished. Done.

Your certain requirements and needs of 2 or 3% interest rates are Done. Read my lips, Done.

Not coming back, unless we have economic Armageddon/Depression.

I agree with the logic, but there’s no blood in the streets. Yet. People still have jobs. Mortgagee sales are still negligible.

Yes correct, blood in the economic streets, is still 1 to 3 years away.

There's 13 mortgagee sales in Auckland today's Herald, a minuscule cross-section of the actual number, and certainly not representative of what's happening throughout NZ.

When first mortgage interest rates were 21% it didn't last long, a couple of years. Goldbugs and other Chicken Little's are always predicting financial Armageddon, but it never happens.

Best of fortune with your multiple rentals Wingman.

One little bit of advice that most NZers completely ignore......diversify.

That way you will always have a massive winner to sell in the tough times.......and not have it all locked up in depreciating housing.

Each market will have its Bear and its claws can exact pain for many, many years.

I only have one rental, I sold 2 properties before the current downturn, now I've just bought 2 acres close to what's going to be a couple of huge real estate developments. Just outside Auckland. Even in the bad times, there's pockets of expansion.

Sounds interesting. North or South of Auck?......Im looking at similar too. You near the SleepyHead factory??

But Im personally waiting for the extra 20-30% drop is values, coming down the pipe, when the pains show.

Most Kiwis only have RE and a little bit of Kiwisaver tacked on = risky business.

Hilarious, your comments make sense now. Waiting for the bottom. Going to buy up large. Going to start spruiking at some point. I see..

Would just be moving from an OO to an OO. So can do in any market. Not interested in paying the overthetopcheap3%loan/prices rates however.......this is in its early days of unwinding now, like NZ has never seen before.

I do hope to see housing prices within the aspirations of the average Joe, so lesser they become as a speculative financial asset, the better for NZ as whole.

Its not just all about Me, me, me.

I invest in companies employing people, discovering and building/selling products and pay dividends - you know, it's called real investing.

Praying for a bigger fool, to buy from me, is not required.

If you bought at the bottom of the cycle you wouldn't be a fool so your buyer wouldn't be "a bigger fool".

Yet where is the bottom ??? I've dropped another stone and still hear no noise.

Your stone must have had a soft landing

You invest in 'real companies'?

I speculate a bit myself on the stock exchange, have done for decades. Your 'investments' won't have done very well for the last couple of years, and no matter how good you are at stock picking, a rout takes everything down, ask the 'investors' in 1987, I watched the whole meltdown after cashing out a few months before. There's been others as well. At the end of the day, property punters still receive rent and they still own a property, many companies on the NZSE simply evaporated. Ask all those 'lucky' Brierley, Judgecorp and Equiticorp 'investors'.

It was a very exciting time actually, people were spending money like water. I had a floating mortgage from Countrywide Building Society which I ran it up to the max which was $100k, and did a bit of speculating on the NZSE. I lost my nerve after a few months and sold it all, but made enough to pay off the mortgage completely. Aaah, the good ol' days, I'm getting quite nostalgic.

It's good to have such a capable wingman on these sorties.

I find these folk who have done so well in real estate in the past now coming into the comments with such anti property fervour rather unpleasant.

i can assure you, that you have no idea about my company investments. I have received strong dividends, 3x what a Rotbox rental would return annually and my capital has been stable. Diversified.

I have no net borrowings - so using my own cash and this is the way in the new HIGH interest rate environment, for the time being.

Cash/property available, should it make sense.

Most property speculators in the last 3 years have done most,. if all of their cash deposits and many will be forced to set these losses in stone and sell in the coming months/years, with no uptick in the foreseeable, to allow a cash positive exit.

Complete disaster for these sops.

Borrowing to speculate on housing has been a winner for the last 40 years. Its now Done.

Those owning debt laden properties, as their major investments will be fried.

.

I beg to differ. it depends of course where you're buying.

In this case I'm taking a punt on Riverhead. There's huge works planned in that area but the Labour Govt. seems to have thrown a spanner in the works meantime. A Kumeu bypass, widening SH16, an 1,800 house subdivision by a Fletchers consortium, a massive 422 apartment retirement village with 90 bed hospital, leisure activities and childcare facilities in central Riverhead, and widening the Riverhead-Coatesville Highway through Riverhead. And right next door to NZ's most expensive suburb...Coatesville.

There's also the matter of the railway line running through the area, but who knows what's happening there?

I'm somewhat averse to having my money managed by others, and there's plenty of Brierley Investment punters who'll agree. I remember being with a few colleagues in 1987, and one who was highly respected for his betting on the stock exchange as it went vertical told all the others to "sell everything and just buy Brierley's". Brierley's was just one of many that got wiped out , and who can forget Equiticorp's Allan Hawkins strutting around followed by a few sycophants and finally doing a stretch in Mt. Eden?

https://www.epa.govt.nz/assets/Uploads/Documents/Fast-track-consenting/…

agree wingman

Property completely depend on where and what you buy. Then what you do with it.

People here seem to discuss property as if you buy an indexed fund of the nz property market.

Best of luck is realising your onsale dreams at 6 to 10% interest rate environment.

The experience of the lasts 40 years is no longer relevant. Higher interest rates are the new reality. This changes everything we have become accustomed to. Most do not understand this.

Wtf

You told us that you want to do the exact same as wingman. Swap riverhead for Drury or ohinewai or something else

NZGecko | 17th Jun 23, 6:53pm

Sounds interesting. North or South of Auck?......Im looking at similar too. You near the SleepyHead factory??

No. 100% not!

Will only replace and OO with an OO. Where......still to be decided.

"Onsale dreams"

Guilty as charged. Another f-ing trader

Cut down the Hooch. You make no sense at all.

Its making you obviously delirious.

Suddenly the cats got your tongue

You admitted to having plans to buy a plot of land where there is an expanding town development. Whoops

"now I've just bought 2 acres close to what's going to be a couple of huge real estate developments. Just outside Auckland."

"Sounds interesting. North or South of Auck?......Im looking at similar too"

Maybe somewhere you will grow your own herbs while you wait for the services.

I don't understand why you express such contempt for people who were just trying to secure a better retirement for themselves when other investments had very low returns and governments signaled that low interest rates, even negative interest rates, were here to stay.. Especially as you are waiting for distressed sales so you can benefit. Are you a homeless person using the free library internet? If so, enjoy your schadenfreude.

Borrowing to buy a house with a low deposit first started after the WW2 in the US when all the GIs came home. Prior to the war people needed 50%+ down payments and most lived in poverty. This change created the modern suburbs and resulted in a great lifting up of low income people into the middle class and the concept spread to the entire West. I doubt this will fundamentally change.

Wrong assumptions again. I hope you do better in assessing investments!

I have been a landlord many years ago, it was not my choice, but a short term circumstance. I saw no joy in it and will likely avoid it, apart from commercial.

The business case for residential, viewed from any angle, is now a very bad one.

I admire people investing honestly for their futures.

I detest what has without doubt, become the over financialisation of our housing stock. This has been aided and abetted by various Landlording tax rorts, that are now almost fully extinguished - good.

To see the vested REA interests and property collector class cheer: "How smart we are" while the average DTI is raised to an eyewatering ratio, driving out FHBs and cutting off the first rung of home ownership, by the "specuvesters" outbidding them, as totally indefensible.

If you are happy to be party to this ? well then......sleep well.

You detest the 'landlord class'? Actually the amendments the socialists have made to rental properties and tinkering with the Residential Tenancies Act have worked in reverse.

They haven't made any appreciable dent in house prices, they've increased rents and believe it or not there's 40,000 empty houses in Auckland owned by people who can't be bothered with the hassle of tenants.

Wrong. Accounting for inflation (and the averaged wage) increases, RENTS HAVE EFFECTIVELY DROPPED!

Incase you been living in cave? -

NZ Inflation: 6.7%

NZ Rental increases: 2.7% (Auckland 0% increase annually - an effective 6.7% drop!)

Real rents have dropped a REAL 5%. Real House prices dropped much more.........

I hope you can do better on future investments.

Don't you actually look at any the trusted resources on this site??

National median rent up by $15 a week in 12 months to March | interest.co.nz

When National win the election, they'll reverse some of the amendments the socialists have made to the Residential Tenancies Act. It's also worth noting that the Treasury advised the government not to tinker with the Act.

Rents are up, not down. As predicted by many pundits. And if you've got shares as you say, you might be getting dividends, but the share prices have tanked the last 18 months. The NZX50 is down 13%, I keep reading letters to financial advisors from frantic 'investors'.

https://www.1news.co.nz/2023/02/21/rental-prices-at-all-time-high-up-4-…

https://www.nzherald.co.nz/rotorua-daily-post/news/mark-lister-house-pr…

You would be a mug to have more than a fraction in the NZX and exposed to the NZD. Our share market is far too tiny.

I am mostly in ASX/US and exposed more to the worldwide economy/USA.

Riverhead I believe.

Correct, I haven't made too many mistakes, I sold my last house for $1.95m more than I paid for it. I made a killing in West Harbour, buying when there was nothing there. I ended up with 4 properties there. I remember when I was building my first house there, a guy wandered up to me when I was working on my own on the weekend, and he said "nothing will ever happen out here".

What year did you move to West harbour

Back to the Future Hill Valley 1955, and old man peabody with his shotgun, classic

I think it might have been 1989. Westpark Marina was just being completed.

There's no rocket science to this. if you actually want to sell, lower the price.

Most vendors do not work for RocketLab, they still want yesterdays prices......

Sometimes I love reading the comments more than the articles. Anyone that uses an analogy is a muppit and this seems to attract a lot. Good for a laugh though. Funny how successful people just keep quiet and get on with it and generally speaking succeed. But keep up the chat it is entertaining.

So your contribution to the discussion is making a condescending comment about other posters, subtley suggesting of course that you're one of the 'successful people'.

It's not the vendors that are finally coming to their senses, it's more so the morally bankrupt, unscrupulous agents with their 'reality checks' starting to bite.

There's still hoards of home loans to be refixed on dramatically higher interest rates this year. Those under the most pressure will take a few months to deplete savings, beg steal borrow, sell cars/boats/toys, get behind on loan payments, a few will lose jobs as the economy declines. That leaves them deciding they need to sell, or maybe the bank might make that decision for them. I think 3rd quarter of 2024 will be the time we see the effect of interest rate increases.

I have a cunning little spreadsheet that calculates the ROI from when a property was last sold until now.

Bad news folks. Avg ROIs are below 4%. Who said safe as houses?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.