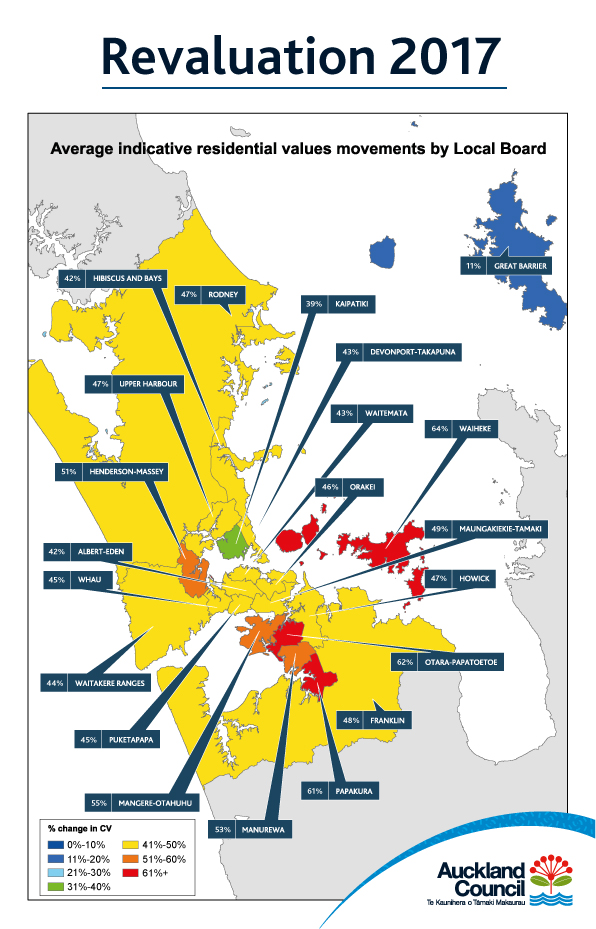

Auckland’s property trend revaluation data shows significant value movements across the region and an overall average increase across all sectors of 45 per cent.

Reflecting the upward trend in the Auckland property market, the residential valuation shows an average increase in value of 46 per cent since the 2014 valuation.

Higher demand in outer suburbs

Local board areas with the largest movements – of more than the 45 per cent average – are in Waiheke, Ōtara-Papetoetoe, Papakura, Māngere-Ōtāhuhu, Manurewa, Henderson-Massey, Maungakiekie-Tāmaki, Franklin, Howick, Rodney and Upper Harbour.

Movements within the remaining boards range between 11 per cent and 44 per cent.

The largest movements in the outer suburbs appear to be a result of higher demand in areas where property is less expensive.

Central Auckland values now increasing near average rate

Auckland Council Head of Rates, Debbie Acott, says that Aucklanders should remember that a high increase in property value doesn’t necessarily mean there will be a corresponding increase in rates.

“We expected to see an increase in valuations since the last revaluation in 2014, so movements in the 40 per cent to 50 per cent bracket really aren’t a surprise,” she says.

“Generally speaking, the values in Auckland’s outer suburbs appear to be catching up with the 2014 revaluation.”

“Areas that increased the most in the last revaluation – by and large central Auckland – are now moving roughly along the average. Those that didn’t last time – mainly outer Auckland – are the ones with the highest increases this time.”

“Property valuations are used to help us work out everyone’s share of rates – they don’t mean that we collect any more money. However, we won’t know the impact of this revaluation on rates until we agree our next budget in 2018, so I encourage Aucklanders to view these valuations with that in mind.”

Lifestyle properties show 57% increase in value

Commercial and industrial properties received a rise of 43 per cent and 47 per cent respectively, while lifestyle properties increased by 57 per cent and rural by 35 per cent.

Property owners will receive their notices in the mail or via email from 20 November.

“Because of Auckland’s dynamic property market, and valuations only capturing a moment in time, they should not to be viewed as current market value,” says Ms Acott.

Population growth, low interest rates drive increases

Auckland Council chief economist David Norman says that the rise in residential property values reflects at least three things.

“First, Auckland’s strong population growth over the last three years has not been matched by increases in the number of new houses being built, and this has pushed prices up. Second, record low interest rates have allowed people to bid up prices to secure somewhere to live because housing has been in short supply. And third, the Unitary Plan has added a lot of value to properties that can now carry higher intensity residential development than before.”

All councils are required by law to revalue every property in their region every three years. This year in Auckland more than 549,000 properties have been revalued, including every piece of land except roads and waterways.

Individual property data will be available from 20 November at the Auckland Council website.

Download a copy of the indicative residential average change in capital value since last revaluation

Download notes to the indicative residential average change in capital value since last revaluation

131 Comments

Dear boomers,

There are 81 million dollar suburbs in Auckland.

This is why we don't own houses here. Not because of avocados.

Pray for us.

Peace and love, millennials.

Most of these CV's are probably already out of date in this sick market. Only by listing does one figure out if buyers are as keen! Like others here, I wonder if the present torrent of new listings will morph to apocalyptic proportions after release of CV's. FHB, your patience will be rewarded - market is heading down.

It certainly looks this way... I sure hope we're right!

Early and mid boomers ate all the cream out of the economic cake

Millennials have every right to call out unfair

Hold onto your horses cause GFC2 will upend the worlds biggest e con ponzi as quantitative easing unwinds

Just remember millennials the world debt roosters will be coming home to roost

Your time will come

Latest comment from The Economist on rich-world countries: "A new report finds that global wealth rose by 6.4% in the 12 months to June, the fastest pace since 2012. But millennials have a lot of catching up to do. Higher student debts and the difficulty of buying a housing have made it harder for them to save. That disparity might come back to bite baby-boomers. When boomers want to cash in their assets, they may find millennials cannot afford to buy them at current prices."

Philly

Yes that 6.4% increase is a fluctuating number which can and will turn negative when GFC2 hits markets

The millennials will have their days in the sun I know they will

Life is a short game but there’s enough time in it to experience many ups and downs and boomers won’t have it all their own way forever.

Alzheimer’s will hit a number of them and strip them of wealth among other catastrophes

Once the new migrants can get NZ residency it won’t be long before many will seek a faster pace in Australia’s bigger cities either.

People over emphasis their own back yards especially those who cant live in other parts of the world

Look wider not just NZ would be my advice to millennials

Well I am breathing a sigh of relief for now, as my rates look as if they will go down but I really feel for the less affluent suburbs that look like they will have huge rate rises and what makes this awful is I suppose most people will be renting in these areas and the landlords will increase the rents.

Why aren't landlords charging more rent now? Answer: Because they are charging the marginal amount their tenants can pay already! No business owner, no matter what it is, 'sells' their wares for less than the maximum they could get.

I suppose we will see stressed landlords putting their rental properties on the market with outrageously high asking prices next week when they receiving their new CVs and the first release of properties caught out by the bright line test introduced two years ago in October.

In free markets, market price equilibrates quantity supplied and quantity demanded. Works in both the residential property rental market and the residential property ownership market.

Only to the extent that The Buyer can afford to pay? If a tenant can't afford to pay $X + % increase...they'll just go elsewhere. Sure, it may be 'downmarket' and those rents will appreciate relatively, but eventually, properties 'out of reach $ wise' get left empty. Then what do those landlords do? I'll tell you ....DROP THEIR RENTS! Because any rent, is better than no rent, and when The Top comes down, it will compress all property rents below them....

Trouble is, this dysfunctional market has been propped up by importing ever more people to fill the gaps left by those who have had to abandon their own home towns.

"Kiwis don't know how lucky they are to face low wages and unaffordable housing! Look how many people are happy to come from the third world and face these conditions instead!"

The rates in the less affluent suburbs will go up, yes. But not to a total anything like the rates payable in the more affluent areas due to Lens' and Phils' extremely low uniform annual general charge and high variable split.

Do you mean that everyone is going to be badly effected by this 45% increase not just the properties over the average. I thought Phil Goff said that rates would not rise above 2.5%. I think I should just keep quiet and try to listen to you all as I am well over my head

Like the Republican Party are to cut corporations taxes and retain all the loopholes so too the Auckland Sup City passes the rates burden to the cheaper suburbs

It’s called class warfare by the rich politically well connected to get what they want and force everyone else to give them a tax or rates break

Ain’t Human’s greedy

My 2014 valuation + the % change for my suburb = within $1k of the valuation I got last month. Sounds good to me

The valuers and the council used the same formula?

How did you work that out?

When two estimates coincide with less than 1% variance I think it's a reasonable assumption that they used the same methodology.

Thank you

Does anyone know how the Council revalues after a new home has been built do they ask the builder the cost of the build, do they come and assess it or do they guess on a square meter basis?

Simple regression analysis on TradeMe listings.

I kid. Wouldn't be surprised though.

That's funny. I suppose I could start building at the beginning of the year have it completed nine months later and the CV could quite possibly be lower with a house on it after all the prices have crashed. That would work for me, I might suggest it.

Your designer or Architect has to put a $ value of construction cost on the building consent application. There you go.

Thank you that information is really helpful

My pick would be an educated guess. Yes there is a spot in the building consent form for an estimate of the construction value but that does not include the cost of land. Today is the first time I have ever heard of a council employing a valuer (in the modern era). Usually someone in the rates department has to notice that a capital project has been completed on a plot of land and update the rates records. (Remember empty sections are already paying rates.)

Property valuations are carried out under contract to councils (mostly by QV but it can be by anyone) on a three-yearly cycle. The valuations aren't supposed to be particularly accurate. QV will look at some sample properties in depth and extrapolate over the rest. I would be surprised if any council cared enough to get sporadic valuations of new dwellings done between re-valuations.

So a staff member makes an educated guess to get the records up to date and enable the council to charge higher rates. And it all gets tidied up at the next re-valuation.

The good news is that they can't charge the higher rates until the following financial year. So try to finish your building project on July 2.

I am already paying rates on the land I was just trying to establish how the Council calculated the increase in value after you had built. It appears you just add the value/cost? of the building which is estimated by the architect. I will need to investigate this further as I would imagine the value would be more (or should be more than the cost), however it would be helpful to me to have the lower figure recorded. The way my architect is going it will be two years away. The cost to me of his mess and the resulting delays has cost me enormously as the cost of building has increased dramatically which would probably negate any saving in finishing the project after July 2, but every bit helps. Thank for you reply

I'm not 100% sure of the mechanisms but in a council that rates on capital value they will simply add an amount in the box labelled "Improvements". It could be the nominated cost of the project (from the Building Consent) although a better method would be to use the QV data from the last revaluation and just calculate a number based on the scale of the project (i.e. floor area).

Bear in mind councils don't need accurate data just data that lets them rate progressively so that low value properties (as a proxy for low income) pay lower rates than expensive properties.They aren't going to worry at all if they are guessing at the capital value of a new dwelling for a couple of years.

Often the calculations have no relationship to the land topology, usability, the house standing on it or those next door. Whole suburbs are treated with the looks good on paper valuation brush and rarely does QV actually value a property or group of properties, (normally they only go out if someone complains, most just blinding trust them). Hence QV valuations can easily be shown to be faulty and if you get value that does not meant the actual land value and improvement cost then you can present that information to them for review. Normally they just copy the value another company provides in the review. Ah QV a buggered algorithm, poor add on services and relying heavily on existing contracts with councils for work.

The only time I would complain to the Council about my RV would be if I thought it was too high and were paying more than my fair share of rates, unless I were going to be selling. I know, RV does not equate to market value, but believe me there are plenty of people out there who are blinded by RVs. I would expect there to be a huge standoff between vendors and purchasers in the coming months

Rates win for owners....left wing council all smiles. End of the day, money to grow AKL has got to come from somewhere.

I hope every ambitious young kiwi leaves and never looks back. There are much better places in the world to be than this dive.

Like where?

I just sold my 220 sqm property in Sydney and bought a 500 spm property in Auckland for the same price. Auckland one is 5ks from the CBD.

There is still value in Auckland property relative to other big desireable cities.

Like Melbourne, Sydney, New York, Perth, London, Ireland, Los Angeles, mainland Europe, Canada etc. Young Kiwis aren't homeowners, and the home ownership rates for 20 to 35 year olds are still falling. There's no point staying in NZ with a low wage job, high house prices and a high cost of living when you're better of outside NZ.

That's cool. NZers have been leaving for years...and some even come back.

I don't think you're going to find bargain housing in half of those places though...certainly not Melbourne, Sydney, New York, London, Vancouver, Toronto, Paris...

Many of those places have much better pay rates, better job opportunities (especially in skilled work), and they actually have transport systems available to the public at large. Take Sydney, transport is not only available it is plentiful and disability accessible, housing is comparatively cheaper (for equal quality, age, facilities and time to work), cost of food is lower and the jobs in engineering are far more available. Many highly skilled NZders do leave, especially where roles require specialization and quality above the level of doctor, and they pay off the loan and save up. Many do not come back for years, some do when they want to have kids. That way when they do come back they have the a higher career entry level which is more employable in NZ than just a mid level skilled role, savings ready for a NZ house, loan mostly paid off, and get in ready for the free kids healthcare and schooling. It is win win. Although the downside is the Australians.

Again, people are fooling themselves if they think Sydney and Auckland are equivalent in the desireability stakes.

Auckland is definitely better than Sydney in many ways.

You're welcome to leave Brock

Actually it is you evil property vultures that should leave but of course you wont. Too busy screwing this country

Brilliant. Encourage the young Kiwis to leave their home country and to not come back. That's what we need to improve NZ.

These parasites don't care if they kill their host.

We bought at 85% of the then CV in 2009. Based on our area average increase, the homes.co.nz value will be at 87% of the new CV. Seems about right for a base value, albeit the Council/Valuers would have no idea of the $ tipped into renovations as none had to be permitted so who knows what the true value is. We're not going to argue the case as we don't want to up the rates bill.

I would like my property valued as low as possible as I may end up building a house that I cannot afford to pay the rates on.

My rates bill is $4,900 or ~ 2% of CV. I imagine that's the margin for error on any number of bills that come with building a house.

A stand alone house in another large city of NZ in which I have an interest, has a RV of $1.3m. Rates are $6600. I appreciate that a greater number of higher value homes in big cities will depress the average rates payable on more valuable homes but when comparing just the cost of rates, we don't have much to complain about in AKL.

You would expect some economies of scale with ~ 550,000 properties.

I'm not sure places with a population less than 500k can be called a "City" in this day and age. A city I think has to be over 500k even 1m. The days of requiring a City to have a cathedral is dated...it's a numbers game.

Have you slipped a decimal place there? $4900 at 2% of CV suggests a CV of $245,000 which seems unlikely for Auckland.

Sounds like Ex Expat must be living in a trailer in the Takapuna holiday park.

(I wouldn't knock that...a nice location with good morning walking.)

Correct, it's 0.2%. Reminds me of the time a customer rang and said his bank had told him his accounts didn't balance. Must be getting old.

Thank goodness for that, I was seriously beginning to think I was an ignoramus (probably still am) but I was unable to reply to you as I could not understand.

I had to look up my rates bill it is $2,950 so i suppose I will have to more than double it maybe treble it. I might have to pitch the tent.

Question time for the thinkers.....were valuations in Dublin overpriced by a 100% before their bubble burst or 50% undervalued after the bubble burst?

And if a valuation agencies can have their estimates wrong by a factor of 50 or 100% - what value do they really have in the big scheme of things? If I were wrong by 50-100% in my industry, I'd be certain to be out o a job....but I'm sure Auckland council and other valuers are on top of their game and the valuations they provide are a fair reflection of the actual price of housing, without any irrationality included in pricing..(sarcasm?)

Some houses in CHCH are now on the market for below the 2016 valuation - either the valuation was never right or the market has shifted that much - take your pick. Something is only worth what someone will pay for it.

(and by the way I'm surprised how many of those houses are empty)

For a Dublin style fall you need a banking crisis. The banks, I thought until I read the scandalous Westpac news yesterday,are meant to be over capitalized.

Funny you should mention Westpac, I cleared out my account there today for the same reason..

The staff had not even heard that story....Makes me wonder...even more.......they advise us....not supposed to be the other way around.

I thought it 'scandalous ' they were over stretched too.

By no stretch of the imagination are they safe and sound...apparently. ...Not enuff in the 'Bank"

How bizarre a way to run a sound business....into the ground, leveraged to the hilt....I thought that was just Awklanders.

But, then I think it is scandalous that just about every Country known to man, is in the same boat....still.

Trillions in debt...even a picture tells a story.....450million....is safer hanging on a wall....than by a thread in a bank.

Not that I had that much.....Oh well......A few Guinesses.....will help Dublin...if nuffin else....

...

When I had a meeting with my bank and asked them what they thought their secure limit was under the OBR they had not even heard of it, that was a personal banker not just the teller. I do wonder whether they have been told not to engage in discussions regarding this subject as it seems bizarre they have no understanding of the situation considering that is their profession

Higher valuations = higher annual rates = higher income for Auckland Council = more people on 100K+ and 200K+ salary. Work harder, the council is depending on you

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

That's not how it works - the valuations are irrelevant to the size of the budget, it just decides each household's share of the budget.

err.. get a job with the Council and you'll see how the fund being used.

The argument over how the Council sets its budget and spends it is completely separate to this story about valuations. If they doubled all valuations overnight then rates bills, the budget and spending do not change.

It's forecast in LTCCP

What a disaster for Auckland.

Heaven forbid how teachers, nurses, care workers, police, firemen etc will live in this city.

Hopefully Kiwibuild helps repair this disaster

Already a major issue: http://www.radionz.co.nz/news/national/343918/teacher-shortage-i-ve-had…

How can teachers build a life in Auckland? They can't, really.

This is why National needed to do what they campaigned on an address the housing crisis, rather than denying it for the next nine years. Very disappointing.

They live in a rental with flatmates – indefinitely. Like those in many other professions.

The 'indefinite' of it is what grinds, after many years. You just run out of hope for the future.

That's the thing, eh.

They can live in a holding pattern but they can't build a life.

It's only a disaster if you're not an owner

so, how bout all those young kiwis entering all these critical professionals, that support many of the boomers who have done so well for themselves?.

NZ's future has been sold down the river by successive National and Labour govts, all in the name of flimsy GDP growth

Disgrace

Well growth does allow us to buy nice new shiny things: "Core Crown tax revenue was $75.6 billion, up $5.2 billion (7.4%) from the year before, with most of that coming from growth in nominal GDP".

Now I do understand that growth driven by immigration has costs to it. But just think about trying to provide existing government services if growth was negative, nevermind incerasing demands from things like health and super.

Yvil, it's only a disaster if your not an owner. Is this the message to give a tenant just prior to demanding more rent? Seriously now, who are the buyers at these lofty valuations - tapped out tenants or the shrinking pool of fools? Market heading down. Realestate.co.nz, Auckland @ 13438

Personally, I don't have too much faith in KiwiBuild.

Good intentions, undoubtedly, but the new Government will likely end up with major fiscal problems relatively soon. KiwiBuild will have to be scaled back - which will disappoint many people.

TTP

It's still far better to give it a go and fail than do nothing and tell everyone that unaffordable housing is a sign of "success."

Kiwibuild promise of 10,000 homes a year (40 per working day) in this regulatory environment? Required rate rising every day as they have already fallen far behind in 6 weeks since election.

But Jacinda assured us she doesn't lie, so there won't be any scaling back.

Foyle. Even you must understand it takes time to get such schemes underway.

Oh yes, just pointing out the mountain they have to climb is getting steadily higher, and that talk is exceedingly cheap.

Are there any commentators here who would put money on them delivering on their kiwibuild promise over the next 3 years?

Only for horrible shanty towns

The former council flats at the top of Shortland Street are now desirable apartments in a building that doesn't leak. That's a government build result of yore - as are quite a number of the weatherboard 100-120sqm houses that enabled Kiwis to achieve home ownership.

.... multitudes feeling good about gazillions of dollars worth of dog boxes in a city rapidly going bust. We gotta be one of the stupidest peoples on the planet.

Well we did have the largest sharemarket boom and bust (60%) the world has ever seen in 1987. NZ'ers love a good bubble.

We would be - but the competition out there is fierce.

What do you base your comment that "AUckland is going bust" based on ?

this new valuation just means investors having to pay more rates, even though the market has changed, ie falling..

The old RV was anyway ignored as people bought/sold based on market price. so cant see the new RV having any difference apart from people having to pay the council more

100% correct. RV is just for local body taxation. Auckland City is at the max of its borrowing limits based on revenue, so expect them to "go for the doctor".

100% incorrect, higher valuations do NOT mean higher rates

To clarify....you think the cash desperate council are not going to lift rating revenue on the incoming 45% value uplift...?

Of course they are.

If they were going to take more money, there were going to do it no matter what the CVs were. CVs just determine how the cash grab from the council is spread out between you and your neighbours, the total grab the council takes is what the council sets.

For the millionth time, higher CV's do not mean higher rates,

Well said (repeated ) Yvil. Some pretty stupid posts this afternoon

Although this has been true historically we now have a severely cash poor council so one does wonder.

Prediction: surge of new listings next week.

This bubble is about to spectacularly explode.

yes, suspect you are right. What many have saying here for 2 years or so has suddenly become 'news' to mainstream. Still amazes me that some long time readers of this site have been (and still are) in denial. One would think that 'business' readers would have a bit more nous (or are they all ppty sprukers?)

Hamilton: Seems to be happening, trade me hit 701 yesterday, a 12 month high from just 580 listings 12 months ago. Now just hit 722. It's all on folks.

It must have been a good ride for them – I guess you start to believe your own hype when your net worth soars to those heights.

I don't respect them for it but I can't say I wouldn't have dabbled in property investment if I was of that generation.

> TradeMe Auckland Properties 11949 listings

I reckon she'll hit 12,000 tomorrow. Happy days.

And just you wait til people receive their individual 2017 valuations on Monday....

Next week I think you will find quite an increase in the amount of listings as vendors try and cash in on their increased RVs. What happens after that is somewhat reliant on how desperate the REAs are and whether they will try to explain the reality to their clients, that RVs do not reflect the market value. I have been to a few open homes recently and when I have tried to open a discussion regarding dropping houses prices the REAs flatly deny the fact that house prices are dropping.

You'd be quite right, seeing as the RV's tend to be a benchmark for sales i.e. get as far away or over the RV as you possibly can.

AKL houses will be selling below CV in 2018. Mark my words.

They probably already are. Listings pile grows larger, selling volumes shrinking.

Yep, property prices are about to drop 120 to 150%

Yvil, only at Briscoes - this weekend only.

i agree with Zachary Smith that property will drop by 150%.

see you at Briscoes.

Does anyone know if banks require insurance over property they hold as security to be updated based on new valuations?

Not sure what the bank requires, but I insure for the cost to reinstate the house, retaining walls etc, which is a relatively stable amount that needs annual adjustment for construction cost inflation. The CV or market value of the property is largely irrelevant.

Not sure I follow, if the mortgage is $200k (say) and the house now worth $300k as long as the bank's "bit" is insured the loss of that gain is all on the owner surely? On the other hand, its also a full recourse loan, so if the property value drops to $150k from $200k I'd assume the insurance company wouldnt pay out $200k anyway, only the cost of re-building to $150k and the owner would again face repaying the $50k loss to the bank.

Ok, so if you have a mortgage on 80% of the value, would the bank require you to update them on a regular basis that this part is insured for full replacement?

Oh boy...

More BS spin courtesy of ASB. I especially cracked up over the line "weakly positive house prices in October":

https://www.stuff.co.nz/business/property/98894726/falling-auckland-hou…

Thanks for the link. Why "BS" ? it's quite an accurate, neutral piece

Woohoo !!!

"Lifestyle properties show 57% increase in value."

I think this is the big problem indicator. When a city's land cost rises faster than the housing value; 57% vs 45%. The relative value of the city living is shown to be in decline.

Which means if either or both of the current price drivers reverse course:

"Population growth, low interest rates drive increases"

may be substantially lower than previous expectations may have caused us to believe. And we have just elected a government seemingly determined to reduce population growth.

Or it might be boomers selling up in the city and head for the hills. Not too far though, as still will appreciate the odd visit from grand kids.

In a healthy city their capital would be getting replaced by wealthy investment capital faster than the boomers hit the exit. Shouldn't even be close.

Maybe could be a by-product of general Auckland planning idiocy? Large numbers of lifestyle blocks offer shorter and more convenient commutes than the new suburbs Phil Goff likes to build.

Any Boomer who Heads for The Hills should understand 'what that means' before they do it!

"Life Sentence Block' is a better term for anything over half a hectare! If an ageing body wants to mow the 'lawns' for 10 hours a week...then go for it! The only thing worse is buying a Place in The Vineyards....and all that is entailed with actually growing; pruning; fertilizing, picking the things, and then hoping it doesn't hail....

I agree, but a lot of these new blocks have been subdivided with a council requirement to have a large portion of covenanted bush. So a growing number of blocks are actually just big sections with a bush view.

Your not thinking ahead all that land is going to be sub divisable at the stroke of a pen within 5 years. Prices are going through the roof

Talk about blaming the wrong people !

There is nothing special about Baby Boomers , we are just an amorphous bunch of modern day Plebians , and like the next man, we as individuals, have been largely unable to influence events that have unfolded , over the past two decades .

We are certainly not to blame for the current Auckland housing crisis .

Many scribes , poets and lyricists have written of how the youth blame their fathers for all their ills . The words of Bob Dylans Times are a changin' is particularly thought provoking in this reagrd

I blame my fathers generation for the Second world war and to some extent the Cold War ( was it all worth it ?), and I recall as a child my father being indignant about how the Dutch settlers where he grew up treated their indentured labourers as slaves .

So those who cast the stone upon Baby Boomers would do well to remember that their children will one day too, have reason to complain about them .

Boatman, no offence to you personally, but the Boomers started the mud slinging! There have been numerous high profile cases of baby boomers saying offensive and patronising things to Millennials about why they can't afford houses (too many flat whites, too much smashed avocados, too much whinging etc).

And in addition, there are just the cold hard facts. Various factors converged to make "boomers" the lucky generation. When you reached adult hood, there was an unprecedented era of global economic growth, there was ample fossil fuels, and as yet, no knowledge of environmental damage of that, there was the very demographic fact that your generation dwarfed the "silent generation" that preceded you, and that the generation that came after you, were also a smaller generation. During your generation, there was also huge innovation in farming and food production techniques, so food got much cheaper, house building innovation, meant houses could be built more rapidly and cheaply too (house building costs have actually increased since then) etc etc. You didn't have to pay for uni, you could buy a house on ONE SALARY, such at thing as a "job for life" still existed and pensions offered were very generous compared to what is available now.

And dollar to dollar, you are much much richer than the poor ol' Millennials (as a generation) . Who will probably reach retirement to find they are still paying off mortgage debt, having only just paid off uni, (sadly no wage inflation in the foreseeable), they probably won't have a state pension to look forward to, and no doubt public healthcare will be dead in the water too, so they'll be paying threw the nose (think American healthcare costs) for their hip replacements.

I got very annoyed to see Boomers attacking Millennials from their positions of power in business and finance and so I don't blame them for slinging a bit of mud back.

On ya Boatman! The talk about the greedy Boomers is bullshit talk from people who don't know and don't care to know about the true causes of the price rises. Global money creation had nothing to do with the situation..yea right! We were told that superannuation would not be there when we retired, so we bought rentals! The recent generations will get the benefit of Boomers conscientious effort to build wealth for their retirement. Take note! Learn and do the same!!

No long term rental investor will "head for the hills". Get some understanding of positive cash flow properties please!

Gingerninja, I agree about the mud slinging....I dont know where you are at with your own properties, but if you dont have any, start to think about doing the same thing...buy rentals in say New Plymouth or Nelson, (where there is not enough rental accommodation) for example, and rent out using a property manager so that the rent pays for the mortgage and other outgoings. These properties are out there. Then at the appropriate time after inflation has increased equity, sell or borrow further to buy something in Auckland. Use the economy or the economy will use you. You may not want to do this, it might not be your bag, but dont sling off at people who are providing rental accommodation and building their wealth at the same time. Yes you have to do a bit of renovation but its all worth it.

PKchew I don't have a problem with Property Investors per se. NZ government has given preferential tax treatment to property, of course people who can, will take advantage of that. That's human nature.

I have a problem with Baby Boomers bashing younger generations, suggesting they somehow Boomers worked harder and were more frugal (the data shows this isn't true), that they earned or deserve their "luck". Come on. Imagine being a millennial, starting out in life with uni debt, not earning enough to save for a deposit (because house price inflation outpaced wage inflation by a staggering amount) until you are in your 30's, and then having to take on a whopping mortgage over 30 years!! Do the maths! Think of the retirement issues this generation will face! I am a Gen X, so I am in between the mighty generational battle here but I do think that it was the Boomers who started the mud slinging, when frankly, Millennials have an economic shit sandwich to eat and that isn't their fault or choice.

There are huge cultural differences that have faced each generation of the last few centuries because of the rapid technological advances each generation has brought to bear. And obviously, the major difference between Boomers and Millennials is actual access to data and mass communication. Millennials have had access to the internet since childhood. I think there are fairly profound differences in values and behaviours between these two generations because of that, so I think some tension between those two groups was perhaps always going to be somewhat inevitable. But I just think it would be nicer in general, if Boomers accepted that mostly they had it a lot better financially than Millennials and perhaps, felt like addressing this crisis would be a benefit to society as a whole. Some Boomers care about the plight of future generations sure, but I hear about a lot who don't.

I'm in Melbourne right now and $1.2m gets you a 2 bed flat joined to the one next door in Richmond it makes Auckland look cheap.

Depends on where you live. A 2-beddy duplex with a single carport is already selling for over $1.5M in postcode 1071. That's way more than Richmond in Melb.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.