The housing market is having a buyer's summer with new listings and total stock for sale both at their highest levels for the time of year in more than a decade.

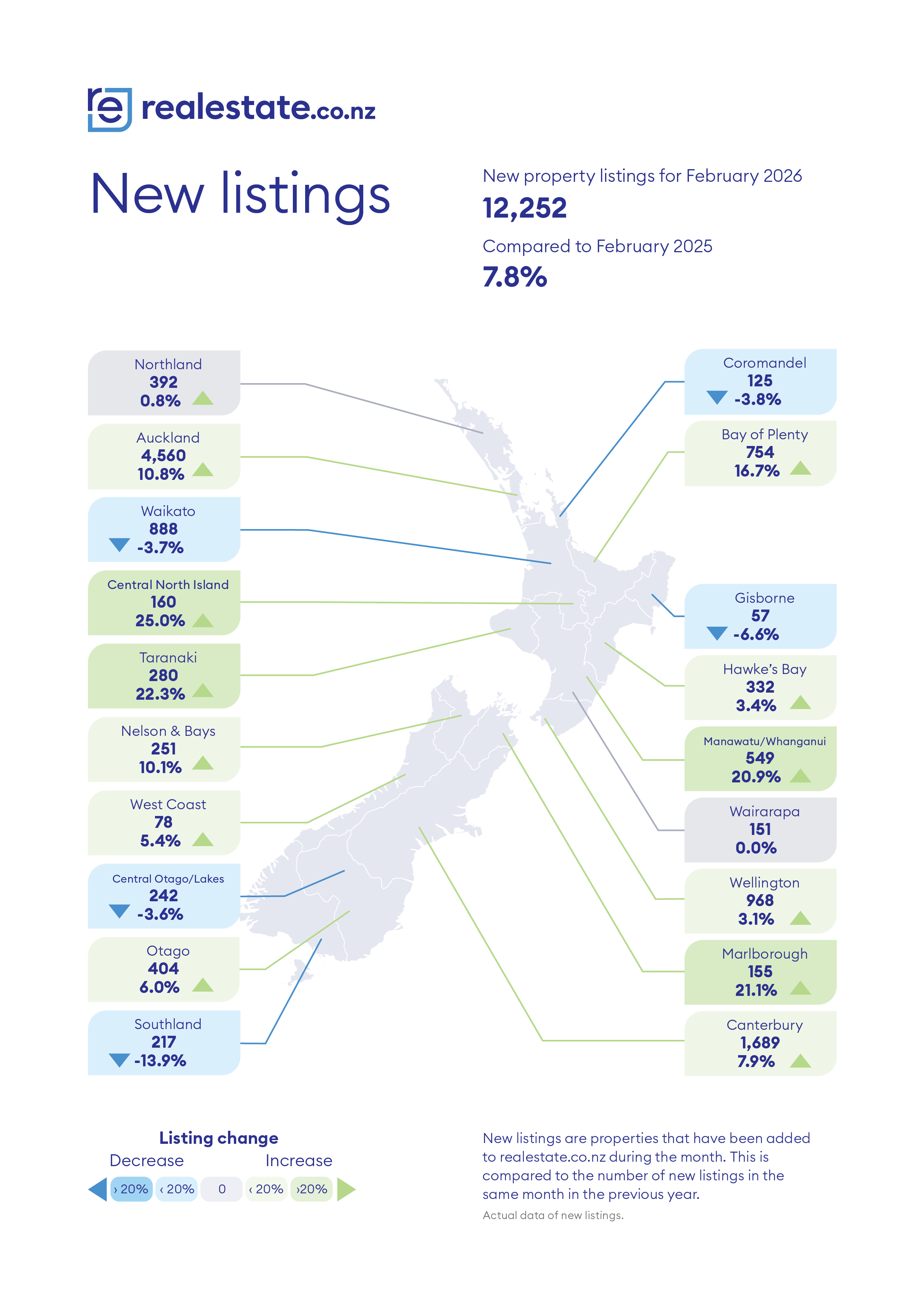

Property website Realestate.co.nz received 12,252 new listings in February, up 7.8% from February last year, making it the most new listings the website has received in February since 2013.

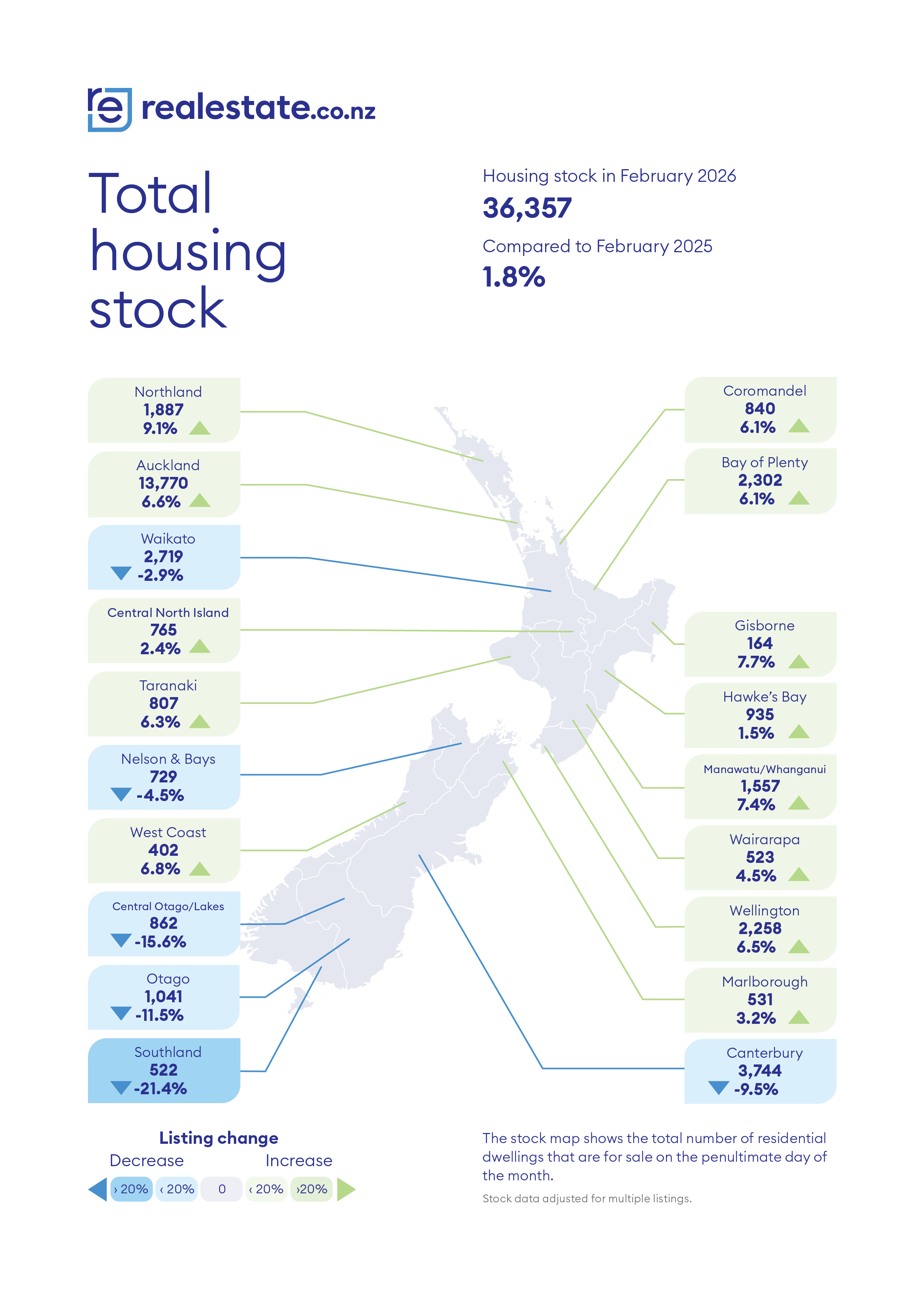

That pushed already high total stock levels up to an 11-year high, with the website having a total of 36,357 homes available for sale at the end of February.

The biggest increases in new listings last month tended to be in the smaller provincial centres, with new listings in the Central North Island (which includes Taupo) up 25.0% year-on-year, followed by Taranaki 22.3%, Marlborough 21.1% and Manawatu/Whanganui 20.9%.

However, buyers in most main centres will also have plenty of choice, with new listings in the Bay of Plenty up 16.7% compared to February last year, followed by Auckland 10.8%, Canterbury 7.9% and Otago 6.0%. See the table below for the full regional figures.

Asking prices were basically flat, with the national average asking price of properties available for sale on Realestate.co.nz moving up just 0.1% in February to $849,061.

The comment stream on this article is now closed.

37 Comments

From the report:

"When new listings rise faster than total stock, it tells us homes are being sold through rather than sitting on the market."

Asking prices are neither here nor there however they're up YOY and MOM.

Momentum and confidence building.

🥂

When new listings rise faster than total stock, it tells us homes are being sold through rather than sitting on the market

That's moot if they don't specify the number of listings withdrawn from the market without being sold

I'm glad Greg didn't parrot their talking points, which are just spin without substance when using incomplete data

Yes however the clear tendency here is to spin numbers and news to the downside. Balance is beneficial 👏🥂

Our most complete report on the housing Market is the Housing Market Activity Report which comes out in the second half of each month. It is based on data from both Realestate.co.nz and the REINZ and includes trends in properties withdrawn from sale and the monthly overhang of properties for sale. Here's a link to the January report: https://www.interest.co.nz/property/137239/housing-sales-dropouts-and-m…

The clear tendency here is to spin numbers and news to the downside

No the tendency here is not to spin anything... maybe that's the bit you do not understand.

Spin by omission for example.

There's always a bias, conscious or not.

👏🥂

Maybe there's a tendency to the downside because the endless upside rhetoric we've been subjected to over the last couple of years hasn't materialized.

Let's not forget the developers who list only 1 or 2 of 8 for sale.

"total stock for sale both at their highest levels for the time of year in more than a decade." - that isn't that bad is it? I don't remember people thinking there was too much stock a decade ago.

Be Quick....

Hey I'm not saying house prices are going to take off again. But it doesn't seem like the house price apocalypse either.

WGTN is down 39%

AKL is down 33%

in real terms, that's almost a zombie apocalypse, numbers according to NZ Herald Liam Dunn

Its not flash considering houses are a leveraged buy in most cases.

That is old news, and they pretty much went down by the same stupid amount they went up after Covid. They have been flat for a while now.

Sure it doesn’t look terrible… if we just completely ignore the broader context

Like interest rates decreasing, economy improving?

Not sure what your lookng at. Inflation is not conquered and rates forcast to rise. More stock arriving, more stock unsold. A few overseas private finance guys being found to be smoke and mirrors with big losses which is how GF started.

Hope the economy has turned the corner but will believe that when I actually see it.

Popcorn.

There are definitely potential negatives out there, but also potential positives. I feel like the most likely outcome still is fairly static house prices.

So you're predicting flat nominal prices this year, while the real value continues to decline?

I wouldn't say its a prediction, I would say that's the most likely outcome. Fairly flat, probably below CPI.

And that's also the best outcome.

The other possibilities of house prices dropping or even rising are also on the table, and given the history of the housing market (and many completely wrong predictions I have seen from comments on this site), anything is possible, hence it not being a prediction.

Agreed - below CPI. Throw a little risk thats simmering into one's assessment and it's less return than cash in the banks.

You always get below CPI from the bank (after tax). With houses you also get rent and no tax on the capital gain.

But I agree, I wouldn't own an investment house right now. I contemplated it when the neighbours came up for sale so we could control the tenants, but couldn't make the numbers even remotely work.

Agreed, the numbers don’t work at current prices. And in a supply heavy market the buyer is in control, this is part of that broader context.

So prices either fall further, or stay flat until the numbers eventually work. A reversion to the mean.

Opportunity cost needs to be factored in. Five flat years is a significant financial leak to your portfolio

rents have to rise a lot to make numbers work, that impacts inflation ocr goes up thus prices fall

hint - only prices falling can fix the numbers

Option A

Lock it in Eddie

Oil price increases --> Inflation increases --> prices increase --> disposable income drops further --> ability to pay drops --> higher mobility of tenants coupled with larger rental options ---> lower rents --> more investors exiting the market due to the numbers not stacking up --> increasing supply of housing --> lowering house prices until an inflection point where numbers again stack up for investing.

The point that numbers work is circa 2015 prices thereabouts. So wages double, in an AI landscape yeah right, or price retreats another 30-40%. Otherwise it's ongoing stalemate with the better quality future renters and buyers continuing to evacuate to Straya.

Banks will have to start driving mortgagee sales otherwise it's just a drawnout stalemate.

oh dear

I personally think this is a trend that is likely to continue the next decade or two (high listings/weak demand). Remember approx 50% of the boomer generation are going to be dead in the next 10 years and they are the largest property owning demographic. Each day more die, are diagnosed with cancer or other significant health issues, they are downsizing their properties as the 3-4 bedroom family home is not longer suitable for their needs.

Doing a quick google, there are approx 1,000,000 boomers in NZ and half of that will be dead in the next 10 years or so. Think about the significant implications of this at the macro level of our demographics/economy. We've lived in a boomer fixated/centered/influenced environment for decades now and this is coming to a very quick end (ie policies that were mostly beneficial for that generation because they were the largest voting demographic). What is the future going to look like as a result?

If my rough calculations are correct, there could be around 500,000 boomer deaths in the next 10 years (average age of death 80+ e.g. born 1950 so 80+ average age of death is coming around very soon, especially for men, perhaps not so much women who are project to live a bit longer...) so around 50,000 a year (on average). (Happy to be corrected if these figures are materially incorrect/inaccurate).

Are we going to have net immigration high enough to offset these deaths? If not, what fundamental changes are we going to see in our economy (and housing market)?

Seems to me like the elephant in the room that everyone is quietly ignoring - and yet it is going to be one of (if not) the biggest influences on our economy - starting now and last the next 2 decades - a lot of people are going to die here relative to our overall population. Ie boomers currently 20% of the population and they are nearing their expiry date.

ps. last year it appears we have approx 58,000 births so perhaps we will be okay if external immigration remains low?

I know a downsizer who listed rural LSB at 2.8mil eventually sold for 1.85 mil.

I think i'm turning Japanese, I really think so.........

And often the kids want mum/dads old place sold as they need the money to reduce their own debt.

Same for the shares that many of these boomers have as well!

There is a belief that credit availability will fall (or interest rates rise) on the back of this, many of the boomers were forced to invest for retirement, thus this credit will be missing over the next few decades.

https://www.zerohedge.com/geopolitical/85-babies-2026-will-be-born-asia…

85% of babies will be born in Asia / Africa <1% in NZ or Aussie.

I'm a widowed boomer with no dependents who recently bought a large family home, triple garage etc on a large section - to share with family, to keep costs down & support each other as we age..

Yip one way of doing it but has the same result - if you have multiple generations living in one house then there is less demand on existing housing than there would be if multiple generations were competing for individual ownership of that same home.

The only downfall of this strategy is a reduction in super (I believe) - if that is an issue, which it may not be if you are flush for cash or kids chip in for expenses.

Don't get me wrong - I have no issue with this idea. It is how 'things' used to be.

Seems the sensible option given the cost of a rest home, provided there is adequate space for multiple generations to feel separate when they want to. Preserves the family wealth also and grants time with family before their time is up.

Lots of yachts for sale on Trade Me. Many have been getting relisted for well over a year now. Not sure who's going to buy these either.

Looks like the speculators (debt unsupported by income) are beginning the rush to the exit. The big question is who is left in NZ to buy?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.