Rapidly evolving technology could easily accelerate the disintermediation of commercial banks, with deposits and even lending migrating to central banks, Macquarie analysts suggest, converting central banks into direct participants rather than mere custodians of trust.

This, Macquarie adds, would convert an implicit guarantee underpinning money into an explicit guarantee, and raises the question of what would become of the role of financial intermediaries?

Macquarie says this in a research note entitled ‘Stablecoins’ and Cryptocurrencies Do we still need banks or credit cards? The analysts note there are no financial stocks in its portfolios, noting technology and growing central bank power is reshaping banking and finance, and asks of banks; "what is their raison d’être?"

The analysts point out that money is a mere social convention, meaning people accept money in expectation everyone else will do the same.

"Hence, anything can serve as money, from seashells, rocks and gold to paper and electronic digits. At the same time, to be a sustainable convention, money must be backed by equally sustainable institutions of trust. Over the last several centuries, this trust was re-enforced by either gold and silver or by the credibility of central banks. Modern central banks are in turn backed by the fiscal authority of sovereigns and provide wholesale liquidity to lubricate the banking system," Macquarie says.

"However, AI [artificial intelligence] and distributed ledger-based technologies have the potential to generate trust and resilience and in the case of some (e.g. bitcoin), they can also offer a degree of protection against extreme outcomes in our over financialized world. The new technology can significantly reduce transaction costs and spread finance to otherwise unbanked segments. But it also poses a challenge to the conduct of monetary policy and the future of fractional reserve banking system that today multiplies public money based on implicit central bank trust."

"Hence, the forthcoming launch of Diem, re-branded and truncated Libra, and experiments with central bank digital currencies (CBDC) are starting to attract a great deal of attention. Unlike cryptos, these promise to be far closer to ‘stablecoins’ or in other words backed by liquid and trusted assets (e.g. the US dollar)," says Macquarie.

"As in the case of Bank of Amsterdam, first central bank prototype which existed for two hundred years, before collapsing in the late 18th century, it is a question of whether these stablecoins are rigid and limited by the store value of the underlying currencies or whether they are able to expand their balance sheet and provide liquidity support. Given the temptations, the more flexible these stablecoins are, the less stable they become and the greater chance of a collapse, unless they are backed by central banks and that’s where CBDCs come-in."

Macquarie's comments echo those made recently by credit rating agency Moody's, which warned CBDCs could have "profound negative consequences" for commercial banks - displacing their current role in the payments system, disrupting their business models, and forcing changes to their funding model.

Just last week the Bank for International Settlements (BIS), the central banks' bank, trumpeted a successful wholesale CBDC experiment known as Project Helvetia. BIS says Project Helvetia shows the feasibility of two proofs of concept, using "near-live" systems to settle digital assets on a distributed ledger with central bank money. It involved comparing a proof of concept linking the existing payment system to a distributed ledger and another issuing a wholesale CBDC. BIS says Project Helvetia sets the scene for further joint experimentation to assess the impact of digital innovation on the future of the financial system.

Closer to home the Reserve Bank of New Zealand (RBNZ) has no immediate plans to launch a CBDC in New Zealand, Assistant Governor Christian Hawkesby said recently. However, Hawkesby did say the RBNZ is "following developments very carefully, and are among the 80% of central banks that are actively researching CBDCs."

Overnight the Institute of International Finance issued a report on China's digital renminbi (RMB), noting the People's Bank of China has been working on it since 2014. Known as the DCEP, digital currency, electronic payment, experiments have been run in four cities with the DCEP's debut scheduled for 2022.

Meanwhile, Macquarie asks why should central banks issue wholesale tokens only to other central banks and commercial banks but not to non-bank financial institutions, businesses and people?

"The argument has been that central banks cannot collect deposits, assess risks and monetize assets as efficiently as commercial banks. But, over the last decade, we have already seen central banks becoming major direct players in the bond and credit markets and they even provide direct lending to the main street. Also, technology is proving that almost anyone can collect deposits and assess risks at a fraction of historical costs," says Macquarie.

"Hence, technology could easily accelerate disintermediation of commercial banks, with deposits and ultimately lending migrating to central banks. This will turn central banks from the custodians of trust into direct participants; or convert an implicit guarantee underpinning money into an explicit guarantee. What would be then the role of financial intermediaries?"

"There is now a crowded field of economists and central bankers, simulating disappearance of bank deposits and their replacement by central bank tokens and the impact on liquidity and lending. Unlike previous centuries, we live in a world flooded with excess capital, and instead of discounted cashflow, it is ‘fair’ allocation of this excess that matters. Commercial banks and fintech can help but they will exist solely at the grace of central banks and their returns will be determined by them," Macquarie says.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

49 Comments

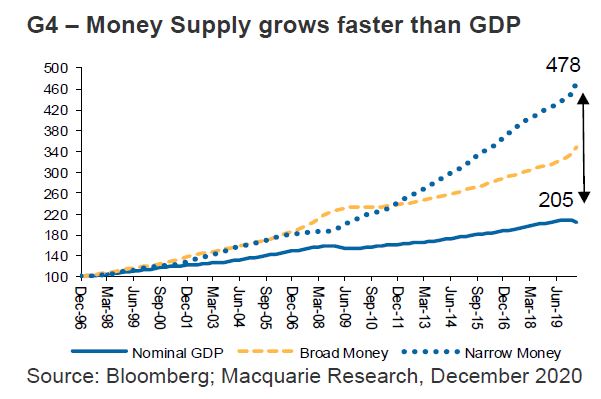

I've been pointing out for years that the money supply is growing faster than GDP.

Credit is borrowing from the future. What happens when there is no more future to buy?

Agreed. Great question btw, Gareth.

As we crest the Limits to Growth, zero then negative interest-rates were all that fitted. This is why cultures from less resource-endowed lands outlaw compound interest; you can't repay it with sand. But this also tells us that those who built a temporary 'business model' issuing interest, were always going to be in trouble. Sure, you can charge a one-off flat fee (which cumulatively fit the resource/energy underwrite) but that's it. Makes one wonder why?

Better society controls activity within planetary (and local) limits, and this may well reflect in Central issuance. But, as Scarfie points out, if the future can deliver less and less, the issuance will have to reflect this.

We're basically borrowing against productivity and environmental gains from future tech now. And the longer it takes us, the longer we're pushing out the payback periods and that's assuming we don't get cold feet and start cancelling research projects in the here and now.

If we'd printed a billion dollars and helicoptered it into advanced materials start-ups, we'd at least have a shot at getting something out of it, maybe. But we haven't done that.

The median lifespan of a country isn't that long. As soon as they are invaded, have a civil war, revolution, collapse etc. the clock gets set back to zero. In fact often debt is responsible for triggering these events, think about the outcomes of the finance deals JP Morgan backed in pre-war Germany and South America

We should be decentralising banking into the community on a non-profit basis.

Ideologically captured central banks serve no useful purpose, beyond exercising mutually agreed regulatory oversight.

They’re right that banks serve little purpose in a disintermediated world.

If this is all going to happen , I would rather it be controlled by a central bank than Zuckerberg. Lesser of two evils, etc.

The idea seems sensible but just if central banks would become democratic institutions, otherwise we would be effectively be creating a private monopoly ruling the economy of our nations.

Scarfie and PDK are correct above - agree totally.

The banks have largely done this to themselves, become too greedy, too powerful and too controlling and driven the inevitable push back.

Monetary technology in the blockchain space represents the final transfer of power to big tech. To predict the future in the decentralisation of our present systems look to the past and the decentralisation of information systems throughout the last 20 years. Following that pattern the trend is democratisation at an individual level, and centralisation at a corporate/govt level. The early adopters will hold the keys to the kingdom ala Musk, Thiel, Bezos, etc. The laggards will pay a premium to meet the market, or fade from existence.

If they use Facebooks token, maybe. But that's the point of Bitcoin. It's not run by big tech, or anyone. Facebook is the epitomy of centralisation. Bitcoin is the opposite. Thats why countries could use it as collateral to transact in a neutral format.

2nd later solutions for everyday transactions are coming. It could really be the end for banks, it should be. They have to compete with decentralized networks and they can't.

A world with bitcoin as the medium of exchange is a world without a dominant empire/s. It is the empire that decides the currency.

No it isn't, it is the market that decides the money. Look at the gold standard, countries came to the conclusion that if they weren't using gold as their means of exchange, their currency was losing purchasing power and it was more difficult to do trade/transactions. Ergo it became the (basically) global standard, with countries like India and china that kept using the softer money, silver, having their resources pillaged.

But yes the defacto world reserve currency has changed with the dominant empire at the time from Portugal to Spain, the Netherlands, France, Britain and now America, but these were all backed by gold so the issuer was of less importance. Until the US broke the tether to gold etc. But Bitcoin is global and is not controlled by anyone and therefor is for everyone, so people can voluntarily opt out of the current system if they want.

@Galloleous is onto it - this is not about bitcoin (which is a reserve/hedge exactly like gold) but rather blockchain which is a historical first where the world is suddenly able to share a decentralised ledger that matches a pre-agreed set of unchangeable rules. The transactional governance that banks provide is finished because the rules of a cryptocurrency are set in stone from the outset and can't be adjusted undemocratically. Going forward the RBNZ are going to have to bake their policy into our currency in this format. Banks and Card companies will lose out at point of sale, as zero fee instant peer to peer transactions become standard. My pick is much of the government involvement after coding the policy/currency will be at the POS terminal, tracking payments and individuals for tax purposes. When everyone has an eftpos machine in their pocket connected to their own personal bank with the ability to make instant transactions to their neighbour who has the same, it makes sense to me that the legislation is likely to be targeted at this area and there will be an approved set of systems.

I'm a bitcoin maximalist and crypto-wonk because these systems exist already and I think they're inevitable, but I've never been more worried about the macro outlook and the amount of control these tools are going to give to the flawed individuals who hold our highest office. Any individual in a conventional job is going to have zero financial anonymity, as the whole chain from salary to item spend will be auditable by the IRD without explicit consent. In a country where we've got on board with "nothing to hide, nothing to fear" that's an unnerving prospect if history is anything to go by.

So when I talk about "big tech" I'm talking about centralisation of our entire financial system onto decentralised blockchain networks. The "laggards" are likely to be the banks and traditional financial institutions who through organisational size, company culture and decreasing relevance simply aren't able to keep up. The "early adopters" are the crypto maximalists at an individual level; and businesses and governments that have the motivation and staff to engineer and deliver these services as they become increasingly mainstream at the macro-level.

Great stuff and well expressed Ezy.

Can not like this comment enough my fellow maximalist.

That is the problem with CBDC, at this stage digital transactions are fungible ie it is just another number. But with CBDC each transaction is trackable and could lead to a very bad outcome.

The other thing I find unbelievable is the articles put out by the IMF and ECB. They advocate to create a digital currency and ban cash because then you can have negative interest rates. But they completely ignore the existence of Bitcoin. Why the hell would I use their shitcoin with -ve rates when I can use BTC lol

The hardest money always wins. See Michael Saylor is aiming to raise $400m in Sinor notes to buy more Bitcoin with. https://twitter.com/michael_saylor/status/1336650683072831496?s=20

Pretty much the start of the speculative attack Pierre was talking about back in 2014

https://nakamotoinstitute.org/mempool/speculative-attack/

Thanks for the nakamoto institute link Galloleous. Really interesting well authored reading. The article on Bitcoin fixes this is breath-taking:

History has consistently established that the experts are limited in the field of their own expertise, yet policies such as quantitative easing continue to be pursued, largely because macroeconomics and central banking is a monoculture, as Taleb describes. The mainstream policy position starts with the assumption that central banking is core to the function of an economy; then debate centers on what levers to pull and how best to manage the economy via central bank planning. Active management of the money supply via quantitative easing is taken as a given; it’s a question of how much and when, rather than if.

Sorry wrong conclusion

The US realised that it's all about OIL

Hence the petrodollar

Nothing else matters but control over energy resources

The rest is just majic beans

But that has changed now with fracking and the easy access to shale oil. the USA has gone from an importer of petroleum products to a net exporter now. They are more then energy self sufficient so don't need to invade the middle east anymore. Look at that change from early 2000's

https://www.eia.gov/todayinenergy/detail.php?id=5290

Bitcoin's value is not primarily a means of exchange. That's a big misunderstanding.

No at this stage it is a store of value. If you own 1 Bitcoin, then you own 1/21 millionth of the entire Bitcoin supply and NO ONE CAN EVER DEVALUE your stake in the network. As the network grows in size and value it will evolve into a means of payment with second layer scaling solutions such as the lightning network. On chain transactions should be used for large and valuable transactions that need to be immortalised on hard drives all around the world, not purchasing your coffee cough Bitcoin Cash cough. So people will make numerous transactions on second layers and then settle 6 monthly (or as regularly as they feel like the need too) back to the main chain. Strict scarcity is only found in time and Bitcoin, everything else can be created with an increase in human effort.

OK. That's better. The means of exchange will be coming from a 'bridge currency' between the different silos: BTC, CBDCs, Libra, JPM Coin, etc. Ripple is leading the charge with the software, but their own XRP may not be a de facto choice. However, I wouldn't write off XRP at all. I've used it to transfer funds (from myself in Australia to myself in Japan). Cleared in literally seconds.

Just an observation: one can send money from NZ to other parts of the world using virtual banks like www.transferwise.com and depending on the target location it clears in 4 seconds.

This was unheard of even a year or so ago when it took several business days.

'If you own 1 Bitcoin, then you own 1/21 millionth of the entire Bitcoin supply and NO ONE CAN EVER DEVALUE your stake in the network.'

But what if a child says one day 'Oh look: the emperor wears no clothes!'

But what if a child says one day 'Oh look: the emperor wears no clothes!'

All currencies are based on trust. Bitcoin is no different. The reasons why BTC owners hold it are quite compelling compared to the trust people put in fiat currencies.

Except the power of a fiat currency isn't just in the psychological willingness of others to accept it, but on the power of the institutions that generate it.

Governments have the power to demand you use their currency to pay your taxes, ultimately.

If you think that's true then you should be buying Venzuelan Bolivares like they're going out of fashion. There's quite a few for sale as sculptures right now https://www.etsy.com/nz/listing/823601799/brown-made-from-100-real-mone…

The strength of a sovereign fiat currency depends on the strength and sobriety of the sovereign, as Venezuela, Zimbabwe, Weimar, and others demonstrate.

The value of digital currencies that lack a sovereign, such as bitcoin, is entirely consensual, like a Da Vinci painting worth either $50,000 or $500,000,000, depending on whose signature you think it is today.

Exactly. Which is why Japan can't get inflation of their yen, even when they want it. People just believe that the Japanese gov't will pay its debts, with good reason. Japan makes a lot of useful stuff, the companies that make it pay Japanese taxes, the Japanese gov't has a reliable income and it's a politically stable nation. No one is worried about whether the bulk of Japanese debt can ever actually be repaid, only whether they'll get their own chunk of it back. No one cares about the principal.

Or if internet connection gets disturbed. Ask people of Kashmir where ruling govt has turned off internet for public from past 2 years!

... so , Kashmirian kids will have to read actual books ... dusty olde tomes .... NOOOO ! .. . oh , the inhumanity of an uninterneted world ...

If you have a cellphone that can connect to any network then you have internet. And starlink will bring internet to almost the entire world within this decade.

https://chrisgimmer.com/bitcoin-reserve-asset/#:~:text=Portability%3A%2….

Great article about Bitcoin summarising several other articles and the main use case. Enjoy :)

Are we on the path towards a soviet style banking system? It looks like the central bank owns the risk of our retail banks, so why do we allow them to make a profit? We may as well just allow the central state owned bank to lend directly to who it wants in the quantity it wants. Soviet style banking anyone?

The banks have been doing this for decades IO with the tacit approval of Governments. It's called socialising the risks while privatising the profits. Refusal of Governments to limit bank influence and power has allowed to problem to become significant to the point they are now afraid to act.

Banks cost an awful lot to run. Crypto provides instant processing, no fees (if done right) and none of the political considerations that modern banks have adopted. A potentially more stable (decentralized) vehicle of value. Be your own bank!

Since the banks employ armies of people who pay tax and they make massive profits which are also taxed. The existence and profitability of banks is in any NZ governments interest. As long as they play with a straight bat around tax compliance they will continue to enjoy government and RBNZ support. It is just a shame that the excess profits are repatriated to Australia. Maybe that has an element of political quid pro quo as well.

But if those armies and all their fees are removed, and all the working days wait time, and the inefficiency, then those armies need to look for different work but every other industry is far more efficient and saves a ton of money. The banking system is a sponge sucking productivity out of the rest of the economy as it stands, and requiring constant bail outs to continue. Plus blowing up all the ponzi rort bubbles.

Yes this has been a direction my thinking is shifting - but has only happened the last couple of years given central bank actions. Banks almost become a self licking ice cream cone. In theory we could all just work in the FIRE industry and sell financial products to each other and call it an economy. But if you can't sell those products internationally, how does it benefit a country and its people?

I have thought of late, that in a 'neo-liberal' society like NZ, where the focus has moved to individual enrichment, can we still regard exports as a "national good", or do they just benefit the exporter? And should we even be considering what "benefits the country and its people"?

I think we've got the point where neoliberal economic thought is driving inequality. Wealthy are getting wealthier. Business owners want to minimise cost inputs (including labor) and people are being left behind, but then socialist policies ('being kind') are supporting that growing distortion without intelligent regulation to prevent that distortion in the first place.

I think our current PM talks socialism, and acts neoliberal.

Yip so it will only make things worse. Paying accommodation supplements and housing people in motels that costs the taxpayer billions per year while landlords grow richer by the day because of state regulations and fiscal/monetary policy is just so completely stupid that you couldn't make it up - but here we are.

In theory we could all just work in the FIRE industry and sell financial products to each other and call it an economy.

I've thought about this myself. Essentially, that is much of what the economy is 'kind of' doing (or at least for wealth generation). We all think the Zespris, Fonterras, Silver Ferns are great because they enable the selling of goods abroad. But if the FIRE industry is so inexhaustible, why do we bother with exports? And why is it generally admired and seen as virtuous? Exporting of commodities or services appears to be a waste of resources given that our mechanisms seem better at producing wealth out of nothing.

Now my comment carries a bit of devil's advocate about it. Nevertheless, I don't think the idea is too far removed from what many people believe (and that includes the ruling elite).

Do you mean like this https://bankprofitclock.kiwi/

Here's a laugh (with a bit of 'truth'):

https://pbs.twimg.com/media/Eo0RqFAUYAAxxg5?format=png&name=small

'Central banks should consider offering accounts to everyone: Individual accounts could improve consumer welfare and macroeconomic policy'

https://www.economist.com/finance-and-economics/2018/05/26/central-bank…

Yes.This is not a hypothetical question of whether banks as we know them will remain relevant or not. This is a notification of the direction of navigation.

Banks have swallowed the morally correct woke cool aid ... they're refusing loans to Bathurst Resources , because it mines coal ... regardless , it does so legally

... not for the first time banks are basing business decisions on their moral compass , not on the business investment merits .... yet they lend to casinos .... hypocrites !

They keep laying off staff and closing branches. If there is no personal human face to face scrutiny on ones banking, and everything is simply electronic based on your digital footprint, then simply, they are a dinosaur.

In the approaching digital currency work, what value will they actually add....?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.