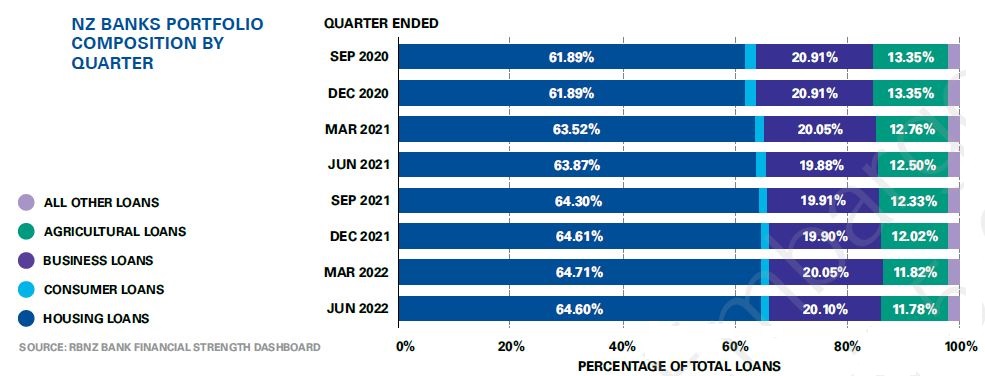

Housing loans as a percentage of New Zealand banks' total lending fell in the June quarter, albeit only slightly.

KPMG's June quarter Financial Institutions Performance Survey (FIPS) shows housing comprised 64.60% of NZ banks' total lending at the end of June, down from 64.71% at the end of March.

The drop bucks the trend over the Covid-19 period, during which housing has surged as a percentage of total bank lending. At the end of September 2019, housing loans comprised 59.33% of total bank lending. (Interest.co.nz also spoke to ANZ NZ CEO Antonia Watson about the rise of housing loans as a percentage of ANZ's total lending here).

Business lending increased as a percentage of total bank lending during the June quarter, taking it back to levels not reached since 2020. Business lending comprised 20.10% of total bank lending at June 30, up from 20.05% at March 31.

Reserve Bank sector credit data shows total housing lending up $3.721 billion, or 1.1%, to $339.412 billion during the June quarter, with business lending up $2.81 billion, or 2.2%, to $128.535 billion. Personal, consumer lending fell $147 million, or 1%, to $13.306 billion.

Meanwhile, the FIPS shows combined net profit after tax across the banks of $1.73 billion in the June quarter, only just lower than the record high $1.74 billion recorded in the March quarter. KPMG notes the highest net interest margins in three years as a "highlight," with net interest income across the banks up 7.6%.

"The net interest margins of the big five banks were each the highest that they have been since at least June 2019 with increases of approximately 10 to 30 basis points between March 2022 and June 2022 alone. This may be due to more borrowers rolling off their historically low fixed interest rates and onto longer term higher interest rates which have priced in future increases in the OCR," KPMG says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

3 Comments

RBNZ claimed around two-thirds of households have no mortgage debt, but nearly 40 percent of new mortgage loans are to borrowers with DTI ratios above five, in the May 2019 FSR - page 7 (13 of 48) PDF

KPMG's June quarter Financial Institutions Performance Survey (FIPS) shows housing comprised 64.60% of NZ banks' total lending at the end of June, down from 64.71% at the end of March.

Such a high level of lending concentrated on around one third of already wealthy household borrowers poses high risk levels to those creditors underwriting the bulk of these collateralised loans.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Be nice to see current debt concentration. Would show just how effective those interest rate increases are actually going to be...

If we take 1/3 of the population having mortgages, and 2/3 of mortgages being half average rent and paid several months ahead (as reported by both ANZ and Westpac), then that leaves the vast majority of high DTI loans requiring servicing in the hands of a very small number of people...

This is going to be a case study for future generations, I'm sure.

Housing Lending down should be a good sign that average person is being cautious specially when worse is yet to come as suggested by all data/news not only in NZ but around the world.

It is pity that many mum and dad who helped with their equity are or will be in negative and should be a learning to not use your equity/saving tat may break or make you near to retirement age.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.