The Finance and Expenditure Select Committee has reported back on the Taxation (Annual Rates for 2025-2026, Compliance, Simplification and Remedial Matters) Bill. This Bill contained measures in relation to changing the tax treatment of non-resident visitors who are working remotely while visiting New Zealand, introducing the new Revenue Account Method for calculating foreign investment fund income, plus the usual host of other amendments tidying up various issues.

The amendments to the tax treatment of New Zealand visitors are designed to encourage people to work here remotely without triggering too many adverse tax effects. One change proposed relates to disregarding the activities of a non-resident visitor present in New Zealand when determining whether a company is tax resident in New Zealand.

Watties, Heinz, tax and a Lions legend

This is a long-standing point and with Watties being in the news for all the wrong reasons, I recall an interesting point raised way back in the 1990s when Watties was acquired by Heinz, the international food manufacturing giant. Apparently, Tony O'Reilly, the former British Lion and then chairman of Heinz, was in the country at the time the deal was being finalised. Did this mean Heinz had a permanent establishment in New Zealand because key decision makers were here?

Tony O’Reilly in action against the All Blacks in 1959

That was a somewhat mischievous question. But it is an example of where key personnel being in a country may trigger unintended and adverse tax consequences. The Bill tidies up a number of issues relating to this as well as clarifying the treatment of remote working by non-residents.

No major changes to the Revenue Account Method proposal

When the bill was introduced, much fanfare was made of the proposed Foreign Investment Fund (FIF) Revenue Account Method. This allowed an eligible person’s FIFs to be taxed on a realised gains basis with a discount of 30% applied to the gain resulting in an highest effective tax rate of 27.3% (i.e. 70% of 39%).

This was seen as disappointingly high so many submissions on the Bill requested a higher discount to reduce the effective tax rate. These have all been knocked back on the basis that the maximum rate of 27.3% is broadly comparable to the 28% payable under the PIE regime.

But there are some minor mostly technical changes. For example, losses arising under the Revenue Account Method were initially to be ring-fenced and only available against future gains. Any such losses will now be available to offset against dividends from the same interests. So that's a bit of a win.

And there is the ability also to allow taxpayers to sometimes use other method calculations which are required at present rather than and not lose their eligibility to apply the revenue account method to other interests. In other words, you can sort of split treatment on that. So generally, the rules are a progression, but I think you can read when you get into reading the fine printing, you sort of see the technical minutiae and issues that pop up because of the complexity involved.

There was an interesting, there's also a proposal for essentially there's a realisation tax on migration, and a point has now been clarified that If this happens, the calculation of any tax payable, because someone has used the revenue account method and then migrated out of New Zealand, they would use the market value of the interest at the time the person departs New Zealand, not the market value received when the interest is subsequently disposed of.

Quick example, a person leaves New Zealand when the market value of one of these interests is say, $500,000, subsequently sells it and realises the market value of $1,000,000. Any New Zealand tax payable will be based on the 500,000 being the market value at the time they left.

Don’t look the parents are squabbling…

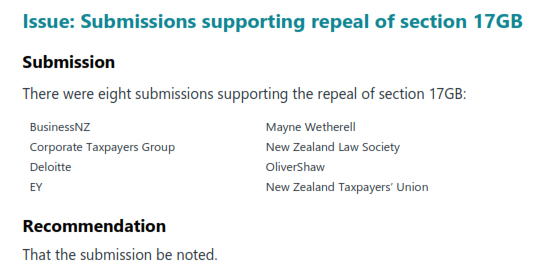

There was a nice little spat between the various parties on the committee over the proposal to repeal the Section 17GB of the Tax Administration Act 1994, which allows the Commissioner to collect information for the purpose relating to the development of policy for the improvement of the tax system. This was the measure introduced under the last Labour government, which was then used as the basis for finding the information for Inland Revenue's controversial 2023 High Wealth Individual Review. Unsurprisingly Labour and the Greens opposed its repeal as did 202 submissions (including for the record Baucher Consulting, and the Chartered Accountants of Australia and New Zealand). Eight submissions supported the repeal.

Information sharing risks?

Labour was also opposed to the provision expanding the ability to allow Inland Revenue to share information about individual taxpayers with other government agencies more easily by way of Ministerial agreement. The Labour Party MPs made this very valid point,

“While Inland Revenue has strict rules about which employees may access information about individual taxpayers and it polices those rules rigorously, the same protocol may not apply in other agencies.”

Indeed, Inland Revenue, to the best of my recollection, has never had issues where someone has emailed out a spreadsheet full of confidential details which we've seen both the Ministry of Social Development and ACC to name a couple of culprits do. The Labour Party also noted “This is a significant change to the rules that protect the privacy of taxpayers' information. We note the Office of the Privacy Commissioner has concerns about these proposals.” Despite this the provision is to go into effect.

Financial arrangements – three welcome surprises

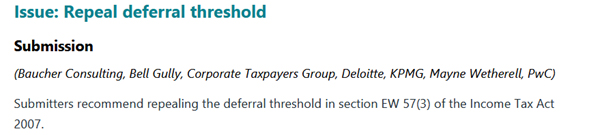

A big and welcome surprise relates to changes to the financial arrangements regime. Under the financial arrangements regime if certain thresholds are exceeded taxpayers must calculate income and expenditure on an accrual, or unrealised, basis rather than on a cash, or receipts, basis. These thresholds had not been increased since 1999, and the bill proposed to double them.

The regime also has a deferral threshold which means income and expenditure must be calculated on an accrual basis (unrealised) if the difference between calculating income on a cash (receipts) basis and the accrual basis exceeded $40,000 at any point. This applied regardless of whether a taxpayer’s total financial arrangements were under the $1 million threshold. Unsurprisingly, this deferral threshold frequently tripped up taxpayers (I even once saw advice from a Big Four firm which had overlooked its impact). I was one of several submissions recommending repeal of this threshold.

Inland Revenue has accepted our submission noting the deferral threshold

“…imposes a high compliance burden, requiring taxpayers to calculate income and expenditure on an accrual basis to compare it with a cash basis result and ensure that the difference is below a threshold. This is the same compliance burden that being a cash basis person is intended to avoid.”

This is an excellent result.

But wait, it gets better

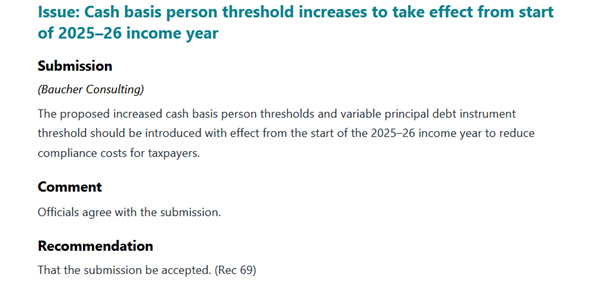

Under the Bill the increased thresholds were due to take effect from the start of the 2026-27 income year (1st April for most people). Adopting the principle of you don't ask, you don't get, I also submitted the threshold changes should be effective as of the start of current tax year (i.e. 1st April 2025). This would reduce compliance costs for the taxpayers, one of the key objectives of the Bill.

To my great surprise and delight, that was accepted as well, which is another excellent result.

But wait, there’s more…

KPMG made a very sensible submission that foreign currency loans used as mortgages over property should be removed from the financial arrangements rules and calculations. Exchange rate fluctuations can mean the deferral threshold is breached making any unrealised foreign exchange gains taxable. This once happened to one of my clients resulting in a tax bill of over $100,000.

Although Inland Revenue did not accept KPMG’s submission in full, it proposed instead “limiting the effect of foreign exchange fluctuations for the absolute value threshold”. This would be achieved by testing the absolute value threshold (now $2 million) is tested using the principal amount converted at a set date, for example, the first day of the financial arrangement, and ignoring subsequent foreign exchange fluctuations. If the principal amount changes for non-foreign exchange rate, reasons i.e. increases or decreases in borrowing, the financial arrangement should be reassessed for the threshold.

A bit late for my client perhaps but still a good result. The three change are also good examples of the Generic Tax Policy Process in action resulting in sensible law changes.

Controversial shareholder loan proposal halted

Moving on, late last year, Inland Revenue dropped what I described as a bombshell, with a consultation proposal for significant changes to the treatment of shareholder loans. Inland Revenue proposed that shareholder loans above a certain threshold would instead be treated as dividends, similar to the treatment for Australian and UK taxation purposes.

These proposals have hit a major roadblock with opposition from Winston Peters and New Zealand First together with the ACT Party. The end result is that the proposals as put forward in December will not be proceeding. Instead, Inland Revenue will continue to review the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The proposals were quite controversial but the same time there was something of a tacit acceptance that yes, perhaps something needed to change. Simultaneously, there were concerns that Inland Revenue was perhaps muddling two issues. One of the issues was that companies that went under often sometimes owed substantial sums by shareholders, and in some cases, this meant Inland Revenue was missing out because funds were paid to shareholders instead.

John Cantin, former guest of the podcast, and also the independent advisor to the Finance and Expenditure Committee on the current tax bill has made public his submission to Inland Revenue on the shareholder loan proposals. His view is that more information is needed on the interaction between outstanding shareholder loans and company failures and the composition of the tax debt of such companies. If it is mostly GST and PAYE? Then yes, maybe that is something to be considered. He also thought there was merit in looking at changing the tax treatment of what happens on liquidation.

The upshot is we'll be going back for round two of consultation. It'll be interesting to see what comes out of this. Like John I think changes around what happens when a company is put into liquidation are sensible and also around keeping records of what we call available capital distribution amounts and available subscribed capital.

Property flippers – what about the tax impact?

And finally, an interesting story from RNZ about a complaint to the Real Estate Authority about a rise in so-called ‘property flippers’ making six-figure returns from unwitting vendors. Property data firm Cotality has noted a rise in significant rise in what's called contemporaneous sales, with the number happening last year was almost double the total for 2024.

In a contemporaneous settlement, a property flipper makes a purchase offer with a long settlement period and then finds another buyer to purchase the property on the same day the property flipper has to settle their purchase. If it all goes to plan the property flipper makes a quick gain.

According to iFindProperty co-founder Maree Tassell who has complained to the Real Estate Authority about the practice:

"It's quite common that there are some deals out there where people are making over $100,000-plus on contemporaneous settlements, getting a property under contract. The poor old vendor, and even often the vendor's agents will think 'oh this is a real purchaser'. …It's quite deceptive to the vendors and quite deceptive sometimes to the agents."

Although tax isn't actually discussed in this story, these transactions would be considered a taxable trading activity even if they are not specifically within the bright-line test rules. It’s the sort of activity Inland Revenue should be watching with great interest. Property flippers should therefore beware, you may be making a quick buck, but Inland Revenue will be tracking these transactions. If you are not declaring the income, then you could find yourself with a big please explain somewhere down the line.

And on that note, that's all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.