Banks and other lenders are now under greater legal compulsion to ensure that the people borrowing from them can afford it.

Changes to the Credit Contracts and Consumer Finance Act (CCCF Act) came into effect on December 1, 2021.

In essence these rules put much greater emphasis on banks and other lenders getting more detail from would be borrowers about why they need the loan, their income and their expenses. And the lender is required to make sure the would be borrower can afford what they are borrowing.

So, in other words, if first home buyers want to borrow a large sum from a bank, said bank has to make much greater inquiries than previously about the FHBs' suitability and ability to pay.

The Commerce Commission says lenders "will no longer be able to rely solely on the fact that information has been provided by the borrower to show that they have made reasonable inquiries about the affordability and suitability of loans".

Additionally, lenders "must keep records demonstrating compliance with their obligation to undertake affordability and suitability inquiries".

Commerce Commission Chair Anna Rawlings said the new CCCF changes were "significant" and built on the existing responsible lending requirements.

"For borrowers, this change means more information will be gathered by lenders about the reasons why they need the loan, their income, and expenses. This information will enable lenders to properly assess whether the loan will meet the borrower’s needs and that the borrower can afford the repayments without getting into financial difficulty."

Rawlings said the changes were intended to better protect borrowers from taking on unaffordable debt and provide greater clarity for lenders when assessing loan applications.

"Lenders are obliged to help their customers to make informed choices when they are taking out loans. These changes to responsible lending requirements should help to deliver greater consistency in the provision of suitable and affordable loans to borrowers throughout the sector."

A range of other changes also came into force on December 1.

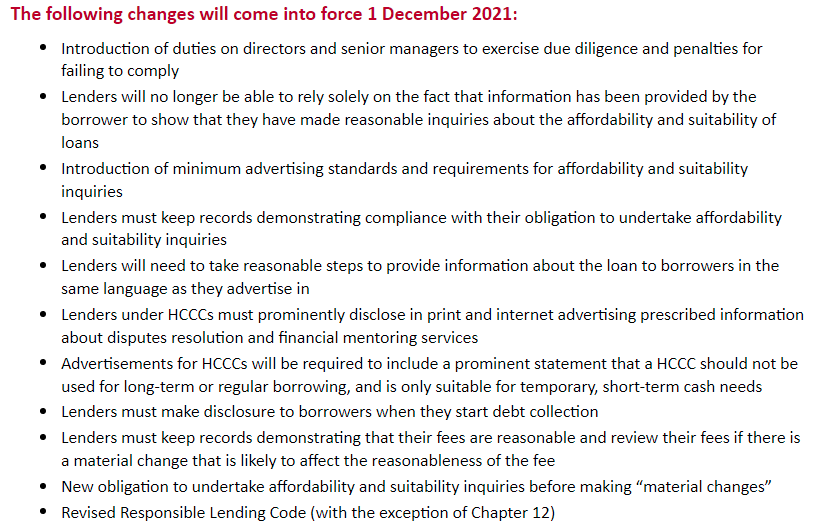

Directors and senior managers are required to exercise due diligence to ensure lenders comply with their consumer lending obligations. There is greater clarity about advertising standards for consumer loans and three new types of disclosure requirements have been introduced. Lenders must also keep records demonstrating that their fees are reasonable and regularly review their fees. Lenders may face financial penalties if they do not comply with their consumer lending obligations.

"The commission’s priority in recent months has been to educate lenders about recent changes to consumer credit laws and the changes coming into force today so they understand what is required of them and take steps to comply with their additional obligations," Rawlings said.

Below is a list from the commission's website of the new rules (note - HCCC refers to 'high cost' (above 50%) loans):

13 Comments

Don't worry about it bro.

Banks are stress-testing borrowers for interest rate increases up to 7% which everybody can afford.

Also, in other news, 90% of Kiwis don't have $1,000 in savings

but that's a different thing, so don't worry about it.

Households forced to shell out more on their existing large mortgages due to higher interest rates, while inflation takes bigger chunks out of their incomes and savings.

Then we have businesses shutting down at record pace, as reported by Stats NZ.

That number seems incredibly high. Got any sauce with that?

When people say bank stressed test borrower at 7% so it's ok. They forget the implication of the word 'stressed', how long can someone put up with constant stressed before giving in.

Pretty sure you mean 40%

https://www.stuff.co.nz/business/126800836/four-in-10-people-have-less-…

Doesn't really matter, 98.3% of statistics are made up to suit a narrative.

I welcome any additions to the financial landscape that will curb house prices without having to rely on OCR changes. Interest only mortgages and DTI next please. If Orr feels inclined in the next 12 months to reverse interest rate increases because of more variants, there needs to be adequate alternate measures to prevent another surge in asset buyers.

Banks already ask for bank statements, accounts, tax receipts, credit checks, credit card bills, pay slips etc.

At this rate people will need a colonoscopy to buy a new carpet.

Oh no. The banks actually have to do their job and the directors are liable if they don't. Who would have thought....

Like it or not, banks have been doing a pretty good job at determining who is credit worthy and who isn't for a long time. The banks are in it for profit. Giving out loans to customers who are likely to default is not good business, so it has ALWAYS been in their best interests to stress test customers and decline riskier lending.

These law changes make it so banks need to go through things to a much more extreme level which mainly serves to increase wait time for bank call centres and branch appointments and piss off borrowers for having to jump through a thousand hoops, all while the non bank lenders bend the rules and get away with it

"These law changes make it so banks need to go through things to a much more extreme level which mainly serves to increase wait time for bank call centres and branch appointments ...."

Or, banks could use their record profits to hire more staff to man the call centres or branches.......oh, but that would effect the bottom line.

Another way to slow the economy by increasing compliance cost.

Im glad im not a mortgage broker in this environment each loan will take forever to go through all the bank statements of each and every account and tie it all up to some solid monthly expendture especially when expenses change all the time. Cant really see this myopic approach reducing risk that much either especially for owner occupied borrowers. They want to hold their houses and previously you looked at their fixed expenses and ensured they had enough uncomitted income, now you have to itemise all the uncomitted income too. The big risk is loosing your income not spending too much on takeaways.

We recently refinanced and I have to say the process was majorly OTT. It actually pissed me off, feeling like I was grovelling for the privilege of paying them interest. I feel sorry for anyone trying to get a new mortgage now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.