The housing market has made a very slow start to 2024, with January's sales at their second lowest level in at least 32 years.

According to the Real Estate Institute of New Zealand, 2995 residential properties were sold last month.

Interest.co.nz's property sales records, dating back to 1992, show the only time the number of homes sold in a January month was lower than it was this year was in January last year, when 2855 properties were sold.

And both of those months were the only times January sales have been below 3000 since 1992.

To give an idea of how much sales numbers have fallen over the last year or so, there were 3761 sales in January 2022 and 5135 in January 2021.

The record number of January sales was in 2003/04, when more than 8000 properties were sold in each of those months. Sales numbers have been in more or less steady decline ever since. And looking at the latest figures, it's hard not to conclude that the slump in sales that dominated the housing market last year appears likely to continue this year.

Last month's low sales numbers are particularly concerning because the amount of houses on the market for sale is running at high levels, so buyers have plenty to choose from and are under less pressure agree to a price when they find a property that suits their needs. That situation will likely make for some hard bargaining over price.

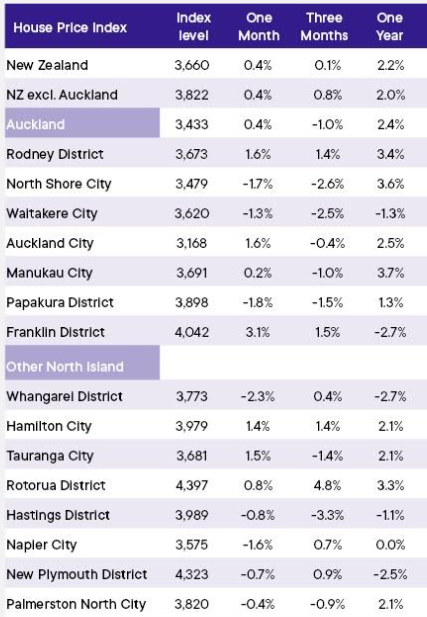

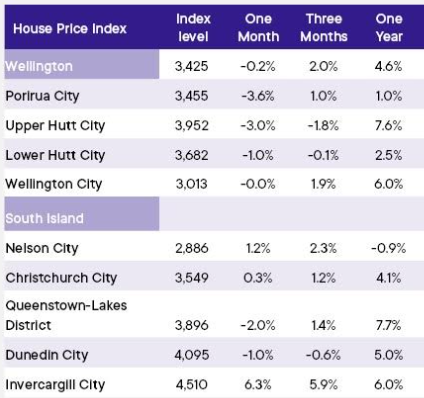

Price movements were mixed last month, with the REINZ House Price Index showing declines in prices in 13 of the 24 main urban districts it covers, improvements in 10 districts and no change in one. (See the table below for the full figures).

The REINZ's national median house price was $760,000 last month, down 2.5% compared to December 2023.

In the critical Auckland housing market, the median price dropped back below $1 million last month to $975,000, down 6.7% compared to December last year.

The number of sales made in Auckland last month was down a whopping 17.2% compared to January last year.

"Despite the wave of listings favouring buyers, the challenges of last year, including the cost of living, inflation, interest rate changes and government reforms, mean some buyers remain cautious," REINZ Chief Executive Jen Baird said.

"However, most regions are reporting more buyer activity across the board, with some seeing a particular surge in first home buyer interest.

"Vendors are also being confident but realistic with prices as activity increases over the summer months.

"This is likely to resolve in inventory moving over the coming more active months in the year," she said.

The comment stream on this article is now closed.

REINZ House Price Index - January 2024

Volumes sold - REINZ

Select chart tabs

Median price - REINZ

Select chart tabs

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

126 Comments

Might be slow in the North Island, but the south Island is going crazy. The reporting is very Auckland centric.

No problems in many parts of the North Island, sold signs still out, looks pretty normal out there to me.

You read the article right?

"Interest.co.nz's property sales records, dating back to 1992, show the only time the number of homes sold in a January month was lower than it was this year was in January last year, when 2855 properties were sold."

"Last month's low sales numbers are particularly concerning because the amount of houses on the market for sale is running at high levels"

To hell with facts, I've walked down my street and seen a couple of sold signs so extrapolated that to the whole country.

Likewise, I hear a certain RE advertisment about 27 times a day stating all is well and they are preparing for the market to "take off", who am I to argue.

"To hell with facts, I've walked down my street and seen a couple of sold signs so extrapolated that to the whole country"

An example of cognitive dissonance. For the highly leveraged, it can be used as a coping strategy.

"The discomfort is triggered by the person's belief clashing with new information perceived, wherein the individual tries to find a way to resolve the contradiction to reduce their discomfort"

The data does not support your assertion.

Purely anecdotally, here in Chch it seems that:

- FHB- friendly properties are selling faster than Taylor Swift concert tickets. Have a couple of younger family members who are in that FHB stage and every open home seems to be packed, multi-offer scenarios etc (particularly for anything that isn't a Williams Corp-type new build).

- Good school zone family sized properties selling fine.

- Properties that sit higher than FHB level but aren't in the desirable school zones seem to sit. There's a guy private selling a really nice house down the road from ours - 3 bedroom, 3 bathroom, big garage, solar system, ducted AC all sorts of stuff for a "reasonable" (by current market standards) price and he's had no takers after about 30 open homes. It's too much for an average FHB, and not big enough for a large family or one where schooling is critical as the local schools are a bit iffy.

- No idea what is happening with the higher end (1.25 mil plus) stuff as that's not the space I'm interested in.

I've got a bunch of properties on my TM watchlist that have sat for weeks, months now with price reductions and not selling but none of them are FHB suitable, investment suitable or "family home in the zone".

A good summary. The 1.25mil + market is slow with most buyers reluctant to buy a dollar above the 2022 rating valuation. People are looking for renovated properties and re scared off by the cost of trades and materials. Units and townhouses (old and new) have taken a big hit, due to oversupply, and even at current prices yields don't stack up for investors. Investors buying in Christchurch at the moment are buying under 4% gross yield for the average unit/townhouse. Freehold freestanding purchasers are getting an even lower yield on purchase.

A 2 bedroom house a couple of streets down from me went on the market, open home was busy with midlifers/retirees looking to downsize but it didnt sell at deadline as it turned out they wanted $300k more than the CV (CV was $1.7M). It has sold though, will wait to see for how much. Seems that there are still people prepared to pay $2M for a 2 bedder in a good street.

K.W.

Given what you see and know, what have you done with your property portfolio?

I dont have any debt so not fussed. Waiting to see if the new Govt will change the tenancy laws, to decide if I sell or rent my currently empty property.

Word from agents in Hawkes Bay is anything under $650K can barely be listed before it's gone, while anything over is a much harder sell. TM listings for the Bay are rapidly approaching 1100, which I've never seen in 15 years of monitoring.

That may be consistent with the buyers market leading the sellers market downwards?

If most people can only afford to pay max $650k, when previously that figure was $800 to $900k, then that's where they'll be shopping. Eventually the market adjusts downwards. High interest rates pretty much have an instant effect on future borrowing, vendor expectations are another beast all together.

Vendor delusions…

Here in NP, my observations.

- Listings are up, particularly the 2-3 year old McMansions and lifestyle blocks.

- Saw the first mortgagee sale a few weeks ago, followed by another this week (for context haven't seen one in the last 12-18 months)

- Asking prices appear to be dropping.

- Houses staying on the market for longer

but, there are still houses selling for above market. Ultimately the state of the house/location appear to be holding value.

Seems to be running as expected. Newer/higher priced houses on the fringe of the city are struggling. Houses closer to the city are holding value/increasing.

Many in the FHB category are looking to take advantage of the Home Start/First Home Grant (you'd be nuts not to if you qualify!) - and so the price caps are important to understand when targeting sales at that local market;

https://kaingaora.govt.nz/en_NZ/home-ownership/first-home-grant/house-p…

Of course. I recall that grant/scheme from 2019/2020 when my wife and I were looking for our first home.

However, because I'd had a good year with my business our HHI exceeded the cap so we couldn't take advantage of it.

What I recall at the time (and I presume still true now based on data and anecdotal feedback) is that when we looked at properties under $500k - which was the cap at the time if i recall - the open homes were always packed, every single property was a multi offer or auction scenario and it was very stressful.

I remember going with the in laws to a first viewing open home one Saturday morning - we got there at 10.05am, it had opened at 10.00am and the agent informed us they had already had two offers on the spot and multiple made in advance of even seeing the property. It was a done up villa-type house with nice millennial-white finish in a good school zone for $500k on the dot. That was just one example of the same phenomenon.

We decided in the end to spend more (closer to $600k) as we couldn't get the FHB grant anyway, and the experience was so different. Sometimes only people at the open home, we had choice of a number of nice properties and got a very good home without all the stress.

Vendor expectations still higher on average than the market is willing to meet. There’ll still be sales but anecdotally spriuker articles are a being quoted by those downsizing and thinking they’ll still get 2022 prices

No way bro everyone on here thinks the whole NZ market is screwed.

The West Island is doing extremely well. We sold my late mum and dad home for 710k in 2021. It's now listed for 1.2mil after a new lick of paint and kitchen, no other major reno.

"It's now listed for 1.2mil after a new lick of paint and kitchen, no other major reno."

Can you provide a link to the listing?

Will be interesting to see what it ultimately sells for vs the vendor's asking price.

ummm, not this time Batman, I treasure my anonymous status!

We respect your privacy and anonymity.

Please keep us updated on the sale price when available.

A tide of change is coming and that is what you fear

The earthquake is a coming, but you don't want to hear

You're just too blind to see

Have you seen the writing on the wall?

Have you seen that writing?

Can you see the riders on the storm?

Can you see them riding?

Can you see them riding, riding next to you?

Based on the comments by commenters, a few can see the potential risk and vulnerability of a tsunami of sellers coming.

Most of the general public are oblivious. They don't know what to look for, or where to look. They don’t know what they don't know.

NZ housing data reminds me of the weekly reports presented back in the eighties on the condition of Ronald Reagan’s prostate gland.

LOL. Have an uptick.

The housing market engine has been stuttering.. it's about to shutdown..

Ground Control to Specu Tom

Ground Control to Specu Tom

Take your pepto pills and put your brave face on

Ground Control

To Specu Tom

Commencing freefall

Ponzi engines off

Check bank rates

And may Banks love

Be with you

Ha, ha, very good, David Bowie would be proud of you...

This is Specu Tom to Ground Control

I'm stepping off the ledge

And my specuvestment's falling far away

And my interest fix is ruining my day

For here

Am I sitting in my Cayenne

Tears beyond control

Portfolio's poo

And there's nothing I can do

HPI moving in line with 10% value increase this year. Rates coming down then give 15% increase next year. Happy days!

Congrats to Wellington, already 6% up on the calendar year!

Wellington City was revalued for rating at Sept 2021 - near the November 2021 peak of the market - everything presently is selling way below GV. And now they've updated their natural hazards maps as well.

It's a really difficult market to buy in to at the moment due to valuation uncertainty. If this government succeeds in its aims to downsize central government, then the whole region (incl. Hutt, Kāpiti and Porirua) will be affected. The million dollar question is whether QV will revalue them downwards this year. So, very buyer beware at the moment there.

NZ must be one of the only countries that have/use QVs RVs CVs HomeEstimates etc. When you look at the history over the 3 year periods, many have doubled in just 6 years. Agents say, "oh don't worry about them" unless it suits them.

When prices go up QVs go up, (rates go up) and then prices go up again. Annoying..

Yep. If we calculated the General Rate (which is only one component of your rates bill) on something other than property valuation - say distance from a main center of employment - and gave it a number out of 50 to assign a factor component to the General Rate calculation - we'd have to go back to the old way of getting a registered valuer into each home individually to put a value on the place for mortgage lending purposes.

QV/RV/GV/CV is one of the major scourges in our housing market. Totally, unnecessary and wildly misleading.

Who is your copium supplier? it clearly hits pretty hard.

If you were a real person and not a troll I'd bet a grand with you that's not going to happen.

P.S. : Côte d'Azur spells with a circumflex on the o

No amount of attempted hype from vested interests can overcome the simple fact that with interest rates hovering around 7%, prices are still too high for most - investors and owner occupiers alike. A median house with a 20% deposit for a FHB, you'd be paying just shy of $50,000 in P&I alone, and if you're a leveraged investor you're paying $53,200 in interest alone... Rent is not coming close to that, even with interest deductability coming back.

Prices are going nowhere fast unless rates come down a lot, even with high immigration.

Maybe it's the other way around. Interest rates did not matter, it was the house price explosion that drove the house price explosion. Classic bubble. Any idiot could make money. But that was then

And when (if?) interest rates go down why assume house prices will go up. The bubble might have no more puff.

I don't disagree there was a lot of FOMO and that it was acting like a bubble - but it could only do that because the low interest rates + interest deductability meant investors were able to leverage to ridiculous levels, thanks to a self perpetuating rise in prices. Because rent more or less covered the cost of owning, you could use the gains on your properties to keep buying more and more housing essentially "forever". However with interest rates so much higher now the negative cash flow from owning a rental property entirely on leverage, even with an interest only mortgage, means this is no longer possible.

I agree there's no guarantee prices will go back up if rates go down, but I think NZ's obsession with property investment plus the current government obviously having vested interest in prices going up mean there's still significant risk of the bubble re-inflating, unless there is a real burst that burns people bad enough to be properly scared of speculating on property. Who knows though?

Yes that's the standard explanation, but I suggested that what really drove property speculators was the expectation that anything they bought now would be worth $100,000 more next year.

But maybe there is a natural ceiling price which was reached a couple of years ago, and so interest rate drops might not light the fire that some here pray for.

DTI is critial to reigning in the specu stupidity. Even Hosk had a winge about it on his radio show this week.

Had the RBNZ not removed the LVR limits then we would not have had such a peak as it would have been limited by lower borrowing ability to pay such prices, and arguably to some degree this would have limited investor interest.

Interesting that people moan and groan about Government debt ballooning. But crickets when it comes to mortgage debt which has increased by $70b since Covid (RBNZ C32).

Sure, one is an accumulation of private debt, but whyyyy did we need an extra $50 - 70b of stimulus through the housing market? Makes the $500m cost overrun on Transmission Gully seem quite insignificant, and this extra mortgage debt could have built another 40 Transmission Gullys.

Interesting comment that last month’s sales are ‘particularly concerning’. Hardly objective. Not at all concerning for FHBs who will be hoping for more softening in the market.

If Auckland gets back to the flatline we had between 2016 and RBNZ inspired covid madness, then FHBs will be well served.

The flatline tend to hide the activity of FHBs which operate at the lower end and frequently pick up bargains if they keep their cool. Whereas the flatline is raised by over-enthusiastic non-FHBs, and the selling of trophy homes which tend to have been held for many years and sell above CV and release significant gross capital gains on the original purchase price. (In a few areas of Auckland the sales of trophy houses disguises the fact that non-trophy houses in that area are actually falling.)

FHBs should keep their powder dry, keep their cool and remain extremely discerning. There isn't any need to rush - in Auckland at least.

I don't disagree but of course with each passing month that FHBs wait it out, many are paying exorbitant rents. It really is not a young persons paradise.

The rents are still much much lower than mortgage payments.

And that's the investor dilemma, there's little yield opportunities at these prices, and it's not coming any time soon. Rent would need to double for yield to make sense, even at lower interest rates. The flip side is that to make it work, capital losses.

"Rent would need to double for yield to make sense, even at lower interest rates. The flip side is that to make it work, capital losses."

So given the current rent, to achieve the same required doubling of existing rental yield, prices need to fall by 50%?

Depends on what/where you are renting. Just anecdotal experience, but in AKL and WGN if you are not a university student or a young flatter (i.e., prepared to live in a dump and/or in a bad neighbourhood/school district) - then rents can very much exceed mortgage repayments, provided as a FHB you have saved a good deposit and/or are cashing in a healthy balance on your Kiwisaver, that is.

Lots of FHBs (mostly dual income families) in this situation with circa $1,000+pw going on rent payments and holding a $200K (20%) deposit on a million dollar home - but the house values are so inflated that what should be a million dollar home is sitting there with a GV of $1.5m+.

Here's a really good example of asking price vs GV in Wellington at the moment;

https://www.realestate.co.nz/42507710/residential/sale/70-owhiro-bay-pa…

But the problem for a FHB is that they'd need to be mortgage free as with the new coastal hazard designations one would need to self-insure and the banks aren't prepared to loan without a standard insurance policy.

Every which way you look at it - FHBs are being screwed - via monetary policy; via lending conditions; via insurance companies; via local regulators; via the building industry; via landlords; via those that 'got in' to purchase when things were fair/sensible prices .. you name it.

That’s only correct if a FHB has s very large deposit. Which is easier said than done….

I think your numbers might be a bit off for Auckland at least.

$1000 a week in rent is getting you a 4 or 5 bed property in a top location in Auckland. Same properties selling for at least $1.6mil. At current rates mortgage for the same house is double rent, and that is with a 360k deposit.

Doesn't make sense to buy for any sensible FHB at present, based on anything other than sentiment. The risk of deep recession should be enough to keep those feelings at bay.

Exactly. Kate was way off the mark

Might not be the case for AKL, but here's a selection of family-type homes in good school districts in Welly;

https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

https://www.trademe.co.nz/a/property/residential/rent/wellington/wellin…

Our rent was 40% of what our landlords would have been paying in mortgage - if they'd put down a 50% deposit 7 years earlier - and the house is now valued less than what they paid for it.

"Our rent was 40% of what our landlords would have been paying in mortgage - if they'd put down a 50% deposit 7 years earlier"

Extremely clear example of renting being much cheaper than owning. Remember that the owner occupier also has other costs not mentioned - rates, insurance, & maintenance.

My family would be about $1500 pm worse off if we were renting our home. Granted, I'm not a FHB and my deposit was close to 50%. But it is not always the case that renting is cheaper than buying today. The circumstances are different for everyone so do your own sums before deciding to buy or rent.

"But it is not always the case that renting is cheaper than buying today. The circumstances are different for everyone so do your own sums before deciding to buy or rent."

Yes, you are correct. People should do their own calculations for their circumstances.

For example:

An owner occupier purchasing on a 0% LVR (i.e 100% cash buyer) will be slightly higher than renting (due to maintenance, rates, insurance, etc)

An owner occupier purchasing on a 0% LVR (i.e 100% cash buyer) with multiple boarders / flatmates would likely be cheaper than renting.

Many FHBs are paying zero rent (e.g. living with parents) or paying the barest minimum by significantly compromising on their wants, e.g. boarding. If you're prepared to compromise there are cheap rentals or flat-shares just about everywhere. And couple up - and things get cheaper again.

The people who get stuck with higher rents are typically older and with kids and they need a more stable environment. Sadly this group is quite large.

Yep. My son moved in with his girlfriend. Now paying about $150pw compared to $275 pw for his own room in previous flat

Not quite sure the point - of course if you put two people in a single bedroom the cost of renting a room is halved.

I've seen a few situations where REA have put a trail of signs up to direct people to open homes that start a few blocks away. I expect to start seeing them go up next to the motorway off ramps next.

And both of those months were the only times January sales have been below 3000 since 1992.

And to understand just how slow that is - one needs to be mindful that back in 1992 our population was a lot smaller and (as I understand it) building growth has not kept up with population growth.

How strange, I am not seeing this reporting on NZME.

Maybe they are in a editorial meeting to determine how spin this as good news.

They will hate the Fletcher developments too.

All of these outfits are intertwined as part of the great NZ housing ponzi

If you look back to the 1970s many councils in Auckland opened up significant new land for development. And up until the creation of the 'super city' councils on a piecemeal basis opened up new areas. Almost always, they were 'green field' sites that used to be farmland.

Guess what happened? Prices in those areas flatlined until the land was filled up with land-wasteful single dwelling houses which was all council would allow. (One needs to break down dwelling prices by where these large developments were to see this. Using 'whole of Auckland' figures hides this.)

Now we have one of the biggest ever re-zonings in Auckland's history that was achieved in 2016. Unlike past foolishness where farmland was turned in suburbs of land-wasteful single dwellings, the bulk of new capacity for more dwellings is on 'brownfield' sites. I.e. where an existing dwelling is situated but is now 'allowed by council' to have 3, 4, 10 or even 100+ dwellings.

Can you guess what will happen?

A site that can be intensified is rated higher, and should carry a higher value vs one that cannot be. Makes sense. That said there is still the development math to make any project stack up and the affordability of the finished product. Specu land expectation is killing that off currently.

re ... "A site that can be intensified is rated higher, and should carry a higher value vs one that cannot be. Makes sense."

To be honest, I'm just not seeing that at this time. While many buyers are valuing the house, developers are valuing a developed site. And there have been a plethora of sales of 900+ sqm sites that have gone for a song because the house is a dump. This suggests developers are stepping back. No surprises there. I am too. As you say, the maths isn't great if you need borrowed working capital. And the maths is disasterous if house prices keep falling ... And once the NACTF re-instate interest deductibility for non-new houses it gets even worse.

I made the same observation of a derelict home recently. Fairly well sized section, offers around $450-$550k, and even then I thought it would be too steep. One nearby in slightly better condition was sold and bowled a few years ago for well over $1m.

Land prices, ain't what they used to be.

re ... "Land prices, ain't what they used to be."

Like I've said - NZ's housing market is none too bright.

re ... "One nearby in slightly better condition was sold and bowled a few years ago for well over $1m."

If it was bought by a developer, I would guess that they needed the rental income to help cover the mortgage before the build got underway. Also, they could have struggled to get the mortgage in the first place if the house wasn't in good enough condition to sell quickly if the bank came a'calling. (Banks are dumb like that but developers with good track records - 20 years plus - get better treatment.)

Agreed, inflation driven reality in development costs and buyers ability to pay for end product can only drive underlying land prices south. The last wave of development only worked because interest rates had a "2" in them. So we agree, simply does not stack up.

Greg says it plain. Note the last sentence.

".....Last month's low sales numbers are particularly concerning because the amount of houses on the market for sale is running at high levels, so buyers have plenty to choose from and are under less pressure agree to a price when they find a property that suits their needs. That situation will likely make for some hard bargaining over price....."

Most people couldn’t afford to buy the house they are in at these price levels even with the 20% drop from highs. To buy average home in Auckland you would need a deposit of 180k and household income of 250k this is double the average household income. To me it obvious the next phase of housing price crash has started.

Loving the tussle in media and this chat. Hosking/Church ramping one day and bears in with real data the next. We still have DTIs coming in a few months. Perhaps that is why ramping stock markets is illegal in other countries. Ramping the housing market should be illegal here too. It is just the overinvested trying to get out.

Difficult to get that sort of progress when you have a bunch of entitled speculators in parliament

Which raises the question:

Can the OCR be dropped a tad without the housing market taking it as a sign that rates will be going back to RBNZ covid inspired foolishness?

A few things to consider:

- the collective housing market is as dumb as dirt (covid showed us that) thus risks are not insubstantial

- a moribund housing market where buyers are standing back waiting for further falls makes for a dangerous financial situation with significant collateral damage

- many livelihoods are attached to the building, owning and selling of houses and most of these people are well outside the top 20%

- Holding the OCR higher comes at significant cost to NZ Inc as the RBNZ pays out interest to hold these levels high.

- A high OCR makes the already wealthy even more wealthy at the expense of the young / indebted

- Retail banks in NZ will take months to pass on any cut

- The RBNZ needs to take great care that it is not seen as implementing any 'social policies' that are not expressly in their remit (e.g. affordable house prices)

The RBNZ should cut IMO.

A 0.25% reduction with a strong message about any silliness will be soundly dealt to with a 0.5% rise.

Your critical error here is assuming the OCR is currently high. It isn’t. It’s about right, if anything too low. If you went into the money lending business would you be happy charging only 5-6% interest?

It's not a 'critical error'. It is a difference in how you and I understand the current rate of the OCR.

And the RBNZ (and many other economist, even bank economists) is(are) in agreement with me.

In the RBNZ's last MPS they say:

The neutral OCR is the rate that, on average over time, would neither stimulate nor constrain the economy, and be consistent with no over- or under-utilisation of resources and stable inflation in the economy. Based on our neutral OCR indicator suite, we have revised our estimate of the long-run nominal neutral OCR from 2.25 percent up to 2.5 percent from the December 2023 quarter onwards The increase in our neutral indicator suite primarily reflects that long-term interest rates have increased substantially since the end of 2021. The OCR remains contractionary at its current level based on this revised assumption. Taken on its own, the upward revision to the neutral OCR creates gradual upward pressure on the OCR over time.

Source: https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/…

Sorry Frank - but I get sick of such statements.

Just to add - this number is under review each MPS so it could go up or down at the next one. I wouldn't be surprised if it goes up to 3%. (Messaging is everything.)

Not sure that Frank was actually thinking about this in any great depth, but his statement isn't necessarily wrong based on the facts you've presented.

It's quite plausible that even though the current rate is contractionary, the magnitude of contraction is inadequate. The RBNZ would consider an OCR of 2.75% to be contractionary based on their assessment of the neutral rate, but obviously don't consider that to be adequate.

If the real neutral rate is trending back upwards (which the RBNZ seem to believe) after decades of decline, then the OCR is likely to remain high in order to keep inflation in its target band, no?

Happy to be educated, as I'm very much a beginner when it comes to economics!

Thank you Harlow, I think. Today’s day trading has closed but my day drinking has rolled into the evening and I’m pretty buzzed out. The alcohol, along with trying to keep up with all the comments on this great website, has taken its toll.

the nz day time is night time in us... you are a night trader..... live and learn

re ... "It's quite plausible that even though the current rate is contractionary, the magnitude of contraction is inadequate."

We'd all like inflation to come down. But is a contraction actually required to do it? What about an expansion that increases supply instead? The US economy had plenty of spare capacity as they exited covid and that additional supply is one reason the US economy is looking weird with growth just trucking along while inflation falls. This is especially obvious in US energy markets - lots of unrecognised capacity came on stream as the economy grew.

Let's leave that one for a moment and assume for the sake of this argument that a contraction is necessary.

How fast do you want inflation to come down? Remember the economy is like a massive oil tanker and can not adjust course quickly. Would, say, a 15% OCR bring inflation down more quickly? It probably wouldn't. Raising interests is itself inflationary and a rise that large - in the short term - would not only result in further inflation, it would start a massive contraction akin to a Depression. Over the medium term, people would save rather than spend, furthering Depression like conditions. And there would the inevitable transfer of wealth as those with wealth buy up stuff at rock bottom prices as businesses fail around us. (And land and houses likewise.)

So where should it be to bring down inflation in a reasonable time frame and without too much damage to the economy? The answer to this lies in the target rate of inflation. A 2% inflation target largely suggests an OCR about 0.5 to 1% above would be enough to ensure inflationary spending will be kept in check because borrowing money costs more than what inflation gives back in nominal terms. Or put simplistically - the target inflation rate sets the neutral rate. And anything above the neutral rate will see contraction.

It's worth mentioning too that higher interest rates - driven by an OCR higher than the neutral rate - also reduces investment in further plant and machinery (and the building of new houses).

re ... "If the real neutral rate is trending back upwards (which the RBNZ seem to believe) after decades of decline, then the OCR is likely to remain high in order to keep inflation in its target band, no?"

I've mentioned before why NZ's interest rates have been declining. It's mainly to do with overseas lenders trusting NZ Inc. not to let politicians back in charge of monetary policy. Thus they accept a lower 'risk premium' in lending to us. The RBNZ's tweaking of the neutral rate from 2.5% to 2.75% is IMO mainly about messaging. As I said above, with an inflation target of 2% the neutral rate of the OCR should be 0.5% to 1% higher. If the RBNZ comes out with anything higher then they'd need to explain why.

If one looks carefully at the RBNZ's rational for lifting the neutral rate (see CHAPTER 6 Economic projections in the link above) many of their predictions seem a little off now. I've no problem with them talking down inflation and lifting a vague conceptual factor like the neutral rate of the OCR to send a message, i.e. don't spend up big because OCR cuts are on the horizon as the cuts may be few and far between. But if they persist with this rhetoric when empirical evidence shows otherwise, then they'll lose what credibility they have left.

You don’t deny making assumptions then?

Assumptions about what?

If RBNZ cut rates the NZD will tumble very quickly adding to inflation so this will not happen until US FED lowers rates but looking at US bonds this could be some time away.The NZD is already down 13% from average over previous few years.

Where do you think the NZD will go if we're into a period of negative and/or serious sub-par growth because the high OCR is crippling NZ Inc.?

BTW - can you surface any empirical data that there is in fact direct relationship between Fed rates and NZ rates and the NZD? Most of what I've seen on this relationship is from FX pundits and researched papers are far more circumspect. Outside of geopolitical ructions, what is happening to our exports prices seems to have a far greater influence.

Exactly

The housing sector avoided it medicine during the GFC due to the panicked suppression of interest rates. Unfortunately for society this has lasted for over a decade. Yes a lot of activity and ticket clipping is engaged in this area, but as a sector it has bloated into something that is crushing society via fueling of inflation and inequality. The only winner has been bank profit and the risk proxy specuvestor. Inflation still pumping. RBNZ do your job.

Yes those that cleared debt and horded cash against populist opinion waiting for this sea change, aka the non excessive risk taker, are poised to do ok.

- A high OCR makes the already wealthy even more wealthy at the expense of the young / indebted

No it doesn't, the wealthy are proportionately more indebted than the poor (largely because you need significant assets to secure any kind of significant debt).

It's blindingly obvious that the low interest rates in 2020-21 caused a massive transfer of wealth towards existing asset holders and that the subsequent normalisation of the OCR has reined that in. The narrative that we need to lower the OCR for the sake of the hardworking poor is breathtakingly dishonest.

re ... " the wealthy are proportionately more indebted than the poor "

And you can back up that assertion on a DTI basis? I can wait.

re ... "The narrative that we need to lower the OCR for the sake of the hardworking poor is breathtakingly dishonest. "

Since when is a fact dishonest?

HGWR,

Utter crap. Back it up with some facts, not your prejudices.

If interest rates halved tomorrow, house prices would rise. People who own houses, generally have more wealth that those who don't. So the wealthy would get a large increase in their net worth in dollars.

The non homeowners would become further away from being able to buy themselves, as the minimum deposit required gets ever larger, and the amount required to borrow skyrockets. Low rates are not guaranteed, making any new buyers at higher risk of rates rises.

Therefore inequality increases. That is how I understand it.

You understand it well.

re ... "If interest rates halved tomorrow, house prices would rise."

Current 1yr mortgage rates are 7.4%. I can't find anyone suggesting they need to fall to 3.7%. Can you?

But I guess your point is that any fall in interest rates will lead to house price rises? This isn't the case at all. If supply increases to meet demand prices can, and most likely will, flatline. (See my comments 2016 AUP, NPS-UD, REINZ Auckland flatline between 2016 and RBNZ inspired covid madness)

re ... "People who own houses, generally have more wealth that those who don't. So the wealthy would get a large increase in their net worth in dollars."

I think your definition of what wealthy is, and what mine is, is the problem here. I was referring to the top 5% who don't own houses (their vehicles own them) and their core wealth is certainly not held in a single house, or even a few investment properties. Owning your own home - even mortgage free - doesn't make you wealthy - just ordinary.

re ... "The non homeowners would become further away from being able to buy themselves, as the minimum deposit required gets ever larger, and the amount required to borrow skyrockets. Low rates are not guaranteed, making any new buyers at higher risk of rates rises.

Therefore inequality increases. That is how I understand it."

Taken isolation what you said sounds correct. And 7 people gave you a 'thumbs up' for it.

But as in most things in economics it can't be taken in isolation.

What if wages rise faster than house inflation? (Yes this happens)

What if more houses are added to supply? (This is happening throughout NZ)

What if the RBNZ gets stuck in with LVRs and DTIs? (This will happen if rates get down to 3.7%)

What if our useless governments finally get around to addressing the tax advantages an 'investor' has over an owner occupier? (We might even see this from the NACTF!)

Or even - god forbid! - what if our useless governments start rebalancing our tax system? (This has to happen. But when? God only knows.)

A high OCR makes the already wealthy even more wealthy at the expense of the young / indebted

This is such a narrow minded view. You try being a saver for the past 10 years and see how wealthy you are. Hint: I can't even afford a deposit on a house. So it's not very.

Who you're really blaming is those at the top of the pyramid so you're a fool for trying to climb it after them.

It appears that interest rates aren't going to fall as quickly as the market was anticipating last year. So investment properties aren't going to make any sense for longer, then we are hitting the drop to 2 years on the bright line in mid year.

Wouldn't it make sense for some investors of long held properties to sell out now before the rush in mid year?

Or do we have enough immigration that rental yields don't matter because there will be capital gains regardless?

The headline immigration figure isn't what should be considered for capital gains - though it will raise rents slightly, not enough to make that yield equation work. What you should consider as new demand for housing is new residency, as residency is needed to buy, and those figures are dropping like a stone.

"It appears that interest rates aren't going to fall as quickly as the market was anticipating last year. So investment properties aren't going to make any sense for longer, then we are hitting the drop to 2 years on the bright line in mid year.

Wouldn't it make sense for some investors of long held properties to sell out now before the rush in mid year? "

Those owners with expectations of house price growth and rapidly falling mortgage interest rates may choose to hold on.

Seen one non owner occupier owner say that they expect house prices to double as base case, triple as their optimistic case by 2030. Given these house price expectations and if they're in a position to hold on they may choose to hold rather than sell.

There may be a number of other property owners who expect house price growth based on extrapolations of recent house price trends or believe in Tony Alexander's house price forecasts of house price growth of 10% this year with 15% more to come next year.

https://www.oneroof.co.nz/news/tony-alexander-expect-10-house-price-gro…

Bank economists are forecasting house price growth this year I believe. Haven't seen any economist forecasts of house price falls, so there is general expectations of house price growth and that house prices have bottomed.

Then there are the property promoters with their vested financial self interests and their ongoing property promotion activities repeating their narrative.

There is also a group of property investors that are aiming to own 10 investment properties for wealth creation as promoted by property mentors. They are likely to be focussed on reaching their goal and be oblivious to potential house price risks. Some of these people may have been buying in the 2021 - 2022 period.

FYI, a summary of economist's forecasts for house price growth in 2024 can be found here

https://youtu.be/p-jSj3a5Dko?t=226

The median is 5.2%, with the range from 2.0% to 8.0%

I saw in the news that the build-to-rent sector is asking for tax breaks (depreciation) to make it worthwhile.

Obviously they haven't read up on the comments section on Interest.co, otherwise they would know that as profiteering slime they should be grateful for the long term potential for capital gain and the opportunity to provide housing.

New Zealand - A country where most of the politicians are property investors. Most of the media are property investors. Our reserve bank employees move on from mismanaging our collective finances to well-lined jobs with foreign banks making a mint out of our property market. Banks that the reserve bank funds with NZ tax payer money at a huge discount.

The people who work productively and rent are taxed highly. The people owning the property and renting it out are hardly taxed at all.

It is perverse, almost feudal. Tear it down and rebuild. "Fīat iūstitia ruat cælum -"Let justice be done though the heavens fall."

It does have some interesting parallels to the Enclosure Acts in England, and the economic instability and vulnerability the de-landing of many those similarly achieved. Made them prime fodder for 100-hour weeks in factories, obviously, in their desperation.

Taking affordable housing left by the efforts of postwar generations and using it to extract wealth from following generations has been despicable policy, the real policy of entitlement.

Yet, strangely, people complain that poor indebted home owners have to pay the rich wealthy renters who have saved their money. And OCR must come down to stop this 'injustice'.

Who are the rich ones again??

Hmmm the question who is paying tax to fund govt services?

Person with cash in the bank is. Specvestor will be doing all they can to avoid tax on a capital gain.

Who is the real citizen...

median house prices tracking down while house value measures (HPI etc) are tracking up. This means more lower end houses are selling.

It tells me that buyers are lowering their house expectations rather than vendors lowering their price expectations.

Time will tell.

What would the financial media including interest.co.nz do without the constant stream of articles on property? As was once said, NZ is a property market with a small economy tacked on.

Imagine a whole week with not single mention of our grossly overpriced, all too often badly built houses? No, I can't either sadly.

To have buyers increase you need people to agree that their place is worth less than believe, deluded wise, it is worth. They take 12-18 months to get this.

Doesn’t matter how many listed. Turnover is issue. Until rates fall 2% the sales will continue to be abysmal

During the GFC watched the directors of a large RE firm addressing their staff. Key messages -1) "say whatever you have to to get the listing, and 2) then condition the buyers over the journey to accept less. All about sales or no one gets paid". The pressure put on sellers during Auction to meet the market in the small rooms next to the auction floor was bad. Would not want to be a supplier to one the the large RE shops while turnover is a dribble. They will expect everyone else to take a haircut, except themselves.

They have Neuro-linguistic programming training materials in how to have discussions, such as "do you need to sell this house or are you merely testing the market", I have some of these, they are great .....

"A-B-C. A-Always, B-Be, C-Closing." - Glengarry Glen Ross.

Not just real estate agents, or sales people employed by real estate developers.

Also mortgage brokers (who have rebranded themselves as mortgage "advisers" to give an impression of trustworthiness & respectability to their clients)

Remember the reports of mortgage brokers suggesting to their clients to include income from non existent boarders or flatmates to inflate and overstate income in borrower mortgage applications? To me, that behaviour is far from being honest or trustworthy.

A little reminder on change since peak in AUCKLAND

- AUCKLAND Peak $1.30M Current $975k -25%

- Auckland City -36%

- Franklin -19%

- Manukau -21%

- North Shore -25%

- Papakura -28%

- Rodney -20%

- Waitakere -27%

And these numbers are before the impact of inflation since Nov 2021.

2.25 years of inflation might deflate these prices by say 1.14 - 1.16 (14-16%)

https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

Remember this is also before the impact of leverage.

Crash? What crash?

Reminder:

What were property market commentators saying at or just after the peak?

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/life-style/homed/real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

Lies, damned lies, and statistics. Shame none of these are capable of being held accountable for their 'influence", which is not insignificant when magnified by the Press. A press that is compromised by its advertisers. Adverts from the ticket clippers, the commission takers.

House builder, Compass Homes (Franklin) - “The company hasn’t made a sale for 12 months,” he said of a desperate situation.

There is supply but an absence of buyers (at current sales prices).

https://www.nzherald.co.nz/business/house-builder-compass-homes-frankli…

Remember those with their vested financial self interests repeating the narrative - increasing population results in higher demand, higher house prices?

lowest sales in 30 years and if you have green shoots, pass the dutchie from the left hand side

Normalization of the cost of debt is the weed killer for green shoots. Ingest your poison in blind belief.

Oh well. I guess that's what happens when the cost of building chases borrowing power on the way up. It starts off with the builders who are the last in line to claim their share of the price gouge pie. The costs in all other stages of building are already sunk and locked in at peak (low interest rates). Assume they have very little room to move compared to other parts of the supply chain.

FYI, there are currently 5,734 new builds listed for sale in NZ listed on trademe.co.nz

Over 3,000 of these are located in Auckland.

A further 939 are located in Canterbury

We sold before Christmas while the market had a lack of listings in our area. December and January listings for good new houses were pretty soft in the auckland region but definately a lot of listings after waitangi weekend and some good properties.

At harcourts auction room in north shore today it was pretty quiet. Great properties were selling but nothing like 2018 when there were loads of bidders on each property and lots of Chinese offers. 2 or 3 bidders was the norm with a lot of properties only having conditional offers.

Good properties (renovated) and good school zone or view are selling for CV or above. Other stuff seems like a very hard sell.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.