Treasury is forecasting government financial support will have less and less impact on economic demand over coming years, meaning fiscal policy should support Reserve Bank monetary policy efforts to rein in inflation.

In the Government's Half-Year Economic and Fiscal Update (HYEFU) out Wednesday, The Treasury says the strategy of returning the Operating Balance Before Gains and Losses (OBEGAL) to surplus, from deficit, by 2024/25 and to retain current settings for allowances for new operating spending, should see a net reduction in public demand, helping cool inflation and reducing the need for the Reserve Bank to continue raising interest rates.

Fiscal policy is the use of government spending and taxation to influence the economy.

"Focusing on public consumption spending, the Treasury’s forecasts are conditioned on the profile for spending on core government services detailed in the fiscal forecasts. Over the period ahead, inflation and public sector wage increases are expected to raise the cost of purchasing goods and services and to reduce the volume of services that can be provided," the Treasury says.

"This results in a decline in real public consumption spending of 8.2% over the period to the December 2024 quarter. This would be the largest fall since at least 1987 when current reporting standards were adopted. For comparison, the decline that occurred between the start of 1990 and the September quarter of 1991 was 7.8%."

"The current episode follows a period of strong growth leading into and during the COVID-19 period. Between the start of 2020 and mid-2022 real government consumption increased by 21%, meaning that after this decline real government consumption remains above pre-COVID-19 levels. As a share of GDP, public consumption declines by around 3.4 percentage points and returns to its pre-pandemic share of 18.5% of GDP at the end of the forecast period [2027]," the Treasury says.

"The fall in real government consumption plays a key role in unwinding excess demand in the economy, which reduces pressure on the private sector to contract further."

It goes on to say that the drop in public consumption accounts for nearly half the total decline in domestic demand in 2023/24, and that it continues to "subtract from demand" in 2024/25.

"Real government consumption grows modestly thereafter as the pace of input price growth slows."

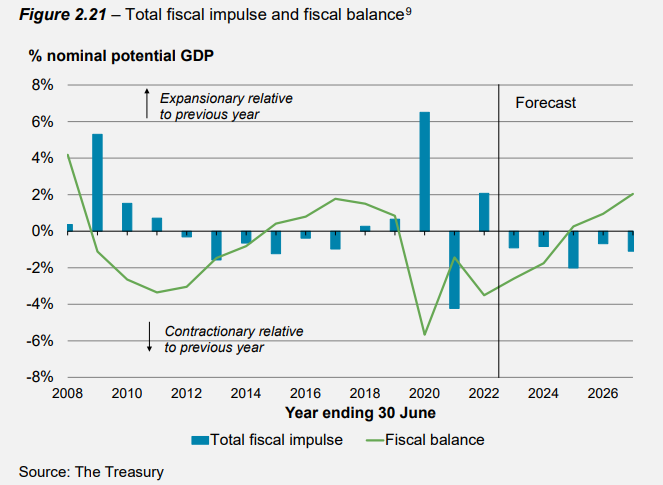

The Treasury refers to what it describes as the total fiscal impulse. This measures the change in the Government’s fiscal support for aggregate demand from one year relative to the next.

"A positive total fiscal impulse implies that the level of fiscal support is expanding compared to the previous year, while a negative total fiscal impulse implies it is contracting compared to the previous year. The total fiscal impulse does not estimate the absolute level of support or the economic impact of that support, which will vary depending on factors such as the composition of spending."

"From 2021/22, the fiscal balance is forecast to improve throughout the forecast period, with a surplus expected in 2024/25. As a result of tightening fiscal policy implied by an improving fiscal balance, the fiscal impulse is expected to be negative - contractionary - throughout the forecast period. This shows that the Government’s contribution to aggregate demand in the economy is forecast to reduce relative to each preceding year, indicating that, overall, fiscal policy is expected to support monetary policy’s objective of dampening inflationary pressures," the Treasury says.

"A materially smaller fiscal balance deficit in 2021/22 than previously forecast, relative to the Budget Update, means that the fiscal impulse for this year was markedly less expansionary than previously forecast. As the fiscal impulse measures whether fiscal policy is expansionary or contractionary relative to each preceding year, less expansionary fiscal policy in 2021/22 has likewise resulted in a less contractionary fiscal stance forecast for 2022/23."

Treasury suggests Consumer Price Index (CPI) inflation, 7.2% in the September quarter and 7.3% in the June quarter, is near its peak, but will fall relatively slowly, returning to the Reserve Bank's 1% to 3% target band at the end of 2024.

Timing and composition of fiscal decisions seen as key

Kiwibank's economists note that the Government is sticking with a $4.5 billion operating allowance for Budget 2023, as announced at Budget 2022. Of this $2 billion has already been committed.

"The $4.5 billion boost earmarked for next year is still a serious chunk of change for an economy that remains capacity constrained. In addition, stronger planned capital spending will add to resource demand," the Kiwibank economists say.

They note that the Government’s multi-year capital allowance was increased by $9.1 billion, with much of this increase not yet allocated.

"But given NZ’s infrastructure deficit there is a seemingly endless list of need, from transport to health."

"There is concern a fiscal spending spree would exacerbate inflation and require even more aggressive monetary policy tightening down the road. The planned lift in capital spending doesn’t really take off until the 2024 fiscal year. By which time NZ is expected to be in recession and resources should start to free up," Kiwibank says.

"The Treasury’s fiscal impulse analysis suggests that fiscal policy settings will add less to total demand over the years ahead. Implying less inflationary pressure from government. However, this will depend on the actual timing and composition of fiscal decisions."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.