Getting into a home of their own became slightly easier for first home buyers in April, as falling house prices outpaced increases in mortgage interest rates.

Mortgage rates continued to increase in April, with the average of the two-year fixed rates offered by the major banks rising to 5.18% in April from 5.05% in March.

However, the effect of that on mortgage payments was more than negated by a drop in house prices.

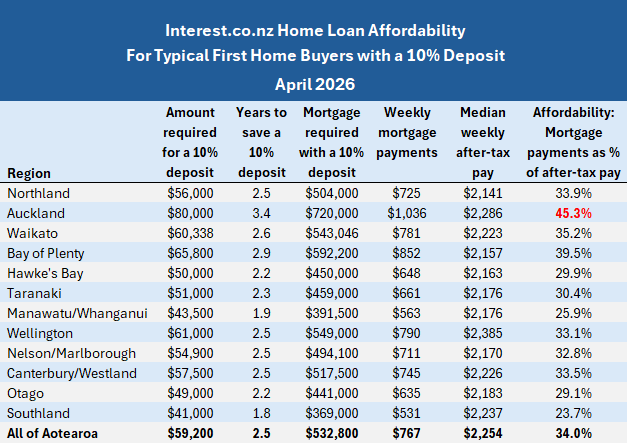

According to the Real Estate Institute of New Zealand (REINZ), the national lower quartile selling price dropped to $592,000 in April from $610,000 in March.

The combined effect of those two movements meant the mortgage payments on a home purchased at the national lower quartile price with a 10% deposit declined to $767 per week in April from $779 a week in March. That's a saving of $12 a week.

Although the difference is small, it is at least heading in the right direction. But perhaps more importantly, it marks a reversal of the trend over the first three months of this year.

Between January and March, the REINZ's lower quartile price increased to $610,000 from $583,000, while the average two year fixed rate increased to 5.05% from 4.74%.

Those two factors pushed up the mortgage payments on a lower quartile-priced home to $779 a week in March from $720 a week in January. That's an increase of $59 a week in the first quarter of the year.

So the $12 a week decrease in April would have been a small but welcome relief.

Unfortunately, one month's figures do not make a trend.

Most economic forecasters are expecting interest rates to keep rising this year. So for affordability levels to improve for first home buyers there would need to be a significant decline in prices at the bottom end of the market.

While the housing market is decidedly soft heading into winter, significant falls in lower quartile prices are infrequent, because they tend to be much more resilient than prices in the middle of the market (median prices).

However, given the economic uncertainties facing the world, there's at least an outside chance of further improvements in affordability as the year progresses.

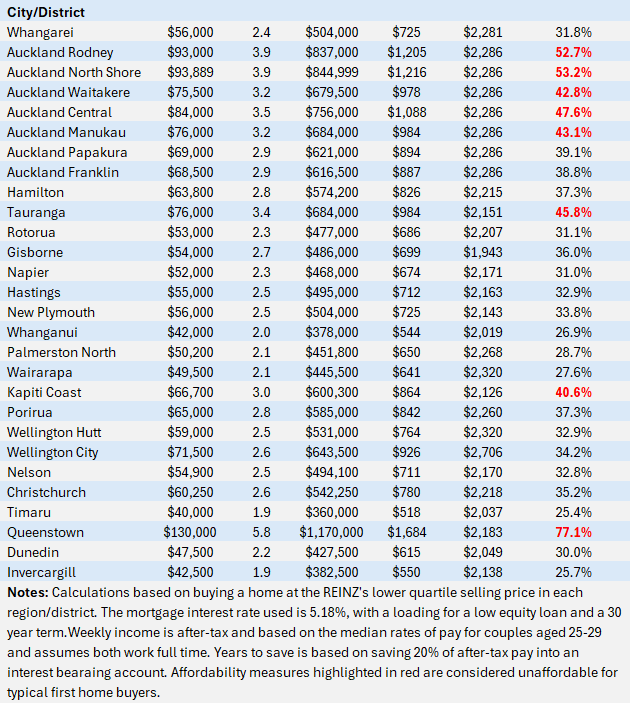

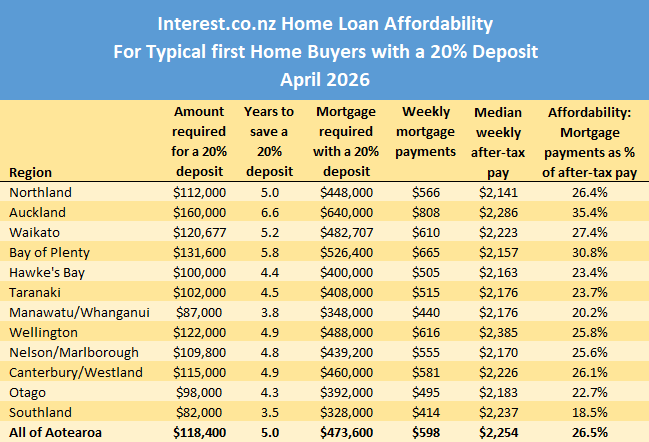

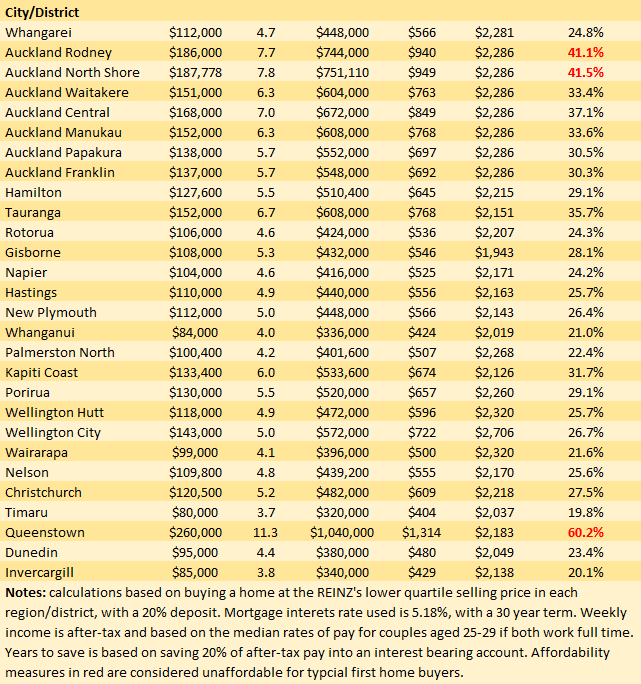

The tables below show the main measures of affordability for homes purchased at the current lower quartile price with either a 10% or 20% deposit. Note the explanations for the affordability calculations, at the bottom of each table.

The comment stream on this article is now closed.

12 Comments

Wow that tables show how far out of whack Auckland is re % of household income still has to be spent on housing, let's not even discuss QTown.... 70%

I'm not sure "spent" is the correct term, more like invested.

We can argue about terminology, but the hard fact is much of NZ is low 30% but Auckland and Tauranga 45% ish...

How much further do Auckland prices need to fall?

I can see the historic value in living in inner Auckland, but these benefits seem to have dissipated since Oct 2021.

Is the higher cost worth it?

House prices reverting to long-term measures of price to h'hold income (3-4x as a rule of thumb) means massive wealth destruction; the capitulation of banking business models; and huge negative impacts on GDP growth.

In other words, we need the K-shaped profile to keep an even keel. This is why Ponzinomics needs to be suppressed to some degree. Bit late to be talking about that now.

I've been reading similar ideas about global equity markets. If it returned to any more long-term sober ratio, the implications could be devastating, particularly for the Anglosphere.

Devastating maybe, but valuable to society in reviewing the real value of shelter vs other things such as energy and essential skills. For example I know how to compost, garden, plant at certain times of year for certain harvest times as a basic skill through my upbringing. I know so many who have no idea and have to search it online or read it on a seed packet.

Invested implies return

Both Auckland and Queenstown share a common problem - high expense to build new houses. Queenstown is restricted by lake and mountains which make land scarce and building is a real challenge. Auckland is restricted by a bunch of..., collectively known as Auckland Council.

Of course, Lake Wakatipu and the Southern Alps are beautiful.

So is the Hauraki Gulf, concerts that only come to AKL and so is the Sophistication

of avoiding random stabbing attacks on AT buses. I suggest that any hidden advantage of AKL living is pre AI, WFH and energy prices, I suggest that rural and regional living is probably now preferable.

https://youtu.be/ZN4vmZSPkFQ There's an INFINITE Amount of Cash At The Federal Reserve - Neel Kashkari

suggest people own some gold, seems like central banks think its a good idea, oh and nothing can fix the ponsi, its run out of suckers.

More property Specarrazi carnage

https://www.oneroof.co.nz/news/mortgagee-sale-of-failed-flips-linked-to…

Everything about this awful when it could be a story about turning hovels into nice places for people to live. An indictment on our collective values.

I presume from the numbers in the article that no or very little tax was ever paid. Absolutely parasitic behavior cheered on for years, especially by his bankers.

Bloomberg research shows the NZ economy it like a strung out Junkie......completely rooted without ponzi cash flowing strongly.

We need this cold turkey for a few more years. Let it roll.

https://www.bloomberg.com/news/features/2026-05-25/new-zealand-s-housin…

Let the junkie detox.....then no more dangerious lending past 4x DTI.

PROBLEM SOLVED.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.