A union for bank staff says New Zealanders are enduring “higher rates of profit extraction” from our banks and there should be a 5% levy on bank profits.

First Union said a levy on excess bank profits could have raised more than $300 million in revenue in 2022.

The union said in a press release that it also supported an enquiry into bank profits.

Commerce Minister Duncan Webb has said no decision has been made on a banking market study by the Commerce Commission, but it is widely expected one will be announced.

First Union, which represents bank workers, said an excess profits levy could be used to fund the establishment of a Ministry of Green Works.

The bank profit debate got new life this month after KPMG released its annual survey of the sector which found the banks made more than $7 billion profit for the first time.

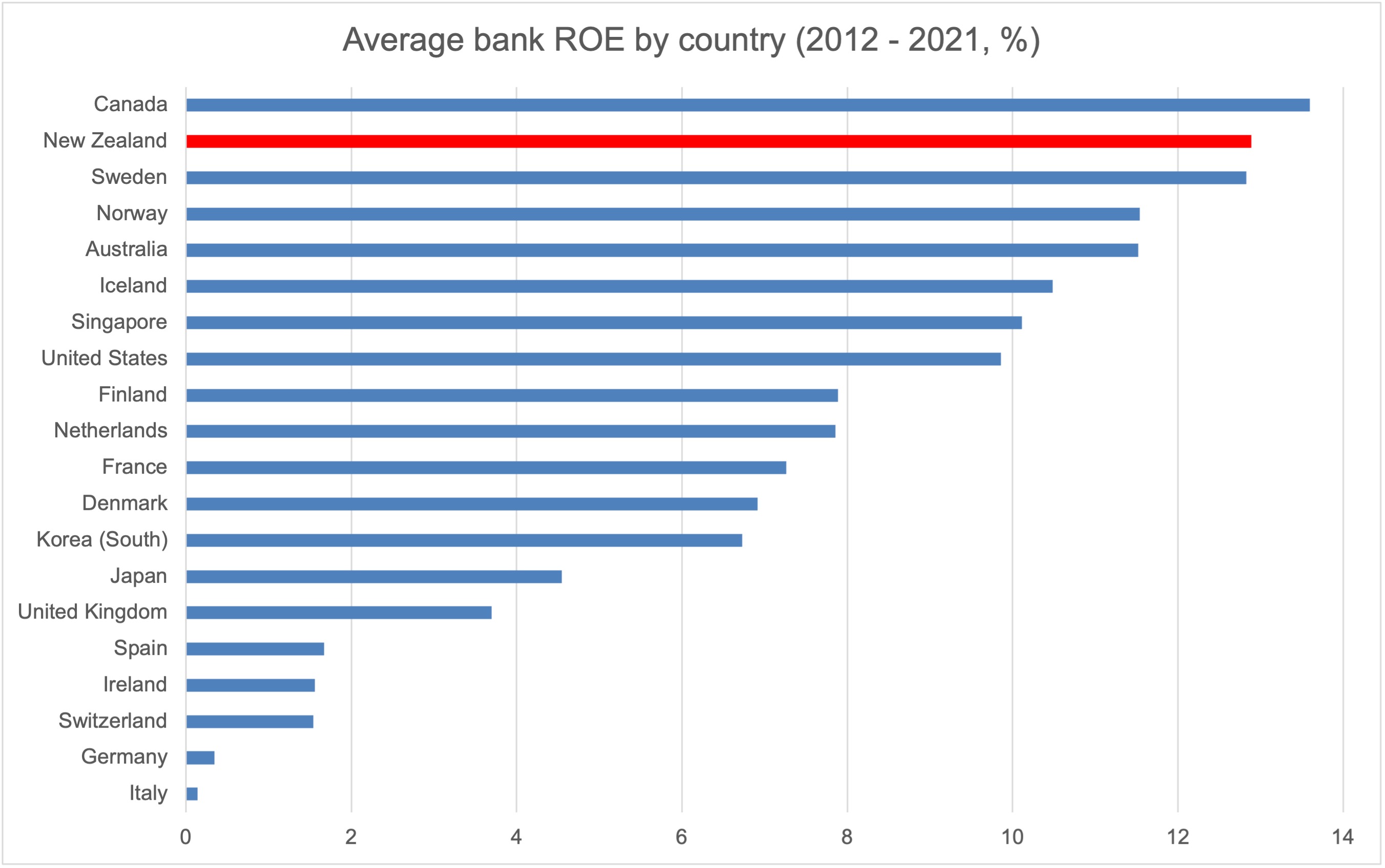

First Union researcher and policy analyst Edward Miller said that a decade’s worth of data showed New Zealand banks’ returns on equity were among the highest of comparable countries. (See First Union's chart below).

"While the big four banks’ 2022 return on equity figures clearly trumped those of their Australian parents, our analysis of World Bank data shows New Zealand banks have some of the highest return on equity figures in the developed world.”

New Zealand’s banking sector is dominated by the Aussies, with about 90% market share held by ANZ, BNZ, ASB and Westpac.

Miller said bank profits are extracted from New Zealand communities.

“It is unclear why we have to endure higher rates of profit extraction than Australian, British, Dutch, Japanese or Spanish citizens."

The return on equity of the NZ banking industry was 13.4% in 2022, data from the World Bank showed. Only Canada’s banks were more profitable.

There have been growing calls for a deep dive into bank profits and competition in the sector, including from anti-monopoly campaigner Tex Edwards. The Green Party has also called for a levy on bank profits.

Green MP Julie Anne Genter last month said; "A 10% levy on the banking sector’s record profits would raise over half a billion dollars which could be used to support people."The New Zealand Banking Association has previously said this was a matter for the Minister.

New Zealand Banking Association chief executive Roger Beaumont said bank profits look big because banks are among New Zealand's biggest companies.

He said New Zealand's banks were profitable, well-regulated and resilient, and that was important in the current economic climate.

“Last year banks made a net contribution to our economy of $1.92 billion. They spent $9.1 billion running their businesses and paying tax in New Zealand, compared to combined profits of $7.18 billion ... Our banks’ average return on equity is 13.4%, which falls in the middle of the pack when compared to other major New Zealand companies."

The Commission has completed market studies into residential building supplies and the supermarket sector. The Banking Association has previously said a market study into banks was a matter for the Minister.

39 Comments

The banks are enjoying a good time at the moment, but bearing much more risk down the road.

Yes if you look at that graph the countries with the biggest returns for banks have been in the countries with the biggest housing bubbles. surprise surprise

As the housing markets in the same countries continue to slump, the banks will need to be financially robust to survive.

UK had a housing boom over that same period.

be interesting to understand where the bank profits 'really' go.

The bankers and board will take a big chunk in salaries and bonuses but surely the balance goes to shareholders which presumably is some high net worth individuals that we dont know about... but i reckon somehow the biggest haircut would be taken by our kiwisaver and supperannuation funds. a suspicion that we lose on the way up and on the way down - and the rich somehow win all the time?

paying a bigger tax is one idea - but surely a better one is to cap their margins somehow - else we pay over the odds for something and pay a tax on the extra money (which will probably end up being on top of the already high fees... and then. the tax wasted by the govt. i would rather keep it in the first place and save everyone the extra cost of paying and collecting the tax and wasting it

If they are making super profits are they not paying super tax on the back of that...?

who determines what excrss profit is and is it only banks making it?

what happens if a nz owned bank starts making "excess profit"

If we live in a fair and equitable democracy then surely any percentage profit above the percentage increase they give to their lowest paid worker should be considered in excess.

I can't help but feel banks would just pass on even more cost to customers and margins would sit pretty much exactly where they are.

You know, because they can.

Juist like all of the minimum wage increases over the last 10years

Yeah , all those bankers on the minimum wage.

Perhaps I wasn't specific, what I meant was the increases in costs passed on by employers consistently forced to increase pay for staff in many unskilled jobs. Resulting in this eating into the middle income earners, and winding up with the minimum wage workers having same purchasing power not long after the increase due to the increase in goods and services resulting from said increase, further resulting in minimum wage workers asking for more money and the cycle continues.

Or you increase supply so that demand doesn't outstrip it, then bingo no price inflation.

Why is it so hard for people to see that as the solution to inflation?! or are those neoliberal talking points wedged so deep in everyones brains from the moment they are incorrectly taught the concepts of money that it interferes with their cognitive abilities?!

(wink wink nudge nudge), employers deliberately keep supply tight (much like their recently discovered land covenant shenanigans) so they have an excuse to monopolise their market, while keeping prices rising and extracting the greatest profit.

It's really not that hard when you exercise a few brain cells a little is it! Or maybe it's just mass capitalist psychosis creating deliberate ignorance.

Has an arbitrary profit levy ever actually fixed a non-competitive industry ?

We have a fully functional not-for-profit retail bank (Co-op) which most people avoid because they’re too lazy to leave whatever bank their parents helped them open an account with when they were 12.

The super profits have occurred because we have been unusually desperate to enter a transparently overpriced property market at any cost.

We’re idiots and we deserve to get fleeced.

We ran our personal and business finances through Co-operative Bank for 4 years. Left when they cancelled the 2020 payout, then still made record profits.

From a personal banking perspective, Kiwibank beat them hands down in terms of both fees and features.

From a business banking perspective, they had fantastic support, but the systems were too primitive - e.g., couldn't give a company director read-only access to the accounts. They also took zero risk on lending - you either had a property or a TD equal to the value you wanted to borrow - they wouldn't lend on either cashflow or contract (I don't know how this compares to other banks, mind).

Overall, despite the yearly cash-back, they were more expensive than the other banks.

A bit harsh on Co-op Bank given they were following an RBNZ directive at that time; - https://www.interest.co.nz/banking/104468/co-operative-bank-says-it-wont-be-paying-customer-members-rebates-year-following-rbnz

A fair point, but note the "subsequent announcement from the RBNZ" - they had already decided prior to directive. I don't recall the directive having been issued at the point they notified us, but I recognise that doesn't mean it hadn't.

We don't have a mortgage, and they simply weren't competitive enough. We've saved $440/year on bank fees since, rebate taken into account.

But the staff were great to deal with (even when they gutted all their branches and made it appointment only), and if you were willing to travel, the Botany Downs branch was open on Saturday mornings.

Amen to that..

Dont these people read? We should be celebrating having highly profitable, stable banks. Thank goodness we arent facing the contraction the under-regulated US banks will undertake

The govt should encourage a nz listing of the big 4 Australian banks in Nz. It's doable as all are regulated to be able to operate independently of their Aust owners in NZ. I expect all have considered the possibility of NZ listing to deepen their nz connection and equity base.

Very good points. The NZ sharemarket (and NZ capital markets in general) is way too small and it would be greatly beneficial to expand its presence in the banking sector.

They might need the cash!

NAB says hybrids down 15pc....Loss Absorption. Conversion or Write-Off may occur at any time due to the occurrence of a Common Equity Trigger Event and/or Non-Viability Trigger Event.

Is return on equity or assets a fair measure when one compares performance say a power generator company with a bank?

A power company has huge investments in brick and mortar - real stuff.

The banks assets are largely digital are they not? Created from thin air. So this claim by banks about their returns not being out of the ordinary are a load of nonsense. Comparing apples with oranges.

Not my area, so perhaps i misunderstand.

Yes, you have misunderstood what a bank is, where the money from, and how money being created.

I think Rastus is quite close to the mark.

Just means your are both wrong, sorry. Banks have massive assets, largely loans for homes and busiesses. They are no more or less digital than any other business, apart from the very rare ones that hold physical cash. They are certainly more "real" than real estate and plant.

As we are seeing at the moment, equity is key to stability and ROE is a key measure, along with ROA. Banks have an ongoing tension between holding enough equity to remain stable in volatile times, and thinning their equity down to increase the ROE.

Banks have massive assets, largely loans for homes and busiesses.

We are both aware of this. Their "assets" are "debt obligations". The point is that these debt obligations are not based on banks being financial intermediaries as most people believe they are. Now your response may be "whatever", but if we also consider that global debt is 3-4x GDP, you should be able to understand that debt obligations are far beyond what is being "produced".

Also, commercial banks don't just create debt "out of thin air". They also create fictitious deposits when they do so. Those deposits are not the transfer of money into a bank.

...but the equity they created was due to inflating the money supply and making a $200k home now $1,000,000. They didn't build it, just created credit to create their 'asset'.

People buy into the magic money paradigm as the enlightened path to creating wealth perpetually. They are blind to the weaknesses of the method.

I think you have misread Rufus comment

I know how money is created - but you don't need a 20 year plan and move a zillion tonnes of earth, pour zillion a tonnes of concrete. You type on a keyboard.

there is a lot of things to be done before you can press that button.

A union for bank staff says New Zealanders are enduring “higher rates of profit extraction” from our banks and there should be a 5% levy on bank profits.

This is not good. A business whose foot soldiers fundamentally disagree with the outcomes / value they're delivering to customers and the wider public.

What does the top brass think? Do they think the foot soldiers might be better off working in a different industry? Do they think the wider public has to accept the trade off between high bank profits and the ability to create perpetual property bubbles through credit creation?

Nz Banks "profit extraction" is mostly about efficiency, including a more aggressive digital transformation, and low loan loss rates. Simply applying extra tax to mop up profits is a horrible precedent. Nz banks are already taxed on profits. We have the most inefficient, ineffective government in our history, and no surprise they and their fellow travelers want to raise taxes in preference to replicating that efficiency.

Banks "profit extraction" is mostly about efficiency, including a more aggressive digital transformation

Would you care to explain with examples?

Nz banks cost to income ratios are low and return on assets/equity are high because of several factors

- the geography ...lots of small towns over an extended archipelago provided a challenge to service. The solution was thar small town and suburb branches were extensively replaced by electronic banking and depowered agencies with reduced sevice levels

- bank cooperation in eftpos and other interbank transactions led to more widespread adoption of electronic transaction, much earlier

- apart from that cooperation, there has been pretty intense competition. Four players, each defending a solid market share operate quite differently to a lesser number - say supermarkets.

- the huge volume of house and farm lending creating loan volume and income, diluting the cost base.

Where do they want the levy to go.

I have an interest in Westpac, NAB, Comm Bank and ANZ. And am pretty happy with how NZ banks are doing. What I think should happen is that all employees and officers of Unions should have to pay a 20% levy over and above what they pay in tax. It could be called a "parasite levy".

LOL.

Great idea. But as a name, "parasite levy" is going to need some tweaking from a "lets do this" point of view.

Great article Rebecca ! Well done.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.