HSBC, the first overseas bank to gain a banking licence in New Zealand, could be a high profile casualty of the Reserve Bank's proposals to make banks operating in New Zealand as branches of overseas banks quit retail banking.

The proposed changes could see HSBC having to either incorporate in NZ or quit retail banking. In a submission to the Reserve Bank HSBC says it supports the current policy and acknowledges it; "may need to substantially change strategy in response to such a significant change in the regulatory environment."

HSBC established a branch in NZ in 1987 becoming the first overseas bank branch to be registered here. HSBC operates in NZ as a branch of the Hong Kong-based Hongkong and Shanghai Banking Corporation Ltd, with its ultimate non-bank holding company being HSBC Holdings PLC of the United Kingdom.

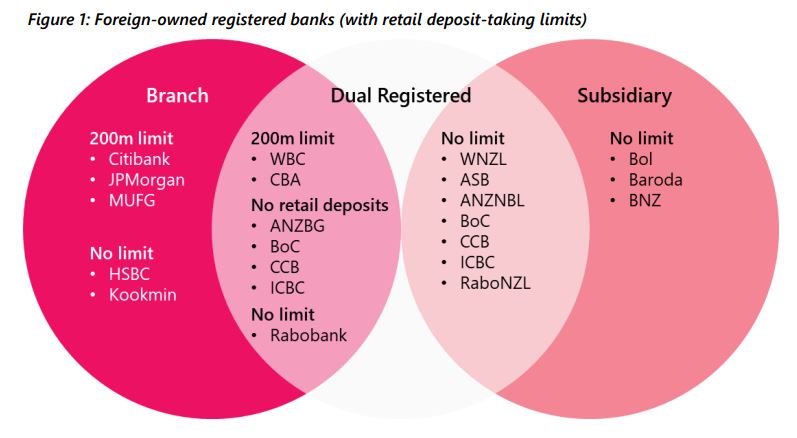

Overseas banks wanting to operate as a NZ bank can apply to the Reserve Bank to register as either a locally-incorporated subsidiary, or as a branch of the overseas bank. Albeit in some cases an overseas bank is allowed to register both a subsidiary and a branch, which is referred to as dual registration.

As the Reserve Bank puts it, the key difference between a locally-incorporated subsidiary and a branch is that the branch is part of a legal entity incorporated overseas. The branch operates its banking business in NZ, which is the host jurisdiction, but the legal entity of which it is part is incorporated in another country, which is its home jurisdiction.

"As a result, branches cannot be made subject to many of the requirements we impose on banks incorporated in New Zealand. We rely on a branch’s compliance with regulation and supervision in its home jurisdiction," the Reserve Bank says.

The Reserve Bank is reviewing its policy for branches of overseas banks, issuing the second consultation paper in this review last week. It's proposing that all branches of overseas banks operating in NZ be restricted to wholesale business with corporates, institutions and other wholesale investors, meaning they couldn't take retail deposits or offer products or services to retail customers.

"Our proposals would mean that a small number of branches would have to divest themselves of existing retail customers, and that none of them could compete for retail business, unless they decided to incorporate in New Zealand and become subject to the full extent of our regulation and supervision," the Reserve Bank says.

HSBC says such a move would be "detrimental and onerous, putting those bank branches at a disadvantage due to the resultant costs and other implications."

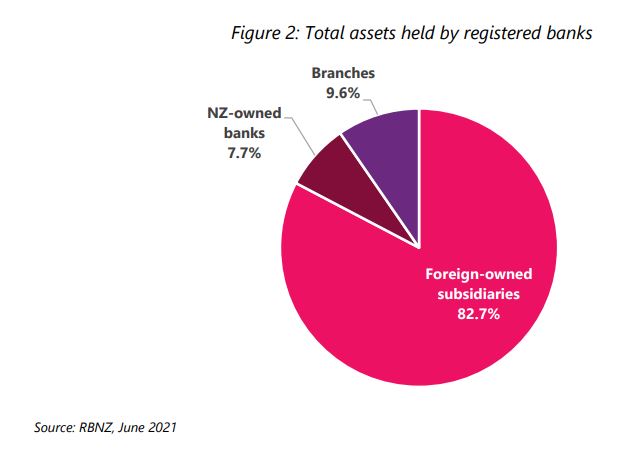

Branches hold 9.6% of the NZ banking system's total assets, although HSBC argues this includes both dual registered and non-dual registered branches.

'We are reviewing the recommendations and will respond'

HSBC is prominent among overseas banks operating in NZ via a branch. As of June 30 it had $1.8 billion of residential mortgages, and $4.4 billion of customer deposits. HSBC NZ's unaudited after tax profit for the six months to June was $15.8 million.

Interest.co.nz asked HSBC what it will do if the Reserve Bank follows through on its proposals. Might the bank divest its NZ retail business, and just focus on wholesale services? Or could it look to incorporate in NZ and become "subject to the full extent " of Reserve Bank regulation and supervision?

"We are reviewing the recommendations and will respond, so won’t speculate on the outcome. If there are changes, we will review how this will impact our model; however, we remain business as usual and very focused on supporting our customers and their banking needs," an HSBC spokesman told interest.co.nz.

In its submission to the Reserve Bank, HSBC says it supports the Reserve Bank's current policy framework, which it says isn't overly complex. The provisions set out in the Reserve Bank of New Zealand Act are "entirely appropriate" to manage the different branches in NZ.

"We do not believe that they are overly complex to implement. At the same time, having a flexible and tailored approach allows the Reserve Bank to look through to the different jurisdictions of those branches as well as other obligations imposed on those banks," HSBC says.

The bank says it's concerned that "a more rigid" set of policy requirements for branches might be envisaged, which would "either force banks to locally incorporate or change their business model for their branches."

"We see limited benefits for New Zealand: if changes are made to retail limits for branches, this would affect only a small portion of the New Zealand banking market since many banks are dual registered. If restrictions were placed on dual registration in addition by forcing all business activities into a subsidiary, it could significantly affect the diversity of the New Zealand financial system," HSBC says.

Ultimately HSBC suggests the justification for international banks to maintain an overseas branch presence in NZ could be undermined. Especially, it says when "modest scale and specialised nature of business models may offer relative few opportunities over which to amortise the additional cost of operations."

HSBC notes "a considerable number" of its NZ retail customers bank with HSBC in multiple jurisdictions, saying "almost half of our retail portfolio bank overseas." Its wholesale customers are generally multi-national corporations and large corporates looking to do business in NZ or do business overseas from NZ.

HSBC says if it could no longer support retail depositors in NZ, this could potentially have a detrimental impact on their financial wellbeing.

"Removing the ability of a branch to provide services to retail customers will also reduce competition, lessen the choice for consumers and make it harder for international customers to have a seamless banking experience," HSBC says.

It supports the current threshold for local incorporation which is required when an overseas bank intends to have more than $15 billion in net liabilities. At June 30 HSBC NZ's total liabilities were $7.6 billion.

"We consider this control, when combined with specific reforms to deposit protection, is adequate and proportionate to other jurisdictions."

*Figures 1 & 2 below come from the Reserve Bank. It's seeking submissions on its branch review by 5pm, November 16. (See our story on the Reserve Bank's first consultation paper in this review here).

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

10 Comments

When I hear HSBC, I think laundered drug money.

Fond memories?

Westpac and ANZ don't exactly have a clean history

HSBC is genuinely a challenger bank in the home loan space. It would be unfortunately if they picked up sticks.

I dont actually understand what the the RBNZ is trying to achieve here with this move - it feels quite anti-competitive.

If the move is to protect bank customers from bank failure- then capitalisation rules and - ultimately putting in deposit protection laws would protect the customer

If its for transparency and to stop money laundering - again laws can be implemented to protect against this - licence to operate regulations would be a lot simpler than making overseas companies incorporate.

this feels very much like a solution looking for a problem - and in NZ this ultimately has done little to support the common man - building, petrol and supermarkets are all good examples of this.

The reasons are fairly technical but if there is a problem with an offshore bank then there is greater potential for cross-contamination to the local branch than via a subsidiary. When things get tricky, you can be sure that the NZ depositor and taxpayer will be ranking behind the overseas regulator's or even management and shareholder's interests and hence an NZ incorporated company offers better protection against those conflicting interests. Local director liability to act in the best interests of the NZ company might also strengthen bank balance sheets.

I don't think that NZ incorporation would deter banks from competing in NZ retail but they might prefer to act as a branch and raise objections to it (as Westpac did). Subsidiary funding issues should be resolved by an issue of an irrevocable guarantee from the parent.

Anti competitive are not incorporated branches. They have an advantage over the incorporated ones as they can avoid some of the expenses of local obligations. As they have said in the article...these NOT incorporated branches are not able to be FULLY subjected to many of the banking regulations and laws of New Zealand. Staff and customers can be left without legal recourse for failures of their main entity outside New Zealand. It also means they can take all their revenue offshore and avoid tax in New Zealand.

It is getting difficult to separate this inept management of the RBNZ from our inept Government. Both incompetent, ideologically driven, woke, incapable of listening and of understanding that competition is actually good to the consumer, running away from real problems while trying to find solutions to problems that do not exist. What a pathetic s..tshow.

Having worked for a subsidiary of a major international bank, offshore, the biggest impediment we found was when we went to transact a deal, say borrowing funds, the first question that invariably was asked was : "Are you a Full Branch of (one of the Top 10 Global banks at the time)?".

Our reply being "No. We are a wholly owned subsidiary" was often met with a response of "In that case, I'm sorry, we can't help you".

Exactly, often a full branch is viewed as a better credit as an offshore bank will have a relationship with the bank already. This will drive up funding costs of locally incorporated banks as offshore lenders will not want to process and maintain credit lines for a minor bank in NZ.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.