Affordability for first home buyers was little changed in June, with lower quartile house prices and mortgage interest rates both bouncing along the bottom in a very quiet market.

The Real Estate Institute of New Zealand's national lower quartile selling price increased by $10,000 to $590,000 in June, up from $580,000 in both April and May.

However around the regions lower quartile prices movements were mix, with six regions - Manawatu/Whanganui, Wellington Region, Nelson/Marlborough, Canterbury, Otago and Southland recording decreases in their lower quartile prices in June compared to May. Three regions - Hawke's Bay, Taranaki and Bay of Plenty posted increases.

Lower quartile prices in Northland, Auckland and Waikato were unchanged in June from May, with Auckland 's lower quartile price remaining unchanged for four consecutive months.

Similarly there has been very little movement in mortgage interest rates of late.

The average of the two year fixed rates offered by the main banks declined by the smallest possible margin in June, dropping from 6.51% in May to 6.50% June, putting it back where it was in April.

So overall, with prices and interest rates largely flat, there was very little change in affordability levels in June.

Not a happy place

However although affordability may not have changed, the housing market is probably not a happy place to be for many first home buyers.

Although prices have retreated form the peaks of 2021, they remain so high that they probably present an insurmountable barrier to home ownership for many young people on average wages.

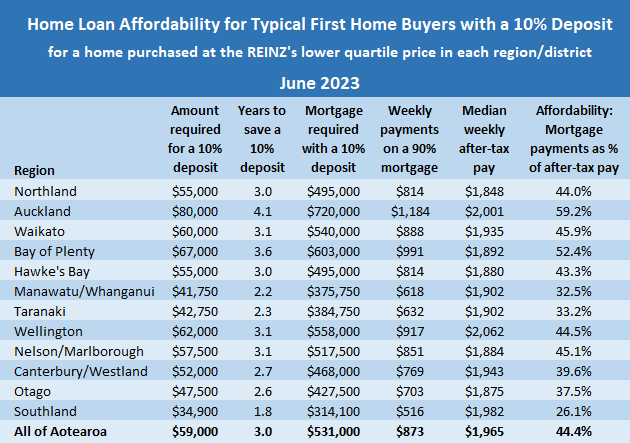

The amount required for a 10% deposit on a lower quartile-priced home ranges from $34,900 in Southland, which is the only region in the country where it is under $40,000, to $80,000 in Auckland.

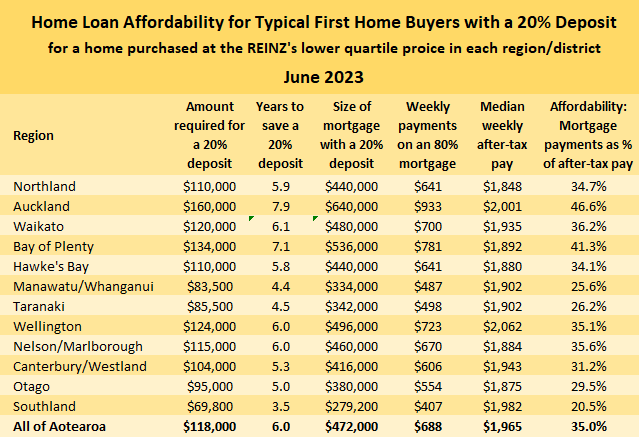

And of course you can double those figures for a 20% deposit.

Although banks will provide low equity loans to first home buyers, this option leaves many caught between a rock and a hard place. That's because most banks charge a premium on top of normal interest rates for low equity loans, which pushes the mortgage payments out of reach for many typical first home buyers on average incomes.

This leaves many of them in the position of being unable to save a 20% deposit on a home but unable to afford the repayments on a mortgage with a 10% deposit.

A typical first home buying couple working full time at the median rates of pay for 25-29 year olds, who had saved a 10% deposit for a home, would probably find the mortgage payments unaffordable in Northland, Auckland, Waikato, Bay of Plenty, Wellington and Nelson/Marlborough. Canterbury is on the verge of being added to that list.

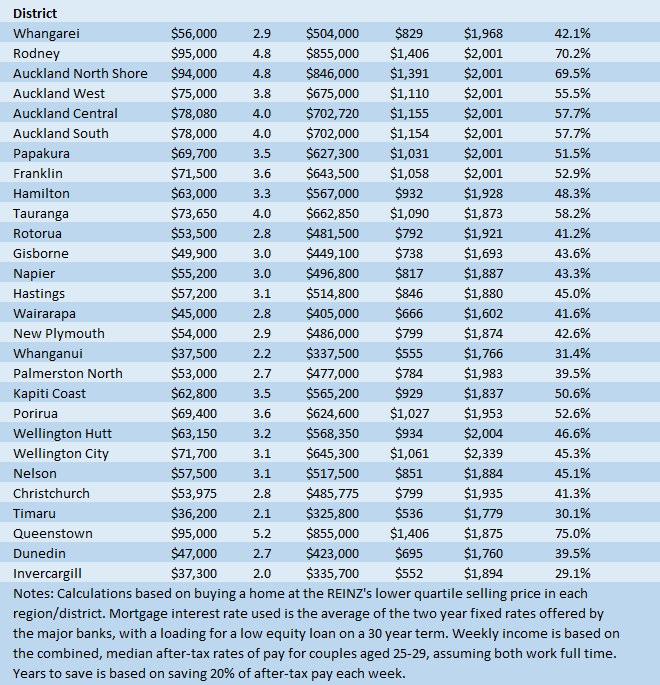

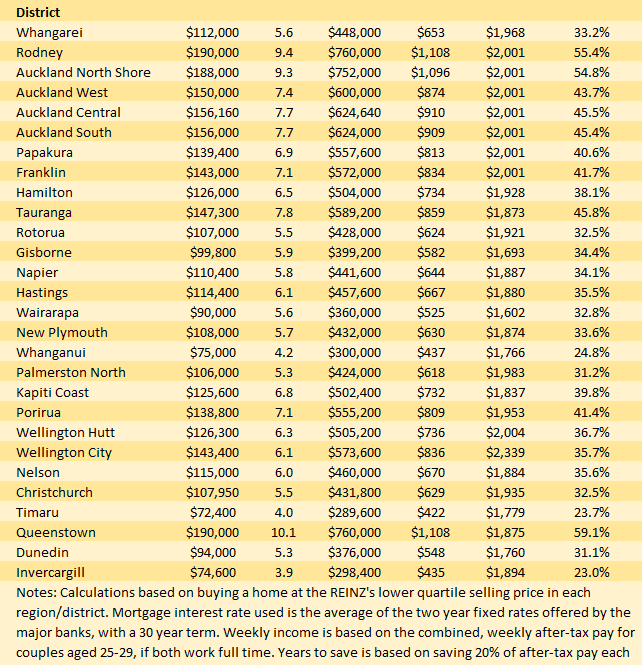

The tables below show the main affordability measures for typical first home buyers with either a 10% or 20% deposit in all major urban centres throughout the country.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

58 Comments

High interest rates on lending are not good for anyone hoping to buy a property that are not cashed up. FHB's are generally the spark that lights the flame in terms of getting chains to successfully complete transactions and are heavily reliant on home loans. The knock on effects are clear to see.

Probably, once things look sad enough, there will be some form of market juicing using FHBs. Lower deposit rates or lending allowances, that sort of thing.

Yea like cashing in on your retirement fund, or some sort of government deposit scheme or similar...

No, there's been enough juicing going on, time to take the punch bowl away - let prices come down to an affordable level.

Juicing it is, until the Ponzi black hole has accreted every cent NZ can earn, save or borrow.

We are all going to be millionaires.

I bet ya the Nats will bring something in to juice things up

And yet you're still voting for them...

Not me..

Yep, only because Labour have become totally unfit to govern. I can’t vote for a party in that state.

But for me it’s also just the final straw of a deeply disappointing government that have failed to deliver with such a strong mandate. If they couldn’t deliver in the last 3 years, when could they?

C’est la vie.

Hmm if only there were more than two parties to vote for...

Perhaps we could allow them access to their kiwisaver, with perhaps a leverage-able 10k to put an extra 100k floor on the market? Oh, we already did that, you say? Do you think anyone will notice if we increase it to 20k?

Low interest rates weren't good for FHBs either. This chart here shows a negative correlation between mortgage rates and house prices.

My point is that the current interest rates aren't making houses unaffordable, but the recent hikes have put mortgage rates out of whack with still-high housing prices left behind by years of low interest and other monetary stimuli.

Further, so much capital has been sunk into unproductive assets chasing easy gains that accommodation costs have risen to unsustainable levels pushing up living costs for most of us. Moreover, our productive capital-starved economy also means young workers with fewer economic opportunities to earn more, save up a larger deposit and service more debt.

Low interest rates weren't good for FHBs either. This chart here shows a negative correlation between mortgage rates and house prices.

The correlation is interest rates, but the cause is much higher lending requirements for buyers. When rates were higher, people were also taking out 110% mortgages, and banks were much freer at lending money in general. Since then, much harder to borrow, so the low rates were enjoyed by less.

Well at least our Australian owned banks will do well out of it.

Agreed. The problem is whenever a bubble bursts everybody wants a bail out. Too late! There is no escaping reality. Somebody has to pay and usually the costs are transferred from the reckless to the prudent.

If we as a society do not want financial/asset bubbles to burst then we should not be blowing them up in the first place.

Robert Shiller and Barry Ritholtz ("who dat" for the Granny Heraldites) thinks that the U.S. bubble may pop when the Fed stops hiking.

Down in Nu Zillun', this would be classified in the 'madder than a cut snake' category. You definitely would get strange facial expressions if you mention this around the water cooler.

https://markets.businessinsider.com/news/stocks/robert-shiller-housing-…

It just shows that any data can be spun in any (pre-concieved) direction if one tries hard enough.

Likes of Robert Shiller are different to you Dr Y. Schooled in and reached a level of understanding about behavior that you couldn't even imagine. As for Ritholtz, whole different level.

You regularly bring out a stream of experts, and rave about their credentials - what's your authority to evaluate experts to recommend to the rest of us?

I’ve read most of Shiller’s books. Irrational Exuberance is a great book and is guess that 1% of the commentators on this site would have read it - and yet it is possibly one of the best books ever complied on asset pricing, economics, behavioural finance, society and governance/central banking.

The quality of the commentary on the site would improve 10x if more people understood Shillers research - noting that he received the Nobel prize for his work on asset pricing - and 90% of the commentary of this site is on that exact topic (asset pricing).

Be like discussing psychics or science but to do so while ignoring the views of Einstein or Hawking.

And this is the problem we have in our society - we follow the views of OneRoof when it comes to housing/house prices but nobody even know who the guy is that has a Nobel prize for asset pricing (Shiller)

= foolish and mislead society

Would it not be wiser to modify/educate your views on asset pricing from the guy with the Nobel prize on that topic as opposed to the firm/people that have a vested financial interest in selling/promoting that product.

But this is a flaw in human nature..it requires a certain amount of intelligence to have the ability to recognise the intelligence of another.

Maybe, but Schiller and co could be just over-complicating things.

As a consumer with a certain amount of money to spend, I’m just as qualified to decide what something is worth…

All many of these economists can do is tell you is tell you prices don't stack up, in whatever model they've devised.

That's true of so many things, but, hey look they're still that much anyway.

Generally I avoid things I feel don't make sense financially, but sometimes you have no choice.

Most people think they're above average intelligence, but obviously can't be.

There are some pretty switched on people able to assess and address many facets of existence, this much is true.

But brilliant economists (or any social scientist), often aren't much better at predicting the future than the toss of a coin, they can just make sense of the ashes.

Assets seem over valued, this much is true. And if they get re-valued, you couldn't be surprised. But many of the arguments and scenarios promoted here verge into the fantastical. Trotting out an expert doesn't change that, you've mentioned bias, people can and do try and make their views expert adjacent, in order to give them legitimacy they may not have.

I’ve read most of Shiller’s books. Irrational Exuberance is a great book and is guess that 1% of the commentators on this site would have read it - and yet it is possibly one of the best books ever complied on asset pricing, economics, behavioural finance, society and governance/central banking.

Bingo.

Remember when Nassim Taleb used the example of the journo George Will asking Shiller, "if everyone had listened to you, they would be in a worse financial position" (housing valuations had doubled).

Quote (Taleb): "To such a journalistic and well sounding (but senseless) argument, Shiller was unable to respond except to explain that the fact that he was wrong in one single market call should not carry undue significance. Shiller, as a scientist, did not claim being a prophet or one of the entertainers who comment on the markets on the evening news. Yogi Berra would have had a better time with his confident comment on the fat lady not having sung yet."

Taleb's comments about Shiller / Will deserve some air:

"I could not understand what Shiller, untrained to compress his ideas into vapid sound-bites, was doing on such a TV show. Clearly, it is foolish to think that an irrational market cannot become even more irrational; Shiller’s views on the rationality of the market are not invalidated by the argument that he was wrong in the past. Here I could not help seeing in the person of George Will the representative of so many nightmares in my career; my attempting to prevent someone from playing Russian roulette for $10 million and seeing journalist George Will humiliating me in public by saying that had the person listened to me it would have cost him a considerable fortune. In addition, Will’s comment was not an off-the-cuff remark; he wrote an article on the matter discussing Shiller’s bad “prophecy”. Such tendency to make and unmake prophets based on the fate of the roulette wheel is symptomatic of our genetic inability to cope with the complex structure of randomness prevailing in the modern world. Mixing forecast and prophecy is symptomatic of randomness foolishness (prophecy belongs to the right column, forecast is its mere left-column equivalent)."

Taleb had a turkey, he fed it really well and the turkey was very happy until X-mas day, when he was made dinner. The other turkeys not put aside for X-mas were not fed as well and never made it as far as X-mas, they were slaughtered to be put in the supermarket much earlier.

Talebs turkey was the luckiest turkey of them all!

Do you now understand my previous post that anything can be spun in any way ?

Dr Y, I imagine you and the other sock puppets would like to consider themselves as Taleb's 'Fat Tony'. If that doesn't register, here's a nice description:

Fat Tony is not based on any single individual, but a consolidation of tropes and expression of specific concepts such as street smarts, outwaiting your enemies/betting against them, and never doing things that are fragile.

So you have no counter argument that any story can be spun to fit a narrative, so you change the subject, and quote a different story to show your "knowledge". Still the original point stands, any data can ben spun to match a pre-conceived theory, such as, "the recession will come when the Fed stops hiking rates".

Unless you want to stick to the topic and counter the argument, I'm waiting with bated breath.

This will go over most peoples heads J.C.

Often people have the tendency to say 'look you are wrong' (over a short time frame) because they have a vested interest in you being wrong.

They can't distinguish between their own self interest and what could possibly happen.

J.C.

Eugene Fama, who was co-recipient with Shiller of the 2013 Nobel Prize in Economics, has written that Shiller "has been consistently pessimistic about prices, so given a long enough horizon, Shiller is bound to be able to claim that he has foreseen any given crisis.”

Those who live in fear with Shiller will be life-long renters.

Well said, I can make any prediction and given a long enough time frame, it is most likely to come true. A prediction without a timeframe is worth nothing at all.

We are past the bottom in Wellington. It may not rise quickly but it isn’t falling further from here. Have a look at this one in Woburn Lower Hutt just sold for $1.4m! That is getting back to near peak prices.

If Act hold plenty of power after the election - quite plausible - I can see big cuts to the bloated Wellington bureaucracy looming. That would whack the housing market there.

I don't know about that Piggy, even the nicely maintained houses I've seen selling in the Western suburbs lately have been well below RV. The ones that need work are just sitting there or being withdrawn.

I would fully expect everything in Wellington to be selling well below RV, given they were set near the peak of the mania. Anything even approaching its 2021 RV is a very, very good outcome for the vendor.

Earlier on in the year our Valocity/ANZ valuation was 25% down from purchase price in December 2021. Just checked now, it's gone up 15% so we're now down 13% on original purchase. This is in Wairarapa.

I'm always mindful of the accuracy of property valuations, but I think the bank valuation is the 2nd most important behind an actual sales price. Homes.co is valued over 20% up since buying.

having tracked the lower hutt makret for 2 years- the house you refer to would have gone for $1.8-$2M in 2021. That suburb has been particualrly hard hit - average price in Jan 22 was $1.65M , now its $1.17M. Nothing has sold over $2 Million in 18 months and less than a handful have gone for over $1.5M. Back in the frenetic days 3 and 1 bedroom bungalows on 300 sqm were selling for $1.3M - so the silly days are well gone.

Trust me the market has been tested too- there was a house (effectively a townhouse relative to the area) that sold in Oct 21 for $1.660M - they went to market with it in Feb - passed in at Auction for $1.15M. I believe they rented it in the end.

Great thanks for your comment ikp. If we are talking about the same place it sold above its 2022 RV and is in the lesser desirable area of Woburn 3 bedrooms. I went to see it and got feedback from the agent - they reckon the open homes were packed and had multi offers - not sure it would have been at $2m at the peak. There is another superior one on Hinau Street that they had on the market last year didn’t sell then just relisted and sold quickly - it’ll be interesting to see how that one goes.

So when houses were at most unaffordable 2021 and banks lending and stress testing at low interest rates. People were leveraged to the hilt

Now we have rampant inflation, stress tests at higher rates by banks. How do prices go up, if banks don't lend since people cannot afford houses at current prices and rates. Don't you need money to buy a house.

However although affordability may not have changed, the housing market is probably not a happy place to be for many first home buyers.

Maybe. But I know some very happy first home yet to be buyers who are on increasingly higher levels of happiness as they observe what is happening to the finances of their recently purchased friends and acquaintances.

And of course well aware of the BS narrative that the bottom is in. Not all young people are stupid.

The only hope for young FHBs is to leave NZ. Rampant immigration and an incoming National Govt whose principal loyalty is to property speculators means that the situation will never improve here.

Yup. Just given this exact advice to my nieces and nephews. A bit sad, but on the other hand, they may get to explore the world!

I am seeing so many fresh kiwis around my workplace and our shopping centre.. How do I know? going to supermarket you often heard this remark " this is so much cheaper than Countdown/New World"..

Quite sad really, NZ will be just a transit point or waiting room!

Agreed.. Get on that plane and leave. You young ones will thank me later for this advice.

There is no point living here if you are semi intelligent and want to do more than cleaning the houses and offices of rich.

Your father's and grandfather's due to their greed have taken decisions and brought in policies and governments who have made this country unaffordable for the next generation

Not sure what's going to cause the entire system to eventually collapse. Productive workers and enterprises leaving for greener pastures or governments successfully replacing them with lower skilled workers in greater numbers.

Either way, my neighbour who's a registered nurse from South Africa is moving to Melbourne in 2 months' time. She feels bad having to leave yet another country "turning into mulch" in 8 years.

HSBC has reduced its expectations of house price falls through the rest of this year, and says they will be increasing at an annual rate of 5% by the end of 2024.

I have some snake oil I think you might be interested in.

Yes, me thinks another RE agent specuvestor has arrived on site.

Stop it Piggy our hospitals are in bad shape and cannot cope with hundreds of DGM's having heart attacks.

So 1184 per week out of a combined income of 2000 what happens if couples wants a baby or one is out of work for a period on top of this mortgage payment food rates water petrol power has to paid. For a young couple this is a crazy amount of pressure, just wait as house price’s will take a bigger tumble over next few years the people who purchase 18 month ago are already down 20%

Simple don't have kids. You won't believe how less stressful life is without them, basically they totally wreck you because 90% of them are little shits these days anyway. Why put more people on a totally overpopulated planet ?

Zwifer you are the scarecrow and tin man all in one no heart or brain.

As someone with no kids myself, I understand where Zwifer is coming from. But I also recognise in myself that those words come from a place of fear, wondering what life is going to be like down the track on your own.

The problem is, you can’t live both lives to compare, so you’ll never know which is better. Just gotta do what feels right.

Saw an interesting doco by someone who studied collapsing demographics all over the world. Turns out, over the last few decades the average number of kids (in families with kids) has stayed around 2.something. What has changed is that it used to be one woman in 20 who did not have kids. Now its one in three.

Funny how people see the world so differently. Kids are worth more then all the money in the world. As an older parent who has traveled the world. It is best thing to happen to me. When you get older you get more cynical and nothing excites you as much. But with children they have an excitement and joy that you can share in. You also learn that life and happiness is more about giving then receiving. Without children you only focus on yourself, it's a mind change, that's changed my life. I also have children that can take me fishing and clean the boat, then go for a beer. Not sure about you but it's the simple things in life and my kids help with that. Life will be lonely if your older with no family, you can't put a value on that.

6 out of 10 properties sold at the B&T auctions today. All got reasonable prices considering the market conditions.

very good compared with what they might get in 24 months good on them for getting out

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.