Questions are being raised over whether there is any real need for the Reserve Bank (RBNZ) to tighten bank lending restrictions, effectively aimed at preventing first-home buyers from doing too much high-risk borrowing.

The RBNZ is consulting on its proposal to halve, to 10%, the portion of bank lending that’s allowed to go to owner-occupiers with deposits of less than 20%.

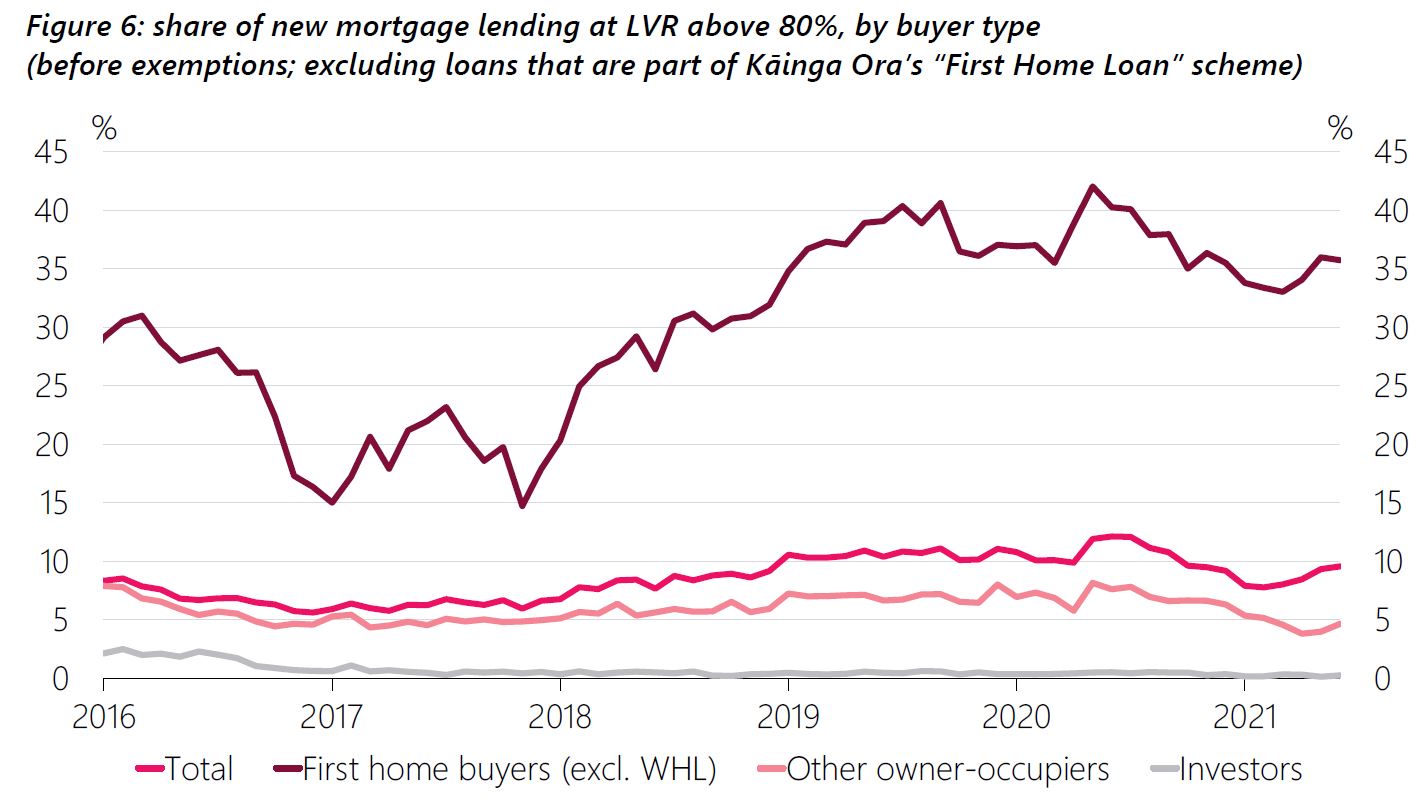

Currently, first-home buyers make up much of banks’ ‘high loan-to-value ratio (LVR) lending’ allowance, so will be hit hardest by the change, proposed to take effect on October 1.

While the RBNZ makes the case that first-home buyers are more at risk in the event of a property market downturn, its data suggests they aren’t putting the stability of the financial system as a whole at risk.

“If there is a compelling financial stability case, it isn't made in this [consultation] document,” Michael Reddell, who formerly held a number of senior roles at the RBNZ, wrote in his Croaking Cassandra blog.

He accused the RBNZ of being overly paternal in its attempt to save first-home buyers from themselves.

“It all just has the feel of more action for action's sake,” he said.

CoreLogic’s head of research, Nick Goodall, likewise questioned whether tightening LVR restrictions was absolutely necessary.

The data

The RBNZ acknowledges LVRs are suited to mitigating the risk of borrowers getting into negative equity - that is, a borrower leaving their bank exposed by owing it more than their house is worth.

Data provided to interest.co.nz by the RBNZ shows that of the mortgages issued in the year to July 2021, $600 million of these would be in negative equity if house prices fell by 10%.

That’s equivalent to 1% of the mortgage lending done in that year and 0.19% of the stock of all mortgage lending, valued at $315.9 billion as at July.

If house prices fell by 20%, $5.1 billion of mortgage lending done in the year to July would be in negative equity. That’s equivalent to 5% of mortgage lending done in that year, and 1.6% of all mortgage lending.

And finally, if house prices fell by 30%, $27.1 billion of mortgage lending done in the year to July would be in negative equity. That’s equivalent to 28% of mortgage lending done in that year, and 8.9% of all mortgage lending.

While Reddell noted these numbers weren’t high, the RBNZ made the case that first-home buyers would be hit much harder if house prices fell.

For example, a 10% fall would see 3% of mortgage lending to first-home buyers in the year to July in negative equity.

A 20% fall would see 22% in negative equity, and a 30% fall would see 64% of mortgage lending to first-home buyers in the year to July in negative equity.

Are banks really that exposed?

However, Goodall said there was a low likelihood of A. House prices falling by more than say 10%, B. First-home buyers being in negative equity, and C. Enough first-home buyers losing their jobs and not being supported by their banks to help them hold onto their homes to the extent this puts the banking system at risk.

Reddell said the RBNZ pointing to first-home buyers being more exposed was “hardly news”.

“The typical first-home buyer has always - at least in liberal financial systems - borrowed at least 80% of the value of the home they are purchasing. It is usually sensible and rational for them to do so (indeed 90% would often be sensible and prudent),” he said.

“If I borrowed 82% of the value of the house, the house fell in value 20%, and I lost my job and had to sell up, the loss to the bank might be not much more than 2% of the loan.”

RBNZ typically doesn’t back down

Goodall said he could see how the RBNZ could justify its proposal based on the fact the share of high-LVR lending to first-home buyers is increasing.

However, Goodall suspected the proposal “won’t be met with very much positivity” by submitters.

Goodall said the RBNZ typically didn’t back down.

“But you just never know, depending on how compelling the feedback is,” he said.

“There’s no doubt the RBNZ is much more concerned about where [house] prices are at than the Government is.”

Reddell maintained the RBNZ wasn’t really interested in taking feedback on board, with the change proposed to take effect less than two weeks before the two-week long consultation ends on Friday.

“With that sort of urgency and disregard for any serious bow in the direction of consultation and reflection, you'd have to assume the Bank had a compelling case for urgent action,” he said.

“But there is nothing of the sort. Instead, they are actually at pains to stress that the financial system is sound at present, so the worry is about what might happen if things went on as they are.”

Robertson comfortable

Interest.co.nz asked Finance Minister Grant Robertson whether he was comfortable with the RBNZ effectively trying to protect first-home buyers from themselves, when the data suggests they aren’t threatening the stability of the system as a whole - for now.

Robertson said the RBNZ’s job in terms of managing financial stability was an “overall systems one”.

“But they will inevitably look at particular groups, because it is important,” Robertson said.

“I think the Reserve Bank’s role is both a macro one, but also to look at individuals.”

Effect of Govt’s instructions to the RBNZ questionable

Robertson was also quick to point out that he hadn’t put the same parameters around the RBNZ using LVR restrictions as he had around it using debt-to-income restrictions.

Robertson last month agreed to give the RBNZ the ability to apply debt serviceability restrictions on banks on the proviso the RBNZ has “regard to avoiding negative impacts, as much as possible, on first-home buyers".

Nonetheless, Robertson in February issued the RBNZ with a directive, requiring it to have regard for the “Government's housing policy” when carrying out its job maintaining financial stability, including setting LVR restrictions.

The “Government’s housing policy” is to "support more sustainable house prices, including by dampening investor demand for existing housing stock, which would improve affordability for first-home buyers”.

Reddell concluded, “Perhaps the Government isn't too keen on first-home buyers being squeezed out. But at least when they are criticised for not fixing the dysfunctional over-regulated housing/land market, they can wave their hands and talk about all the things they and their agencies do, however ineffectual.

“As even the Bank notes, LVR restrictions don't make much difference to prices for long.”

For more on the RBNZ’s case for tightening LVR restrictions, see this story.

38 Comments

I used to work with a guy that bought his first home in I think Minnesota for about $150k around 2007. His equity was maybe $10k. A couple of years later the value had fallen to $100k, plus he had lost his job there and had to move away. He was in negative equity of something like $35k at this point. Fortunately for him, it was a non-recourse loan and despite his bank chasing him for repayments he walked away and only lost his deposit and repayments, maybe $20k.

If the same thing happened in NZ today, he would be in a massive pile of the proverbial, because the house would be something like $600k+, his deposit maybe $100k, and negative equity $100k+. We don't do non-recourse loans here so he'd have lost his deposit, all the repayments plus be on the hook for $100k+. Bankruptcy would likely be the only viable option.

I'm glad RBNZ is aware of this risk and how devastating it can be to an individual, because from what I can tell most first home buyers aren't.

USD20K. Chump change.

Yip I was living in the US during the GFC - it was pretty common place for the younger people I was working with to be in negative equity. The stress levels were insane as they knew they couldn't afford to lose their jobs but then at the same time the economy was terrible and companies didn't want to fire people but knew that if they did fire people, they wouldn't get hired anywhere else and they would default on their mortgages. It was a real #%#@ place for people to be - but yet, where we find ourselves in NZ with respect to property, would make the US property bubble seem like a walk in the park...

I fully understand both sides of the argument here. However, I am still puzzled as to how this will collapse if the RBNZ and government hold it afloat or so it seems.

In this COVID scenario, the government has paid people to substitute lost income thus backstopping a mortgage repayment crisis.

I feel its a certainty that this step will be taken again.

The RBNZ will also go negative if/when needed .. they are pretty adamant of that a few months ago.

Please help me understand this better.

You understand well already

Yep, mortgage holidays and money pumping to infinity every time prices are off by more than 5%.

Noone will be allowed to take a loss, ever.

Pretty much. Its is far more important that a life time of debt enslavement to printed money be protected at all costs. Not that anyone voted for this.

A point often overlooked is negative equity does not require a Bank to forclose so if repayments are maintained the Bank will do nothing and in a climate of few sales how do you know the value to determine negative equity.Becoming unemployed and defaulting is a different and frightening situation which looks like playing out in China if Evergrande fails and is not bailed out by CCP, there is already social unrest at the prospect and hedge funds are bailing out of Chinese debt, could this be a Lehman moment repeated?????

What, exactly, is a "more sustainable house price". How does something get worse, but also more sustainable at the same time?

Maybe Labourthide could translate the Labour newspeak for us?

Brock - you need to improve your capacity for doublethink and if you don't, the thought police will be after you!

As it stands, you're guilty of thoughtcrimes. I trust that you watched the ministry give its daily update and cheered at the success the ministry is having on the war against COVID.

If you want a picture of the future in New Zealand, imagine a landlord stamping on a human face - for ever.

Think we're already there - but who gives a toss, the proles don't care!

I wish someone from the press would ask him and JC that question? Its utter bollocks. There is nothing sustainable about the how price growth that has been occurring

Jenee has attempted a few times.

But they are slippery buggers that will waffle and laugh their way out of giving a real answer.

It doesn't really matter. We know they are full of it. They know they are full of it.

Cheers. And yes, I asked Robertson about this a couple of weeks ago: https://www.interest.co.nz/index.php/news/112066/finance-minister-grant…

Personally I think this misses the whole point. FHBs going into negative equity is only part of the problem. The aggregate effect across the economy of 'feeling less wealthy' is the big unknown and hasn't been / can't be modelled by RBNZ or the banks. That is where the stability of the financial system lies: the extent to which people tighten their belts due to declining asset prices.

How about nearly half the population that are feeling less wealthy as house prices march over the horizon, give up trying and striving, and we slide further into the growing underclass of unmotivated unproductive people. In the present set up, if you are young and are going to stay in NZ, you have no future to hope or strive for. Little wonder that so many are joining gangs and supplying the growing market for drugs. The next hit is about all that many can ever hope for.

"Those who make peaceful revolution impossible will make violent revolution inevitable."

Your forsight is spot on I suspect the result will be ugly withmuch voter/buyer regret.

I remember back in uk early 1990,s the house price went down a huge amount at the time I worked in a bank my interest rate were low around 3% but the pound came under pressure and raised rate to 14% 15% a lot of my mates were just giving keys to bank. I think it was around 10 years to regain losses on houses. Sometimes it’s just bad timing if the same pressure was on nzd it would probably do same thing. It would be a mess as buying and selling houses is the big thing here. I know this pain sitting in negative equity can’t move know you house is only worth 60% of purchase price. All I say is young people need to think hard and don’t overextend yourself.

The RBNZ LVR restrictions and caps are non-sense and preventing people from becoming a first home buyer. More importantly, they should be enabling young kiwis to get onto the property ladder and build their own home and builders can build and this can drive the economy. Without this, everyone will be out of work and then the negative wealth effect would kick in and reduce discretionary spending.

Higher LVR restrictions would drive negative equity because the next buyer is unable to leverage up and transact at a higher price point. People feeling poorer would mean less discretionary spending and the real economy contracts.

That's a great post for expressing that the bubble must continue at any cost.

Higher LVR restrictions would drive negative equity because the next buyer is unable to leverage up and transact at a higher price point == ponzi

"enabling young kiwis to get on the property ladder"

Sounds like a well intentioned fantasy about 20 years too late...

So excited for the new Matrix movie coming out in December.

Such good timing with the way the world is.

The RBNZ has far more pressing things on their mind....like "The massive inequality they've caused by reckless monetary behaviour".

They need to put up interest rates where they should be. Collateral damage on the way down, won't be anything like the collateral damaged they've done to the non-asset owner community on the way up.

The good Orrd giveth, The good Orrd taketh away.

Putting pressure on FTBs always seems like trading one thing for another. We know that home ownership has manifold societal benefits from earning more, and therefore paying more tax, to better health outcomes and lower crime rates.

The implications are far greater than just financial stability but the view of Government and the Reserve Bank is myopic.

Ah, M. Reddell, the chap advocating for a deeply negative OCR....

Reddell and goodall are been quite disingenuous and frankly misleading in their commentary. I have little faith in either as both continue to prosper as a direct result of house prices rising - so their interest is to keep the party going.

What both Reddell and Goodall know is that the credit changes proposed by the RBNZ have little to do with FHB's and a lot to do with NZ's credit rating and as for unemployment - thats not the main reason why houses are forced to be sold.

1. Credit standards are been tightened primarily because the housing market is well into bubble territory and the RBNZ has been warned by both Standards and Poor and the IMF that its a major looming problem. It's extremely unlikely that a major financial stability crisis will occur where one or more of banks fail - but its highly likely that in the near future ( ie between 6-12 months) NZ's and NZ banks credit ratings will be downgraded if they allow the bubble to continue- resulting in much higher wholesale lending costs for the banks and the economy as a whole. This is not what either the government or the RBNZ want or need. The IMF and the various rating agencys have warned them - they will not give a second warning they will just start to downgrade the ratings.

Evidence of the above can be seen by

1. IMF warned NZ about its bubble on the 11th March- a week housing tax changes were announced

2. Standards and Poor warned NZ about its bubble on the 23rd June - 3 weeks later the RBNZ finally announced it would introduce DTI's, higher lending calculations and higher LVR's .

2. Unemployment is not the biggest risk associated with negative equity (and Goodall and Reddell- both know this) The number one reason houses are sold unintentionally - is divorce. Approximately 5% of all houses sold annually are a result of a marriage/ relationship breakdown. Divorcing couples with negative equity - dont just walk away having lost whatever savings they had put in as a deposit but can walk away with a joint debt that must be paid back. The results are devastating for both sides - whereby 8-10 years of scrimping can result in nothing to show for it and worse still without another partner little chance on one income of been able to buy another house.

Goodall and Reddell - know all of the above (after all both are economists) - but as I said there is a self interest for them to wring as much as they can out of the housing boom whilst they can.

Nice explanation.

I'm not sure what you mean about Reddell prospering from house price rises, as far as I can tell from reading his blog he has one house that he lives in and is as worried about his children being able to ever afford a house as most of us.

He opposes the RBNZ restricting lending because he's in the camp that wants all land use restrictions gone (like a lot of economists). And there's no doubt that would crash the price of land, but of course it would be terrible for the environment and sacrifice all our best food producing land.

Correct me if I'm wrong but is in not a bit late in the game now to be worried about this ? The massive lending has already been done and its clear from the powers that be that they are trying to let inflation bail us out of this mess. Simple really, high inflation, interest rates rise, wages rise, House prices increase, problem solved. Its worked before so what could possibly go wrong this time ? I mean apart from the fact we appear to be stuck on step 1 and nothing else is happening.

I don't care anymore. The whole system is just people trying to keep their six figure pay packets going for another cycle.

I think framing this as a way to avoid negative equity for FHBs misses the point. The goal should be to prevent bubbles by keeping prices somewhat in line with real incomes. If you don’t, you have no brakes on the bubble, because the ‘value’ of property as collateral is always rising, making every instance of leveraged borrowing appear perfectly safe even as systemic risk rises.

The only reason *not* to frame it this way is that you might have to admit we already *are* in such a bubble, with a huge value of ‘safe’ debt collateralised not by an uncorrelated and stable asset but by *more of the same thing*.

When the RBNZ removed LVR restrictions in April last year, they took it upon themselves to emphasise that they had proactively engaged with Maori and Pasifika groups to ask for feedback and that some had mentioned that their removal meant they might allow more first home buyers to purchase a home. It would be interesting to see if they have approached those same groups for feedback this time and if so what their responses were.

“The Reserve Bank received more than 70 submissions from members of the public and industry, expressing a wide range of views. The Reserve Bank also directly approached a number of NGOs - including Māori and Pasifika groups to make them aware of the proposed changes, and to provide them a chance to provide feedback on the proposals.

“Although the consultation period was short by the Reserve Bank’s typical standards, this was necessary to respond swiftly to an unprecedented set of economic events. The feedback raised a number of valid points and concerns which were all carefully considered.”

Views on the proposals were mixed, reflecting both the costs and benefits of borrowing restrictions.

Some submitters recognised that removing the restrictions might allow more first home buyers to purchase a home.

https://www.rbnz.govt.nz/news/2020/04/reserve-bank-removes-lvr-restrict…

"a borrower leaving their bank exposed by owing it more than their house is worth"

oh it's the borrowers fault... where's an emoji when you need one

'Questions raised over whether there's a case for the RBNZ to protect first-home buyers from themselves in the name of keeping the financial system as a whole stable'

100% True.

Thanks for raising it but it has to be hammered on every platform and medium for this so called messiah of the economy to understand.

Everything is done in the name to support economy and help FHB but reality is that one part of economy is getting a boost - that is speculative side (All decession maker be it in government, rbnz, bureaucrats, experts, media belong to and benifitting, also has as has power twist can and are manipulating to suit their vested interest) and all other economy and average Kiwi are been screwed.

You are bang on for FHB : Not having a house is frustrating and disappointing but buying by borrowing in extreme will be disaster even if situation changes slightly and also on well being as will be screwed as over burdened.

After initial lip service what is happening to DTI (Most FHB in Auckland are borrowing 7 plus times). Mr Orr has been wanting it since number of years and now that he has it (may be waa not expecting politician to give) why is he sleeping over it.

Re DTi - I 100% agree. After chasing it publically for years there is no sign of an Orr in the water on this.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.