Credit rating agency S&P Global Ratings doesn't anticipate the Commerce Commission's market study into retail banking competition will cause New Zealand's big four Australian-owned banks any significant drama.

The competition regulator's study is focusing on deposit accounts and home loans.

In a new report S&P's Melbourne-based credit analysts Lisa Barrett and Mark Symes say they expect the structure of the NZ banking industry to remain stable and dominated by the four Australian-owned banks, - ANZ NZ, ASB, BNZ and Westpac NZ. Barrett and Symes don't believe any initiatives introduced by the Commerce Commission through its competition probe will materially affect the major banks' market positions or their profitability.

"The four major banks, all rated AA-/Stable/A-1+ [see credit ratings explained here], have long dominated the banking system. As of June 30, 2023, they held a combined market share of more than 87%. The next largest bank in the country, the government-owned Kiwibank, had a market share of 5.2% as of the same date."

Barrett and Symes note NZ's big four banks are among the most efficient in the world, with only banks in Norway more efficient.

"The preference of New Zealanders for digital technologies, particularly for payments, supports bank efficiency. The cost structures of the Australian-owned New Zealand major banks benefit from the services they share with their parents. These are largely services outside the Reserve Bank's Banking Standard 11 outsourcing requirements."

"The average cost-to-income ratio for the New Zealand major banks was 37.7% over the past five years, lower than their Australian parents' 44.7%. We expect the Australian major banks will continue to support the cost structures of their New Zealand subsidiaries, allowing them to continue to provide dividends to the group," S&P says.

A cost-to-income-ratio of 38% means a bank spends 38 cents to generate $1 of earnings.

Call for greater financial literacy possible

Barrett and Symes say the competition inquiry could "moderately enhance" the competitive position and profitability of non-major banks.

"One possible outcome is a call for greater financial education and literacy for bank customers. This could increase customers' awareness of the differences in bank product pricing and financial management in general providing more impetus for customers to shop around."

"While we understand that it is not difficult to switch banks in New Zealand, in July 2021, the government decided to establish a consumer data right (CDR) framework in the country. In August 2022, the government agreed to explore banking as the first sector to be designated under a CDR. Work is now under way on the design and cost of the CDR," S&P notes.

"CDR should result in the creation of products and services that help increase competition. This could in turn could benefit customers by prompting lower prices and improved products. In theory CDR (or open banking as it is known in Australia) increases competition by giving all accredited parties access to the proprietary data that banks hold."

"This in turn could accelerate the rollout of technology to consumers by making it easier for fintechs and banks to develop customized and data-driven products. It could also make it easier for customers to switch among financial services providers. However, the rollout and take-up in Australia and the U.K. has been drawn out. We do not expect New Zealand to be any different," Barrett and Symes say.

Proportionate regulation

S&P goes on to say that smaller, less well resourced banks and financial institutions are at a competitive disadvantage against bigger entities in meeting the same regulatory requirements. It says the Reserve Bank recognizes this and applied proportionality in its 2019 bank capital review.

"Under those requirements systemically important banks [ANZ, ASB, BNZ and Westpac] are required to hold capital equal to 18% of risk weighted assets (RWAs) by July 1, 2028. Whereas all other banks will be required to have total capital equal to only 16% of RWAs."

"The Reserve Bank is also consulting on proportionality within the recently enacted Deposit Takers Act. In it, the Reserve Bank proposes three groups of deposit takers based on total asset size--banks with more than NZ$100 billion; those between NZ$2 billion and NZ$100 billion; and those less than NZ$2 billion. It also proposes three possible variations to prudential requirements for each group--variations included in the design of individual standards, bespoke variations for individual deposit takers, and opt-in to higher prudential requirements," say Barrett and Symes.

"To level the playing field, the regulator could continue to apply proportionality across other regulations. This would ease the regulatory burden for smaller banks without compromising their soundness or the financial stability of the broader New Zealand banking system."

However, Barrett and Symes believe it'll be hard for smaller competitors to make any material market share gains against the big banks due to the pricing advantage the major banks have.

"Smaller players provide customers an alternative to the Australian-owned major banks in the provision of banking products and services.

However, their competitive advantage will remain limited because customers are generally indifferent to who provides their banking products and services; they tend to focus more on price and turnaround time. As such, these smaller financial institutions will remain susceptible to the pricing power of the major banks, which benefit from greater scale and lower cost operating structures."

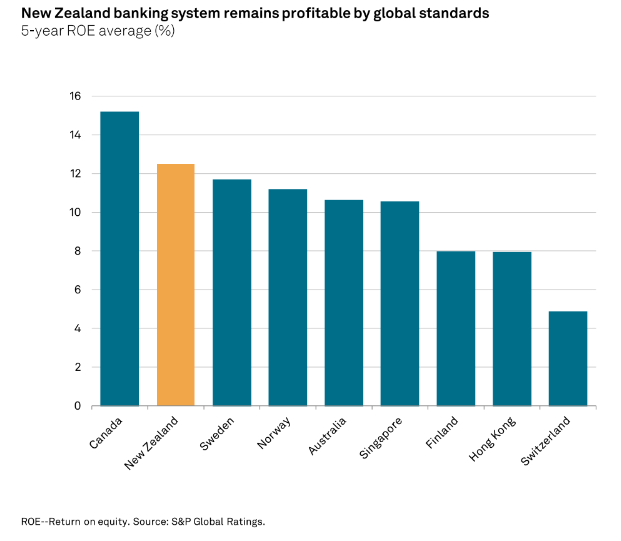

S&P expects the big NZ banks' return on equity (ROE) to remain high relative to similarly structured global banking systems that are weighted toward retail lending such as residential mortgages.

"Despite the high equity levels of New Zealand banks, the ROE for the banking sector has averaged 12.5% over the past five years. This is near the top end of international peers, including Australia," Barrett and Symes say.

The Commerce Commission is seeking feedback to its preliminary issues paper by 4pm on Thursday September 7.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.