ANZ New Zealand, the country's biggest bank, has posted a 15% fall in half-year profit with credit impairments and expenses up, and revenue down.

The bank says net profit after tax for the six months to March 31 fell $140 million, or 15%, to $789 million from $929 million in the equivalent period of its previous financial year.

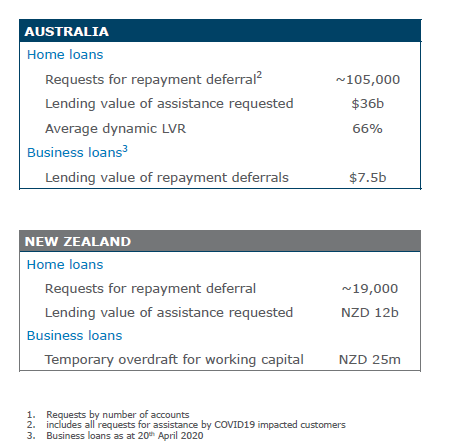

ANZ NZ says to date it has provided financial help to about 30,000 personal, home and business loan customers through repayment deferrals or adjustments covering lending of around $12 billion. (See more detail below).

"New Zealand's response to COVID-19 has resulted in extraordinary changes to the economy, the fortunes of businesses and the lives of customers," ANZ CEO Antonia Watson says.

"New Zealand has made much better progress in fighting the virus than nearly all countries, and that potentially paves the way to a quicker economic recovery. While that's encouraging there will be many challenges as the country emerges from the high level of response and starts to rebuild."

Watson says ANZ NZ has substantially increased its collective loan provision to recognise the possible impacts on economic activity through the bank's September financial year and beyond. ANZ NZ's credit impairment charge rose to $232 million for the March half-year, up from $32 million a year earlier. The extent to which the impact of the COVID-19 crisis on economic activity continues through the second-half of ANZ NZ's financial year, to September 30, will depend on how and when NZ fully emerges from lockdown, Watson says.

"We're optimistic many businesses will survive, but we know the next few months will be difficult and we're preparing for a higher-than-usual number of loan defaults," Watson says.

Operating income fell $288 million, or 13%, to $1.992 billion even though net interest income was 1% higher at $1.648 billion. Operating expenses increased $93 million, or 13%, to $828 million. The bank said its sale of OnePath Life and its 25% stake in Paymark partly contributed to the revenue decline, with the expense increase mostly due to regulatory compliance. Combined gains of $98 million on the OnePath sale to Cigna, and Paymark sale to Ingenico Group, were booked in the March half last year.

ANZ NZ says its total capital ratio, as a percentage of risk weighted exposures, stood at 13.9% at March 31, versus the Reserve Bank mandated minimum of 10.5%. The bank says customer deposits increased 5% and gross lending rose 3% in the March half.

ANZ Group defers dividend decision until August, sees 13% GDP contraction

The ANZ Banking Group, Australian parent of ANZ NZ, has deferred its interim dividend as it posts a 60% fall in cash profit from continuing operations and takes an A$1.67 billion credit impairment charge.

ANZ says it has deferred the decision on paying a 2020 interim dividend until the economic outlook is clearer. The bank's board will continue deliberating, and provide an update in August. In the first half of its previous financial year ANZ paid an A80 cents per share fully franked dividend.

The group's cash profit from continuing operations fell 60% to A$1.413 billion, with its credit impairment charge up to A$1.674 billion from A$392 million in the first half last year. There were also A$815 million of impairments on investments in Asian banks. Return on equity fell to 5.1% from 10.8%, and the group net interest margin fell 10 basis points year-on-year to 1.69%.

ANZ group chief risk officer Kevin Corbally says the bank is assuming Australian Gross Domestic Product will reduce by 13% in the June quarter, the largest contraction since the Great Depression.

"We then forecast some rebound in the September quarter, but it's actually not until 2022 that we get back to the levels that we saw pre-COVID-19," Corbally says.

Meanwhile, ANZ NZ says among other things to help offset the economic impact of the COVID-19 pandemic so far it has:

Deferred 19,600 home loan repayments and moved 20,900 home loans to interest only.

Granted 1,345 temporary overdraft facilities to businesses needing more working capital, worth around $25 million.

Waived the fee for contactless debit transactions for around 14,000 small business customers until the end of June, with collective savings of around 500,000.

ANZ NZ's announcement is here.

The ANZ group release is here, and ANZ's presentation is here. ANZ has also released an internal interview with group CEO Shayne Elliott here, one with group chief financial officer Michelle Jablko here, and one with group chief risk officer Kevin Corbally here.

38 Comments

Tipping over. Remember the virus impacts are only at the tail end of this reporting period, likely only the last month. The question is: what happens in the next 6 months.

There is no way they will be paying any dividend in August, that's just dreaming. Impairments for that period will be massive and likely growing.

As far as I'm aware, the big four have to retain dividends as part of government measures to protect them. They'll find another way to extract from NZ through transfer pricing however.

What gets me is every other business (excluding supermarkets and utility companies) has been asked to take a fall in their income for the greater good, but we have not seen or heard of any subsidy these banks are prepared to give the businesses. Mortgage holidays are certainly not subsidies. Quite the opposite, and generate a better return for them. Its unlikely to be available to everyone either, so its just lip service. I thought we were all in this together.

Putting this in context, collectively banks have $400 billions (approximately) of loans out to NZ business and people. On an average interest rate of say 5%, this would represent an annual interest cost of $20 billion. Just how they make $5 billion profit per year out of that doesnt seem right anyway. If the banksters were genuine with their offer to subsidise NZ business and people, they could afford to reduce their lending margins (difference between mortgages and deposit rates) by 1.25% and still not make a loss. Tell me which businesses are making a profit in these times please?

The NZ Government have been too soft on these parasite overseas banking cartel for too long. How could you support National now, when its plain to see their ex politicians have done nothing for the country, other than enrich themselves.

There is a new international accounting standard which now applies to the Aust/NZ banks where they have to assess impairment levels looking forward, rather than just backwards. Hence the large impairment numbers allowed for based on guesses as to what is going to happen with the economy and business with COVID.

The new standard was implemented as a consequence of the GFC where banks continued to report historic profits while knowing they were facing large impending losses.

Oh really? Good info Mac, thanks.

How long do they forward look their impairments? Is it for the next 6 months only?

This is so unfair.

With JK on the board as Chairman my prediction is the dividend payout will stand - with excuse it was for prior period and "the banks are strong and well capitalized" . (We can get a bailout if required - to big to fail)

The moment JK says he is leaving ANZ in a good state to explore other options, get your money out.

Wonder what he did with his options s before this came out.

The only good to come out of this epidemic for ANZ is that Cruellas tame valuer can sleep easy at night as Hiscos house will only be 7m after all.

Out of interest why did she get the label "Cruella"?

Probably a junior staffer at ANZ, they get blamed for all the shite that goes down. Something JK dragged along from other careers.

You can understand the juniors being aggrieved with C. They get thrown in the slammer for helping themselves to a few grand from the till yet management can give what is essentially 4 mill from the bottom line to one of their group in full view of NZ and nobody gives a toss.

Interesting reply from my bank yesterday regarding at what covid alert level they will lift the $1000 dollar restriction on cash withdrawals.

Their answer: The $1000 restriction on cash withdrawal will remain in place for the foreseeable future across all levels.

Not filling me with confidence.

Can you guys from interest.co.nz do a run around of the banks to see what is going on?

Seriously. Why does it matter?

I can't remember the last time I took out my wallet and paid $1000 for something in cash.

I can transfer $100,000 from any bank to any other bank or payee, on any given day at the press of a key ( much faster than you can run down to the ATM and press another set of keys!), and if I want to do more, I just have to give them a ring, and it will be authorised on the spot. ( subject to the obligatory talk about 'are you sure you know who the recipient is?' etc.) I think the default amount is $50k, but you can nominate the amount that suits you.

I cant remember the last time an economic contraction like this happened either. Do you really think the banks are going to allow you to electronically transfer $100k, if it doesnt suit them.

Suggest you consider all scenarios going forward, as cash in your wallet, in a safe or under the mattress may come in handy some day soon.

I can't see any restrictions on transfers coming, as the funds stay within the banking system. There should be no health reason to clamp down on cash withdrawals under alerts 2 or 1.

I am wondering if the government have directed that large cash withdrawals be restricted as far as possible....why?....

This is a BIG issue, and since when do banks get the "RIGHT" to limit how much of your "OWN MONEY" you can have?

It's not their money, it's yours. Why is this not making mainstream news, because this is a BIG ISSUE!

I disagree, mine above.

Cash is non-existant in some countries; Scandinavia countries etc.

If it makes you feel more secure to carry around a wad of cash, fill your boots! But make sure you don't lose it; have it stolen or get stuck with a whole heap of counterfeit stuff etc.

Cash was fine in the days when it was a Promissory Note - when it could be exchanged for another medium of trade - gold, in the main. But that was eons ago. Cash hasn't been what you think it is, for a long time. Probably before you even got your first dollar in pocket money!

If we lose the right to cash we also lose the right to freedom and governments/banks can do anything to us they like at the fiddle of a keyboard.

Which is why it will be left in place.

And it is also why taking cash out of the bank will continue, subject to physical constraints - like, not being able to restock the ATM or supermarket checkout tills because of delivery issues etc.

EVERYTHING has been 'rationed' over the last couple of months. Supermarkets would only sell you two of many things at a time etc.

Cash, for whatever worth it may give us, is no different.

Personally, I find it an inconvenience, but I accept that other's don't.

BW. You are missing the point entirely.

Which is?

Don't tell me!

You want to get your cash out of the bank and spend it on something more tangible, like the deposit on a house, that's going nowhere, right?

Can't you see how you are falling for the establishment line?

"Get your money out now! And spend it before the dreaded inflation destroys its value " etc.

That's what you are being' told ' to do - spend and buy, and that, my friend is exactly what you shouldn't be doing right now.

Later? Sure. But not now. Not when unemployment is going to sweep across the globe and devalue the price of EVERYTHING that you see with a "For Sale!" sticker on it this afternoon.

Because the price is going to be far, far lower in the months and years ahead, And 'cash in the bank' is going to be a scarce commodity.

And if it's because "Banks are going to fail!" that's stupidity. Banks, as a group ARE the economy. We can't exit without them. And if one, two or 100 get 'into trouble' they will be absorbed by other larger banks and depositor funds retained. That's why banks are merged, so the acquiring bank can assume the depositor funds into the new entity. Otherwise, what's the point!

negative interest rates

It's not their money, it's yours.

It's not your money, as in an asset you physically own.

Depositors just have a claim against the bank as unsecured creditors.

Remember when banks purchase a customer's IOU (loan contract) with their IOU (promise to pay) and credit said customer's deposit account with it, that's the sum total of the transaction - no cash (another promise to pay) involved at all.

since we introduced the OBR they have the right to take it all if they need it

There is no coincidence banks no longer guarantee deposit holders investments and Jonkey being at the helm of NZ's largest operating bank.

He has connections to the top, and knows alot more than the rest of us. Draw your own conclusions here, however the pattern should make it obvious.

Remember, you're an unsecured investor as a bank deposit holder.

Which is why I'll be sending my cash at hand to the UK soon. With interest rates so low, and the GBP exchange rate not too brutal, I don't see any perks of keeping it here. At least there (roughly) $172,500 is guaranteed.

Yep good on you, I'm doing the same the larger UK banks such as Barclays and Lloyds do offer international personal banking services for overseas customers. Which will also allow you to keep money in different currencies if you like and they have way more online security features then any of the more primitive options offered here in NZ.

After seeing some people saying ATM withdrawals were being restricted etc I happened to visit an ATM yesterday, had no problem pulling $1k out, and the limit that appeared on screen was $2k. Doesn't seem to be an issue with ATMs at the moment. Now i just need to decide where to put the money, no doubt to be forgotten about until next time we move, which might well be a decade away.

With all the 6 months offset in principal deferment happening, is anyone surprised? Agree with keeping an eye on JK. If he bails, then follow suit - quickly.

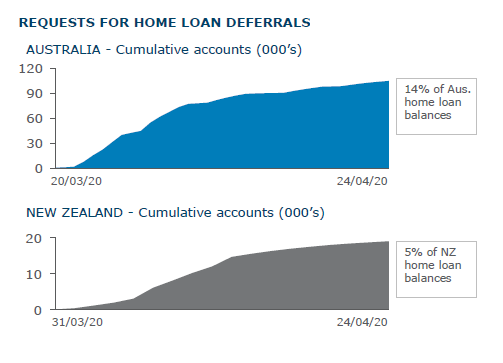

1 in 20 of ANZ's mortgage customers had asked for a deferral by last Friday. $12 billion over 19,000 customers gives an average loan balance of just over $630k. Assuming they all go interest only that's over $17 million in principal payments a month that will be deferred.

And if they all went for a complete payment holiday its more like $60m-$70m per month of payments not being made

There's a very interesting piece in the Herald on John Key's views on the economy, especially the property sector. Don't care for the guy much, but he has some interesting insights.

looks like he lost his midas touch in sydney,would he have been captured by the foreign buyers tax?

i would say he sold to retain his capital he knows a fall is coming so get out in the beginning or wait ten years for the recovery

he hasnt sold it yet!

From 90@nine this morning:

In Australia, regulator ASIC has told banks that when assessing new customers, they should not assume income levels will return to pre-coronavirus levels.

Surely that applies to all borrowers?

The change to dividend policy actually represents the most substantial change to the relationship banks have with shareholders in generations. Traditionally banks paid dividends through the cycle by being prudent lenders buy no longer will they be heavily favoured by pensioners as boring but dependable staple of a retirement portfolio. The fact they cannot do so now is going to change the type person who can invest in a bank and will make bank shares more volatile in future reducing the options available to banks (e.g. issuing more shares) in a crisis meaning they will have to issue bonds. It will also unleash executives to pursue growth instead of having to manage for a stable long term business.

Are we ready for pro cyclical banking? Well, it has just arrived courtesy of unintended consequences.

And hopefully an end as well to the interminable accusations that bank shareholders enjoyed excessive returns on their investments. Earnings and dividends were in the upper range but on a total return basis the shares had been under performers for ages, reflecting their elevated risk profile, which has now been emphatically realised. I think your predictions of the future profile of bank investor and increased volatility is correct.

Expenses rising? .. may be she just hinted what has been done months back by HSBC & Deutche Banks?

It's not easy does it? to deflate the balloon that has been inflated, but you just have to before later on opt for equilibrium which again favouring the Banks cartel side. Just a reminder the interconnected WORLD debt means not just OZ & NZ.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.