The Reserve Bank (RBNZ) acknowledges its proposal to tighten bank lending restrictions from October 1 will hit first-home buyers the hardest.

The RBNZ last month proposed allowing banks to let a smaller portion (10%) of their mortgage lending to owner-occupiers go to borrowers with relatively small deposits of less than 20%. Currently, 20% of mortgage lending to owner-occupiers can go to this riskier cohort of borrowers.

The banking regulator on Friday released a consultation paper seeking feedback on its proposal.

It made the case, intervention is needed to prevent first-home buyers in particular from stretching themselves too much to buy increasingly costly houses, ultimately putting themselves and the financial system as a whole at risk.

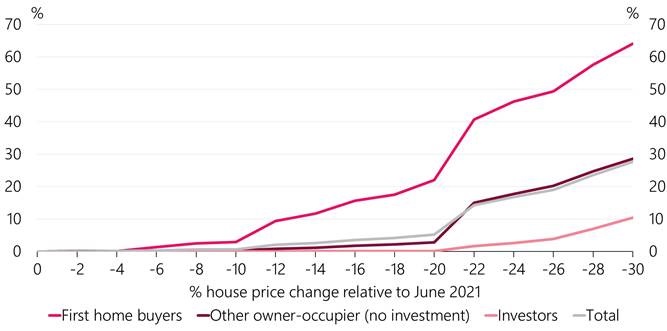

It estimated that if house prices fell by 20%, around 5% of new mortgage lending issued in the year to June 2021 would be in negative equity.

Whereas around 22% of new mortgage lending to people who bought their first home in this time would be in negative equity. That is, they would owe the bank more than what their property is worth.

The graph below shows the portion of new lending in the year to June 2021 that would be in negative equity at different levels of house price falls.

The RBNZ explained: “Growth rates of house prices in the last year mean that households that already owned homes built up balance sheet resilience through large gains in the value of their equity.

“Recent movers and investors have benefited from the equity gains on their previous properties, whereas recent first-home buyers have come into the housing market with less purchasing power and have generally needed to borrow at higher LVRs, and hence are more vulnerable to price falls.”

FHBs effectively the target of tighter restrictions

While the RBNZ isn’t explicitly proposing to create new LVR rules for “first-home buyers” as such, it recognised this group would effectively be targeted by it tightening existing rules for all owner-occupiers.

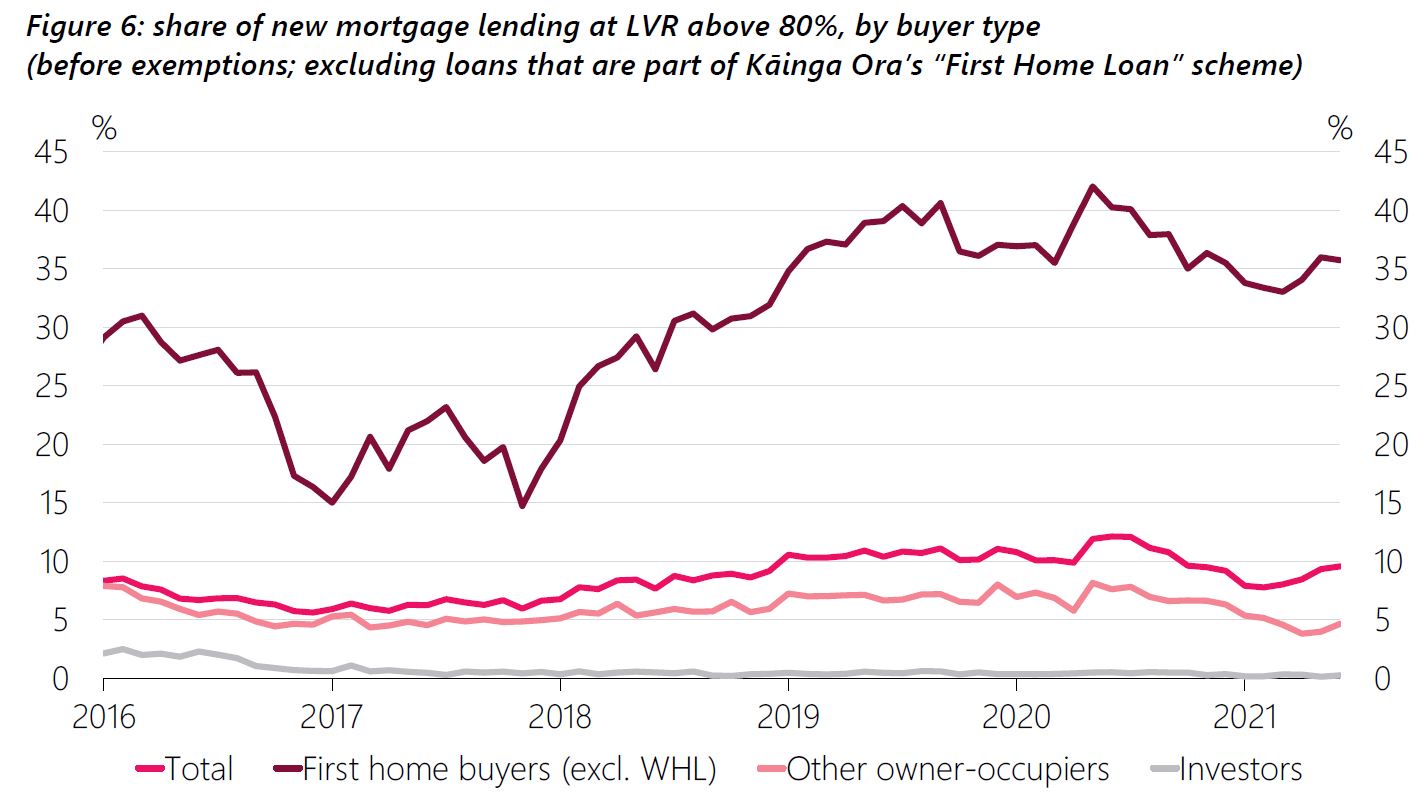

It said banks tend to use up their high-risk, or high-LVR, lending allocations on first-home buyers.

For example, around 35% of new bank lending to first-home buyers is to those with deposits of less than 20%. Meanwhile, less than 5% of new lending to other owner-occupiers is at this level (at LVRs of above 80%).

Economy-wide risks

The RBNZ stressed its job is to consider the strength of the financial system as a whole, not control house prices.

“Financial system resilience is starting from a strong base, but without action the outlook is expected to deteriorate over time,” it said.

Commenting further on the risks associated with negative equity, it said: “A high proportion of lending in negative equity does not on its own imply that banks would face credit losses, but their portfolios would be significantly more vulnerable to a servicability shock - for example, a rise in unemployment - whereby customers with negative equity who cannot service their debt default on their loans.”

Because so much of New Zealand households’ wealth is tied up in housing, the RBNZ also noted a fall in house prices would cool the economy more broadly. It said a 20% decline in house prices would reduce New Zealand households’ total wealth by more than 10%.

The RBNZ also said its research suggested New Zealand homeowners are more sensitive to house price falls than rises. Households cut their consumption if house prices fall by more than they increase consumption if house prices rise (3 cent consumption increase for every dollar rise in house prices).

Serviceability to be addressed via new restrictions

The RBNZ said New Zealand is even more sensitive to the impacts of a housing correction because households have taken out so much debt.

Mortgage rates are currently low, but the RBNZ recognised, “A large share of New Zealand mortgages are on a short-term fixed interest rate, putting a large share of borrowers at risk of sharp increases in mortgage costs, if interest rates rise before they next reset their fixed term…

“Recent first-home buyers would be the primary group to experience serviceability stress, as they typically have lower incomes than other borrowers, and therefore need a greater share of their income for living expenses.

“Investors are the second most likely to experience serviceability stress overall.

"Existing owner-occupiers are less likely to experience serviceability stress but it should be noted that these borrowers represent the largest share of the market.”

The RBNZ said it would start consulting in October on introducing bank debt serviceability restrictions.

Finance Minister Grant Robertson last month gave it the power to use such restrictions, which could require borrowers to have a certain amount of income relative to the debt they’re seeking, or require banks to ensure borrowers can meet repayments at set interest rates above existing rates.

“The LVR tool is better suited to mitigating the risk of negative equity in borrowers, while a serviceability tool should be better at building borrowers’ buffer against serviceability shocks, such as an interest rate rise,” the RBNZ said.

Lending to investors doesn’t need to be reined in more

While the RBNZ proposed tightening LVR restrictions by shrinking the portion of lending banks are allowed to do to borrowers with deposits of less than 20%, it also considered increasing the size of deposits most borrowers need to have to 25%.

However, it didn’t favour this option, in-part because it would affect a lot of borrowers, who only just manage to meet that 20% deposit threshold.

The RBNZ also deemed it unnecessary to further target investors. As of May, 95% of banks’ mortgage lending to investors has had to go to borrowers with deposits of more than 40%.

The RBNZ noted the Government is now also taxing investors more by removing their ability to deduct interest as an expense and extending the bright-line test.

Following these changes, there has been a significant reduction in both the share of overall lending for investment purposes and the proportion of investor lending at high LVRs.

“Therefore, the current evidence does not show new lending to investors as contributing to financial stability risks,” the RBNZ said.

42 Comments

May as well just lend more then to the already wealthy and there will be no problem at all! (sarc)

Well that is pretty much the Labour Govt housing policy isn't it? Only those wealthy enough to have 40% cash deposits, or have 50-60% equity in their home are eligible to buy an investment property now. The days of the average Joe buying a rental property as a means of saving for their retirement, or the First Home Buyer buying a rental in a cheaper area just to get on the ladder, has gone out the window and investment properties are now only for the cashed up, existing property owner.

Yes I am not sure why Labour is working so hard to help all the rich people with lots of houses and high income and equity. I guess they want to keep everybody poor so they vote for them like lambs to the slaughter, is that called Communism or Socialism, I get confused as to which one they prefer, one has a country of serfs and the other has a country of peasants ?

At least National tried to get house prices down.

Everything Labour does is pooring petrol on to house prices and rent prices.

At least under National someone had a chance of getting ahead.

The banking regulator on Friday released a consultation paper seeking feedback on its proposal. It made the case, intervention is needed to prevent first-home buyers in particular from stretching themselves too much to buy increasingly costly houses, ultimately putting themselves and the financial system as a whole at risk. It estimated that if house prices fell by 20%, around 5% of new mortgage lending issued in the year to June 2021 would be in negative equity.

Mr. Soros does recognize that China’s “most vulnerable sector is real estate, particularly housing. China has enjoyed an extended property boom over the past two decades, but that is now coming to an end. Evergrande, the largest real estate company, is over-indebted and in danger of default. This could cause a crash.” By that, he means a reduction of housing prices. That’s just what is needed in order to deter land becoming a speculative vehicle. I and others have urged a policy of land taxation in order to collect the land’s rising site value, so that it will not be pledged to banks for mortgage credit to further inflate china’s housing prices. Link

Good grief Stephen, Counterpunch is a well-known anti-Semitic Russian troll site. Please don't link to such propaganda

David, all you find against Counterpunch does not necessarily apply to Michael Hudson , author of the article claiming:

I and others have urged a policy of land taxation in order to collect the land’s rising site value, so that it will not be pledged to banks for mortgage credit to further inflate china’s housing prices.

The same article is hosted by other websites with different hues and views, including michael-hudson.com.

I and many others found fortunes cornering sovereign bond markets from 1982 onwards with funding secured by collateralised repurchase agreements. Hence the economy is starved of credit for productive GDP qualifying endeavour - read more.

Surely though, on Net, it's better for society to have people being homeowners than not? Homeowners live longer and healtheir lives, are less likely to commit a crime or take drugs, are more financially secure in retirement, pay more tax, have higher levels of income growth etc. They tend to be the the citizens you'd want if you where designing a model society.

The Reserve Bank should actually be targeting increasing home ownership rates if it wants to create a financially safe and prosperous country.

Surely better to focus on why renters have lower life expectancy, commit more crime etc. Renting shouldn't be just for those that can't afford owning ("reluctant renters").

"are less likely to commit a crime or take drugs" - so home owners don't drink.?

Correlation v causation

All it highlights is that houses need to fall relative to incomes to ensure financial and social security for the country going forward.

But we don't want to face that reality as it might be a little bit painful and we want to avoid pain at whatever cost possible.

Correlation does not prove the direction of causation.

Have been highlighting that DTI is must to protect FHB from overstreching themselves under FOMO to buy a house.

Not able to buy a house is frustrating but buying under FOMO than repenting if the situation changes even slight will be a disaster.

FHB particularly in Auckland should give up as this B@#$% have killed the aspiration of hard working Kiwi.

Along with DTI, this a....holes should also increase lvr for invedtors from 40% as exceptional situation requires exceptional measures.

Thanks Jenee for the interview with that gentelman and exposing him with his true intent. Again such people should be paraded na.... on the street and..........

Lament for Young House Hunters by a Sympathetic Babyboomer

The young today just want a house,

‘That’s all we want’ we hear them grouse.

‘All we want is our own home

No matter if it’s out of zone’.

The young just want to know the cause

Why I’ve got mine and you’ve got yours.

They want to see their income spent

On anything but landlord’s rent.

They see the ‘boomers buying them up,

At auction they have had no luck.

The immigrants have bought the rest

But it’s ‘we who want a place to nest’.

The price of houses keeps on rising,

Rate of increase most surprising.

Market shows no sign of cooling

Mr Barfoot’s lips are drooling.

I've literally been saying it for 4+ years; "Labour want house prices to increase".

Government policy will change when it's more uncomfortable for Ministers to maintain the status quo than enact wide reaching change.

It's human nature to choose the path of least resistance, it takes a leader to forge a better path.

Social housing in NZ is looking more and more communist by the day. Social housing tenants are certainly living in the fruits of FHBs.

Indeed, and we do not have leaders. We have caretakers to the status quo.

We have caretakers to the status quo.

Because they do not possess any vision for the country beyond the superficial. I don't believe that NZ can make any meaningful change because there's not enough desperation among those who enter the political realm. They all seem to be biding their time for something better to come along like an overpaid position at the UN with a plush apartment.

The political class come from those in society who have benefitted from the current economic model, naturally they will do nothing that threatens the status quo.

'Labour want house prices to increase"

Care to back up that statement with hard evidence? You can fault them for failing stabilise housing prices but you can't fault them for not trying. Look at the list of things they have put in place since being elected.

o Lifting LVRs for investors

o Removing interest deductibility for property investors

o Banning foreign buyers

o increasing the bright line test

Name a party that has done more.

If the last 4 years have taught us anything it's that even the experts haven't been able to crack this nut. As an earlier comment stated, the only real solution is for wages to rise and house prices to drop. The first government to accomplish this will be voted out by homeowners and investors who think there is some magical solution this problem that will allow them to keep their gains.

First home buyers will fall away anyway. Because of growing unaffordability and because it's effectively impossible to build a 2 bedroom townhouse in Auckland and sell it for no more than 700k - which is the Homestart cap.

They? Labour?.. want to make it harder for first-home-buyers to own property - citing the risk of 'negative equity'.. yet they say they're wedded to continued house-price-inflation.

I think interest.co.nz readers are smart enough to recognize how incongruent that is to FHBs EVER owning real estate.

Property ownership is a historic separator between those whom are free and slaves. Notice the ever increasing government exploitation of the building sector to bolster their property portfolio? They were (clandestinely probably still are) buying properties in the private market - ACTIVELY using the government's balance-sheet to compete with FHBs.

What I'm about to say might sound hyperbolic and extreme:

Powerful people in the government? Labour? Who knows; but it would seem they don't want younger generations to own property and as older generations die out; Labour want to normalize a communist system of government and property ownership.. ownership which is not ownership.

Labour members and their acolytes do refer to each-other as "Comrade" and often self identify as "Marxist" and/or "Socialists". PM Ardern was high up in openly Marxist movements before becoming PM. At a certain point you have to acknowledge what's in front of you?

I aim to avoid the Gulag myself, fingers crossed lol

You're right about the obviously contradictory nature of Labour's statements and policies, but then go wildly off-track.

The Labour Party is *not* run by socialists. There is no evidence that they want to nationalise property -- on the contrary, they're allowing it to be concentrated in a diminishing number of private hands. It's monopolistic capitalism, not communism; it's precisely the situation that communism (and the Labour Party) were invented to militate against. Probably the best description of them is that they *want* to be socialists, but are very very bad at it, because they just want to be liked; and if they do anything to make property owners unhappy, people will say mean things about them.

I'm thinking more in terms of socialist oligarchies like Russia and the later-stages-of the USSR.

Labour's policies and socialist ways are pernicious and dangerous. Waving it off as Labour not wanting to be big meanies will prove to be detrimental and naive.

Labour's policies concerning housing divide along generational lines and prevent social mobility, foment discontent and present it through an "US against THEM" lens.

Marxist ideology is all about achieving power through propaganda and civil unrest. Capital investment and good stewardship are sacrificed on the alter of money-printing and unionism respectively.

A good housing market allows people to progress from say.. renting a house, to owning a house, to building a house, to maybe larger property development. Clearly this social mobility is not a thing in NZ anymore. People often struggle to rent, let alone purchasing property.

As Labour's policies trickle down, the concentration of wealth will intensify. Once socialists achieve power, their response to social issues and the countries maintenance is to write cheques to the oligarchs and their companies. The education system is of course infiltrated and purged of opposing ideas. Opposition, often by their former supporters [card-carrying-communists] is cracked down on hard.

Good Luck.

I remember saying this in 2013 when my daughter was trying to buy her first house - "Don't worry, they'll eventually run out of people who can't afford to buy at those prices, or are not willing to pay so much for rundown houses". I didn't think it would take so long! She was very lucky that she managed to buy what was probably the last house on the shore for under $500K.

FHBs are better off avoiding the whole scene now, at least in Auckland. Every crack-den owner has a million dollars in equity, the bank will throw money at them to buy another for a mil and a half... now that the dynamic is in play I see no reason why the median shouldn't go to $2m, $3m... nothing in the Reserve Bank's playbook prevents it. It's like the modern sharemarket, yield doesn't matter anymore. There'll always be someone there to buy it off you for more.

Agree but no economy is one way street and gets bump along the way be it stock market or house market specially now.

Jerome Powell might be the only reason the market isn’t eating itself in USA ......rest of world follows.

Jerome Powell making his speech the same day as the Supreme Court lifts the evacuation moratorium seems super planned. Feel there been so much discussion about a super correction or a market crash cause of the fear of inflation and I think the only thing stopping that is Jerome Powell periodically coming on tv and stopping the fire from spreading. Like he is literally running around throwing buckets of water at people to shut them up and spilling water into YouTubers computers to stop them from posting.

Similarly following fed our dear Orr is coming out to support and promote the housing ponzi as in NZ only economy is housing and not much stock market to manipulate.

But For how long.

Reserve bank governor in many developed countries like Mr Orr are trying to imitate fed, not realizing that US economy is diverse and massive unlike NZ. Housing bubble is bad for any economy but more so for small country where now only economy is housing.

Debt to income ratios will prevent that. A tool they have finally been granted, but not yet rolled out.

Robertson will unfortunately have his hands tied and not be able to be seen intervening at all because it's home buyers and not investors this time. The independence of our central bank is sacrosanct as we all know.

I think that first home buyers should be saved from themselves. But investors should have rules specific to them which are even harsher. Harsher rules around reducing the term of mortgages back to 20 yrs, loan to income, loan to value ratios, do away with interest only etc should all be gradually brought in. This will cause a drop in house prices but will insulate people from their own selves. Especially reducing the term of the loans. And not allowing interest only except under temporary Wuhan virus type situations. These measures will reduce the duration of the early period where it is mainly interest on the loan which has been paid. If it quickly goes into the principal pay down phase, that is where people can start to rest easy and know that negative equity will not happen.

It will be interesting to see if the govt will increase the Homestart cap in Auckland, from 700k to 750k.

Until Covid hit, Homestart approvals were hitting around 4000 per annum, so they have been a big part of FHB activity, and also a significant driver of townhouse construction activity.

Due to land, labour and building cost escalation in Auckland, it's now almost impossible to build and sell 2 bed townhouses for less than 730-750k. You won't see many new 2 bed townhouses marketed for sale below 720k - that reflects these cost realities.

So Homestart is stuffed.

This is why I expect to see:

- FHB buying activity fall away

- new dwelling rates decline

You heard it from HouseMouse first...

So I reckon the govt will increase to 750k, although as I say that's even hard for developers to hit.

Of course an unintended consequence of raising the cap again is that it pushes the price floor higher again...

Also, it becomes a bigger stretch for households earning no more than 150k to finance the larger mortgage, especially as interest rates nudge up.

oh well

A little bit late to care about FHB's... They locked in new FHB's to sky high mortgages through FOMO & locked out future FHB's through sky high house prices.

Starting to think my idea of deliberately crashing the market and providing the chance for FHBs still living in their first home to refinance at 0% interest to help them work back from negative equity isn't as dumb as it sounds.

I'm kind of with you on that. I think the only problem is that any government that deliberately crashes the market will be voted out in the next election by those who own homes. My theory is that we all want the housing crisis solved.....right up until it impacts us.

It's a bit like taking a watering can to the roaring forest fire, after it's already passed and scorched the earth. At least you can say I tried to put it out. I wonder if they realise that the fire will spread up the hill to their castle in time.

Need a event to shake the the political class and they being thick skin shameless... hoping is not violent.

Investors....I mean speculators have been biting off more than NZ can chew for years. But that's ok...?

Hyperinflation to protect printed debt seems now to be the no1 govt policy. No one voted for that, and its certainly not in the publics interest to continue to get screwed by ever increasing rent. Rent to service endless debt that flow thru to inflate the cost of everything. As it continues against the general public's interest, and successive Governments turn a blind eye to it, one gets some insite into how the extreme political agendas have been voted into power over the course history.

How will it end?

Less competition, I think it's shit for FHB but I'll buy a couple more than I guess. Up down doesn't bother me, 10 years time they will be worth plenty more. Thanks labour. I don't vote for you but you buy maybe I should haha

https://www.cnbc.com/2021/08/27/housing-price-bubble-will-wipe-out-weal…

In US house prices have gone up by 15% and are panicking but here is more than 30%. Also US has big and diversify economy unlike NZ where economy is much small and that too only focused in housing.

Soon blame game will start...Robertson and RBNZ

Hard to directly compare the USA and NZ property market, the USA has so many problems. Just look at all those that drowned in their basement apartments in new York recently. Not only is that type of dwelling illegal but they don't even know the number of those apartments. Totally different bank lending system that has already collapsed once and they have not fixed it so it could collapse again. The USA now getting smashed by climate change, they have plenty to worry about.

I predict this will be a boon for non-bank lenders. The RBNZ isnt eliminating the problem, its just moving the risk from one group to another.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.