New Zealand's banks' combined annual profit surged by more than $1 billion, topping $7 billion for the first time, according to KPMG's annual Financial Institutions Performance Survey (FIPS).

It's an outcome likely to add fuel to the fire amid calls for a probe into bank profits and competition, with drums beating for a Commerce Commission market study. Additionally the FIPS shows the big four banks - ANZ NZ, ASB, BNZ and Westpac NZ - saw their combined market share slip only slightly year-on-year to 90.05% from 90.39%.

The banking sector's net profit after tax rose $1.06 billion, or 17.3%, to $7.18 billion. The annual FIPS covers 20 banks over the period between October 2021 and September 2022.

Net interest margin rise boosts profit

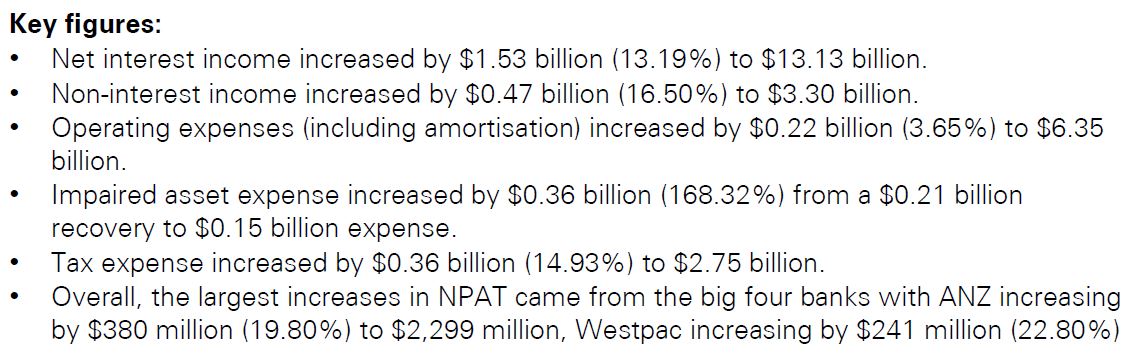

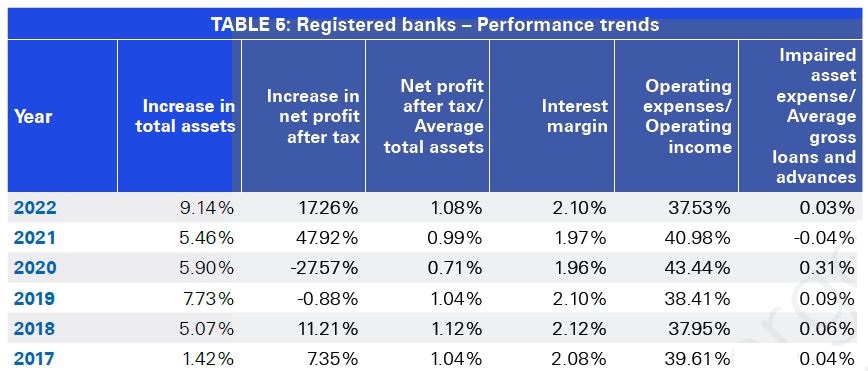

KPMG notes the key to the profit rise was a $1.53 billion lift in net interest income. This was driven by a 13 basis points increase in net interest margin to 2.10%. A $28 billion, or 6%, rise in gross lending to $503.3 billion, and a $470 million, or 17%, increase in non-interest income to $3.30 billion, also helped.

This year's annual profit rise was lower than last year's $1.99 billion, or 48%, increase that took combined net profit after tax to $6.13 billion. However, last year the increase was bolstered by a $1.69 billion reversal in impaired asset expense following big loan provisioning from lenders in 2020 in the early days of the Covid-19 pandemic.

"The banks have enjoyed a very good year," John Kensington, KPMG's Head of Banking and Finance, says of the latest annual FIPS.

"This is on the back of controlled loan growth and margin expansion. The banks have positioned their businesses to benefit in a rising interest rate market, and their prudent lending policies have continued to allow them to report very low loan losses," Kensington adds.

During the period covered by the FIPS the Reserve Bank increased the Official Cash Rate from just 0.25% to 3%. Over the same time period the average interest rate on popular two-year bank mortgage rates rose to 5.47% from 3.052%, and the average interest rate paid on six-month term deposit rates rose to 3.35% from 1.12%.

Kiwibank gains market share, ANZ loses it

Among the major banks the FIPS shows Kiwibank enjoying the biggest market share increase, up 22 basis points to 5.19%. Conversely ANZ NZ's market share fell the most, down 27 basis points to 27.62%.

Banks' funding costs rose for the first time in five years, up 26 basis points to 1.35%, thanks to the rising interest rate environment.

The FIPS notes that whilst banks returned to an aggregate impairment expense this year after the largest impairment recovery in the survey's history last year of $213.43 million, it was still the second lowest level of loan impairments reported since 2006. However, KPMG suggests some banks could be reconsidering whether some of their loan provisions, raised during the Covid-19 pandemic remain needed over the next couple of years.

Past due, but not impaired assets, increased $215.15 million, or 22.2%, to $1.18 billion. And the sector's cost to income ratio fell 345 basis points to 37.53% as operating income rose 14%, or $2 billion, well ahead of the 4.3%, or $250 million, increase in operating expenses.

Over the next couple of years Kensington predicts; "flatter [bank] earnings and higher [loan] impairment growth than we've seen for some time."

This comes with the Reserve Bank acknowledging it's deliberately trying to engineer a recession in order to get inflation down from above 7% to its target range of 1% to 3%.

Of the 20 banks included in the FIPS, 16 recorded an increase in profit. The four outliers were JPMorgan Chase Bank, The Co-operative Bank, TSB Bank and MUFG Bank.

It's the 36th year KPMG, an auditing and financial advisory firm, has undertaken the FIPS.

*The 'key figures' and table below come from the FIPS.

17 Comments

Higher company tax for all companies earning over 1million.

What a foolish knee-jerk thing to say

Tell Australia that.

All at the expense of hard working New Zealand savers.

Indeed:

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

I guess the SVB precedent set in the last 48 hours guarantees the return of all depositors' currently unsecured credit in the event of a bank solvency crisis. Does this mean even lower deposit rates?

yet when assessing risk, what is there to inform potential depositors of the bank's current business practices, that is not time consuming and mind bogglingly complex to the average person not educated in banking business and practices?

Better to write into law that depositors funds are the property of the depositor, and must be secured by the bank in the process of its business practices.

Could always check out the professionals at the rating companies.

Well I thought it was funny.

Also serious sarc

I agree. I continue to hope that the Pollies will one day act in the interest of their constituents. I guess that could be comedy or sarcasm too.

Hey leave our poor bankers and supermarket owners alone.

Anyone would think there was a growing rich poor divide, kids who can barely afford to eat , climate emergency or a infrastructure or cost of living crisis... that by taking unregulated obscene profits the rich are causing social issues and suffering.

Elite rich people have feelings too you know (allegedly)

If you want to fix supermarket supernormal profits you need to substantially increase competition (more permissive planning than RMA, rather than the less permissive planning it looks like we're going to get).

If you want to fix banking supernormal profits you need the yield curve to not bounce around as much + regulatory barriers to competition removed. Payments NZ and RBNZ both act in ways that reinforce the oligopoly.

Also the yield curve bouncing around bit cuts both ways, better our banks position themselves well for a rising rate environment so their profits are growing, than position themselves very poorly for it (like SVB!) and fall over, taking our unsecured deposits with them...

I always find it strange when people rail against those making monopoly profits, rather than the cause of those monopoly profits. You should say kudos to the supermarket owners and bank shareholders for making smart investment choices and batter down the door of your local MP for failing to act on the matter/protest at parliament.

But they didn't share the love.

Depositors (or, "investors" as we are deemed in our terms and conditions), have been left high and dry, not having been offered higher rates.

And as investors in a bank, we are unsecured creditors. Worth remembering.

This is a timely article when news wires are reporting a flurry of bank runs which is being downplayed by our msm...and understanderably so!

If only there was a government controlled bank that could keep the other's honest...

This from the KPMG banking report sheds no light. They could have done some worthwhile comparisons, that eg didn't exclude the lossmaking NZX companies, that left off the ROAs (as they say, meaningless across industries), & looked at say 10 years of data, mean and variance. Link

Pretty clear front loading of interest rate rises there...

You don't get massive profits by not increasing the spread between cost and sell interest rates

Banks work really really hard for their money . Commenters have no justification for throwing brickbats.

A question that came up at the end of National radio's Morning Report this morning. (sort of )

when they talk of a banks total assets , does that include depositors funds,wether it be everyday funds , or term deposits etc? Shouldn't that be a liability ?(i.e they owe that money to depositors)?Mortgages been an asset , but how much of a mortgage is the banks actual funds , vs depositors funds , or lent from another institution?

At a moment when banks are failing around the world due to high interest rates, lets make our banks even structurally weaker. What a great idea! When one of them goes belly up and 1/4 of NZ households and businesses lose all their money, what happens then? Does the NZ Govt have enough money to "backstop" 1/4 of all deposits? If no, then why would you still keep your money in the bank? Something to think about, and if you think "that won't happen here" then you are quite likely going to end up not being prepared for when it does. And don't think that you can quickly get your cash out, unlike the rest of the world, NZ does not have real time payment processing - so all your internet banking transactions will fail to process in time, and you'll go down with the bank.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.