With Fonterra announcing big write-downs on its asset values in China, Brazil, Venezuela and New Zealand, is it a fair question to ask what other assets elsewhere in the world might also need to be written down? Have we heard all the bad news?

The two biggest questions relate to Australia and Chile. These are Fonterra’s biggest overseas milk pools, which no longer fit clearly within the new emerging Fonterra strategy.

I recently wrote about concerns for Australia, where Fonterra has announced plans to write down assets by $70 million. In that article I expressed concern that much bigger write-downs might be needed.

Since then, my Australian network confirms that, particularly in Northern Victoria, Fonterra is indeed in big trouble, and heading towards more stranded assets. The problems are growing by the month. In July, Fonterra’s monthly Australian milk supply was 5.4 million kg milksolids (fat plus protein) whereas two years ago it was 8.3 million kg milksolids,

Fonterra is getting out-muscled for the dwindling Victoria supply of milk. It is already paying more than it can afford, and considerably more than its New Zealand farmers are getting. It is a mess.

But here, I want to focus on the Chilean operations of Fonterra. I see elements of an Australian mirror image, with Fonterra getting squeezed by poor market returns for its particular market products and dwindling milk supply from its farmers.

Although the big picture of Fonterra in Chile has great similarity to Australia, the details are different. The fundamental element in common is that Fonterra keeps getting thing wrong when it heads away from home, largely through inadequate understanding of the environment in which it is working.

The starting point for Chile is to recognise that Fonterra’s investments there go back to the NZ Dairy Board days. Fonterra inherited a majority share in Soprole, at that time Chile’s market-leading dairy company.

At the same time, Fonterra picked up a controlling share from the Dairy Board in Soprole’s little sister company Prolesur.

Whereas Soprole focuses mainly on consumer products produced and processed in the central parts of the Chilean dairy heartland, Prolesur is further south again in Los Lagos where it focuses on the commodity side of things, being mainly milk powder, butter, and more recently cheese. These are produced in high rainfall country, much of it around Osorno.

Then in 2009, Fonterra increased its stake to more than 99 percent ownership of Soprole and 86% ownership of Prolesur. And that is where ownership now stands. The purchase price indicates Fonterra’s Chilean assets were valued at around $NZ600 million in 2009.

To a large extent, Soprole and Prolesur operate as one company, with Prolesur’s profits incorporated into Soprole, and from there through to Fonterra. However, that is not the full story.

To start with, Fonterra has strongly encouraged Prolesur suppliers to focus on grass-fed systems and spring-calving as occurs in New Zealand. The Prolesur payment system has been aligned to this policy.

However, the realities of dairying in southern Chile, although having superficial resemblance to New Zealand, are not the same. Hence, Prolesur has now recognised that seasonal milking also has disadvantages, particularly when it comes to product marketing, and hence what it can afford to pay its farmers. Unfortunately, this understanding has been delayed.

It is readily apparent that Prolesur’s farmers are currently not at all happy. In the calendar year ending 31 December 2018, the Prolesur supply dropped 17.7 percent despite overall Chilean dairy production rising 1.9 percent.

It is also clear that many more of Prolesur’s farmers would leave Prolesur, and hence Fonterra, if they could. They would very much like to join Colun which is a Chilean dairy co-operative that has been smashing Soprole in the market place.

Although Colun is now Chile’s leading dairy company, it is capacity-constrained and has a waiting list of farmers. In consequence, southern farmers are having discussions as to whether they might set up their own co-operative.

Also, Prolesur’s minority owners are trying to sue Fonterra for unfair transfer-pricing of products across to Soprole, at prices that damage their economic interests. This legal challenge in itself has potential to be messy.

Prolesur recognised some years back that it needed to invest in cheese production. This has occurred in the north of Prolesur’s production region, with production capacity now at more than 2000 tonnes per month. This has exacerbated the supply problems for their milk powder production at Osorno, where they already have stranded assets.

Fonterra’s problems in Chile go well beyond Prolesur in the south. Big sister Soprole, which incorporates Prolesur within its own accounts, is also in decline.

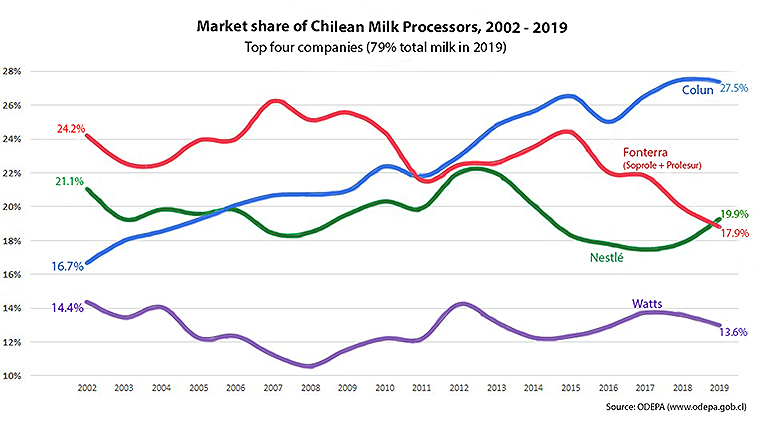

Chilean market-share data goes back to 2002, at which stage the Soprole plus Prolesur combination was number one in terms of national milk supply. As the graph shows, from there through to around 2015, it was a case of large swings and roundabouts, but arguably with no consistent trend in market share. Since then it has been an ongoing decline.

Right through to 2018, it may have seemed to those people who rely on published profit figures that Fonterra was doing OK. There were steady dividends back to New Zealand. For many years it was a great cash cow.

However, if Fonterra’s top managers and directors had been doing some independent foot-slogging they would have known that all was not well. I have seen correspondence going back to 2014 where Chilean farmers were trying to tell both Fonterra and the New Zealand Government that things were not right.

To put it in a nutshell, the Chilean farmers were accusing Fonterra of overmilking the Chilean cash cow. It was all short-term thinking.

Soprole produces accounts for each calendar year, in Spanish, and I have been trawling through those. The latest accounts are for calendar year 2018.

The numbers show that when converted to NZ dollars, the consolidated Soprole operation for calendar 2018 made a profit of around $55 million. The year before it was about $65 million and before that over $70 million. In 2015 it was $80 million.

Soprole currently has a book value, converted to NZD, of around $940 million. Equity is valued at around $700 million. It is hard to argue that the current profits are sufficient to justify these figures. Beyond that, the trajectory is wrong. No-one would buy assets at anywhere near that price.

Soprole brands are no longer considered premium brands in Chile. Some of Fonterra’s Chilean processing assets are less than efficient. Those assets belong to a previous era. And Fonterra lacks a loyal base of suppliers.

Put all of those things together, and look into the future rather than the rear mirror, and Fonterra’s Chilean assets look very shaky. Just like elsewhere in the world, Fonterra has dug a deep hole for itself.

It would have been much easier to not dig the hole in the first place than to now find a way out. The first step forward is for Fonterra to identify the extent of the hole.

*Keith Woodford was Professor of Farm Management and Agribusiness at Lincoln University for 15 years through to 2015. He is now Principal Consultant at AgriFood Systems Ltd. Previous article on Fonterra’s challenges can be found at https://keithwoodford.wordpress.com/category/fonterra. You can contact him directly here.

41 Comments

This will be interesting if they open the books

Fonterra's biggest shareholder Colin Armer says he's taken his long-simmering worries about the company's books to the Financial Markets Authority because he's angry.

He's angry on behalf of the dairy cooperative's 10,000-odd shareholders, who he says have had $4 billion wiped off their balance sheets in recent years.

He's angry with the "inept" Fonterra Shareholders' Council, which should have held the company, its directors and "out of control" management to account.

And he's angry at auditor PwC, which he's told the FMA, has "badly let down" shareholders

I just saw that news. There's more than enough grounds for investigation. Preferably I would like to see PwC prosecuted as they have failed in their duty of care.

It now seems so obvious why the previous management were chasing volume. It was to create the illusion that things were ok, when in fact they weren't. There's near been any margin in chasing volume (with the lack of retentions), which with the negative side effects on the environment have just dig themselves a bigger hole for dairy farmers.

Time heads rolled at PWC, including those who had previous links to them. Clearly PWC has been as useless as tits on a bull, and let their consulting fees compromise their reporting standards; if they have any.

It's not PWC's role to audit strategy. However, having two PWC (ex) partners on the Board is so far removed from governance best practice. This will make a great MBA case study (they don't have happy endings).

I'd take issue with you over the word illusion.

There have been many who have seen it and called their strategy for what it was but generally they have been treated as ignorant cockies as the "business" leaders bleed it dry.

You can't cherry pick only the losses in a diversified portfolio as we all know the reason we diversify is to spread the risk of cyclical loss performers with cyclical gain performers.

It is impossible to win everywhere everytime, which appears to be what the media is unrealistically trying to measure Fonterra with.

The world markets are up in some areas and down in others.

Some balance on the huge wins coming out of other markets would be fair, as would the fact that the Capital Upgrade program is coming to a decade long end, which will be causing a huge IRD non cash depreciation expense to be reducing the reported profit, and which will give a large cash windfall in the balance sheet as the depreciation charge will not need to be spent at the rate it has been in the past.

Many share portfolio's experience ups and downs over a range of businesses, because that's how it works in a global market with competing players over limited resources.

Leonardus,

I think you are confusing tax depreciation rates with the valuation of assets on the balace sheet. This is a common mistake. The balance sheet values are meant to reflect market values, not standard tax depreciated values.

As for those 'huge wins coming out of other markets' you might like to identify what they are. Farmers are currently getting reasonable milk prices based on reasonable commodity prices, but Fonterra itself is strugging mightily to add value above commoodity prices.

KeithW

thanks Keith, but you are confusing Market Value assets with Investments, eg shares or term deposits etc.

I am talking about the new Plant upgrades in NZ, which are Fixed Assets. These are Depreciated each year until written down to a zero book value if not sold prior.

For a long time Fonterra would have been running very old Fixed Assets, Plant mainly, fully depreciated.

This is no longer the case, the renewal program would have replaced old Assets at a huge capital cost and built new plant as well.

So its Historic cost reporting which is at recent upgrade values. Which are then depreciated.

Older assets Cost $ * 10% depn straight line = annual depn expense.

Nothing to do with Market Values, as this applies to Share Assets, Investments, and Livestock stock in trade etc.

We are talking about Fixed Assets.

Thus Depn expense applies for say 10 years until fully written off.

For many years operating, less depn expense would be charged against reported revenue as Book Values were nil for much of the old plant.

DIfferent story today.

New Asset $ * 10% Depn SL = annual depn expense.

Currently going through books now as Plant is all relatively new.

Thus reported current operating profits after depreciation expense will be less today.

The fundamental cash flow will be strong as I said, as Depn is a non cash charge, with the Capital program coming to an end, there will be a benefit in the Balance Sheet bank balance, which can be used to repay debt or payout to farmers.

Provided Milk production and prices remain similar $ same of course.

Leonardus,

I think you are conflating depreciation for tax purposes with the separate process of market valuation of assets as recorded in the balance sheet.

KeithW

No sorry Keith,

I am focusing on Fixed Assets owned by Fonterra which are depreciated.

You are referring to its Investments in shares in other companies which are reported at Market Value.

Fixed Assets are reported at historic Cost and depreciated.

I can;t explain it any easier than this sorry.

Depreciation is causing the operating bottom line to look poor, but as I said in my first blog, underlying cash flow will be strong once the Capital program is complete. Ceterus paribus.

Leonardus

Note 13 of the full financial statememts says, inter alia, "The assets’ residual values and useful lives are reviewed and adjusted, where required, each financial year". Valuing fixed assets is challenging, but it is part of the auditor's role of a public company (or a co-operative company such as Fonterra) to ensure that this occurs. Stranded assets should therefore be valued at their impaired value. Fonterra's fixed assets were valued at 6.81 billion as at 31 July cf 6.39 billion at 31 July 2017. These assets at 31 July 2018 were at approximately 57 percent of historical cost.

Fonterra normally charges depreciation on a straight line basis over assessed economic life, and adjusting for impairment.

For the 2019 year about to be reported, cash flow is likely to look strong owing to low captial expenditure - probably less than depreciation - and from the sale of Tip Top. This will be used to reduce debt. However, the gearing ratio (as defined by Fonterra) will increase, whereas the the equity to total assets ratio will decreas and may end up under 30 percent. Fonterra does not ever announce this equity to assets ratio, but the Wall Street Journal does record and note it, and of course it is easy to calculate. The rating gencies will also have their eye on thse two ratios, which are damaged by the book write-downs. Fonterra has not been explicit so far as to the extent to which the write downs are tangible or intangible assets.

KeithW

If the govt has to bailout Fonterra, oh there will be discontent, especially from those who say dairy became too big in NZ. Too big to fail?

And who will the cockies be blaming? Will it be the incumbents or will it be the loonies that came up with "double primary by 2025" and road roughshod over the environment and democracy with the dirification of Canterbury?

. . the spirit of former Prime Minister Rob Muldoon is alive and well with the Kiwi obsession with " Think Big " projects . . Fonterrible being one such ridiculous concept , the 100 000 houses of Kiwibuild being another ...

We are consistent... we never learn the lessons of history ..

this seems to happen to a lot of NZ companies that operate outside NZ, they don't listen to locals, they don't invest in capital and they wonder why after a period of time the well starts to run out.

I agree its crazy. The arrogance of Fonterra has cost them dearly. it seems Colun has used their home field advantage to full effect. Never under estimate local knowledge

Sobering analysis, Keith. Overconfidence, lotsa funding, and an inability to see which way up the udders were pointing.

. . as I may have mentioned before , the co-operative design of Fonterrible was udderly ridiculous right from the get go nearly 20 years ago . . .

We've dropped Anchor butter where I work , pallets of Kerry butter arrive from Ireland cheaper than the local product !

... grab a big strong umbrella guys ... the cows are coming home to roost ... the fall out promises to be deep and very stinky . . .

Ah... but GBH - what about GHG emissions? NZ butter sold in Ireland has less of a ghg footprint than butter produced and sold domestically in Ireland. So what sort of carbon footprint does your Kerry butter have compared to the local, but dearer product? This is a debate NZ so far has failed to have. Are we really concerned about climate change - in which we allow higher emission food products to be imported and sold cheaper due to subsidies at point of production, or do we show a real commitment and only allow the sale of low emission food, even if it is a higher cost? ;-)

... we work on small profit margins ... GHG emissions do not enter the equation when we can obtain a better product at a cheaper price we will . . If it was Mongolian yaks milk butter we'd take it on , or Ukranian beaver butter ... all good ..

What does it say about the NZ dairy industry when a foreign competitor can send their product half way around the planet at a cheaper price ?

To be fair or frank, it probably says way more about the lunacy and waist of resources that is globalization than anything else.

. . Provided we're competing on a level dairy field ( no government subsidies ! ) , it says to me that we ought not have a dairy industry at all , if others can do it cheaper & butter ...

.... globalization is great if it means the most efficient producers survive , and the have nots find their area of best performance elsewhere

Ah..level dairy field - there is no such thing when it come to the EU and trade. Subsidies GBH - that is exactly why EU butter is cheap. Their taxpayers are financially supporting their farmers. Also they have no tariffs to pay on dairy good in to NZ - unlike NZ processors trying to sell in to the EU market - not only do we have quotas but also tariffs to pay. Folks involved with FTA discussions including the EU, have publically stated that if they have to throw NZ ag under the bus 'for the betterment of other NZ trade' in order to get an EU FTA, they will. In speaking to Irish farmers recently the consensus among them was that the Irish dairy in general was really struggling to be profitable. So who is really paying the price for your cheap Kerry butter - it's Irish dairy farmers.

And now folks, the next stop is Venezuela! What a bunch of self rewarding tin gods this outfit has been rundown by.

Lots of pigeons coming home to roost - the shareholders council have been asleep at the wheel and were intimidated by board and mgmt - they should be sacked or shut down - they add no value. The restructure Theo carried out cost over .....$ 250,000,000 - that is the amount that went to the consultants - more costs came from redundancies etc.

The Shareholders Council knew years back that Beingmate was tanking and that Theo was most likely lying to them but did nothing because they were afraid of the wrath of the Chairman.

The same mgmt team and largely the same board that caused this are still in control.....will the owners never do anything?

This guy should have been on the council.

https://e2nz.org/2016/03/11/fonterra-boss-theo-spierings-punched-at-dar…

Rubbish to your comment TP regarding the same Board that caused this are still in control. Fonterra's problems are legacy ones. Only the Chair is a farmer elected director who has been on the board for more than three consecutive years - i.e. one term. Four of them elected for the first time in the last two years.

Unfortunately, you can't short sell this shower of s***

... SP has halved from $ 6.68 in January 2018 , to $ 3.32 today ... Big Short , if you could've got onto it ..

The Fonterrible share price peaked in 2013 at $ 8 .... it's been a sour milk journey down down ever since ...

They need people like Keith Woodford on the Fonterra Board.

People who speak their minds never make it onto boards, it's not the way it works. You're either in the "club" or a diversity hire.

Tautoko and I've experienced it first hand. Speaking out did my Director's career no good at all. Not 'rocking the boat' is the secret to a long and successful Director's career.

Thank goodness my shares in NZ Farming Systems Uraguay were forceibly taken from me.

Haha funniest comment in a while.

Fonterra has been (and is - as much as it continues in business) the greatest gravy train New Zealand has ever created. Its interest in a dairy value strategy is far outweighed by its value as a cash cow for its executives, management, staff, contractors, consultants, advisers and other hangers-on. In an environment where no-one takes responsibility for failure, where accountability is essentially meaningless, it is easy to pose self-interest as business acumen. Its failures are, regrettably, not limited to the company. They are a looming catastrophe for New Zealand.

Spot on workingman. We have several SAP contractors at work, some of whom were 'milking the cow' at Fonterra for 10 years prior to leaving.

I'd love to know how long the longest serving contractor is at that place, probably since its inception.

When they did the outsourcing to HCL in India the sacked a bunch of perm staff and kept a lot of the contractors, all of them on triple the amount the perms were earning.

Dairy farmers were more than happy to take advantage of dry stock farmers misfortunes, a bit rich to grumble when white gold turns to shit

Do Fonterra still own a 50% share in Clover/ Danone in South Africa ?

Where on earth would you ever find an honest answer to that. In truth, where in Fonterra, would you ever find an honest answer to anything?

Fonterra's problems started being solved as soon as the 43million dollar man ran back to Denmark. They have to write down, close down all foreign operations, refuse to pay dividends to non farmer shareholders, and get back to their basics. The main reason their suppliers have any financial problems is because they paid too much for their land. The usual solution is for them to quit- go broke, and someone buys their unit for a price it is feasible to buy it for. They also have to come up with a solution to the nonfarmer minority shareholder problem. However, being a small minority means that these people have no say in running the show, so it should not be too difficult to buy them out for what their shares are now worth, with no dividends being paid to them, and Fonterra can get back to being the farmer owned co-op it is meant to be.

Interesting - "It is also clear that many more of Prolesur’s farmers would leave Prolesur, and hence Fonterra, if they could. They would very much like to join Colun which is a Chilean dairy co-operative that has been smashing Soprole in the market place"

Chilean Dairy Co-op Colun smashes Fonterra's Soprole

Wonder how

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.