By Keith Woodford*

The latest dairy auction on 7 March has brought a cool breeze to the dairy outlook. There are signs it could turn even colder at the next auction.

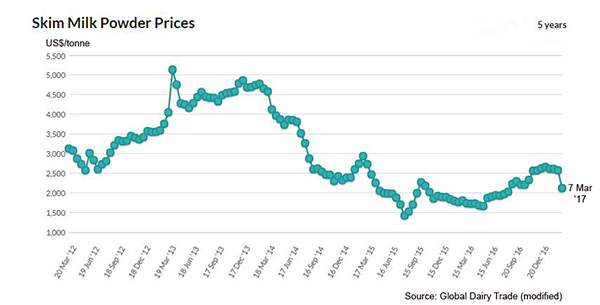

Whole-milk powder (WMP) at this last auction was down 22 percent to US$2785 from the 6 December 2016 high of US$3593. Skim milk powder (SMP) was down by 20 percent compared to December.

The decline has come as a surprise to many farmers and commentators, but the signs were there and had been building. As one derivatives broker said to his clients in the week before the latest auction, it was going to be ‘wretched’. And it was.

The futures price for 2017/18 milksolids has dropped from around $6.30 some weeks ago and is now trying to find a new level somewhere in the ‘fives’. It could go either direction in the next few months. That is the nature of commodities.

History tells us that when auction prices drop precipitously, it is seldom a single-auction event. One week out from the 21 March auction, the futures market prices are suggesting physical prices could easily drop by another 5 percent or more for both WMP and SMP.

Recent optimism around the industry has been remarkable. High quality farms have been selling at very good prices. It was as if the last two years had been forgotten, despite the fundamentals not changing a great deal.

It was reasonably clear in the New Zealand spring that the increasing dairy commodity prices were caused by declining production in many parts of the world, and that some of these declines were due to adverse weather. A big question was always going to be what would happen in the southern autumn.

The Chinese buyers learned the hard way in 2013 about the cost of relying on strong New Zealand autumn production, which in any year may or may not occur. It seems that this year most of them bought up what they needed well in advance. With this year’s autumn production now looking assured, there are problems as to where to sell that product.

Fonterra increased its supply of SMP for the March 7 auction by 49 percent. This sent a clear message that Fonterra was struggling to find sales away from the auction. Some will be critical of Fonterra for showing their hand so clearly, but holding back product usually creates further problems later. Taking the ups and downs is all part of the commodity game.

SMP from New Zealand has in recent months been selling well above the price of SMP from other parts of the world. A resetting of prices was always on the card, and became inevitable with the increasing volumes. But the extent of the drop, and the momentum around that, is a worry.

There are emerging signs of a new global surplus of SMP. Butter prices are very strong, and this is great news, but SMP is the currently unwanted co-product. There are still over 400,000 tonnes of SMP in store in Europe, and that too is casting a shadow. Many are hoping that the European stocks, now between six and 12 months of age, will end up as stock feed.

The six-month WMP outlook is not as gloomy as for SMP, but it seems that buyers are in a position where they can afford to sit back and wait. As always, China is the wild card on the demand side.

The next big buyer of WMP after China is Algeria. New Zealand has had some good sales to Algeria in the last year, but that has meant that the EU has been selling less to Algeria and that product now has to find a home somewhere.

My reading of the EU situation is that their dairy production will now stabilise and even increase over the next 12 months. The prices that farmers are currently receiving for their milk equate to about NZ$6 per kg milksolids. This is up some 25 to 30 percent on prices of nine months ago, and this is enough to encourage some farmers to seek production-cost efficiencies by increasing production.

Production in the United States also continues to forge ahead, with the latest statistics for January 2017 being 2.5 percent above the same month for last year. The Californian drought is well and truly over and that should lower feed costs for the big Californian industry.

The uncertainty for American farmers is whether President Trump’s immigration policies will affect their labour supply, and whether Mexico will continue to buy their cheese. Mexico is the most important destination for American dairy.

I am saying to the farmers I talk with to be cautious about next season. It could be wonderful or it could be disappointing. As always, it only takes one global event to shift prices a long way in either direction.

Part of our New Zealand problem is that we are heavily reliant on WMP which is only used in big quantities by developing countries. However, shifting across to more value-add price-stable products is going to be a long-term rather than a short-term journey.

With our seasonal production, we remain at a disadvantage for many of these value-add products. Seasonal production means low overall utilisation of costly processing plants, high inventory costs, and also increasing scrutiny from buyers concerning older-aged product. We have to balance that against the lower on-farm cost of production from seasonal milk systems, the lower cost of processing and marketing of commodities compared to value-add products, and the inherent volatility of commodities.

*Keith Woodford is an independent consultant who holds honorary positions as Professor of Agri-Food Systems at Lincoln University and Senior Research Fellow at the Contemporary China Research Centre at Victoria University. His articles are archived at http://keithwoodford.wordpress.com

9 Comments

"The decline has come as a surprise to many farmers and commentators" Not to our manon the spot AndrewJ however..

just going to bump along the bottom until someone drops production. In the States they are starting to dump spring flush.

From milk producers

Milk handlers in the Northeast have requested temporary permission to dispose of milk on farms while retaining their pooling privileges. In the heart of the country, milk is selling for as much as $6.00 under Class III, although most spot milk is moving at discounts ranging from $1.50 to $4.00 under.

In New Mexico, “handlers are actively looking for additional sales outlets... to avoid, as much as possible, discarding milk,” according to Dairy Market News. There are some processing issues that have exacerbated the situation, so some of the oversupply issues in the Southwest may ease as plants return to capacity. Nonetheless, it’s clear that milk is abundant and processing capacity is already unequal to the fledgling spring flush.

In the grain markets overproduction is built in

USDA helped the agricultural markets to refocus on fundamentals, which made for even steeper losses. The agency increased its outlook for Brazilian soybean production by 4 million metric tons (MT) to 108 million MT. This year’s crop will be the largest on record, by far. USDA also increased its estimate of Brazil’s corn crop by 5 million MT to 91.5 million MT. Private estimates are in line with USDA’s latest projection, but most analysts did not expect the agency to go so high so soon. USDA also increased its estimates of Australian wheat production, and South African and Argentine corn production. With that, global stockpiles of corn, wheat, and soybeans climbed and prices fell.

When are you getting your own weekly column AndrewJ? You'd have a large following.

Here Here

Careful out there Shaggers, the EU had a record beef kill

Report Highlights:

The European Union (EU) is forecast to produce and export a record volume of red meat in 2017.

While beef production is increasing due to the restructuring of the dairy sector, pork production is also

on the rise due to demand from China. Since 2013, the EU has been the biggest pork exporter in the

world. This year, pork exports are expected to remain strong as new market openings are being sought

and found, and sales are being supported by the acknowledged quality of EU pork and a favorable

currency exchange rate.

https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Livestock%20and%…

Korea is back 25% in six weeks

http://www.beefcentral.com/processing/weekly-kill-grids-dont-so-much-sl…

Too many unsold here

https://www.fedcattleexchange.com/page/SaleResults

USA

Beef production, at 2.10 billion pounds, was 8 percent above the previous year. Cattle slaughter totaled 2.53 million head, up 6 percent from March 2015. The average live weight was up 23 pounds from the previous year, at 1,370 pounds.

Aj, I am actively reducing my exposure to beef and in the main because of the informative links you post. Keeping more ewe lambs this year and buying fewer weaners.

Went for a walk up a hill on the weekend which gives a good vantage of Southern Waikato and man does it look wet. A lot of guys on low lying areas look to have full drains and surface water. While the wet to date has saved the seasons production (two guys I've talked to say after the terrible start, the rainfall through February will see this seasons production on par with last season) but after the last week it must be of some concern.

Maize should be coming off pretty soon, how tough is it going to be for the contractors to get it off then replant into grass without making a complete mess?

If it's a damp autumn how wet will it be at the start of calving?

Meanwhile I hear OCD is offering a GMP for part of next season's milk at $6.00..............

edit: price dropped .50cents

http://www.interest.co.nz/rural-data/dairy-industry-payout-history

click on the dairy payout history on this site. With much higher regulatory costs, are they much worse off than 2001?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.