By Alex Tarrant

The Reserve Bank is taking more notice of credit growth data when deciding whether to raise the Official Cash Rate to cool price rises, following last decade's house price boom.

If this were the case before the boom began in 2002/03, the Bank would likely have raised the OCR sooner in its effort to douse the rampant housing market, Assistant Governor John McDermott indicated in a speech to the Bank for International Settlements in Hong Kong.

See the RBNZ's latest housing credit growth figures in the chart below.

McDermott used the speech to say the Bank felt its primary goal of inflation targeting had been successful since being adopted 20 years ago.

The Bank had analysed the success of inflation targeting during the most recent 1998-2007 business cycle, in which a number of shocks led to excess demand pressure and inflationary pressures.

"In summary, that analysis notes that the New Zealand’s economy expanded from 1998 to 2007 and then had a six quarter recession in 2008-09," McDermott said.

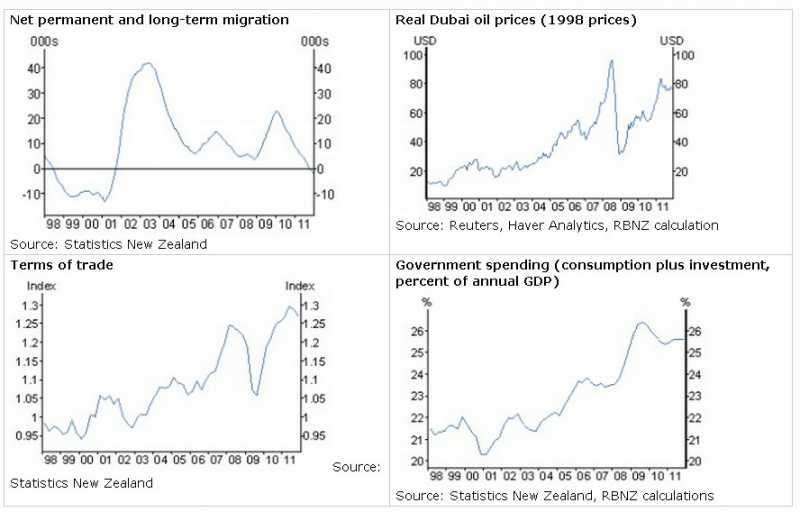

"From 1998 to 2007 there were a number of significant shocks that determined the shape of the business cycle:

- First, there was a strong and unexpected increase in population growth from net immigration in 2002/03.

- Second, there was a significant boost to the economy from a rising terms of trade from 2000, which accelerated late in the period.

- Third, oil prices roughly doubled from mid-2007 to mid 2008.

- Fourth, government spending rose rapidly from 2005. This came at a time of pre-existing excess demand in the economy."

In setting monetary policy, the Bank had to take a view both on how these shocks would unfold and how they might change the inflationary pressure in the economy, as summarised by its view of the output gap, McDermott said.

As a forthcoming Reserve Bank Bulletin article would note, throughout the recent boom, "we expected the output gap to dissipate rapidly. However, as it turned out the output gap remained positive for an extended period," he said.

That meant excess demand could remain long after the underlying shock, like rising migration, had gone.

Inflation pressures

With an extended period of excess demand pressure, average inflation tracked in the upper half of the Bank's target zone during the cycle.

"While the persistent component of inflation was higher than we would have ideally liked during the business cycle expansion, it did remain anchored within the target zone. That outcome was far superior to our experience of the 1970s when inflation was persistently at double-digit levels," McDermott said.

"The difficulty of anticipating how long an inflationary shock will last is central to the forecasting process required for monetary policy. In many models that are used for monetary policy analysis, the output gap often quickly returns close to zero following a simple aggregate demand shock, and it is natural to think in those terms," he said.

"However, the interaction of a persistent aggregate demand shock and inertia in the economy can considerably prolong the time for which the economy is in a state of excess demand pressure."

House price rises; 'We're watching the credit stats'

Even the relatively short-lived large inflow of migrants in 2002/03 had ongoing impacts.

"The housing stock cannot be increased as quickly as the changes in migrant flows. Consequently, house prices rose and, even after the boost to population subsided, continued to rise beyond all forecasters’ expectations," McDermott said.

"Higher house prices in turn stimulated a large construction boom which put further pressure on resources. Private sector credit started to expand well in excess of the nominal growth in the economy," he said.

"In line with conventional wisdom, we put relatively less weight on credit data than on interest rates. Had we had a higher weighting on credit growth data, our view of the persistence of pressure on resources would likely have been stronger much earlier in the boom."

McDermott said the Reserve Bank's monitoring of monetary and credit information had increased in the wake of the global financial crisis.

NZ$ issues

Meanwhile, conducting monetary policy in New Zealand was also complicated by exchange rate issues.

"In a small open economy the inflation target is a complement to a floating exchange rate regime," McDermott said.

During the boom period expectations of tight monetary policy to offset the excess demand pressure probably contributed to the persistently high exchange rate throughout the period, causing considerable discomfort and worries about the sustainability of parts of New Zealand’s tradable sector," he said.

After the global finance crisis there were new challenges for monetary policy to deal with.

"The current recovery in the business cycle, both in New Zealand and in other advanced economies, is proving weaker than historical precedents. Our forecasting frameworks need to be expanded so we can examine possible sources of the disappointing recoveries, such as say the impact of the overhang of public and private debt on the economy," McDermott said.

'It did what it was meant to do'

"Despite the challenges and the ongoing shocks to the economy, monetary policy did what it was supposed to do, keep inflation low. The framework maintained the Reserve Bank’s focus on the target and the frequent publication of forecasts forced us to constantly update our views of the economy and the inflation pressure within it," McDermott said in conclusion.

"The Bank’s analysis on the recent business cycle underscores that the inflation targeting framework is an effective way to conduct monetary policy under a range of testing circumstances and that the framework is a useful tool for future inflation control," he said

"With low inflation and the credibility of inflation targeting came much lower volatility in the general level of prices. That is helpful for resource allocation, affecting longer term performance, and for macroeconomic stability over the medium term. This credibility was very helpful when the global financial crisis hit. To help offset the very large negative shock the Bank started lowering interest rates even while annual inflation was above its 1 to 3 percent target.

"Of course, that is not to say the framework cannot be improved in any way. Over the course of the past 20 years or so the framework has evolved to reflect lessons learned and is likely to evolve further in response to new developments," McDermott said.

"In particular, our monitoring of monetary and credit information has increased in the wake of the global financial crisis. The Reserve Bank has also been looking into the effectiveness of some macroprudential instruments that may limit build-ups of problems in future periods of rapid credit growth," he said.

Here are the four shocks McDermott referred to:

No chart with that title exists.

18 Comments

The Reserve Bank is taking more notice of credit growth data when deciding whether to raise the Official Cash Rate to cool price rises, following last decade's house price boom.

If this were the case before the boom began in 2002/03, the Bank would likely have raised the OCR sooner in its effort to douse the rampant housing market, Assistant Governor John McDermott indicated in a speech to the Bank for International Settlements in Hong Kong.

John Mc Dermott, YOU WERE WARNED by private business individuals like myself in formal letter back in 2003 through to 2008

You (RBNZ) told us to shove off!

So.......how about a "we were wrong, you were right", and then a resignation by you and Bollard immediately?

But credit growth was successive governments policy.

Encouraging personal credit growth? or government credit growth which is the same regardless as government fund their credit by taxing us.

Not sure I follow your point Ralph. What are you trying to say knowing full well the global monetary ponzi scheme is now after just 100 years maxed out? sorry.....maxing out

The same except for who decides to borrow the money and who assumes the liability specifically. Only those who pay tax greater than they receive transfer payments from the government end up paying (net).

I am saying; even as late as 2008 George Bush was saying the US government wanted everyone in America to own their own home.

Justice - glad you put the warning in writing. I also did and sent emails and wrote about this in a business magazine at the time. I never got one response from them.

Calling for McDermott and Bollards resignations is imperative but all those running Government at the time should be held accountable as well as they knew what they were doing and the consequences that it would have.

Helen Clark and her Govt have a lot to answer for, they opened the flood gates on immigration and the idiots in the Govt Depts never had the commonsense to understand any of the implications this would have on the economy. Clark held Ireland up as one of the wonderful economies in the world she also bleated on about how values on property had increased and that all kiwis were better off because their house was worth more.

CPI data was con-pletely ignored oh sorry I meant completely.

NZ must identify exactly what role a Government should play! This would then filter through to all Govt Depts and their roles and functions.

the rbnz are creating the perfect storm. if they they think they can constrain credit growth forever, it aint going to happen. sure heaps of ppl are now on floating as opposed to back in 2008 when they were fixed and therefore upping the ocr will have an immediate impact - problem is most have factored this in already and rates are historically low. the only ppls they will hurt will be speculators and new home buyers! Furthermore because housing stock is now ageing and new builds are non existent, and we have a banking sectory trying to create demand artificially, we now have a mini credit boom feeding the bubble further. this is bolstering ALL property values to silly levels. release some land in Auckland for development, drop compleince costs, and GST on new builds and let the market settle. this will have a far better outcome and ensure house price infation is constrained. basic economics i would have thought. the rbnz is playing a very dangerous game

Game over is getting closer by the day for the RBNZ. All their optimistic predictions have fallen off a cliff. Remember the term a few years back "soft landing". We haven't even hit the bottom globally yet!

Private sector credit started to expand well in excess of the nominal growth in the economy," he said.

"In line with conventional wisdom, we put relatively less weight on credit data than on interest rates. Had we had a higher weighting on credit growth data, our view of the persistence of pressure on resources would likely have been stronger much earlier in the boom."

Moreover, our banks in connivance with supranational entities benefitted from NZD debt issuance at rates below or around the levels available to our government.

This supranational NZD debt issuance cheerlead by the World Bank was labelled Eurokiwi/Uridashi bonds.

{kind=link}

The resultant monetised NZDs were cross currency basis swapped into the coffers of our local banks at rates well below the OCR rates imposed by the RBNZ, in it's valiant, but failed attempt to contain the damaging credit growth, despite McDermott's denial.

{kind=link}

In effect, the credit wrapping function of highly rated supranational entities allowed the local Aussie banks, in particular, to circumvent the rate hiking endeavours of the RBNZ.

Well said; all the more reason to install some credit growth controls on the banks; at affordable interest rates for the economy.

As well, to circumvent the supranational entitities profiting at our expense; to keep a lid on the exchange rate that this activity otherwise causes to artifiically inflate; and to reduce some of our debt; we could embark on our own QE to manage our monetary policy. I sort fof understand an intuitive reluctance to agree to money printing, so will attach yet another story from the UK today.

http://www.cnbc.com/id/47870071

A story about UK inflation dropping to 2.8%, (from a recent average of 5%) and so leading to almost certain QE next month. The UK has been easily the world champion money printer over the last 3 years, and it has clearly saved their manufacturing, housing, and general employment stories in the face of the decimation of their previous heavyweight industry, the finance industry.

One quote from the article follows.

"It's obviously not the main story in town this week, but it's helpful if they (the Bank of England) want to do more QE as soon as July, “Ross Walker, UK economist at Royal Bank of Scotland, added.

There isn't any need anyway to sell all our power companies, but if there were, this approach gives an easy path to avoid such giveaways.

"The resultant monetised NZDs..."

Stephen.... Can u elaborate on this.. What are u saying.??

Are u saying that the reserve bank simply creates $NZs' to allow foreign currencies to be exchanged for $NZ...

Cheers Roelof

Not at all. - the Japanese and/or European purchasers of these notes secured excess trade deficit NZD or financial institutions such as Nomura used their NZD credit lines, at local banks, to settle purchases of the notes. Either way the electronic promises to pay, issued by the supranational, had to get the element of moneyness attached to them.

Stephen L...we have a number of countries throughout the world with negative, or very low, growth rates, yet have much higher inflation than you would have otherwise expected...damn it you even have Greece in a depression, losing 20% of GDP in the past 3 years, yet it has had 10% inflation over that period...money printing cures all right ?

So to say it is successful you have to fast forward to the time when there is an eventual "recovery" and that money has to be plucked from the economy, or otherwise considerably higher inflation will be a certainty. What do you think that will do to an economy when these days just stopping money printing for a period crashes every leading economic indicator ?

There is a damn good reason why only desperate countries print money, they have no choice, but the long-term trade is always a thousand worse than for those that avoided it, even taking a little pain to do so.

Grant A,

Lets see how the UK's inflation pans out. They have had 2-3 years of highish inflation at around 5%, apparently now dropping back, and they have printed in total a whopping 23% of their annual GDP, with more to come it looks like. Greece has not printed a cent- its fundamental problem is that it cannot, and so it has a cost base that is perpetually uncompetitive.

New Zealand is behaving like Greece in that our cost base is 20% uncompetitive according to the IMF- and the current account deficit supports that view. The easiest and best solution to that uncompetitiveness is to get the cost base right by devaluing. Greece cannot do that.

The short term alternatives are: 1) to keep borrowing money off countries in order to buy goods off them- which is what Greece did for donkeys- about the same length of time NZ has. Remember that those countries, particularly Germany, couldn't throw enough money at Greece in the good times. Sound familiar. One day the markets suddenly say enough; and then your destiny is frankly out of your hands. Or 2) to lay off 20% of the workforce in a deep and vicious cost cutting spiral (the current German model for Greece); or 3) to drop everyone's wages by 20%- legally and practically impossible, as well as economically stupid.

I partly think the day of reckoning is already here; who is telling our government to sell our power companies?

Do you agree that the current account is the major cause of our indebtedness, and therefore of our relative lack of wealth for what we actually produce? And if so; what would be your solution? Kick the can for another couple of years, I assume?

Or an element of internal devaluation is implemented along side an external one.

The right to treat oneself to excess profit margins and/or salaries is endemic in NZ.

The costs in lost business are far greater than the benefits of keeping import based shopkeepers and their financial handlers and non-productive overpaid civil servants etc first in the credit queue.

"you even have Greece in a depression, losing 20% of GDP in the past 3 years, yet it has had 10% inflation over that period...money printing cures all right ?"

Greece can't print... i thought that was pretty obvious, and i consider myself financially illiterate but learning. Do you work for a bank or finance company Grant? or maybe a government, directly or indirectly?

Credit is the lifeblood of the NZ property speculators economy...it will never be throttled down by the RBNZ....the parasites are in control but are happy to let Bollard dance on the stage.

How many times must this be pointed out!

It is up to Kiwi peasants to give the parasites the big finger when it comes to the drugs on offer. The sooner most of us realise that..the sooner we will begin to see an improvement but it will still take decades of effort.

Just don't expect help from govt or the RBNZ.

Ask not why Key is prattling on about 'standards' in skools..ask why he is not blathering on about the need for rugrats to learn about thrift and the dangers of debt.

A lot of truth in what you said there Wolly......yes there is.

I agree on the big finger being given to the pushers...the difficulty there is overcoming what is now ingrained in the N.Z. pysche.....the fear of being less than equal...the aspirations to be more than the norm....the inescapable security trap.

For the most part particularly in the post boomer generation the answer has been to borrow into it and worry about it later without conscious thought to debt enslavment , because the outward perception of their neighbour would be one of success.

" borrowing your security "....?

The RBNZ rightly hide behind the successful dischage of their charter (focus) to contain inflation...but have wittingly (I believe) allowed other parts of the economy to become exposed in the process.

As it is too hard for me to imagine they (the RBNZ) were not "aware" the continuance of cheap credit would fuel the hot bed of debt enslavment in the property industry , I can only guess they were a willing party to, or accepting of private debt growth of dangerous proportions when interest rate trends begin a reversal.

In that trade off I would imagine they would have factored in Banking Industry profits to be a positive on the ledger.

But that leads us to judgements made for the greater good and it would appear , (outside of meeting the charter,which in itself is open to debate) ,it has not been for the greater good , or will not have been for the greater good as trends reverse.

I think however we all need to appreciate that Bollard an Co have inadvertently locked themselves in to a holding pattern, because the exposure they have caused in other areas would shift dramatically with a policy change......a case of ,we would rather be recorded as having been seen to do the right thing, rather than ,we got so far in we couldn't get out....

While this has been an incredibly painful period for exporters ( outside of the big F hedgers), with, I've got to say, no end in clear sight , two things will happen when trends begin reversal.....You will get your cure for debt appitie.......Bollard will get an F historically with a great.......big....fat.......pension.......and maybe a little Bonus from the Banking Industry .

I just couldn't help posting this here.

Dummies guide to what went wrong in Europe.

Helga is the proprietor of a bar. She realizes that virtually all of her customers are unemployed alcoholics and, as such, can no longer afford to patronize her bar. To solve this problem she comes up with a new marketing plan that allows her customers to drink now, but pay later.

Helga keeps track of the drinks consumed on a ledger (thereby granting the customers' loans).

Word gets around about Helga's "drink now, pay later" marketing strategy and, as a result, increasing numbers of customers flood into Helga's bar. Soon she has the largest sales volume for any bar in town.

By providing her customers freedom from immediate payment demands Helga gets noresistance when, at regular intervals, she substantially increases her prices for wine and beer - the most consumed beverages.

Consequently, Helga's gross sales volumes and paper profits increase massively. A young and dynamic vice-president at the local bank recognises that these customer debts constitute valuable future assets and increases Helga's borrowing limit. He sees no reason for any undue concern, since he has the debts of the unemployed alcoholics as collateral.

He is rewarded with a six figure bonus.

At the bank's corporate headquarters, expert traders figure a way to make huge commissions, and transform these customer loans into DRINKBONDS. These "securities" are then bundled and traded on international securities markets.

Naive investors don't really understand that the securities being sold to them as "AA Secured Bonds" are really debts of unemployed alcoholics. Nevertheless, the bond prices continuously climb and the securities soon become the hottest-selling items for some of the nation's leading brokerage houses.

The traders all receive a six figure bonus.

One day, even though the bond prices are still climbing, a risk manager at the original local bank decides that the time has come to demand payment on the debts incurred by the drinkers at Helga's bar. He so informs Helga. Helga then demands payment from her alcoholic patrons but, being unemployed alcoholics, they cannot pay back their drinking debts. Since Helga cannot fulfil her loan obligations she is forced into bankruptcy. The bar closes and Helga's 11 employees lose their jobs.

Overnight, DRINKBOND prices drop by 90%. The collapsed bond asset value destroys the bank's liquidity and prevents it from issuing new loans, thus freezing credit and economic activity in the community.

The suppliers of Helga's bar had granted her generous payment extensions and had invested their firms' pension funds in the BOND securities. They find they are now faced with having to write off her bad debt and with losing over 90% of the presumed value of the bonds. Her wine supplier also claims bankruptcy, closing the doors on a family business that had endured for three generations; her beer supplier is taken over by a competitor, who immediately closes the local plant and lays off 150 workers.

Fortunately though, the bank, the brokerage houses and their respective executives are saved and bailed out by a multibillion dollar no-strings attached cash infusion from the government.

They all receive a six figure bonus.

The funds required for this bailout are obtained by new taxes levied on employed, middle-class, non-drinkers who've never been in Helga's bar.

Now do you understand?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.