The Reserve Bank is mulling the possibility of a "single provider" of cash in this country in the future, perhaps through something like a private-public partnership, Assistant Governor Christian Hawkesby says.

Hawkesby was sharing some of the central bank's thoughts on the future provision and use of cash in a speech to the Royal Numismatic Society of New Zealand, Annual Conference in Wellington.

He said it has become clear that the cash system as it stands "will not be sustainable in a world where cash is used less and less".

"This requires a broader response with either a series of changes to the cash system or a transformational redesign of the entire system."

He didn't go into further detail on how the "single provider" system might work, or a timeframe for when such a thing may become a reality.

With the rapidly declining usage of physical cash, the RBNZ has been doing a lot of work on the subject through its Future of Cash programme including the issue last year of a consultation document, in which the central bank take on a stewardship role in the cash system, providing system-wide oversight and coordination.

The Reserve Bank has historically been responsible for issuing bank notes and coins on demand. This meant issuing cash to banks, collecting unfit cash, and processing, storing or destroying the cash that is returned to us. The remainder of the cash system, i.e. the banks’ distribution of cash to the public and the transportation of cash to and from retailers has been in the words of the RBNZ "held together by a set of informal arrangements and commercial incentives".

The proposal for the RBNZ to act as "the steward of cash and the cash system" has been included in the recently introduced Reserve Bank Bill.

Taking care of money

"Stewardship is defined as 'the act of taking care of or managing something'," Hawkesby said.

"For us this means ensuring that New Zealand has a cash system where people can easily withdraw, deposit and pay with cash when they need to, and the cash system remains efficient and resilient to sudden shocks and a declining transactional use of cash."

The RBNZ recently created a new department called Money and Cash - Tari Moni Whai Take.

"Te reo Māori version of the name sums up its purpose nicely, 'the department bringing money that’s fit for purpose'", Hawkesby said.

"This department is now responsible not only for the production and distribution of bank notes and coins, but also evaluating the broader policy issues associated with the future of money in New Zealand. Accompanying this, we are planning to establish a new governor-level Payments and Currencies Committee, responsible for strategic, policy and oversight decisions for our roles as an issuer of currency, operator of payments and settlement systems, and steward of the cash system."

Hawkesby said the RBNZ was continuing to engage with the public and industry, including on "system-level information and resilience needs".

Developing standards

"We are also formalising and embedding the distributed vaulting arrangements deployed during Covid-19. Alongside this, we will be working with industry to develop standards for banknote processing machines to ensure the authenticity and quality of our notes."

However, it had become clear that the cash system as it stands would not be sustainable.

The RBNZ would therefore "undertake a holistic and strategic review of the cash system".

"The objective of the review will be to ensure that the physical and business arrangements for cash distribution are efficient, resilient, lower carbon and set up to meet the public’s needs now and into the future. The review will also take into account the public benefits and the increasing costs and efficiency challenges of providing cash," Hawkesby said.

"One option to ensure that cash is available for the long-term might be concentrating cash services in a single provider.

"For example, the end-to-end cash infrastructure could be provided by an industry monopoly model.

'Private-public-partnership'

"Alternatively, a private-public-partnership as seen in some parts of the water, transport and electricity industries could be used. Such a model would recognise the public case for cash."

Hawkesby reiterated that Covid-19 had also highlighted the important role that cash plays in times of economic uncertainty.

"During the weeks leading up to the March 25 pandemic lockdown, New Zealanders demanded an unprecedented amount of cash, with $800 million of bank notes issued in March alone (compared to $150 million in March 2019).

"These bank notes have not yet returned to the banking system, meaning they are likely still being held by the public."

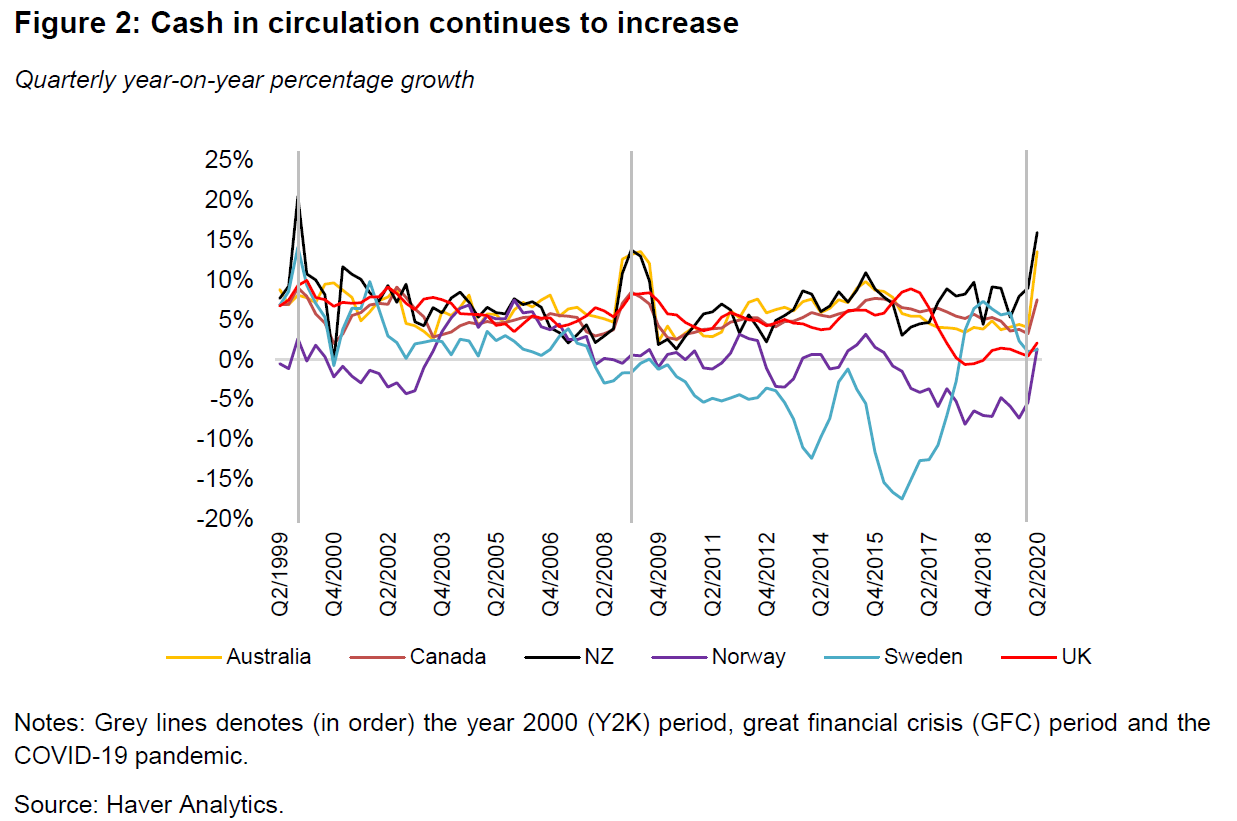

Hawkesby said since then, cash in circulation had continued to increase, growing by about 15% year on year during the second quarter of 2020.

"Many other countries have also experienced increased demand for bank notes during the pandemic, as a store of value and a back up method of payment.

"It is not unusual for cash holdings to increase during periods of uncertainty. In the lead up to the year 2000 wide-spread uncertainty of potential computing failures (the so-called “Y2K bug”) resulted in a sharp increase in cash in circulation (quarterly). Similarly, economic uncertainty during the financial crisis over 2008 - 2009 resulted in a rise in cash in circulation. Smaller increases in cash holdings can also be seen with regional events such as the 2011 Canterbury earthquakes."

Digital currencies

Hawkesby's speech also made reference to digital currencies and the potential for central bank digital currencies (CBDC).

The Bank for International Settlements (BIS), which is owned by 62 central banks, including the RBNZ, recently issued a report in conjunction with seven of the heavyweight central banks identifying the foundational principles necessary for any publicly available CBDCs to help central banks meet their public policy objectives.

The RBNZ has looked at the question of digital currency.

In his speech, Hawkesby said ultimately, the catalysts for researching CBDC depend on local needs.

"Central banks in economies with declining use of, and access to, cash are considering whether a CBDC could deliver an additional form of legal tender. For example, in Sweden, the Riksbank is considering an e-krona as a digital complement to cash given the decline of cash in circulation.

'Stepping stone'

"Conversely, central banks in economies with a heavily reliance on cash are investigating the potential for CBDC’s as a stepping stone to help the unbanked population move into the formal banking sector. A CBDC could improve financial inclusion, particularly if it is established with a government-led digital identity scheme. For example, the Central Bank of the Bahamas has launched a CBDC pilot called “Project Sand Dollar” with the goal of increasing financial inclusion across the islands in the Bahamas, where many people rely on cash but face difficulties accessing bank branches.

"Further, in the case that a foreign-issued or privately-issued currency became prevalent, a CBDC could enable a central bank to retain monetary sovereignty and price stability."

And the case in New Zealand?

"To be clear, we have no immediate plans to launch a CBDC in New Zealand," Hawkesby said.

"We are, however, following developments very carefully, and are among the 80% of central banks that are actively researching CBDCs."

Hawkesby made no reference to the recent stated intention of a new Auckland-based financial services company P^werFinance to launch what it is styling as a "world first" digital version of the New Zealand dollar early next year.

37 Comments

"...the cash system as it stands "will not be sustainable in a world where cash is used less and less" yet RBNZ also says "cash in circulation had continued to increase, growing by about 15% year on year during the second quarter of 2020"

A particulaly useful medium of payment in the event a significant earthquake takes out the local digital alternative.

Today ANZ our biggest trading bank removes the ability to bank and get foreign currency under the smoke screen of Covid.

What a disgrace? It appears they don't want customers being able to take out there money in foreign currency

https://www.nzherald.co.nz/business/covid-border-restrictions-behind-an…

You know the saying about banks..they lend you an umbrella when the sun shines, and take it back when it starts raining.

If a Bank is not able to sell/purchase forex cash, what is the use ? Pushing customers to use other channels ? Total disgrace.

They are very reactive to protect their income/profits, though they talk of serving the public.

Similar to insurance companies, they don't cover many risks.

shooting themselves in the foot. Why isn't everyone using transferwise, it's way cheaper and faster than using the bank.

As some people want physical cash.... USD for example.

Transferwise or Xe or others do not help with this...

RBNZ are dangerous. The only way negative interest rates works is if you cant take the cash out

IMF paper on: Cashing In: How to Make Negative Interest Rates Work

https://blogs.imf.org/2019/02/05/cashing-in-how-to-make-negative-intere…

"When cash is available, however, cutting rates significantly into negative territory becomes impossible. Cash has the same purchasing power as bank deposits, but at zero nominal interest. Moreover, it can be obtained in unlimited quantities in exchange for bank money. Therefore, instead of paying negative interest, one can simply hold cash at zero interest. Cash is a free option on zero interest, and acts as an interest rate floor."

And the kicker in that article... They don't acknowledge or mention Bitcoin anywhere. Woeful ignorance in regard to the thing htat started this whole movement in the first place!

Why would I hold their shit digital fiat at negative rates when I can hold a globally distributed, secure and uncensorable digital asset whose monetary policy cant be changed??

Well because they will outlaw any competition to themselves.

That is because bitcoin is useless as an actual currency, for day to day transactions, if you where to scale it up to the number of financial transactions that occur via eftpos it would exceed the power usage to everything else combined. The only thing it is good for is scams like ransomware and speculating in zeros and ones on your computer.

How do we implement negative interest rates without a bank run... lets get rid of cash!

Take it easy - vault cash held by our collective banks amounts to $843 million compared to a total $629,345 million balance sheet.

Hawkesby is quoted here today discussing cash being held by the public and Not returning to the bank system? What planet is he and RBNZ on....

https://www.stuff.co.nz/business/123136565/households-hoarded-an-extra-…

“During the weeks leading up to the March 25 pandemic lockdown, New Zealanders demanded an unprecedented amount of cash, with $800m of bank notes issued in March alone,” said Christian Hawkesby, Reserve Bank assistant governor, general manager, economics, financial markets and banking group.

“These bank notes have not yet returned to the banking system, meaning they are likely still being held by the public,” said Hawkesby, speaking at the Royal Numismatic Society annual conference in Wellington.

During the lockdown it became clear cash hoarding was happening, but Hawkesby confirmed that it has continued.

This RBNZ data release of it's own balance sheet confirms an $8.042 billion outstanding cash in circulation liability for the month ending Sep. 20. It was $6.853 billion a year earlier.

Assuming people are holding the cash and not converting it into other stores of value.

The purpose of digital currency is to control people's ability to hold money in person, ie cash.

This is a fundamental erosion of freedom and personal autonomy.

And I regard it with deep suspicion.

If you cannot hold cash you cannot withdraw it when bank is in trouble.

of course banks will never get into trouble now will they??

Mike kirk correct. But the media and breakfast shows are using the convenience and black economy narrative. It's disgusting..

Maybe unbank yourself? I.e. go "Bankless"

"The Bank for International Settlements (BIS), which is owned by 62 central banks, including the RBNZ,.... with seven of the heavyweight central banks ..."

There's the seed of most of our problems; in that one sentence.

"Do as you are told RBNZ, or we'll make you regret it"

It's going to take real courage for Adrian Orr and his Merry Men to do what has to be done for the sake of our country. New Zealand has led the way on so many occasions Phillips, of The Curve fame, was one of us; Inflation Targeting was ours first; we brought in the OCR in 1999. Are they up for it again? Against all probability, I hope so.

Mr Orr has shown he will do whatever it takes to destroy NZ and follow Europe / Japan down the bond market destruction with negative OCR.

Never worked in history, he has failed to show courage for 3 years and destroyed savers at every stage.

To say it has not worked, you have to say what it is trying to achieve before saying it's a failure.

And maybe we just need to be more patient?

You mean pumping up asset prices at the expense of savers ?

Look at the EUR bond market and what negative OCR has achieved ? Put it simply they have destroyed the bond market period and no one will buy that crap except the ECB. You think that has worked ?

If you want to have no other buyer in town but the central bank, yep go negative. Can never raise interest, stuck in the corner always buying govt debt ? Your goal achieved alright, you have no place to go as a central bank but buy.

https://businessdesk.co.nz/article/economy/rbnz-threatens-cold-bath-for…

“The limit to monetary policy is high inflation, the failure of monetary policy is deflation. I’d prefer to be battling the quality problem of re-containing high inflation than the real challenge of battling deflation.”

https://www.stats.govt.nz/indicators/consumers-price-index-cpi

Orr has created the inflation or pumping up assets at a point when ALL logic says higher interest rates are required.

Deflation is happening due to the destruction that can be attributed directly to shutting down the economy.

Orr has created an environment of no confidence in monetary policy.

Who has and continues to benefit directly from this easy money, mainly the govt who does not care about risk as hey we can always slap another tax on.

Is the Reserve bank trying to tell us that notes and coins are the only medium of currency that it creates? Are we never to be told that it creates electronic currency every time that the government pays a bill. Why the big secret? No one now seriously believes that taxation and borrowing finances the government, apart from mainstream economists it seems, who don't seem to know where money comes from.

Yes. The biggest losers with CBDCs will be the retail banks IMO. They're the ones who get to clip the tickets and allocate money as they see fit. As you can see with the housing mega-bubble, they operate within their own interests.

Is the Reserve bank trying to tell us that notes and coins are the only medium of currency that it creates? Are we never to be told that it creates electronic currency every time that the government pays a bill.

Can you point to a part of this stylised RBNZ balance sheet where the bill paying authority you claim is registered?

The Reserve Bank is on the same side of the balance sheet as the Treasury, it is part of government. Adrian Orr states that here. https://www.stuff.co.nz/business/money/114923477/why-reserve-bank-gover…

Hmmmm.....interesting timing given the announcement of the 'Bretton Woods moment' by the IMF. The following is the announcement. In layman terms, this suggests that we are indeed moving to Central Bank Digital Currencies. It's just a matter of time.

https://www.imf.org/en/News/Articles/2020/10/15/sp101520-a-new-bretton-…

Some of the leading thinkers in the crypto community have been highlighting that this was inevitable. The debt-based monetary system is out of gas. CBDCs can be used for UBIs etc while everything else unwinds. The trade off is that the average joe will lose freedoms as they will be more reliant on the state than ever before and they will need to comply with the central banks / govts to get their free dosh.

J. C

Yip.. He who gives up a little freedom for protection deserves neither.. Ben Franklin.

So a private monopoly is going to address the increasing costs of running the cash system??? Since when has a statement like that ever made sense.

So why do it....hmmm...maybe so that they clip the ticket so hard on cash transactions that people are driven back into the electronic system where the government regains control.

So a private monopoly is going to address the increasing costs of running the cash system?

And the monopoly being? The central banks themselves? Who contract to fintech providers?

I find it ironic that the imf and Co demand free markets and competition yet endorse a monopoly on the new cbdc..

Harry Dent Explains How 3.44 Trillion Money Printing Will Crash Stock and Real Estate

Better to privatise the Central Bank and list on the Stock Exchange ?

https://www.frbservices.org/financial-services/fednow/what-is-fednow.ht…

"The FedNow Service is a new instant payment service that the Federal Reserve Banks are developing to enable financial institutions of every size, and in every community across the U.S., to provide safe and efficient instant payment services in real time, around the clock, every day of the year."

If we are going to move away from cash, frankly we already have, having a bank account has to become a human right, no more terms and conditions that say a bank can stop having you as a customer, for whatever reason it sees fit. Sure they shouldn't have to lend to you but allowing you to spend your own money should not be at their discretion. Or the government should provide the service to people who banks will not accept.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.