The ability of aspiring first home buyers to scrape together a 20% deposit is probably now the key determining factor of whether they can afford a home of their own.

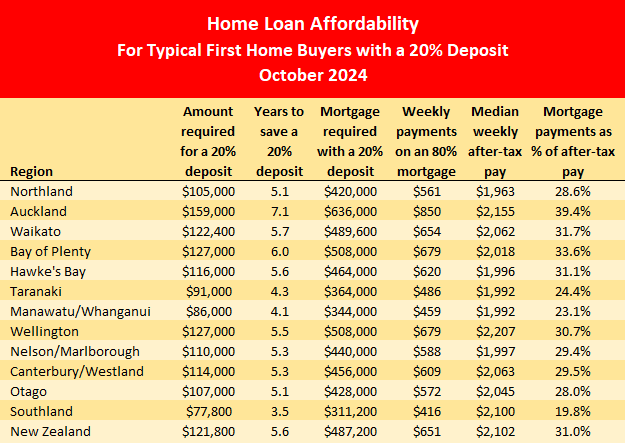

The latest home ownership calculations by interest.co.nz show the amount required for a 20% deposit on a home purchased at the Real Estate Institute of New Zealand's national lower quartile selling price in October, would be $121,800.

Around the country the amount required for a 20% deposit at October's lower quartile selling price would range from $75,000 in Invercargill, closely followed by Whanganui at $81,000, to a massive $203,000 in Queenstown.

Around the regions, you would need $159,000 for a 20% deposit on a lower quartile-priced home in Auckland, $127,000 in Wellington, and $114,000 in Christchurch.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing fairly modest dwellings at the bottom end of the price scale.

Interest.co.nz also calculates what the mortgage payments would be on the resulting 80% mortgage and compares that with the after-tax income for a young couple (based on the median rates of pay for 25-29 year-olds) to see how much of their income would be eaten up by mortgage payments.

Mortgage payments are considered unaffordable if they take up more than 40% of after-tax pay.

The latest mortgage calculations are based on the average two-year fixed rates offered by the major banks in October (5.68%) with a 30-year term.

Using that formula, the mortgage payments on a lower quartile priced home purchased with a 20% deposit would range from $401 a week in Invercargill to $1085 a week in Queenstown.

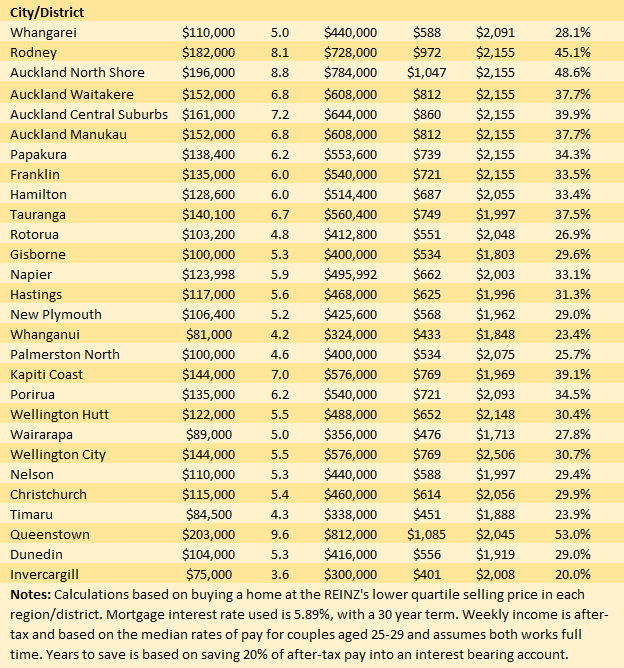

Within the Auckland region they range from $739 a week in Papakura to $1047 on the North Shore.

When you compare the mortgage payments with after-tax pay for the aspiring first home buyers, this shows there are only three urban districts in the country where the mortgage payments would be considered unaffordable for young couples on average pay. They are Rodney and the North Shore in Auckland, and Queenstown.

Mortgage payments everywhere else would be below the 40% of income threshold that would make them unaffordable for young people on average incomes. However, Auckland at 39.5% overall is on the cusp of becoming unaffordable even for buyers with a 20% deposit.

So for the ever-hopeful first home buyers, the main obstacle they face in gaining home ownership is not being able to afford the mortgage payments, it's being able to get a 20% deposit together.

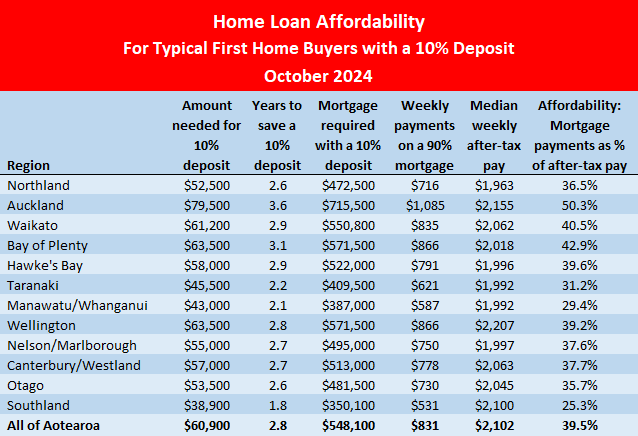

Of course they would have the option of buying a home with less than a 20% deposit and a low equity mortgage.

The problem with that option is that not only would they need to borrow more to cover the shortfall in the deposit, they would also be paying a premium for a low equity loan, which would significantly push up their mortgage payments.

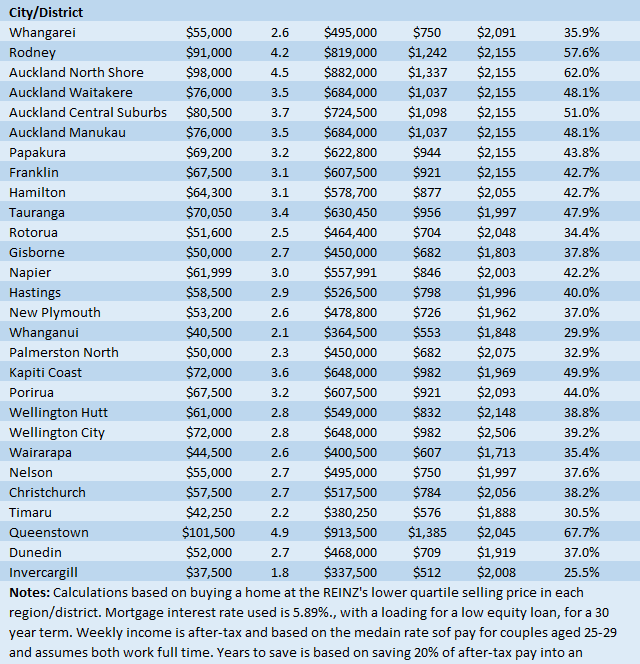

For example, the mortgage payments on a lower quartile-priced home in Hamilton would jump from about $687 a week if it was purchased with a 20% deposit (affordable), to about $877 a week. That's an extra $190 a week, although the exact amount will vary from bank to bank, pushing it into unaffordable territory.

That would mean all of Auckland, Hamilton, Tauranga, Napier, most of the Wellington Region, Nelson and Christchurch would join Queenstown in the unaffordable basket for typical first home buyers with less than a 20% deposit.

The two tables below display the main affordability measures discussed above, for typical buyers with either a 10% or 20% deposit, in all of the country's main urban districts.

The comment stream on this story is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

97 Comments

We are almost at the point where no one can afford a house....

So this is what success looks like in NZ

Isn't there a big crash coming?

Hard to say but people shouldn’t get comfortable (Auckland council moves to amalgamate back office functions across independent authorities like Auckland transport and Watercare)

Thats the concern for these first home buyers.

They’re incredibly vulnerable

The metric of resources that have been syphoned off for deposits on inflated house prices and attendant demands for rental/mortgage payments must be staggering. And yes, social cohesion also seems to likewise be being syphoned away.

More like we are at the point where no one is silly enough to spend the next 40 years paying banks interest for a new low quality garage style chicken coup (or vintage wooden tent).

Better to rent and invest the 20% deposit in stocks, startups, financing a local business - anything that is a vehicle to financial independence - and just rent. No ownership costs and employment location flexibility is worth more than being locked into a wealth sapping 'investment'.

No need for a house if you can't afford to get married or have children even on above median salaries.

We are almost at the point where no one can afford a house....

October saw a record high for FHBs withdrawing money from KiwiSaver to buy homes.

To add to that, RNZ reported on 7 November ....

"First-home buyers have been responsible for 27% of all purchases in the first nine months of this year, well above the 21% long-term average".

For the month of October Core Logic reported FHBs bought close to 28% of the houses.

Of a small total number of sales.

Does anyone have the number of sales? Core Logic reports this for October: Property sales activity increased by around 16% in October compared to the same month a year ago, which was the 17th rise in the past 18 months. However, volumes remain 10-15% below normal for the time of year. There are plenty of listings available on the market, so the relatively low levels of sales are more about buyers – those who still feel confident about their jobs and can get the finance are in a position to take their time and secure a deal in their favour.

Just think how that same money could have been invested in building a sustainable productive nz economy.

Instead it pushes up house prices and drives more smart kids overseas.

We are shooting ourselves in the foot economically and socially.

For sure. And even though we used Kiwisaver to buy a house I'm not sure that we should have been able to do that because we raided our own retirement fund. Some commented that the $5k FHB grant (gone now via the Coalition) helped push up house prices but $5k would have had way less of an effect than Kiwisaver funds.

Your house IS your retirement fund. Once you are mortgage free you are able to live on Super, if you are still paying rent you are screwed.

Our house isn't our retirement fund, it's somewhere for us to live. We don't have a mortgage now so currently invest outside the property market and don't give much thought to relying on Super, although it will likely be available to us unless things change. You're not necessarily screwed if you don't own a house at retirement, it depends on a lot of things - where and how you live and how much your investments make you. For example, I know retirees who invested the proceeds of their house sale and now use the returns on that investment to top up their Super and they rent a small, modest unit in a small town and they prefer that to the costs they had when they were home owners and their funds are liquid.

The dumbest narrative, or the greatest propaganda ever, to have come out of the financial industry in the last 2 decades.

Weekly mortgage repayments in Auckland look to be the same as renting to me.

This is not just in Auckland. Paris, London and other european capitals are also very expensive

Auckland. Paris, London

One of these is not like the others...

Toowoomba, Auckland, Bristol. Now we’re good for comparisons.

Auckland is rated as a Beta+ global city. Bristol is a Gamma global city and Toowamba is not rated, probably because it only has a population of 145K.

Indeed! How about comparing us to other similar population sizes, well away from booming economic centres? I know personally 20% was entirely unachievable for our family on NZ salary vs costs of living, honestly it wasn't even close. I don't know how anyone manages to do it. We had to move overseas and are now getting ahead rapidly. In my own work team (approx 12), ALL of them own houses (whether single or coupled up) - the vast majority are in their late 20s - 30s, near major cities and they didn't have to struggle for years to get there. It was just the next logical step for them. I wish I could say the same for young kiwis, we deserve so much better.

By design though. House prices have crashed 20% in places if not more, so when interest rates dropped they become more affordable and that then increases prices due to greed and lack of supply, and people being able to afford to pay more. There are currently some great deals if you shop around on newer builds espeically..

For a while now it's been about affording the mortgage not the home. That's all these reports have been about since they started.

The wealthiest we've ever been in history and no-one has enough.

Many still can but it requires parental assistance. We are now very much a class society.

The numbers do not support your comment, last check over 5000 FHB a month are buying a house. I wish more of them were on here sharing their experience, it would certainly help outnumber the DGM's on here.

Not sure where you get those numbers from....there were approx 69,000 sales in the past year and i somehow doubt that FHB are the (almost) entire market.

"House sales rose 12.2% over the year to September 2024, with the annual total rising for six consecutive quarters to 68,817pa. Despite the continued rise, sales volumes remain low, well below the ten-year average of 78,315pa."

Maybe make it 5% deposit, boost the NZ (housing) economy.

NZ = super basket case.

This has been the case ever since the introduction of the LVR.

Tell me, which 25-29yo couple has been saving for their house for 7 years on a 25-29 income? Oh, likely none as they were not in that income bracket for half the preceding time!

There's a reason average FHB age is in the late 30s.

The survey is a nonsense and they stubbornly stick to that stupid assumption despite having had the flaw pointed out repeatedly. I am Not prepared to financially support the website for exactly this sort of thing. Why should I support stuff that’s fundamentally flawed. A compelling reason for sticking with it has never been provided

In addition to your valid points, many young couples also have big student loan debt well into their late 20s / early 30s

I can assure you that there seems to be plenty of first home buyers out looking at the weekend in ChCh, and there will be more very shortly.

It is not that difficult to buy in the happiest city in NZ.

Went to an in-house auction today and there were several affordable homes that sold but next to no first home buyers there?

I appreciate it can cost money to do the due diligence, but the best way to buy property is when you have no competition.

"I can assure you that there seems to be plenty of first home buyers out looking at the weekend in ChCh, and there will be more very shortly."

I can imagine you're top of the invite list for the boomer BBQs TM3.

Then proceeds to tell of no FHBs at the point of sale...

Because first Home buyers do not like buying at Auction, when this where they should be, less competition!

Love the Barbecues and socialising.

As for Boomers, not sure I am having the BBQ’s with many?

I certainly couldn't eat a whole one....

There is less substance to them than you think, a lot of fat and filler...

But no avo on toast of course

That would back up the point of the article though, wouldn't it?

Much easier to leverage existing equity than start from scratch.

And if there were no FHBs present for 'NZs most desirable city' - then where are they?

I'd stab a guess at on a plane, and what you're seeing is Aucklanders cashing up and moving out, which has been happening for the almost 20 years of Auckland's property bubble.

I'd stab a guess at on a plane, and what you're seeing is Aucklanders cashing up and moving out, which has been happening for the almost 20 years of Auckland's property bubble.

Does it really make much sense for younger demogs to load up on more debt than any other time in history when it's becoming more obvious that we're at a quasi-Fourth Turning point in time? Not a question I can really answer, except for caveat emptor,

The world is about to change drastically from the relative peaceful last 80 years or so. With a new world order, increased liklihood of military wars, trade wars, economic shifts, climate change, career shifts, pandemics, AI/tech acceleration devwlopmental acceleration and social instability. If it sounds dgm ish.. it's not.. it's just the next part of the cycle and darwins rule will apply.

The scenarios that led to stable/growing land and house prices during the last period may well shift.. in fact are likely to do so as we see how the world changes and adapts.

Not a time for excess debt or putting all of one's mo ey in one basket (a house)... and likely a time to want to be able to move cites/countries etc rapidly. Prepare for accelerates change and new opportunity.

Australia housing in the cities is far more expensive than NZ, but if they want to go and check that out, then good on them.

Good to experience other places when young.

Do FHBs have a sign or something to say that's what they are, how do you know who is and isn't a FHB?

They know it’s still overpriced. The racket is over. Doesn’t matter how much competition shows up to Turners; people don’t pay $80k for the Toyota Corolla.

They do in Singapore.

Most FHB will be drawing down their Kiwisaver as part of their deposit, and if they do that they can't buy at auction under the normal auction rules (deposit payable that day). Its not just a problem with doing due diligence.

Yeah.

Scraping that deposit together ..

when you are competing for a basic right ...

against already well-healed 'investors' ...

thanks to b.s. tax policy for 30+ years ...

that the government most people voted for ...

that they voted for to enabled them to beat you ...

EVERY TIME ...

due to our obscenely corrupt and inequitable tax system ...

It's hard, right?

Don't bother. Other countries - with better tax system favor neither the rich, nor favor the old. But NZ does.

Leave. Make money. Come back and help fix it.

Please ...

From the regulatory impact statement on restoring interest deductions - Page 13

"Restoring interest deductions for residential rental property is likely to put some upward pressure on property prices, making buying a first home somewhat less affordable"

https://www.treasury.govt.nz/sites/default/files/2024-07/ris-ird-ridrip…

its not a basic right to own a home, its a basic right to have a place to live, which basically anyone who wants can get it.

by RookieInvestor | 21st Nov 24, 4:48pm

its not a basic right to own a home, its a basic right to have a place to live, which basically anyone who wants can get it.

Rooked that's not a society either Labour or National are selling.... wake up

you selling rentier future not Labour or National policy here?

The current government's objective of increasing rental supply by allowing non owner occupier owners to compete and outbid owner occupier buyers in the existing residential dwelling market, may have an unintended consequence of a rentier future.

The regulatory impact statement of the re-introduction of interest deductibility explicit states:

"Restoring interest deductions for residential rental property is likely to put some upward pressure on property prices, making buying a first home somewhat less affordable"

Until recently, many investors steered away from existing properties after the previous Labour Government lifted the Brightline test to 10 years and stopped them from claiming tax deductibility on their mortgage repayments when offset against rental income.

New housing was left under the old rules making it more attractive to investors for rentals. A slew of new units, flats and terraced housing was built by developers, much of it now hitting the market and proving difficult to sell, just as interest rates are dropping, the Brightline test has been brought back to two years and tax deductibility will be fully reinstated in the next tax year.

As a result, existing housing has come back into investors’ favour.

New Zealand Mortgages managing director and head of lending Nathan Miglani says his business has seen a big uptick in the number of investors. “The number of property investor loans we have done over the past two months is the same as we did for the whole of last year.”

The majority are looking at existing properties now the Brightline test has been brought back to two years, he says. “Buying an existing house with land with the potential to renovate or subdivide in the future is looking extremely attractive to investors.”

He says first home buyers will be back to competing full on with investors next year.

https://www.landlords.co.nz/article/976523746/competition-between-inves…

FHB can buy those brand new townhouses, which are being discounted by developers now that they are piling up, so prices are falling not going up. Nobody else wants them so FHB have the market all to themselves.

"FHB can buy those brand new townhouses, which are being discounted by developers now that they are piling up, so prices are falling not going up. Nobody else wants them so FHB have the market all to themselves"

In some areas of New Zealand, those housing products are massively overpriced.

First Home Buyers: CAVEAT EMPTOR

It's always been a rentier system. It's standard capitalism. Economic and monetary theory has simply encouraged it further the last 40 years.

Labour have tried to lessen it, even though they were responsible for introducing it, and unintentionally fuelled it in the early 2000's. It's standard National policy though.

The rentier future will simply be a question of who the owners are.

I thought that now the house prices are 20% off the 2021's peak, everyone will be able to buy 2 houses, not 1, but it seems that this is not the case though. For house in North Shore you need 200K deposit, that's a lot of money and I expect the house prices 10-15% up by the end of 2025.

Don't enter a logic test.

can I buy an 1/8?

Ladies and gentlemen take your seats, www3 is about to start. Storm shadow missiles being fired deep into Russia as we speak. If you are in London, leave NOW, come to NZ and buy a house. :)

You'd think prices, that are still several multiples away from affordable, might still be a barrier?

It is not that difficult for first home buyers to get that deposit!

You only need to ask your parents to provide it out of their equity in their own home.

It is amazing just how financially illiterate so many adults actually are!

very easy to do and no cost.

It is amazing just how financially illiterate so many adults actually are!

...

no cost

Oh yup...

No cost to the FHB up front depending on the agreement with the parents (always set up a formal contract), but sooner or later there'll be a reckoning. Are the parents gifting the money to the FHB or expecting them to pay it back later? Or even pay it alongside their mortgage they can barely afford? Can the parents even cover an equity loan themselves?

It is amazing just how financially illiterate so many adults actually are!

So in your world, grown adults asking/relying on financial support from their parents in an entitlement? What a mentality...

Where did I suggest it was an entitlement?

There are so many patents that aren't investors that have equity in their own homes that could assist their children into their own home.

If they didnt want to assist their kids then that is on them.

You only need to ask your parents to provide it out of their equity in their own home..

So the rich get richer? And higher wealth disparity in society? There have been several who started with the bank of mum and dad and now own multiple investment properties who have outbid owner occupier buyers many times. A few have become full time peoperty investors.

There is a huge portion of the population that have no bank of mum and dad or no access to the bank of mum and dad.

Should upward social mobility be dependent upon winning the ovarian lottery?

CN, life is to be lived and do the best you can with it!

Everyone has opportunity snd you are correct not everyone has parents that own or assist with a deposit!

The thing is that even if you havent, there are many ways of owning property but if you have the wrong mindset or not be prepared to work then yes you will not

I believe that the Auckland market is going to be very flat for awhile due to the first home buyers servicing ability, whereas ChCh is where the money is to be made and has been for quite awhile.

That life CN, just imagine being born in Gaza right now, yep over 12 months into the conflict and people are stupid enough to still be having kids.

2 people paying into Kiwisaver for 10 years would get close wouldn't they?

They are paying into kiwisaver to fund their retirement, Kiwisaver is not a saving fund for your property deposit. FFS.

What makes you think an investment in managed funds is better than an investment in a house? Both are good to have in retirement.

1 person in kiwisaver at 10% for 10 years should be the majority on a deposit.

The main obstacle is price, caused by the lack of supply of housing, caused by land use restrictions. The main obstacle is zoning. Abolish zoning.

Nice National party talking point. The main obstacle is a taxation system that benefits speculators and screws owner occupiers.

It's a valid talking point. Not only do we not free up enough land, but there isn't enough infrastructure support relative to the population growth foisted upon us and borne unequally across the region that the land we do have available to be used can't because the utilities providers can't keep up.

No tax system on earth will fix the price issue if you keep adding unchecked demand to it and pretending it doesn't matter.

I don’t really care whose talking point it is, whether it’s Chris Bishop or Phil Twyford. It’s a simple problem, and there’s enough evidence that this is the root cause.

There are secondary issues that inflame the situation, such as taxation. But for the most part, those advocating for those are just using housing as a vehicle for some other ideological goal. That, or they’re NIMBYs weaponising useful idiots.

The issues are supply (where the only real fix is zoning or government building) and demand (where the only real fix is reduction in immigration).

Interest rates massively affect the asking price, but not affordability.

The other things like taxation, DTIs, etc won't change anything. Taxation would make the tax system fairer however.

Taxation causes more problems.

rental problems and increased house prices you only need to look at Oz

I agree that taxation will cause problems if it’s used as some kind of impossible fix - basically the government deciding who should buy instead of price. But making the tax system fair shouldn’t break anything.

Keen to hear how spruiker's can continue to claim house prices in New Zealand will continue to rise in the context of these two recent articles. Wondering if they see a pattern emerging ...

https://www.interest.co.nz/insurance/130886/falling-house-prices-will-b…

https://www.stuff.co.nz/nz-news/360492874/flood-risk-areas-napier-have-…

I do find it funny that people say these prices are unaffordable, but the mortgage is pretty much the same as you would pay in rent. Once the OCR comes down a bit more it will cheaper to buy than rent. This is assuming you can save the deposit that is.

Of course it would be great if houses were cheaper. But I am actually not sure how this can be achieved when we can't build them for less than current prices.

Is the mortgage the same as what you pay in rent though? Sorry I haven't done the maths on averages, but for ourselves on our last rental before we left, our rent was 40% of what the mortgage repayments would have been.

Even now, with a 20% deposit and a 5.69% interest rate, the mortgage would be 50% higher than our rent.

And that excludes additional costs we'd have to pay as home owners - insurances, rates, maintenance (not that our landlord[s] paid for that either...).

Expenses depend on how much work you are prepared to do yourself.

According to the chart above, it’s $651 a week with a 20% deposit (all NZ). That seems about the same as you would pay in rent, give or take.

EDIT: Just looked, median rent in NZ is $600. So it is a bit more expensive to buy at the moment (until interest rates are a bit lower).

For $650 you can rent a $1.6M property in Devonport.

Not sure where you are getting these figures from.

The data seems quite varied depending where you look. According to trademe: As of August 2024, New Zealand’s median weekly rent sits at $640 — 3.2% higher than last year.

https://www.trademe.co.nz/c/property/article/how-much-is-rent-in-nz?srs…

But you're comparing median rents with lower quartile property's mortgage costs. If you were renting an average house you'd be exchanging it for a significantly below average house.

Rental properties are predominantly in the bottom (cheaper) half of all properties, so median rent would still probably only get you a lower quartile property. There are not as many high quartile rental properties. The rental market is not the same distribution as the total or for sale market.

Exactly. I’d say the median rental is probably equivalent to the lower quartile house.

Either way, owning is currently in the ball park and will be even closer in just a few months time assuming interest rates decrease.

I've just given you the example of a $1.6M property in Devonport renting for $650. Your assumptions are wrong.

Keep on dreaming you mean a $1.6M property that really needs to be demolished ? It costs $750 plus down here in Tauranga now for a decent modern home less than 10 years old. You wouldn't let your dog live in some of those Devonport places.

Is the mortgage the same as what you pay in rent though? Sorry I haven't done the maths on averages, but for ourselves on our last rental before we left, our rent was 40% of what the mortgage repayments would have been.

Even now, with a 20% deposit and a 5.69% interest rate, the mortgage would be 50% higher than our rent.

Do you live and rent in a property with a low gross rental yield?

In Auckland that might be inner city suburbs (such as Epsom, Remuera, Parnell, Orakei, Kohimarama, round the bays, Ponsonby), East Auckland, or North Shore such as Devonport, Takapuna.

This is what Jimbo is missing with his calculations. You can rent a much better house in a much better location with no ownership expenses for the same price as buying a shitty house out in the wop wops and you then you have to pay all the additional ownership expenses and additional travel costs.

"You can rent a much better house in a much better location with no ownership expenses for the same price as buying a shitty house out in the wop wops and you then you have to pay all the additional ownership expenses and additional travel costs. "

Exactly. And the money that would be used as a 20% deposit for buying can be invested in a higher returning asset.

Tony Alexander bringing the DGM. But don't worry, despite this good analysis he still ends with FOMO message and 'price rises beckon'.

The man is shameless.

[NZ businesses] Their confidence about the economy has soared along with hiring and more recently investment plans. But cash flows are very tight, margins are squeezed to a greater degree than any time since 1976 according to one measure I track, and some sectors like residential construction look set to continue shrinking through all of 2025.

Prospects for our biggest export destination of China look poor and have just got worse with the outcome of the US Presidential election and potential for 60% tariffs on Chinese goods. Extra cutbacks in government spending here look likely as the fiscal balance continues to surprise on the bad side, net migration flows have fallen away, and the negative economic effects of climate change can only grow from here.

https://www.oneroof.co.nz/news/tony-alexander-three-months-of-rising-ho…

His business sells subscriptions, advertising and charges a fee for his speaking at events.

Shameless or correct? I guess time will tell.

I think it’s hard to deny that house prices have a very good correlation with interest rates.

Nats = Economic Mismanagement under their tenure

Unemployment Up

Social Unrest Up

Growth Down

Infrastructure Lacking

Health Services Down

NZD down

Back on track.

Interestingly, even in relatively risk free housing markets like Texas, 20% in the norm.

But then of course their housing is 1/2 the cost, so is our 10% (or less) equivalent.

What this means for our banks is they are also factoring in a risk premium if they accept anything less than 20%, which homeowners also pay for ON TOP OF PAYING TWICE AS MUCH FOR HOUSING AS THEY SHOULD.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.