The housing market is looking particularly soft, with sales numbers and prices both falling as it heads into winter.

According to the Real Estate Institute of NZ, 6262 residential properties were sold throughout the country in April, -21.2% compared to March and -7.9% compared to April last year.

The drop in sales was particularly significant in Auckland, where April's sales were -29.5% compared to March and -14.8% compared to April last year.

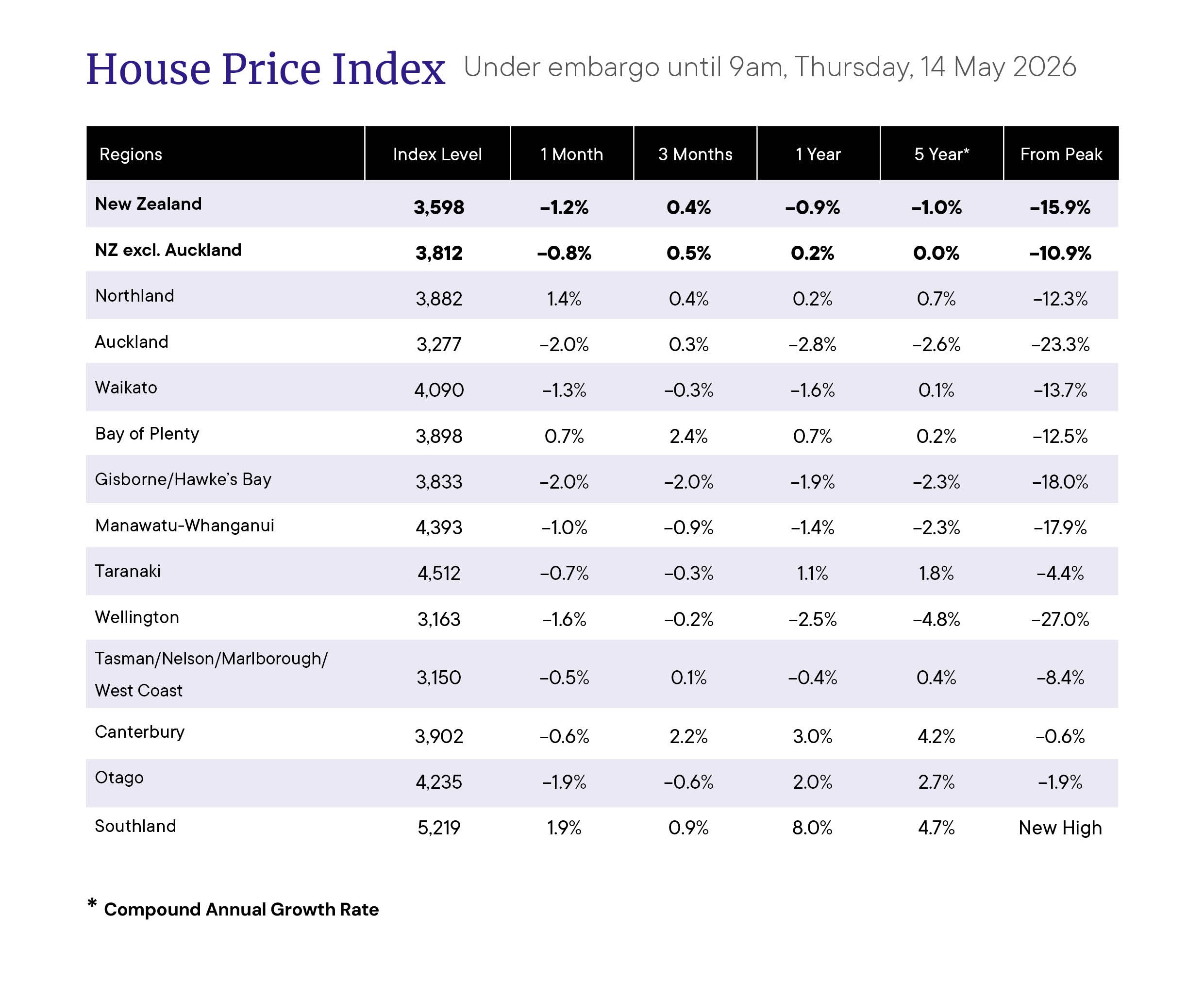

The REINZ House Price Index (HPI), considered the most reliable indicator of price movements, declined by -1.2% in April compared to March, and was down by -0.9% compared to April last year.

The biggest monthly declines in the HPI were in Auckland and Gisborne, both -2.0%, Otago -1.9% and Wellington -1.6%.

Only three regions posted gains in the HPI in April - Northland +1.4%, Bay of Plenty +0.7% and Southland +1.9%.

See the table below for the full regional HPI movements.

The national median selling price was $775,000 in April, -1.9% compared to March and -0.6% compared to April last year.

The REINZ said buyers remained active in the market but were responding to cost pressures.

"April lands the housing market in a testing mid-cycle position," the REINZ's April report said.

"[It's] past the initial shock of the overseas conflict, into its cost of living pass through and now facing a potential OCR hike environment through winter.

"Fuel costs are amplifying regional differences, particularly in vehicle dependent areas, against a broader backdrop of rising living costs, including food, insurance and rates," it said.

However the report also noted that the main challenge facing the market over winter could be rising mortgage interest rates.

"This shift, from a [rate] cutting environment to an imminent hike environment , removes the tailwind of falling rate expectations that underpinned 2025's recovery, and begins to introduce the prospect of new serviceability pressure, a meaningful change from April's starting position," the report said.

"The key question for May and June is whether listings continue to build faster than sales can absorb them as we move into winter," it said.

The comment stream on this article is now closed.

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

25 Comments

Auckland sales count MoM - 14% YoY -29%

Listings up

Probably Nothing

And prices down 2% YoY too (5% with inflation).

It is great that the NZs long addiction to a housing ponzi, is broken and now in the process of being buried deep.

For every NZer to be a total zombielike, addicted gambler on housing, in the period upto 2021/2022, was a sure fire massive bubble.

-Worse than the leadup to the 1987 share market boom/crash. Property just resets over years/decades, not hours/days.

HPI set to drop, well into the 2030's

"well into the 2030's" - seems unlikely to me. Even if prices were flat into the 2030s, inflation alone would make house prices reasonable again.

Once it gets back to being the same price to own as to rent, that will probably be the floor IMO. I guess it also depends on interest rates (and rents), but that should be before 2030.

What about supply? If it continues like this and the cost of compliance stays the way it is we won’t be building much.

Reducing compliance costs/land costs in this market would create fluidity and minimise the fall in house prices. Increase economic activity and employ lots of the young people currently exiting NZ job market, thus creating more new demand for housing and cause house prices to stop falling. It would have absolutely no downside.

However, Auckland Council exists. Wayne Brown declares the future will be expensive to build high density, in expensive locations, around expensive transportation infrastructure, with expensive to operate services.

Lots of council fees and workers and consultants that absolutely dont want fees and complexity to drop. Vested interest in the gravy train.

Compliance isn’t just councils though

Jimbo - you are out of touch with your rent assumption

1. Updated assumptions

- House price: $750,000

- Loan (80%): $600,000

- Interest rate: 6%

💸 2. Annual ownership cost (recalculated)

Mortgage interest

6% × $600,000 = $36,000

Other costs (same as before)

- Rates: $4,000

- Insurance: $2,500

- Maintenance: $7,500

✅ Total cost of owning:

$36,000 (interest) + $4,000 (rates) + $2,500 (insurance) + $7,500 (maintenance) = ~$50,000/year

🏢 3. Rent (unchanged)

- ~$700/week → $36,400/year

⚖️ 4. New comparison

OwnRent

Annual cost~$50,000~$36,400

👉 Owning now costs:

$50,000 – $36,400 ≈ $13,600 more per year

📉 5. Required price drop at 6%

We need to eliminate:

$13,600/year

Convert to loan reduction

At 6%:

Loan reduction = $13,600 / 0.06 ≈ $226,700

Convert to house price:

Price drop = $226,700 / 0.8 ≈ $283,000

✅ 🎯 Final result

👉 At 6% interest rates, NZ house prices would need to fall roughly 25%–35% for buying to clearly beat renting (all else equal).

You missed out that the guy who bought also has $150k tied up earning nothing, so there's an additional opportunity cost of at least a few grand.

Long term the balance depends hugely on your assumptions about house prices - if they can match or beat inflation then things get more even. Some people would give some value to the freedom and stability that comes from owning your own home too (and others would call that inflexibility and burden a cost)

Where did 6% come from? At 4.5% the interest goes down to $27,000.

Also I'm not convinced the average landlord spends $7,500 a year on maintenance, so not sure why a homeowner would. Most landlords almost had a heart attack when they had to install a one off heatpump for $2k

$27,000 (interest) + $4,000 (rates) + $2,500 (insurance) + $2,500 (maintenance) = ~$36,000/year, $400 less than rent.

It all depends on what happens to interest rates more than anything else.

Its all to do with the 2nd law of thermodynamics, asl PDK

AI built the model, its not as biased as many

I doubt I'd have to ask, he'll be along shortly to fill me in again.

I hope you mentioned EROI to AI so it could adjust the model.

it did not include principal repayments in the cost, so the model does not really include cashflow (is it feasibility for buyer) , it assumes this turns into equity for the renter/owner, this assumes prices do not fall.....

Speculative overshoot coming home to roost. Is a tax free capital loss upside...?

according to pooperty apprentice, people losing money just do not know what they are doing.... I wonder how many are apprentices in the poo from peak advice?

We sort of have the opposite of "Clearance" happening

The opposite of clearance includes the following antonyms:

-

Blockage: Refers to a physical barrier that prevents something from moving or flowing.

-

Obstruction: A general term for anything that hinders progress.

- Denial: Implies a refusal to grant or allow something.

Funny Denial is mentioned

Plenty of denial still with Auckland sellers. Worth highlighting they were handed their 2024 CVs in mid 25 and a majority did not believe the new reality shift. Instead, in 2025 most of them chased offers over those 2024 CVs.

Now it's 2026 with economic growth derailed, rates rising and all this overhang. The market floor has shifted further below those 2024 CVs and the momentum isn't slowing. Buyers are very aware.

YOY -29% sales for April Auckland, buyers be 100% aware

Indeed. We all know what happens on the housing bubble curve after denial...fear, capitulation, and despair. Anyone buying a house at the greed driven bubble price should only do so if they "really really need to" (school zone, divorce etc). Every one else sit on your hands...

Due to no one normally going to rainy muddy open hones in winter,

its possible that fear starts to build this winter, as a small number of houses,

start to sell at quite large discounts to current pricing views.

Then the new, NZ housing market crash downleg shows itself, like a drunkard taking the builtup and overdue, building upto the gills, past the eyeballs, leak in the alleyway......

A few leaks in the ole alleyway and the wet and wetter downleg, shows itself........

Listings up + sales down + interest rates up + cost of living up + election year...... must equal = house prices down

why did prices fall ---- more sellers then buyers

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.