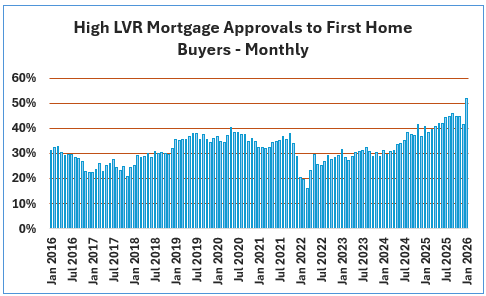

More than half the mortgages approved to first home buyers in January were low equity loans, setting a new record for that type of higher risk lending.

The latest figures from the Reserve Bank show 51.8% of the mortgages approved for first home buyers in January were low equity loans, where the borrower has less than a 20% deposit.

That was the first time low equity lending to first home buyers has passed the 50% mark in the Reserve Bank's data series which dates back to 2014, meaning it's likely an all time high.

This type of higher risk lending to first home buyers has increased rapidly over the last two years, with low equity loans making up just 40.9% of approvals to first home buyers in January last year and 31.3% in January 2024. See the graph below for the trend over the last 10 years.

Low equity loans carry higher risks for both borrowers and lenders, giving them less room to restructure the loan if the borrower suffers a financial setback such as a loss of income.

Size of loans up too

The higher level of low equity lending was not the only record set by first home buyers in January.

The average size of the mortgages approved to first home buyers hit a record high of $599,437 in January, pushed up by the volume and value of low equity loans.

The average size of low equity loans approved to first home buyers in January was $656,148, compared to an average loan size of $539,720 for first home buyers with at least a 20% deposit.

Ironically, the increase in higher risk lending does not appear to have led to a increase in the total number of aspiring first home buyers getting into a home of their own.

The total number of mortgages approved to first home buyers in January this year was 1775, down slightly (-2.3%) from 1817 in January last year.

However, while fewer loans were approved, the total value of loans approved to first home buyers increased slightly, to $1.064b in January 2026 from $1.036 billion in January 2025, up 2.7%.

So it appears that while fewer mortgages were approved to first home buyers in January compared to a year earlier, banks were able to increase the total amount of their lending inro the first home buyer market by increasing the amount of higher risk lending.

The comment stream on this article is now closed.

23 Comments

Owner occupiers and investors are taking a larger slice of the cake

🍰🥂

That doesn't appear to be the case Cote. FHB's accounted for 35.2% of all the mortgages approved for the purpose of purchasing a property in January this year, up from 32.7% in January last year. It was a slow but steady increase over that 12 month period. So if owner-occupiers and investors are taking a bigger share of the mortgage pie, it's probably because they are taking on more debt rather than buying more properties.

Is this correct as per yesterday's rbnz borrower type data split?

Makes sense i suppose, owner occupiers buying in a higher price bracket so more borrowing but not necessarily more houses bought. Investor borrowing also jumped tho.

Time for a 🥂

Banks getting desperate?

They're trying anything and everything to lever up the masses. Shareholders want their payday, didn't you know.

Shareholders are used to justify it, but really the priority is executive bonuses.

Doesn't it show it's getting more and more difficult for first home buyers to afford the entry ticket?

My first home loan was $340k 20 years ago. That’s $564k in today’s money according to RBNZ inflation calculator. So it’s pretty much the same now - except interest rates back then were 7.5%!

And wages have gone up accordingly. Which may be fine until you factor in the jump in marginal tax due to bracket creep, the government may be claiming 50-60-70% of that increase.

Yes and you then had 15+ years of falling interest rates making payments easier, while the CV probably tripled in the same period of time meaning you also gained a great deal of equity.

Todays buyers may have years or decades of flat/rising interest rates on the same size mortgage (in inflation adjusted terms) making paying down the debt challenging, and receive very little capital appreciation/equity gained (potentially less than general inflation meaning the asset is constantly worth less than at the time your purchased it).

So yeah its probably not 'pretty much the same now' as it was for you then. Great investment for you at that time, could now be the opposite for those who have just purchased.

Oh really? Is he sounding too positive for you?

How would you like me to reply to these questions? Not sure if he’s sounding positive or negative 🥱🥱🥱

Agree, but I didn’t know that at the time. And who knows, someone buying now may get the same outcome.

All I’m saying is that when I bought it was probably about as difficult as today, give or take a bit either way.

I'm guessing that was a somewhat above average house, or in an above average area? My first home loan in New Zealand was about the same, buying a nice place in Christchurch 8 years ago with a 30% deposit.

Neither of those, but it was Auckland to be fair, so yeah above the national average. Still I reckon the repayments of an average NZ house would have been more back then at 7.5%. And we didn’t have our employers helping with our deposit via KiwiSaver.

If it is harder now, I don’t think there’s much in it.

If inflation does go up again (the way some banks seem to be betting) and the RBNZ puts up its rate, the low equity loan people are really going to suffer, considering the house market seems static at best.

Yes exactly as ITG says.......

Our short term, ARM mortgage market here, is the riskiest in the world.

It was just a small ARM portion, in the USA that defaulted, helping trigger bank defaults, then the GFC, then mass Govt bailouts......

I'm definitely surprised they are doing this especially when they believe inflation and higher rates are more likely than not. They must know there is a reasonable chance these low equity owners may find themselves in a negative equity position in 1-3 years time if their inflation and interest rate projections are correct.

Its just like a few of us saying here back in 2021-2022 that there is a pretty good chance that low equity owners back then would find themselves in negative equity a few years later - to which we were laughed at and called 'doom gloom merchants'. But then it happened so not sure why people were laughing about this outcome at the time - its not good.

My personal opinion is that all FHBs under a certain equity should be required to go long, 3 years plus.

Similar story in Oz

Thousands break into property market with 5% Deposit Scheme for first home buyers

https://www.abc.net.au/news/2026-02-27/five-pc-home-deposit-scheme-infl…

How Australia's lax property tax has created a class system (note the generational graph)

https://www.abc.net.au//2026-02-27/australias-lax-property-tax-has-crea…

Read: Unaffordable

"Low equity lending to first home buyers surged in Jaunary"

January to January "The total number of loans to first home buyers was down 2.3%"

??

That's some interesting and frankly scary figures.

Summary. More money borrowed at higher risk.

Surely that's to be expected in a rising market.

Banks desperate to keep things going.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.