Heartland Group Holdings, parent of Heartland Bank, has posted an 8% rise in interim profit to $47.5 million, helped by 14% growth in lending.

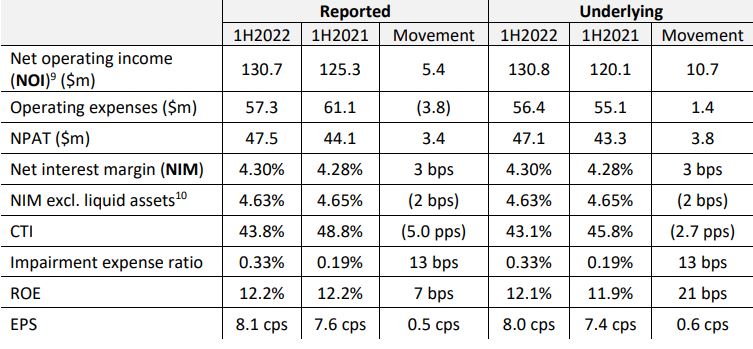

Heartland says net profit after tax rose $3.4 million in the six months to December 31, 2021 from $44.1 million in the equivalent period of the previous year.

"The first half performance included a pleasing annualised rate of growth in lending [of] 13.9% [to $5.358 billion]," Heartland says. "It also demonstrated the benefits of ongoing digitalisation, with a reduction in the cost-to-income ratio."

Heartland says operating expenses fell $3.8 million, or 6.3%, to $57.3 million, with the group's cost-to-income ratio down to 43.8% from 48.8%. Its return on equity rose seven basis points to 12.2%, and its net interest margin increased to 4.30% from 4.28%.

Heartland says its online home loans platform, launched in October 2020 offering market leading interest rates, had lent $218.5 million to 422 customers by January 31 this year.

"The ambition is for the home loans book to reach $1 billion of lending by the end of the 2023 financial year," Heartland says.

The group says growth will be assisted by a new intermediary partnership currently being piloted with NZ Financial Services Group (NZFSG) under an "Engage Home Loans" white label brand.

"NZFSG is the largest mortgage broker aggregator in the country, with a network of around 900 residential mortgage advisors. Rising interest rates motivated many home loan borrowers to review their mortgage providers, driving an increase in the volume of home loan applications received by Heartland. More than 7,840 applications were received during 1H2022 [the six months to December 31, 2021], an increase of 29.2% on the 6,067 applications received during 2H2021 [the six months to December 31, 2020]," Heartland says

Loan impairment expense increased $4 million, or 88.1%, to $8.5 million. Heartland says this reflects the benefit of post COVID-19 remediation activity in the equivalent period of its previous financial year, plus a return to more normal levels of asset growth and associated loan provisioning.

Meanwhile, Heartland says the introduction of changes to the Credit Contracts and Consumer Finance Act (CCCFA) and the Credit Contracts and Consumer Finance Regulations slowed growth in both vehicle and online home lending during January and February.

"This has the potential to impact on the growth rate for the remainder of the six-month period ending 30 June 2022. This is being partially offset by growth in other areas, especially reverse mortgages in Australia and New Zealand, and no material reduction in anticipated full year growth is expected," Heartland says.

"The introduction of new CCCFA responsible lending regulations in December 2021 has had an industrywide impact on decline rates, resulting in reduced lending volumes. The interrogation of activity in bank statements needed to satisfy the new standards has been well publicised and, amongst other things, has slowed down loan processing. Heartland is engaged with the Ministry of Business, Innovation & Employment and the Commerce Commission in explaining the impact of the changes on Heartland and its prospective customers, and awaits the output of the ministerial review currently underway."

Heartland's paying a 5.5 cents per share interim dividend, a 1.5 cents per share increase year-on-year.

Heartland says it expects June year net profit after tax within a previously stated guidance range of $93 million to $96 million, up from $87 million the previous year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.