As it posts a 4% rise in half-year profit, ASB is promising not to force the sale of any ASB customers' owner-occupied homes this year.

ASB's net profit after tax for the six months to December 31, 2020 rose $26 million, or 4%, to $625 million from $599 million in the same period of the previous year. That's just $5 million shy of the bank's record interim profit, achieved in the six months to December 31, 2018.

Against the backdrop of COVID-19 ASB says it's "making a commitment to keep Kiwi families in their homes."

"There will be no forced sales of owner-occupied family homes in 2021 for ASB customers we are working with to resolve the challenges they are facing. Mortgagee sales are uncommon, and they are always the last resort, however, we are taking this step to give customers added peace of mind during what is a very worrying time for some," ASB CEO Vittoria Shortt says.

The ASB move follows a similar no forced sale initiative from its parent Commonwealth Bank of Australia (CBA) last year.

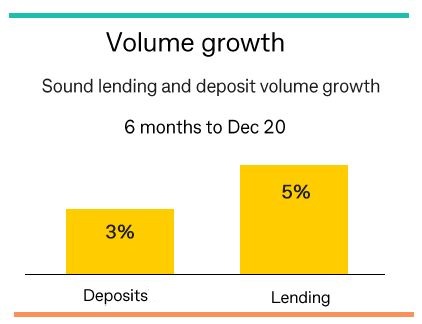

ASB posted an $18 million, or 1%, rise in half-year total operating income to $1.416 billion, with net interest income up $40 million, or 4%, to $1.110 billion. Total operating expenses were cut $16 million, or 3%, to $518 million. Loan impairment losses rose $8 million to $30 million.

Strong home loan growth in red hot market

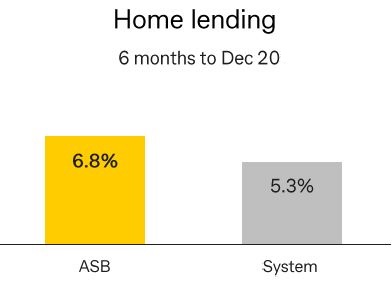

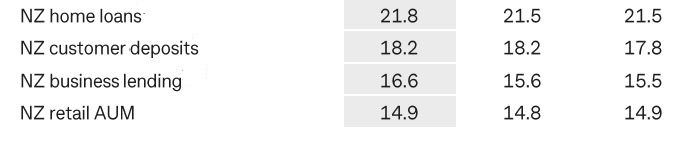

ASB's total loan provisions were $604 million at December 31. That's against gross loans of $95.5 billion, of which $65.8 billion, or 69%, are home loans. Figures from CBA show ASB grew home lending faster than the overall red hot housing market during the six months to December 31, and increased market share to 21.8% from 21.5%.

"We remain confident about New Zealand's ability to remain resilient to the challenges of COVID-19, but the past 12 months have taught us all to expect the unexpected. That is why we have made a conscious decision to continue to provision for the uncertainties surrounding the pandemic and its possible long-term effects," Shortt says.

The tables and chart below come from CBA and cover ASB.

ASB market share percentage Dec 2020 June 2020 Dec 2019

AUM is assets under management.

In terms of key financial performance measures, ASB's return on equity fell 70 basis points to 14.9% from 15.6%, its net interest margin fell six basis points to 2.09%, and its cost to income ratio rose 60 basis points to 37.1% from 36.5%. ASB's common equity tier one capital ratio, as a percentage of risk weighted exposures, rose 50 basis points to 12.2%.

Meanwhile, the CBA group posted an 11% fall in interim cash profit after tax from continuing operations to A$3.886 billion. CBA's net interest margin fell 10 basis points to 2.01%, and its fully franked interim dividend dropped 25% to 150 cents per share, a payout ratio equivalent to 67% of cash profit. CBA's common equity tier one capital ratio rose 90 basis points to 12.6%. The group's loan impairment expense was 36% higher at A$882 million.

45 Comments

"There will be no forced sales of owner-occupied family homes in 2021 for ASB customers we are working with to resolve the challenges they are facing. Mortgagee sales are uncommon, and they are always the last resort, however, we are taking this step to give customers added peace of mind during what is a very worrying time for some," ASB says.

How long can this temporary stay of charitable accommodation last? - ASB shareholders will demand answers. So should we.

CBA share price

https://www.commbank.com.au/about-us/investors/share-price.html

"Irrational exuberance" - to quote Greenspan.

Equities, Real estate, gold, bitcoin everything is up. Is this the beginning of a crack up boom? https://www.investopedia.com/terms/c/crackup-boom.asp

You say crack up boom, I say MMT. [sarc]

Seems to describe the current situation to a tee:

Von Mises describe the process later in his book Human Action. "[I]f once public opinion is convinced that the increase in the quantity of money will continue and never come to an end, and that, consequently, the prices of all commodities and services will not cease to rise, everybody becomes eager to buy as much as possible and to restrict his cash holding to a minimum size," he said. "For under these circumstances, the regular costs incurred by holding cash are increased by the losses caused by the progressive fall in purchasing power."

The school of hard limits:

A crack-up boom is something that can only happen in an economy that relies on fiat money (in either paper or electronic form) and (usually) fiduciary media, as opposed to the gold standard or other physical commodity money, because the available stock commodity places a physical limit on the quantity of money that can be issued and the market discipline imposed by a convertible gold standard helps prevent the overissuance of credit. In the event that they ever become money, electronic cryptocurrencies whose underlying algorithms place inflexible limits on the quantity and rate that new units can be created (or mined) may provide a similar benefit of preventing hyperinflation and a crack-up boom.

此地无银三百两。

What you said only gave yourself away.

Faszomért kell kínaiul írni ide te paraszt.

(Can we keep the discussion in English please?)

What ? - are you objecting against use of Te Reo ?

You can't call people paraszts!

Actually right click and translate to English. I think it's kind of fun.

Property value is soaring. No point for banks to pursue Mortgage sale early.

Those that sell first, sell best.

The key words are probably, for ASB customers we are working with

Refuse to work with them and a forced sale would be likely I would imagine.

That makes sense. Otherwise why would anyone pay their mortgage? What are the penalties and penalty interest rates like in most mortgages?

Recent considerable increases in house prices over the past few years would give those with mortgages greater equity so if having trouble meeting current payments, then ASB will have great confidence in recouping the loan (plus high penalty interest) if forced sale does eventuate.

The high penalty interest and customer equity means there really is no urgency to force a sale. The cynic in me says good business practice by ASB more so than a social conscious.

I doubt we would see this concession in the current Covid economic situation in a falling or even flat housing market. Maybe it’s just because I am always cautious of motives and believe that in business we primarily act in self interest.

"There will be no forced sales of owner-occupied family homes in 2021"

Forced Sale? Who's even mentioned that recently? And if ASB is highlighting the topic now, why?

The answer to all the above is obvious - because there are problems present or lurking.

But not to worry!

At a helping-hand concessional Interest-Only 0% mortgage rate, the current 'owners' can sit pat indefinitely. It cost no more to finance a million dollars distressed debt at 0% than it does a $50,000,000 one. It's the gross loan book that matters, and other mortgage holders can chip in a dollar or two so the distressed can get their concessional rate, from somewhere else in their banking relationship.

And if the current resident keeps up their 'payments' at 0%, then it doesn't even have to be qualified as a Bad or Doubtful Debt on the banks balance sheets.

A Win/Win for all concerned.

Bang on. Maximising profit dressed up as charity. Why hurry, just gobble up the equity with penalties - much more profit this way.

The forced sales will come when the bank has sucked out the maximum.

I also love how all the banks dressed it up during Covid as 'financial assistance'. Really. I didn't see anybody actually getting money out of a bank for nothing. It's all just deferred to some point down the line.

There’s no such thing as a free lunch.

Except if you are reaping capital gain based solely on non-value-added growth, ie most of what is the increase in property capital growth.

Unless you’re a bank

ASB is promising not to force the sale of any ASB customers' owner-occupied homes this year......owner occupied.

Heh. $9 billion in November, what a leap! I guess that's the delay due to post lockdown house hunting -> offer -> accepted -> loan drawdown.

Good PR stunt.

This is one hell of a signal to choose to send at this time.

Keynesian ethics: "we won't take away the rum."

Why make people payoff the mortgage? Why make them sell if you can keep them working for the bank the rest of their life?

The whole point is as long as you can keep feeding the system, just like GYM memberships.

Surprisingly I honestly don't think most people understand this concept. Used to be that cash was king, now sales people in most places are incentivised to sign a deal of some sort, with little or usually no discount for cash.

I think you're probably closest to it, but I agree with pretty much everyone here. What superficially looks like a socially responsible policy, will certainly have fishhooks in it for their customers which may ultimately be quite nasty. Having said that the bank gains more in the long run by not being too greedy in the short term and helping those who are struggling through the storm. As to 'Penalty interest Rates', do the trading banks apply those? I know the IRD does with a severe impact, but apply them to a mortgage and you could push a customer into insolvency and lose it all. Not to mention the bad PR that would bring.

Yeah I would like to know what the typical penalties and penalty interest rates are too! Perhaps it's time to actually read the document I signed D:

But if you are an investor that has trouble finding tenants and making payments in our population new normal. The Reserve Bank (government) will be actively encouraging ASB and other trading banks to wind you up. The prices have been pumped to a sufficient level now to ensure the banks won't loose. But the investors may loose some of their paper capital gains. More stock into the market to "level the playing field for FHB's".

Watch out for lifts in the price limits for FHB grants and Welcome Home Loans. Fine balance to transfer some existing stock from investors to FHB's without prices rising beyond the acceptable annual magic percentage in the minds of Ms Adern and Mr Robertson.

Why would you have trouble finding tenants if there's (supposedly) a house shortage?

Maybe because from Aug 2020 up to today NZ departures 93757 and arrivals 77257. Net loss of 16500 people. Pure tourism is pretty much excluded from these stats due to covid restrictions . Meanwhile new dwellings being completed at an accelerated rate all over Auckland. Eventually we run out of people who can afford to live in these dwellings. If we can't restart immigration and tourism.

Yep, my comment was a bit sarcastic (hence the 'supposedly'). This year is solid proof that supply is not the issue, despite what the average kiwi was led believe. Immigration the lowest ever, following 3 years of records high new builds, yet prices skyrocketing.

I'm not gonna shed any tears for landlords, there is no risk-free investment. It's just sad that govt and RBNZ don't share that sentiment.

You dont need people to live in them, you can sell them to overseas investors who leave them empty.

Why would they force the sale when the Government is now paying people's mortgages for them?

https://www.stuff.co.nz/business/money/300187304/more-homeowners-seek-g…

Does this mean the RBNZ can start raising interest rates?

There's little reason to sell something that's rising in value.

Banks will not foreclose on any NZ houses unless they fall into the 'hardcore' category.

Great marketing team they have there- sizing the opportunity to do some social marketing.

I have been though multiple down times over the years. Yes they are right they have always been loath to go to a mortgagee sale. I have however seen a number of property owners called in and told to list their property sole agency and sell at the best price they can get.

Is this recently?

Kashin the Elephant likes this

Well, hopefully they shaft the investors then.

Typical bank. Giving out umbrellas when the sun is shining.

When the market is roaring at full blast the bank becomes all loving and generous knowing that few mortgagee sales will occur.

Let’s see if they are just as generous when the market hits the wall.

This used to happen but doesn't seem to happen any more.

If we get so much as a hiccup in the property market the RBNZ and government spring into action to save the day.

Banking is the best business ever you just tweak numbers to increase your profits. There now appears to me to be an ever increasing gap between the TD rates and the mortgage rate. Yep you don't have to make anything, stock anything or worry about it expiring just play with the numbers. Home owners don't care if the banks are making more profits because their homes are going up in value, its just one big psychological money go round which works really well on the way up, its the possible way down that worries me.

It must be the best business to be in because when they loan out money, they create most of it out of thin air. And then charge interest on it. How completely fantastic is that?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.