By David Hargreaves

Ailing construction giant Fletcher Building has made provision for yet more losses in its accident prone Building and Interiors Division - this time of nearly half a billion dollars - and has confirmed that much criticised chairman Ralph Norris will step down this year. The company will not pay a dividend in the current half year.

The share price fell heavily on Wednesday.

Additionally, Fletcher says that while it has reached agreement with its bankers over a lending covenant breach because of the latest losses - it's still in discussions with a number of private lenders (collectively owed over $1 billion) and isn't expecting to have that resolved till the end of next month.

The losses in the B&I Division, on top of earlier forecast losses, will bring the total deficit from the embattled division to $660 million for the 2018 financial year. On top of the $292 million lost by this division in 2017, it means that across the two years the division will have lost nearly $1 billion.

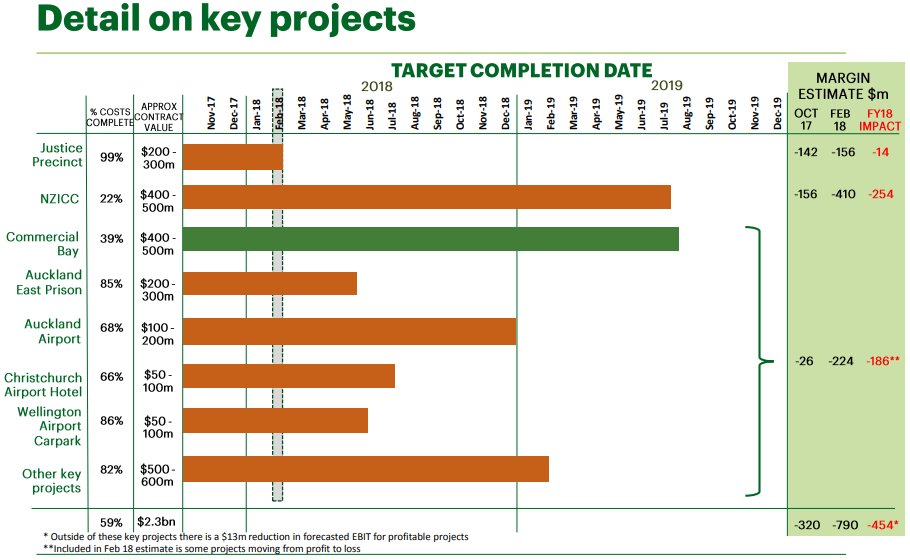

The losses are around several large projects - some of them for the Government. Notable in the latest update is that the company has now more than doubled the expected losses on the SkyCity International Convention Centre project in Auckland.

The total cost of this project is given as $887 million, with an expected loss now of an eye-watering $410 million.

The Fletcher Building shares had been in a trading halt since last Thursday (8th), having last changed hands at $7.77. In early trading after coming out of the halt on Wednesday, the share price tumbled by over $1 to $6.70 before recovering somewhat in very active trading to above $6.90.

The statement released from Fletcher on Wednesday makes no mention of a capital raising for the company - though this would presumably be one option, if shareholders can be convinced it's a good idea. Selling assets may be another - but there was no mention of that either as yet.

In terms of the ongoing discussions with lenders, Fletcher said it had agreed to negotiate changes to its agreements with lenders by March 31.

"If we do not agree new terms by 31 March, we would then be in breach of the terms of our waiver. This would be an event of default with our commercial banking syndicate. However, the banks have moved quickly to grant us the waiver and we expect discussions to continue to be constructive."

'I'm taking accountability'

At a media conference in Auckland on Wednesday, Sir Ralph (Norris) was asked to explain what had caused this situation and who was to blame.

“The fact of the matter is, I’m taking accountability as chair of Fletcher Building. The situation here is a complex one and it is not a situation where there is a single point of failure. There are a number of issues that have conspired to lead us into this situation.

“I think one of the significant issues is that the information flows through to the board were not as fulsome as they possibly could have been.

“I think it is also fair to say that the changing environment around contracting, particularly in the B&I business in the way that risk was transferred from clients to B&I was obviously a significant factor in this.

'A boom is worse than a bust'

“We’ve also had a situation that we’ve had a significant building boom. And often a boom is worse than a bust in many respects because it does put a lot of stress on supply of services, sub-trades, product and the like and as we know cost increases come when demand exceeds supply.

“I think that in calculating these contracts there was a significant underestimation of what the flow-on effect would be in regard to the demands on sub-trades in particular.

“So, we’ve seen significant differences between professional QS firms, calculations of what it would cost to complete these projects, based on their estimation of the cost of sub-trades – and some of those numbers have moved by more than 100%.

“And so that has obviously led to a situation where the cost to complete these projects has been significantly greater than we would have anticipated.”

Sir Ralph indicated that Fletcher would "pursue all of our rights" in respect to the convention centre project to minimise losses. SkyCity has already indicated it expects legal action from Fletcher.

Standing down

Asked about when he decided to stand down as chairman, Sir Ralph said:

“I had been thinking this for a little bit of time. I had decided before Christmas that I would step down in 2019.

“I think given what has transpired over the last week I came to a conclusion over the weekend that I should step down. I think it is only fair for the shareholders to have somebody prepared to take accountability.

“I have to say that I have the full support of my board and management who are of a different view as to whether I should stand down or not and I’ve really appreciated the support from them. But in the final analysis, given the context of where we are today, I think that it is appropriate, regardless of what I think, from the point of view of how I have handled the situation, that from the shareholders’ perspective, the board does need to be seen as accountable.”

Management is 'better now'

He then went on to say he thought Fletcher now had a very good management team in place.

“The strength of the management team that is in place now is significantly better than what it was – so that gives me great confidence – I am also of the view that it is the right thing to get out of the B&I business given the very low margins and the degree of risk that is involved in that and have been very much of the view that that’s what we should be doing."

This was the statement the company released through the NZX on Wednesday:

Fletcher Building announces further losses in Building + Interiors while maintaining earnings guidance for the remaining Fletcher Building Group

-Fletcher Building announces further provisions for expected losses in its Buildings + Interiors business of $486 million, leading to a total projected B+I EBIT loss of $660 million in FY18

-Expected FY18 EBIT for the Fletcher Building Group excluding B+I remains $680 million to $720 million

-B+I business refocused solely on delivery of remaining projects – bidding for all vertical construction in New Zealand to cease

-Waiver received from commercial banking syndicate following breach of covenants

-No interim dividend payment for HY18

-Fletcher Building Chairman announces he will step down no later than the 2018 Annual Shareholders MeetingAuckland, February 14 2018: Following a review of projects in the Building + Interiors (B+I) business of the Construction Division, Fletcher Building today announced a further provision of $486 million for project losses.

Combined with provisions previously announced in October, as well as overheads and other costs, this leads to a projected $660 million EBIT loss for B+I in FY18.

Earnings guidance for the Fletcher Building group excluding B+I remains $680 million to $720 million as announced in October.

Fletcher Building CEO Ross Taylor said the new provisioning was informed by a review of 16 B+I projects, accounting for approximately 90% of the construction backlog, and incorporating external input from independent construction experts and KPMG.

“The provisions we have announced today are informed by a considerable amount of further project analysis, and while we continue to target agreed completion dates across the portfolio, we have factored in significant cost and timeline contingencies.

“Our absolute focus is finishing our remaining B+I projects within these provisions and to a high quality for our customers. To achieve this, we are refocussing the entire B+I business on project delivery only, and ceasing all bidding on vertical construction projects in New Zealand. This will allow us to direct all resources in B+I to the completion of the current book.

“While our broader construction businesses continue to benefit from favourable market conditions and strong growth, the B+I market sector remains characterised by high contract risk and low margins. Unless these dynamics change we will no longer work in this sector.”

The projected B+I EBIT loss has resulted in a breach of Fletcher Building’s financial covenants given to its commercial banking syndicate and US Private Placement (USPP) noteholders. However, the strength of the broader business and the phasing of the cash impact of the B+I provisions means the Company remains well capitalised and solvent.

“We have strong and predictable cash flows across the Fletcher Building group. While the B+I provisions are large, they are phased over a number of years and do not impact our ability to trade with our customers or suppliers or pay our bills.”

In line with the Company’s Dividend Policy the Board has determined that it will not be declaring an HY18 dividend.

“Our discussions with the banks have been constructive. We have received a waiver from our commercial banking syndicate for the breach of covenants and they have confirmed the availability of continued funding while we renegotiate terms. We have also commenced discussions with our USPP noteholders to obtain a similar waiver for the covenant breach. We are targeting to successfully complete renegotiations with all lenders by the end of March.”

Commenting on the reasons for the additional provisions, Taylor said there are many nuances by project, but three core drivers. “Following further project reviews we have taken a more pragmatic view on program delivery and resulting cost contingencies. While we will pursue our contract entitlements vigorously, we have also taken a less optimistic view on client claims and variations. And lastly, since October we have seen further material price escalation across trade finishing costs, which have now been incorporated into cost forecasts.”

In a separate statement made today Fletcher Building Chairman Sir Ralph Norris confirmed he will step down as Chairman no later than the 2018 Annual Shareholders Meeting, allowing an orderly transition to a new Chairman and the completion of the Board refresh process already commenced.

The company also provided, as additional background, this question and answer paper:

Q. Which 16 projects were reviewed?

A. The Justice and Emergency Services Precinct and the New Zealand International Convention Centre (NZICC) projects continue to be the main contributors to the losses. In addition to these two projects the Company reviewed Commercial Bay, Auckland East Prison, Auckland Airport, Christchurch Airport Hotel, Wellington Airport Carpark, and a remaining group of smaller projects.Q. Which projects did KPMG review?

A. In the latest review KPMG focused solely on B+I projects, including the two previously reviewed – NZICC and Commercial Bay – as well as the Christchurch Airport Hotel, Auckland East Prison and Auckland Airport projects.Q. Does this mean Commercial Bay is now loss making?

A. We continue to target a profitable completion of this project, however given it has a long way to go we have provisioned for contingencies.Q. Are the timelines for NZICC or Commercial Bay impacted by this announcement?

A. We continue to target the completion dates we have agreed with our customers, but we have provisioned for significant cost and timeline contingencies.Q. When will the Justice Precinct complete?

A. The project is 99% complete and the client is occupying the building. We expect practical completion to be awarded at the end of February.Q. Does the end of bidding on vertical construction projects mean the Fletcher Construction Company will close?

A. No. The Fletcher Construction Company includes four businesses – B+I, Infrastructure, Higgins and South Pacific. The only business impacted by this announcement is B+I.Q. Will Fletcher Building ever consider bidding on a vertical construction project in the future?

A. We have made the decision to refocus B+I solely on project completion, to ensure our resources are completely focused on this task. While the B+I market sector remains characterised by high contract risk and low margins we will no longer participate. If these market dynamics change in the future we would reconsider our position.Q. Does this change impact residential construction or infrastructure?

A. No. Our Residential Division will continue to operate as it does today. Likewise, our Infrastructure business will continue to complete existing projects and bid for new ones. The infrastructure sector benefits from more appropriate margins, better contract conditions, and alliance models that reduce risk. As our B+I projects complete we will redeploy key talent to these growth opportunities.Q. How is Fletcher Building’s debt structured?

A. Funding facilities are: capital notes ($622m), US Private Placement ($1.13b) a commercial banking syndicate ($1.27b) and other loans ($103m).Q. Which of these debt structures has FB breached covenants on?

A. USPP and the commercial banking syndicate.Q. Which specific metrics have been breached?

A. Senior Net Debt to EBITDA, EBIT to Senior Interest, EBIT to Total Interest and Guaranteeing Group EBITDA.Q. What happens if you do not agree new terms with your lenders by March 31 2018?

A. In consideration of the waiver, we have agreed to negotiate changes to our agreements with our lenders by 31 March. If we do not agree new terms by 31 March, we would then be in breach of the terms of our waiver. This would be an event of default with our commercial banking syndicate. However, the banks have moved quickly to grant us the waiver and we expect discussions to continue to be constructive.Q. Which banks are included in the commercial banking syndicate?

A. ANZ Bank New Zealand Limited, The Bank of Tokyo-Mitsubishi UFJ Ltd, Bank of New Zealand, Commonwealth Bank of Australia, Citibank N.A., The Hong Kong and Shanghai Banking Corporation Limited, Westpac New Zealand Limited, Bank of China and China Construction Bank.

Late on Wednesday, after the NZX market had closed for the day, Fletcher put out a further series of questions and answers, as follows:

Q. Will a final dividend be paid in respect of FY18?

A. No decision has been made by the Company in relation to payment of a final dividend in respect of FY18.Q. What is the position in relation to your capital notes?

No covenant breach has occurred in relation to the capital notes. Fletcher Building Industries Limited (FBI) is currently undertaking a rollover of its FBI110 Series. FBI will allow those FBI110 noteholders who have already made an election, and wish to change that election, to provide a new notice to the Company prior to the end of the election period. An announcement to this effect has been made by FBI earlier today.Q. What are the next steps in relation to the US Private Placement (USPP) noteholders?

A. We have commenced a review process with our USPP holders to obtain a waiver from the covenant breaches (similar to the waiver that we have obtained from our commercial banking syndicate) and to negotiate the on-going terms of our lending agreements with them. Any negotiated position would need the support of a 50% majority of the noteholders in each series of notes.Q. What rights do the USPP noteholders have prior to granting the waiver?

A. As was the case with our commercial banking syndicate, the breach of the financial covenants under the lending agreements with the USPP noteholders is an event of default giving rise to certain rights for those noteholders. These rights include the right for a 60% majority of the noteholders in each series of notes to demand repayment. No demand for repayment has been made by any USPP noteholder.Q. What do you expect to occur in relation to the USPP notes?

A. Based on initial discussions with noteholders and our US legal and financial advisers, the Company believes it should be able to successfully conclude discussions with the noteholders by the end of March.Q. What access do you have to your current funding facilities with the commercial banking syndicate?

A. We have agreed a level of available funding from our commercial banking syndicate which, together with our available cash, the Company believes should be sufficient during the upcoming negotiation period with our syndicate.Q. Is Acciona currently conducting due diligence on the Construction Division?

A. No. As recently reported, an Acciona spokeperson has said “We are not currently looking for acquisitions in the New Zealand market, instead preferring organic growth. We already have a strong working relationship with Fletcher, but any potential collaboration between our companies on future opportunities remains confidential for commercial reasons.”

76 Comments

"......bidding for all vertical construction in New Zealand to cease....."

This indicates how bad it really is. This is their core business.

Just saw how much weighting my recently purchased dumbshares portfolio has on Fletcher Building. This is going to suck as much as last week.

Smartshares' NZ Top 50 has a 5% cap on any single holding, so it could have been worse.

It says that fund is holding 5.52%.

I've got some top 10 as well... 10.66%

I understand. Anyhow, let's see what happens when the market opens in 20 minutes.

Best to hold an index with a larger number of shares. TNZ hasn't been performing well due to FBU having problems for some time.

I'm waiting for the first trades to go up on the board.

.. best to avoid indexes like the plague ... it's counterintuitive that when a company's share price booms , and it's market cap rises ... it's weighting in the index is increased ... at the time it's getting expensive , stretched on fundamentals ...

But , when it falls ... a glitch 'like Fletchers are currently going through ... the index sells the stock a the very best time for a value investor to be buying it ...

.. it's what Warren the Wonderful would do ... buy when there's blood flowing in the streets ... or in the Fletcher boardroom ...

Just saw how much weighting my recently purchased dumbshares portfolio has on Fletcher Building. This is going to suck as much as last week.

Dumbshares (FNZ) actually up 0.8% at the moment. The volatility in the NZX50 has been relatively sober since the start of the year. Part of the reason for that would be that the index's composition. Compare it to Australia, where the ASX is dominated by about 10 stocks (banking, mining, and retail) that set the tone for the whole market in general.

Either so incompetent they couldn't organize a piss up in a brewery or there is fraud going on. And Labour want to use these clowns to build thousands of houses.

Well they aren't going to be taking on any new projects. They've been under pricing their contracts for a long time. However the damage done has been concealed. You don't just have $500m fall out of your wallet.

One of the problems you get with contractors underpricing their work is that they drag the whole market down. The excuse that they used is that they wouldn't win the work. Prioritising winning the work at a loss has ended many construction companies. In the end if you don't make a profit or at least break even you aren't going to continue to exist.

Under Pricing or their cost structures are too high........unsustainable in the market

they are claiming increasing cost of external trade finishers, so contractors they are hiring in to do the work. Big building use a lot of external tradesmen from plumbers, electricians, to jib stoppers etc.

with the housing boom, either building new or renovating old, there is a limited supply of skilled labour so the cost of the labour has increased significantly.

the problem therefore is when they costed the job they under estimated the cost of sub contracting the finishing and didn't mitigate the risk.

Moving out from direct employing to using sub-contractors and subbies get tired of getting screwed (paid late and maybe only a %) so move on quickly. Fletchers look like they are getting what they deserve.

The concern here is if we also look at how ChCh building costs exploded after the EQ then there is a risk many NZ houses are under-insured in major events and that risk / cost is passed onto the un-knowing householder.

:/

"One of the problems you get with contractors underpricing their work is that they drag the whole market down. The excuse that they used is that they wouldn't win the work. Prioritising winning the work at a loss has ended many construction companies. In the end if you don't make a profit or at least break even you aren't going to continue to exist."

Very true. Stonewood Homes fell into the same trap - hugely underestimating future price rises of labour and materials.

We get it in our industry from time to time, under pricing to win the work banking on variations to build up their margins. The problem is, you get the odd project where there aren't many variations normally when the Engineer has done a half decent job at the tender stage.

Great points. But it all seems to lead down one route...

How is everyone undercutting everyone else, yet we are still one of the most expensive places to build?

We have:

- High cost of land

- High cost of Red tape

- High cost of materials

- High cost of labour

Time for the sham that is the NZ Construction industry to get a good beating.

Well, it couldn't possibly have anything to do with productivity deteriorating for many years, could it...?

Has productivity really deteriorated though? How is it measured?

Look at the difference in what goes into building a house now compared to 30 - 40 years ago. You still have a builder and his apprentice building the majority of the entire construct and specialised tradesmen applying finishing touches. Assume these workers are doing their best and are at maximum output per hour per day. Only now you have houses twice the size and with more components.

Is a 200sqm house taking twice as long as a 100sqm house to build or the same time, if the latter, hasn't productivity increased?

If a medium density apartment building is constructed in the same time as a stand alone dwelling, hasn't productivity increased?

The productivity argument doesn't wash. If employees are already performing maximum output per hour how do you get more?

nope I dont think so.

For large projects the land and red tape is deal with by the project team, not the construction company. So their expenses are materials and labour. They also have design and build contractors but they should be able to have a fixed price with them excluding variations (still materials and labour in the end).

They bid for the work even though they knew it was high risk and likely to lose money. The justification being that they do it because they wouldn't win the work otherwise. In a corporate environment when a job goes into a loss the pressure goes on to finish the job and cut costs. People start cutting corners when that happens.

All of this runs the construction sector into the ground. I'm interested to see how bidding for work changes now that Fletchers has exited the market.

I'd be curious how much of this rests upon increased regulatory burdens. IIRC cost of house building ($/m²) in Auckland is up 30-40% in Auckland in last 4 years, mostly extra regulations, and given long lead times for bigger buildings the high inflation in that short time could have swung a lot of tendered projects deep into red.

Yep the regulation is shocking. You want to see the paperwork required just to build a single story residential house. Paperwork will never ensure quality buildings.

The red tape involved makes larger projects more viable as building anything small is mostly made up of costs from the paperwork. Of course the paperwork will never give a good result when someone in the process will fail. A designer could fail to design correctly, the Council could fail to pick up the design problems, the contractor might be too lazy to read to the drawings, the building inspector could fail to identify construction issues.

Lots of paperwork created by MBIE that is ineffective at anything other than increasing the cost of construction. Nine years of National's corruption has done a lot of damage.

Commercial projects? even then I would assume that would be a risk on the client. Also if regs went up they would not usually apply to an already signed off (consented) projects. So sure the next project might well cost more but there shouldn't be much effect in this case, even then the QS people should get a handle on these impacts and cost them in.

Finally, even if some can be laid here such a burden ie increased safety etc is desired.

Almost makes Fonterras loses look competent. Two of our biggest companies making a mess, that's not good.

As with MikeM that cease bidding line caught my eye, what's that going to mean for the industry.

We have had this before. Waitaki International for instance & throw in BNZ & Air NZ while you are at it.. Left hand right hand, no brain in the middle. Too many divisions, and divisions in the divisions. Competitive empire building between the senior executive whose only care is self interest and self reward. Too big, no effective management. Top heavy. All the priority on penthouse luxury while the boilers wear out in the basement. How much money has our good government and agencies wasted in investing in this disgraceful incompetent outfit full of schoolyard bullies. For heavens sake the monopoly & cronyism goes back to Muldoon & Trotter.

What it means is the way now clear for more foreign builders and their foreign workers to control the space?

Imagine you are working on one of the vertical projects - your career with Fletchers is over. So you start looking for new opportunities (who wants to be last on deck on a sinking ship). The projects then suffer more as key staff leave, I suspect a bumpier road ahead.

Can using Fonterra (among others) OOOOPS Fletchers of course for a major house building program be set up in such a way that there is a win win situation for the company and New Zealand. By the way it is losses not loses.

Thanks. Corrected.

Fonterra? Them as wot process Milk? Building Hooses? I realise my old brain does not compute well of a morning, but still....

Salutary lessons to be gained by our key infrastructure providers both current and to come. Watch this space - the issues are more systemic than realised.

Two thoughts some to mind ............ Hubris ( google it ) and " not too big to fail"

If the banks are unwilling to rescue the Company we should let it go .

It will be a wake-up call to the cozy cartel who have taken direction from cartel leader for decades .

We have for too long just accepted the Fletcher dominance of our construction market .

And they thought they were smart going overseas buying up operations in the US which is a way tougher market than lazy slowed -up old New Zealand where we just pay and get screwed......... and never complain.

agree, let the banks take it.....record profits? well carry the risks and costs of that as well.

With that $2.3 billion portfolio of work and cost of materials rising at 15% per year they may still lose an additional $230m to $345m across that selection of jobs

As i understand it the lost is a provision against potential losses not actual losses of 660m therefore cashflow impact is lower and they may be able to claw back some of the provision as the projects are completed.

Shows extremely poor risk management from all of their management.

lucky B&I was not one of their large divisions

Very high turnover of FBU shares at 2.558m traded so far and the price is around 6.75. The price is down 13% since the trading halt.

This raises the question of executive pay to me.

Those at the top, reap all of the reward when things go OK, but none of the pain when it falls to pieces.

Lol. Totally understandable. Basically a rounding error.

My understanding of how Fletchers works is that it is structured as a vertically integrated company that is arranged in concentric circles or layers. In the core there are the basic resources and primary material production assets. From there the products move through succeeding layers; - the processing, distribution and marketing. The most competitive parts are on the outside of the structure and the competition naturally limits profits at this point. Internal pricing to these vulnerable divisions is firm otherwise they have a tendency to give away the profits in an effort to win business. Margins and profits are concentrated towards the center of the company where they will not be easily yielded. In some ways the company does not worry if Fletcher Buildings wins the contract to build something or Placemakers sell the pink batts compared to Mitre 10. The important thing is that they have a very powerful monopolistic and duopolistic hold over the supply of materials, and there is where their profits are meant to be concentrated.

My observations of the poor contracting companies or divisions that are meant to survive on the outside of this sort of set up is that they have little hope of making a profit and get little support to do so. They are just there to keep that market sector competitive so that the profits can be concentrated further inside the company. Not surprising this is pretty disheartening for the staff in these divisions which further undermines their performance and efficiency. Given the high demand for building contracting staff I would imagine that they must be having a lot of trouble hanging on to good staff. Why remain in a job where you are not supported and are basically set up to fail or at best break even.

If I am correct in my opinions and this is at the core of their problems, it serves them right. They thoroughly deserve their troubles.

If the outer skin of the vertical has failed compete I would expect the same to be the outcome for horizontal, ie kiwibuild.

Withdrawing from vertical has left a big hole in the armour designed to reduce competition.

It will be interesting.

The strategy of draining any possibility of a construction profit from the market would make sense if you wanted to squeeze the competition out of the market. However it appears that strategy (if that is what they intended) was more effective against Fletchers than their competition.

Perhaps an Australian company now enters vertical using Australian materials suppliers and independent NZ companies where possible. With a toehold it then eyes up kiwibuild.

The administration can help by offering tenders for large numbers of houses, by Australian standards.

Wait and see.

The market is quite saturated at the moment. Would an Australian company unfamiliar with the environment here take the risk for such a small market?

You also need to consider they have a different construction culture that, from my experience, involves a lot of backstabbing. The risk is more short cuts and leaky buildings or leaky building-like problems.

If they could see a quick buck they may, examples would include the saga of our rail network.

Would that explain why an Australian company is the lead developer at the Hobsonville Point project?

Interesting, in truth Im just taking wild guesses.

Do you think they are doing a good job?

11.2 percent fbu loss as of now damnit. Anyone holding this company should sell right now to stem any further losses and reinvest in commercial or residential property. Properties are a much safer bet and always have been.

Question is, at what price do they become an attractive buy? Are they going to cut dividends to help reduce their hurt? Is their P/E ratio correct at 50 something?

No FY18 dividend was part of the announcement. Too many questions at the moment for me to consider them an attractive buy at anywhere near the current SP. Norris going is a start (his comments at the AGM now seem utterly laughable) but there's still a lot of useless dead wood that needs to go.

This outcome raises questions of the worth of the 2017 audit opinion and its review on behalf of stakeholders of the accounting processes being used to measure the preformance and reporting of contracts in B & I.

Are they still solvent ?

They had to cut a deal with their creditors to remain solvent as they were unable to meet the requirements of their debt commitments. So yes they are still solvent but when you have a net loss in the hundreds of millions cash flow problems will keep cropping up.

Which could mean FB sub-contractors should expect delayed payments.

Excellent question! Powers that be will look the other way. Conditioned to it.

Here in our practice I am starting to hear the older blokes saying ................ TOO BIG TO FAIL .

Shareholders no doubt .

More like too big for their boots.

Fletchers have suffered from HUBRIS and now they must take the consequences .

This is utter bollocks where profits as privatised and losses carried by the taxpayer .

This group has made a fortune out of us over the past century, they are leaders in the buildiing industry pricing cartel , they get tarriff protection for GIB so we overpay for it ........... which is a disgrace.

The price of building materials in Placemakers is also a disgrace .

And they should be allowed to fail without taxpayer help so we dont ever have such a massive dominant player rigging the market as they have done ., and instead we have smaller leaner operations competing on a more level playing field .

And for those of you who suggest that it will lead to job losses ....... thats nonsense too , we are in the middle of a building and civil construction boom , and everyone will find work in that sector

We are a generous nation, A billion to Air New Zealand another one to the BNZ ( im exaggerating)

More modern times SCF

The question is whether they are worth it.

More are coming, AIrNZ will have a round 2 as peak oil kills its business model. The Q is how long do we keep (or can afford) bailing the dodos out.

Funny thing but it seems "no one" wants to bail out dole bludgers, but enough want to bailing out the in-competent especially the "saved".

regards

In case you missed it we already are and have been for years. However I take note of your parenthetical connotation.

.

And there’s the rub. Bail them out and what is quite evident is that the consequence of moral hazard does not abate. Not that its peculiar only to big business either. Simple human nature.

You would be hard pressed to find anyone at Air NZ, and I mean anyone, that would acknowledge that their jobs were saved by a tax payer bailout! Man the arrogance is unbelievable.

how the heck can you take on a project "............as $887 million, with an expected loss now of an eye-watering $410 million. " and be that far out on its actual cost? a 50% error is just mind boggling.

New Zealand is a tight little community.

They try to keep it all in the Family.

Dealing with a stacked deck, a crappy sink, a bit of timber...way, way over priced, compared to a World Market.

Can send a log to China for instance, bring it back in pieces, nailed it.

Has been for many a year.

Or import any other rubbish they like. Put on a big mark-up...discount to the traddie.

NZ has been doing it for years.

Ring fenced. Way over budget..

Get a life...Google it...compare retail here and wholesale there..no comparison.

My estimates are Strife Torn is coming back to bite em....hard.

Never, never try to under estimate an Asian....Wiley.....not stupid.

As several have already said, we know what the problems are, and as I’ve already said, its systemic. Norris was in an untenable position and duly departs. Agreed it was manifest incompetence at numerous levels and multiple failings. Brushing aside any suggestions of fraud. All I can say is keep on sweeping, some of us know better.

Is Fletcher an attractive take over target for an overseas investor, may be from China or Aussie ?

Ask their private bankers that. Theyll get back to you

Could they force a sale to a White Knight from overseas ?

Of course it is, and so is the possible demise of Fonterra

Another symptom of what is to come.

Thinking outside the box for a second. Why not nationalise into a state owned not for profit and use it solely for Kiwibuild?

Because there are people out there who think everything should be privatised because that makes things more efficient etc. Supposedly Governments shouldn’t get involved in areas/industries where people can make a shit tonne of money for little effort.

because it is clearly run by in-incompetents. Plus privatising it bails out the banks, investors and shareholders for no public good I can see. Better to let the "free market" rule this one IMHO.

Even in the heyday of state housing we didn't do that.

A mix of private and public construction was used, plus overseas prefabs and emigrant labour.

Best not.

Looks like we’ve found the red hiding under the bed. Just how many glasses of cab sav have you had?

What are the likely losses on the overpriced and unsaleable Fletcher residential developments in Christchurch and Auckland??

How many developments are nearing completion or completed and unsold?? With each unit averaging $800k plus and potentially $200k overpriced what are the real losses??? Is there another cool quarter billion (or half) to add to the red ink soon??

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.